Michael Vi

1. Introduction

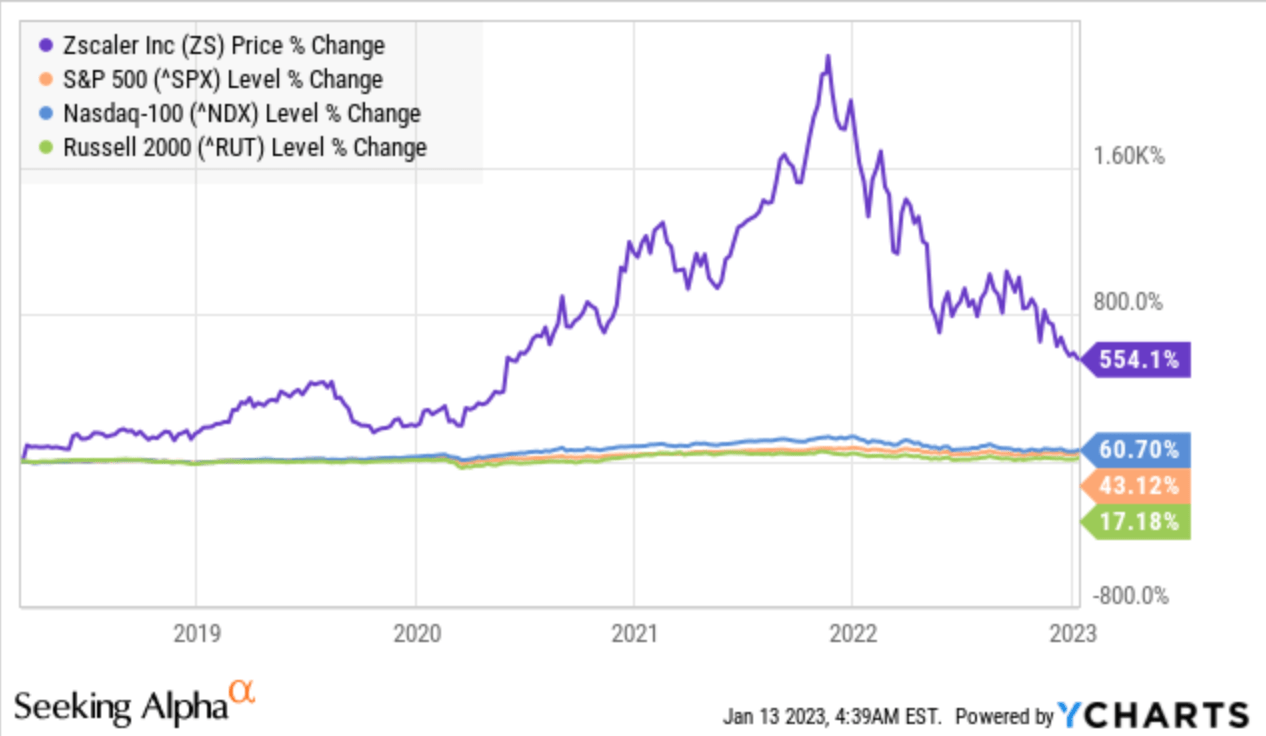

The current shakeout on the stock market has particularly affected growth stocks – One of them is the cybersecurity company Zscaler (NASDAQ:ZS), which temporarily delivered insane returns of around 2,000% for its investors after its IPO until the end of 2022 (see chart).

