Sundry Photography

Zscaler (NASDAQ:ZS) is a leading cybersecurity company that is securing the digital transformation of enterprises. According to one study, Cloud security is forecasted to grow at a rapid 13.7% CAGR up until 2026 reaching $77 billion in market value. Zscaler is poised to spearhead this trend as a leader in the industry. In the most recent quarter, Zscaler generated strong financial results that beat both revenue and earnings expectations. In addition, the company has a proven sales motion, high retention rates and an elite customer base, serving over 40% of the Fortune 500. In this post, I’m going to break down the company’s business model, financials, and valuation, let’s dive in.

Secure Business Model

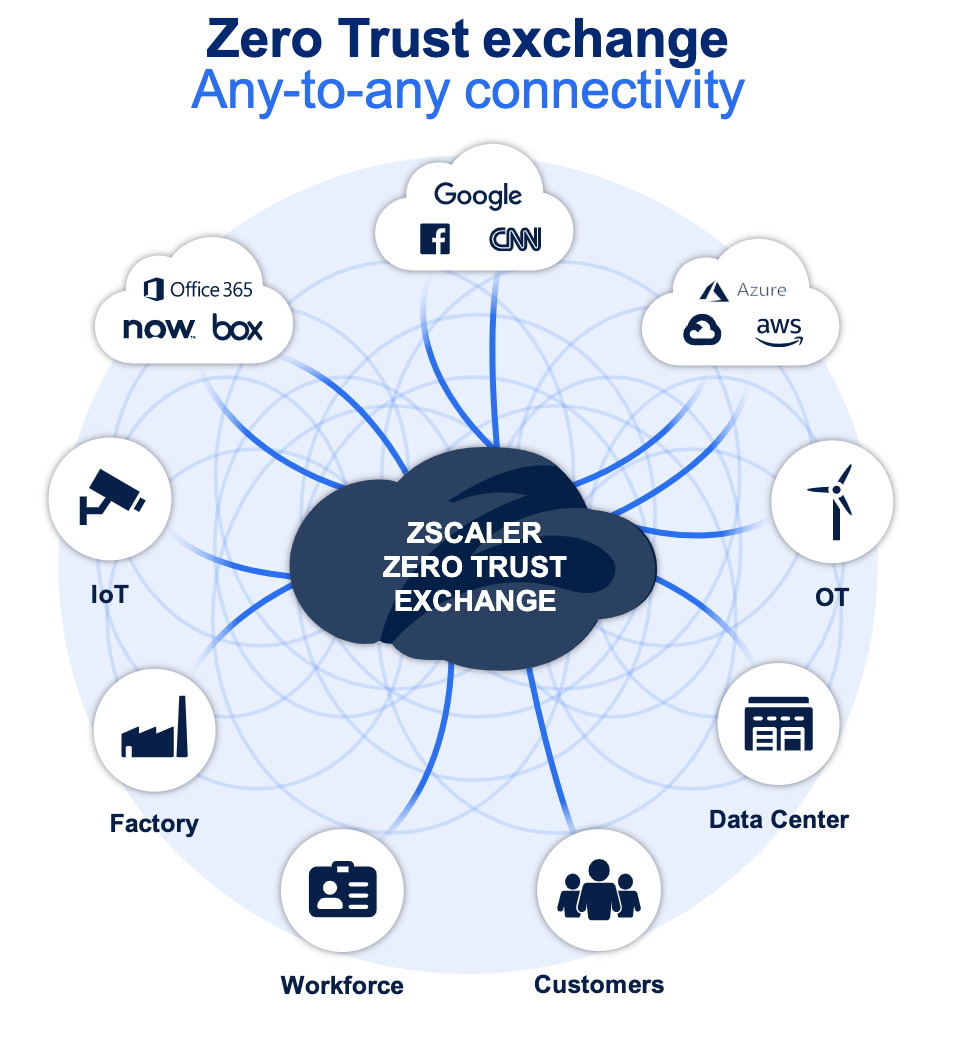

Zscaler is a cybersecurity company that is a Gartner leader in the security edge. The company operates a “Zero Trust Network” which connects over 34 million users across its 6,700 customer base. The platform secures the modern IT operating environment of enterprises. In today’s landscape, we have remote workers, cloud applications, and various different cloud providers (AWS, Azure, Google Cloud). “Zero Trust” refers to the cybersecurity methodology of only giving users access to the applications they need, in order to stop attackers from “moving laterally”. For example, a hacker could breach an old HR application but then move into the finance applications. To offer this protection Zscaler offers an “intelligent switchboard” solution through its network of 150 data centers globally.

Zscaler Switchboard (Investor Presentation 2022)

The company has recently announced new features such as Posture Control and Zero Trust for Workloads with AWS. The Zscaler platform uses advanced machine learning and AI to assess the risk posture of various users and then look for anomalies to help prevent an attack. Its platform even allows encrypted SSL/TLS traffic to be inspected. This is a game changer as most firewalls only look on the outside of the encrypted IP packets, but they can’t see inside easily as by definition they are encrypted.

Zscaler has a net promoter score [NPS] of over 70 which is more than double the average for SaaS companies. In the most recent quarter, they scored a new win with a Fortune 50 pharmaceutical company that purchased all three of Zscaler’s offerings for its 145,000 employees. I covered more details on Zscaler’s business model and its Founder CEO in my previous post you can read here.