ZS price % change since IPO vs major indices (YCharts)

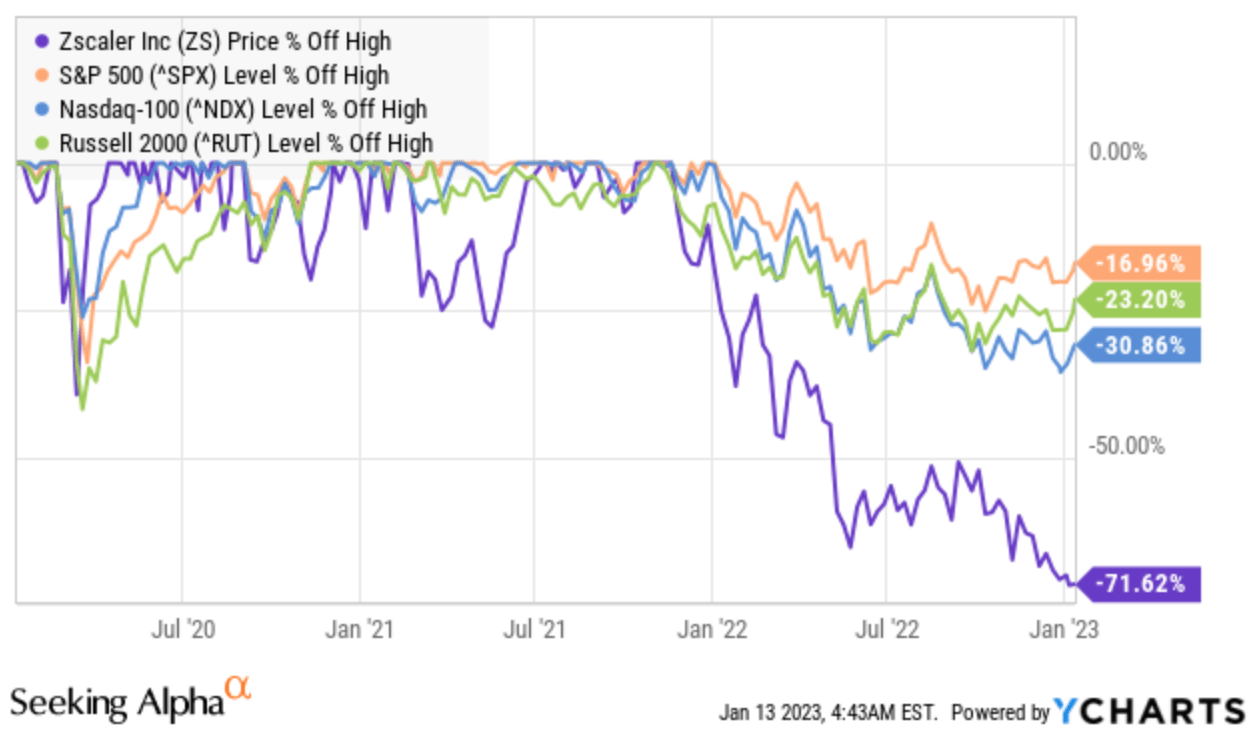

Although the stock has lost about 72% from its all-time high and has thus underperformed all the major indices, such as the S&P 500, Nasdaq as well as the Russell 2000, it still delivered a whopping return of over 500% to its investors since its IPO (see chart).

Price % off high – ZS vs indices (YCharts)

Well, is it worth considering an investment in ZS taking into account the current selloff?

2. Valuation

In terms of valuation, I have chosen two valuation models:

- the enterprise value-to-sales ratio (EV/S), which adds debt and preferred shares to the market cap and subtracts cash as well as

- the rule of 40 by using the revenue growth rate and EBITDA margin.