Growing Financials

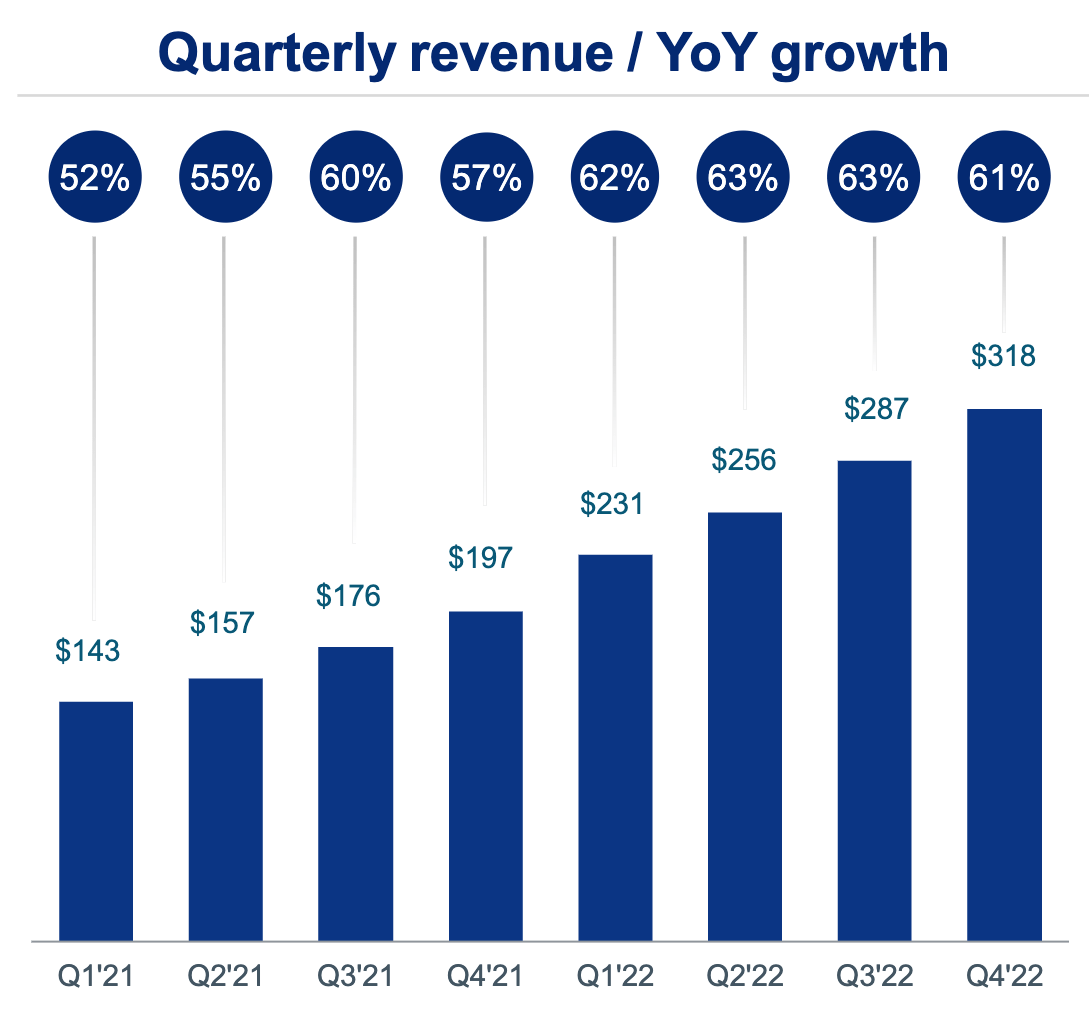

Zscaler generated strong financial results for Q4, 2022. Revenue was $318.1 million, which beat analyst estimates by $15.34 million and increased by a blistering 61% year over year. Just over half (52%) of Zscalers revenue comes from the Americas. With 33% from the EMEA region and just 15% from the Asia Pacific. Due to a strong focus on dollar-denominated markets the company is less susceptible to the FX exchange headwinds that have been driven by a strong dollar and impacting many businesses with strong international exposure.

Revenue YoY (Q4 Earnings Presentation)

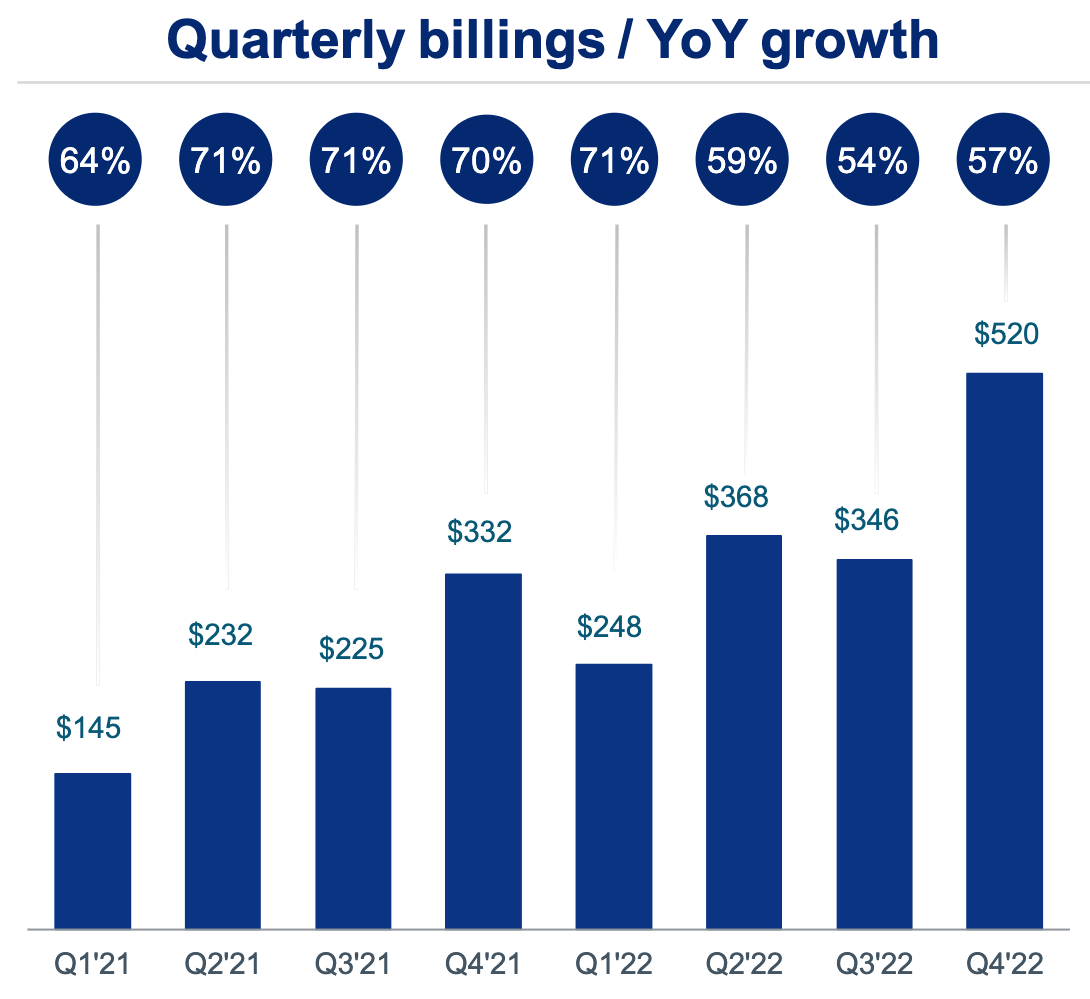

Calculated billings popped by 57% year over year to $520.4 million. Deferred revenue, which is a reliable metric of future earned revenue was over $1 billion also up a substantial 62% year over year.

Quarterly Billings (Q4 Earnings Report)