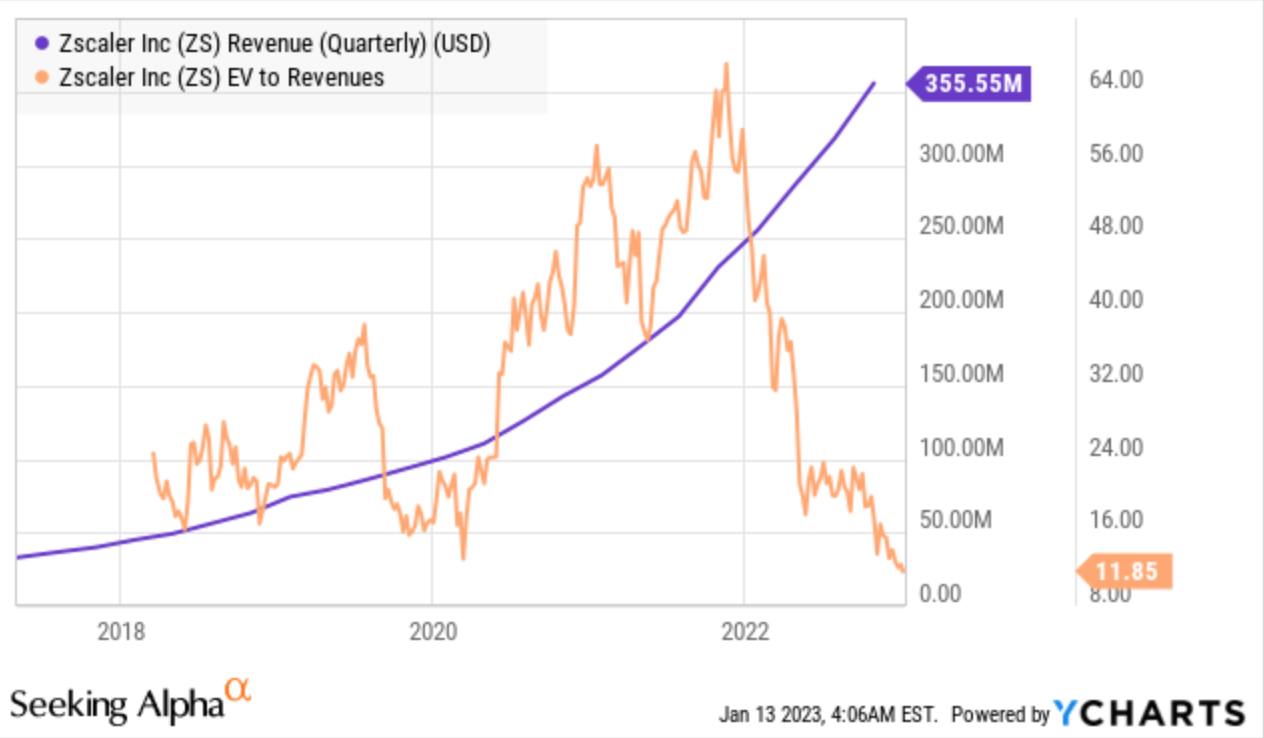

With regard to the EV/S ratio and the quarterly sales trend, it is striking that the EV/S ratio has logically fallen sharply from over 64 to currently 11.58, on a level never seen since the company’s IPO as a result of the slump in the share price. Nevertheless, sales are growing very fast and sequentially on a quarterly basis (see chart).

ZS EV/S ratios and quarterly revenues (YCharts)

It is worth mentioning that the EV/S ratio is even lower than in 2020 during the COVID selloff at the stock market. Nevertheless, the stock recovered quickly and reached an EV/S ratio of more than 64 as a beneficiary of the work-from-home policy as well as the ultra loose monetary policy of the Fed.

Consequently, the current EV/S ratio of 11.58 seems to be quite tempting despite the Fed’s current hawkish monetary policy.