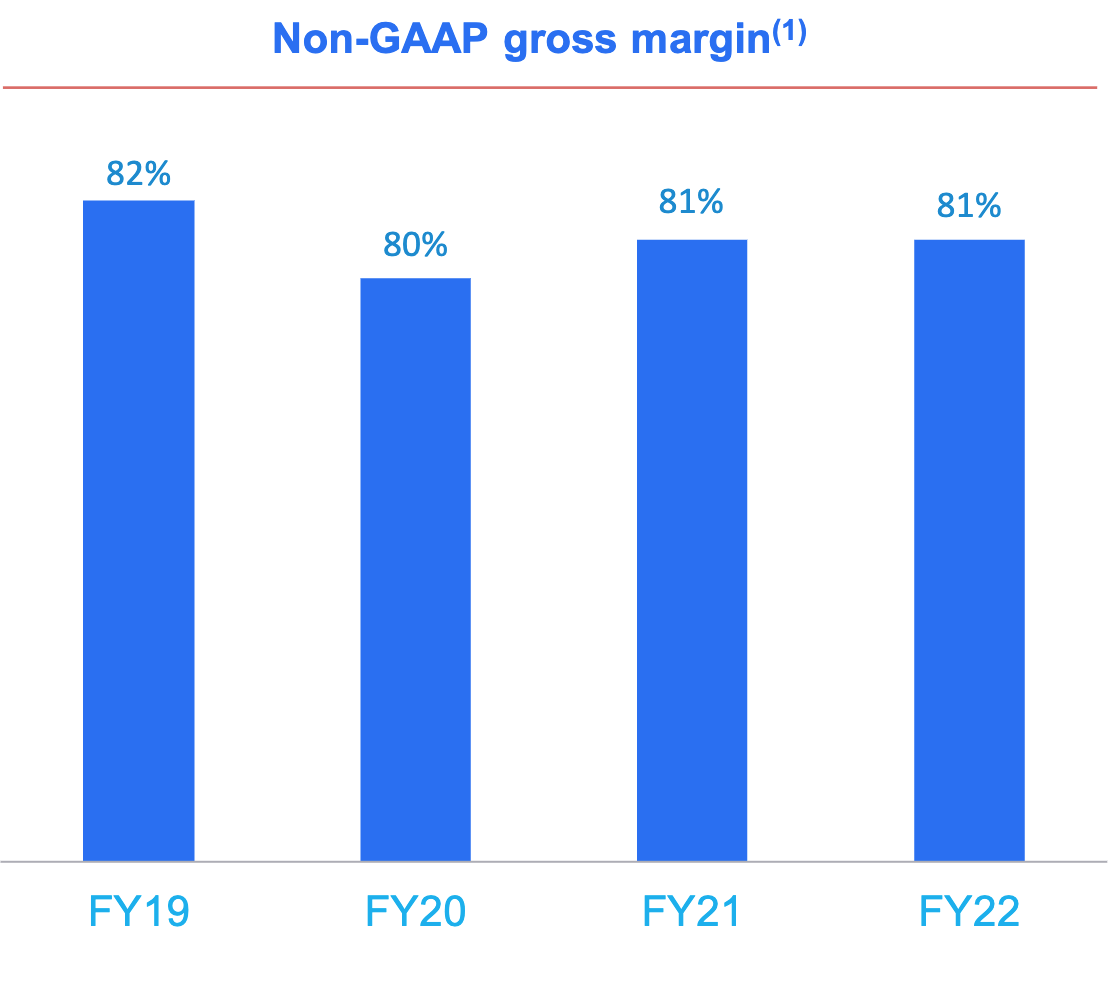

As a cloud company, Zscaler has a super high gross margin of ~81% [non GAAP] which has been pretty stable over the past few years.

Gross Margin (Q4 Earnings Presentation)

The company has also generated a GAAP loss from operations of $82.5 million or 26% of revenue. The good news is this is a lower percentage of revenue than the prior year when losses made up 34% of the total revenue. This is an indication of high operating leverage which is a positive sign and should only improve as the company further scales. On a Non-GAAP basis income from operations was a $38.1 million or 12% of total revenue, which is a positive sign.

Earnings Per Share [Normalized] was $0.17, which beat analyst estimates by $0.06 per share.

The company generated strong cash from operations of $103.1 million or 32% of revenue, with free cash flow of $74.8 million, which makes up 24% of revenue.

Zscaler has a robust balance sheet with cash, cash equivalents and short-term investments of $1.7 billion, which increased by $228.8 million year over year. In addition, the company has just over $1 billion in total debt, with the majority being long-term which is a positive.

For the full year of 2023, management is guiding for total revenue of approximately $1.49 billion to $1.50 billion, which would represent an increase of ~50% year over year which is fantastic.

Advanced Valuation

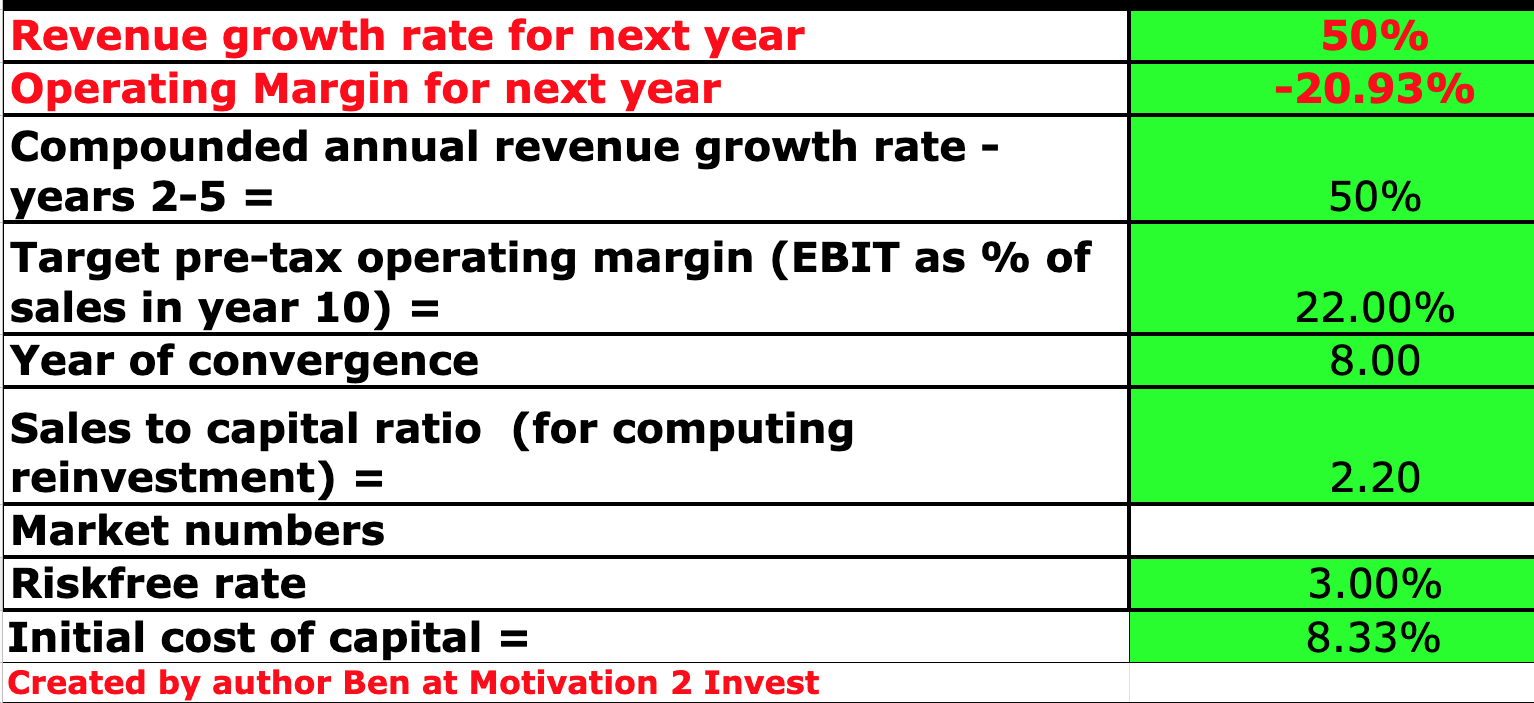

In order to value Zscaler, I have plugged the latest financials into my advanced valuation model which uses the discounted cash flow method of valuation. I have forecasted 50% revenue growth per year over the next 5 years.

Zscaler stock valuation 1 (created by author Ben at Motivation 2 Invest)

In addition, I have forecasted its operating margin to expand to 22% over the next 8 years. I expect this to be driven by greater “scale” and more upsells through the “land and expand” strategy.

Zscaler stock valuation 1 (created by author Ben at Motivation 2 Invest)