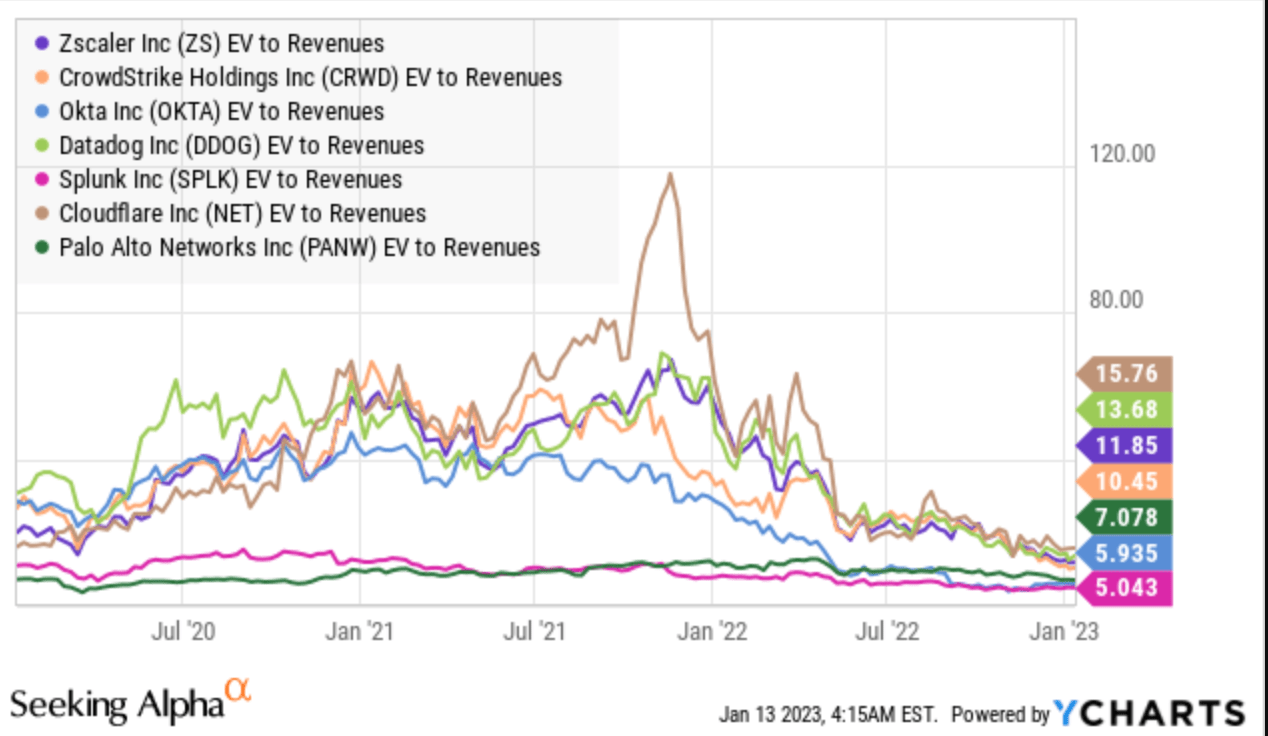

Additionally, compared to its cybersecurity peers, the valuation seems to be reasonable (see following chart).

EV/S ratio – ZS vs peer group (YCharts)