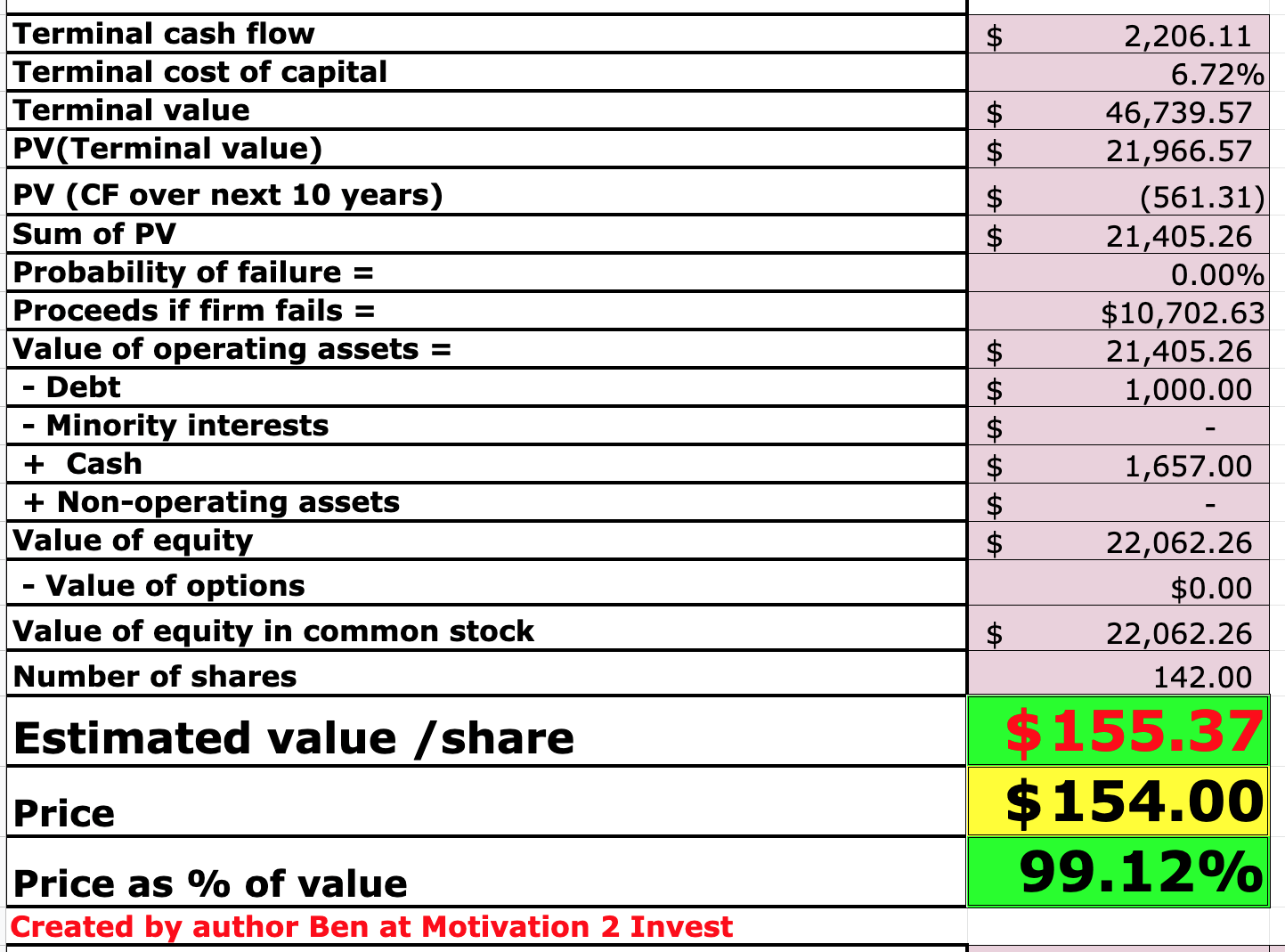

Given these factors, I get a fair value of $155 per share. The stock price is trading at a similar level at the time of writing and thus is “fairly valued”.

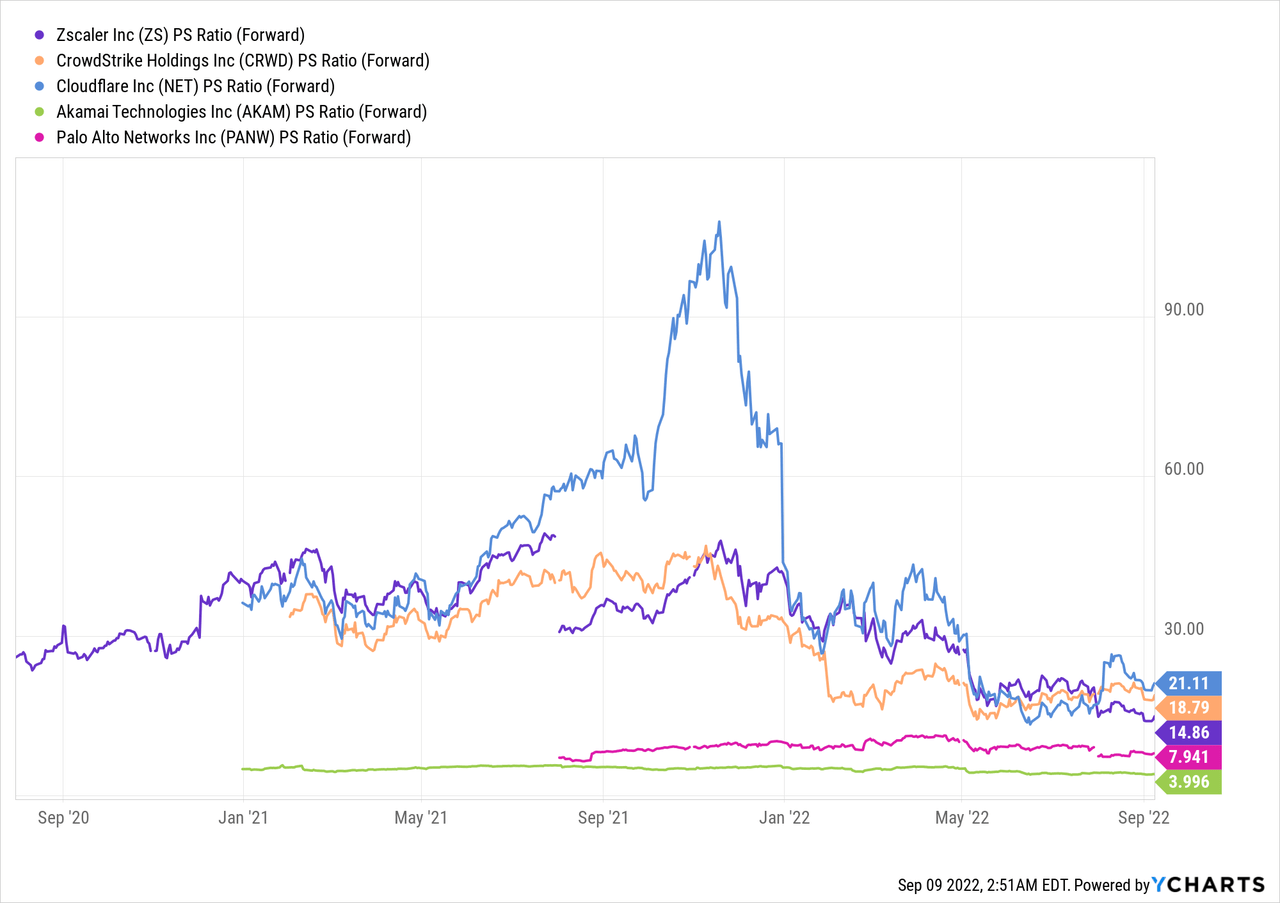

As an extra datapoint Zscaler is trading at a Price to Sales Ratio = 21, which is 33% cheaper than its 5-year average. Relative to the sector, Zscaler (Purple line) is trading mid-range on a Price to Sales Ratio [forward] multiple.

Risks

Recession/IT Spend Decline

Many analysts are forecasting a recession and thus this may cause companies to reduce new IT spending as they focus on cutting costs. However, I do expect longer term the trend of increased IT spending, especially on cybersecurity will increase as per analyst forecasts.

Competition

The Cybersecurity industry is getting more competitive and Zscaler faces competition from companies such as Check Point, Fortinet, Palo Alto Networks, Pulse Secure and Forcepoint. More competition generally results in slower growth and lower margins long term.

Final Thoughts

Zscaler is a leader in the secure edge and is poised to benefit from tailwinds across hybrid work and the cloud. The company has continued to perform strong and has surpassed analyst estimates. Therefore the company looks to be a great investment for the long term.

Be the first to comment