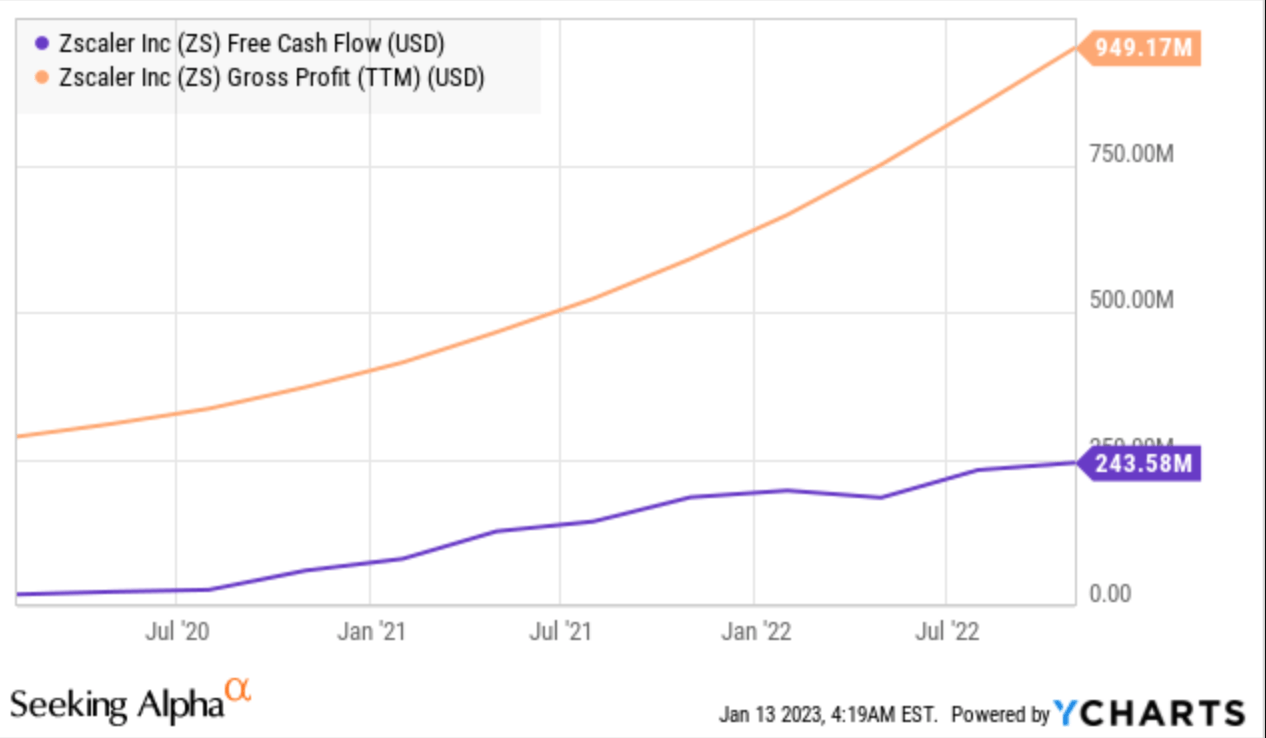

The reason for the stock’s relatively higher valuation becomes clearer by taking into consideration the Free Cash Flow (FCF) as well as the Gross Profit. ZS, as one of a few exceptions among growth stocks, has a track record of sustainably rising FCF and gross profits (see chart).

ZS FCF and gross profit (YCharts)

Additionally, the company is profitable and raised its guidance in the most recent quarter, which speaks for operational success, customer satisfaction and quality of their services.

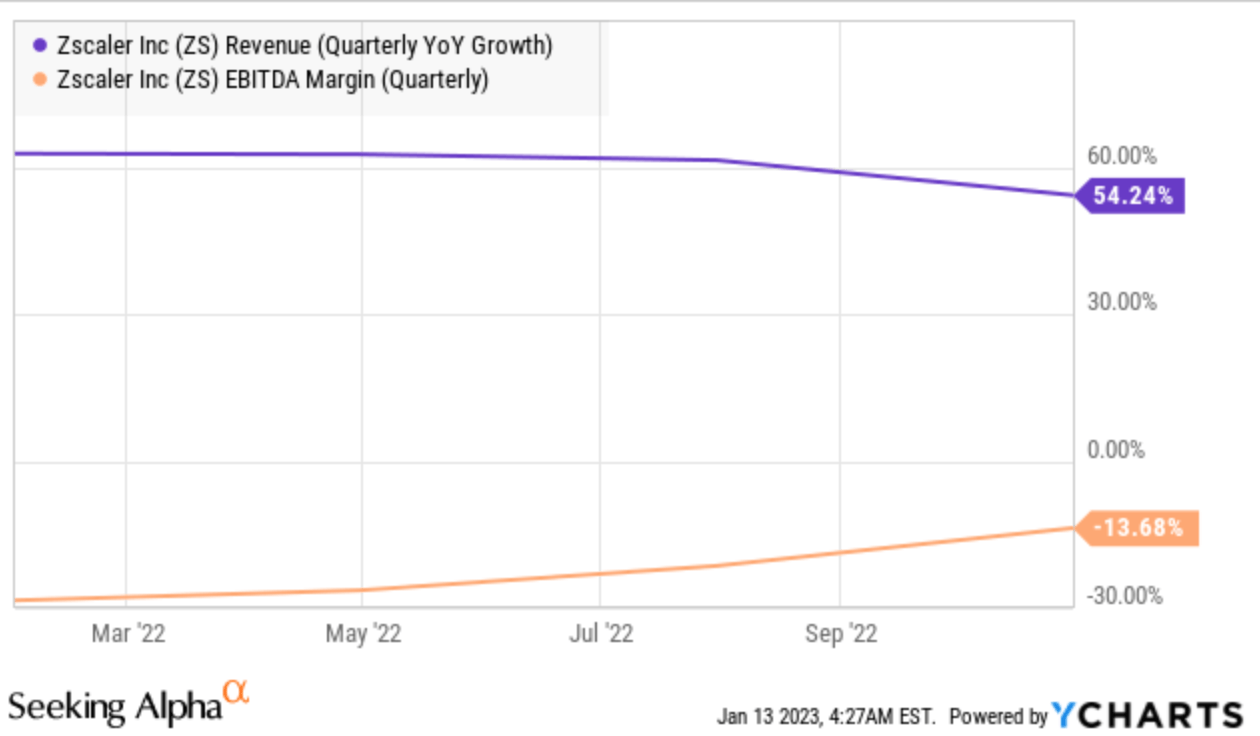

With regard to the rule of 40 and a revenue growth rate of over 54% in the most recent quarter, it can be stated that the ratio of 40.56 (54.24 minus 13.68) is tempting to consider an investment at the current stage. According to the rule of 40, a promising investment should have a ratio of 40 or more.

Rule of 40 – ZS quarterly revenue growth rates and EBIDTA margin (YCharts)

3. Technical Analysis

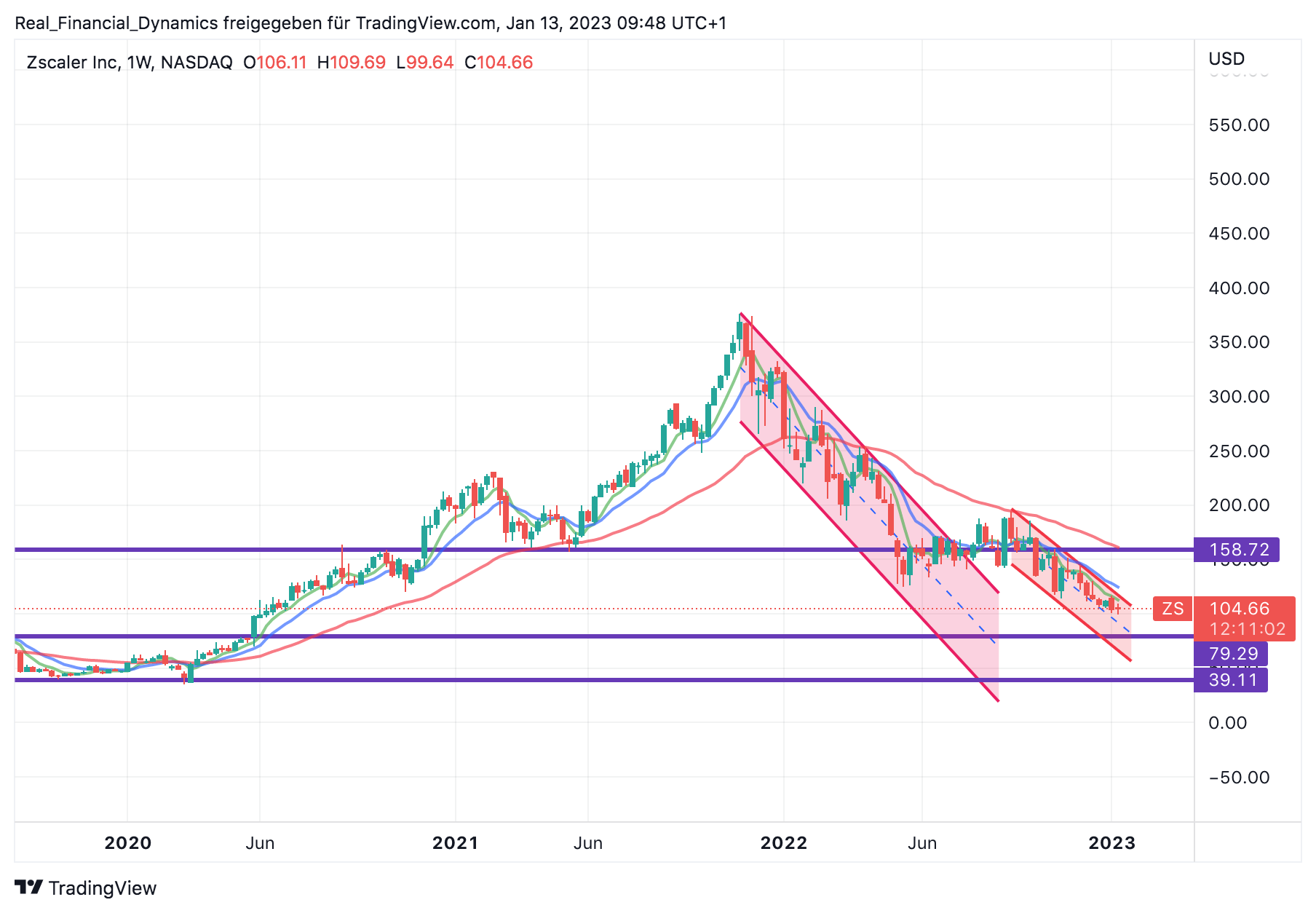

When looking at the chart, it becomes obvious that ZS is still caught in a downtrend. The next targets to the downside seem to be $79. If the support of $79 breaks or the market environment deteriorates further, the stock could even fall to around $39, which marks its COVID low in 2020 (see following chart).

On the other hand, if the market environment improves, the stock could move up to $158, which in turn would mean a short-term profit of around 50%.

However, considering the current market conditions and Fed tightening, a short-term breakout to the upside seems highly unlikely.

Overall, the trend still points downward, signaling more declines than rising prices.

ZS chart – still caught in a downtrend (TradingView)

4. Conclusion

ZS was a tremendous investment delivering a whopping return of 2,000% after its IPO. Even despite the current selloff, investors are sitting on a return of around 500% since the IPO. Additionally, the company was still able to provide revenue growth beyond 50% in the most recent quarter. Moreover, the company is well positioned in the attractive field of cybersecurity which is expected to become increasingly relevant in the future.

From a valuation point of view, the company seems to be reasonable valued with a EV/S ratio of 11.58 as well as a ratio of 40.56 with regard to the rule of 40.

On the other hand, and by taking into consideration the technical analysis, it becomes clear that ZS is still stuck in a downtrend, which tends for further selling pressure in the near future unless there is a short term improvement from the inflation or monetary policy side (which seems to be unlikely at the current stage).

Investors should watch closely the further development with regard to growth rates, margins as well as technical situation. If ZS is able to keep its growth rates and margins in 2023 and beyond, and the chart’s technical situation improves, I think investors could consider an investment promising whopping returns once again.

Currently, under the conditions mentioned above, there is no compelling reason to consider a purchase, so I give the stock a neutral rating.

If you want to learn more about the company’s business model and fundamentals, then you are welcome to refer to my analysis of March 11, 2019, where I have examined ZS in detail.

Be the first to comment