SDI Productions/E+ via Getty Images

Zoom Video (NASDAQ:ZM) is seemingly one of the few tech stocks that is not up by a wide margin year to date but instead trading roughly flat. ZM has kept on to all of its growth coming out of the pandemic, including both its large net cash position as well as strong cash flow generation. However, its revenue growth has come to a standstill and management now expects the tough macro environment to heavily impact growth in its enterprise revenues. For investors who had been valuing ZM primarily based on the secular growth of its enterprise segment, such disclosure may be quite disappointing, though in theory this should be offset by stabilizing online revenues. With share repurchases being the primary catalyst, ZM stock remains too cheap on the basis of earnings – I reiterate my buy rating.

ZM Stock Price

Has there been a tech stock hit harder than ZM? Not only is ZM trading below pre-pandemic levels, but the stock is below where it traded when it came public in 2019, in spite of having grown its revenues by over 10x over the same time period.

I last covered ZM in March where I rated the stock a buy on account of the low valuation and strong balance sheet. Both of those points remain relevant today even if Wall Street continues to ignore the value here.

ZM Stock Key Metrics

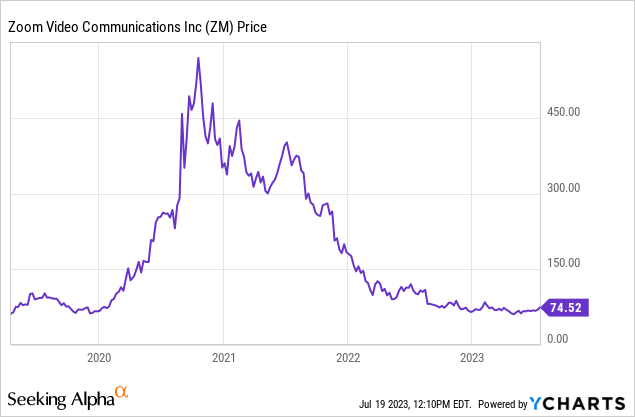

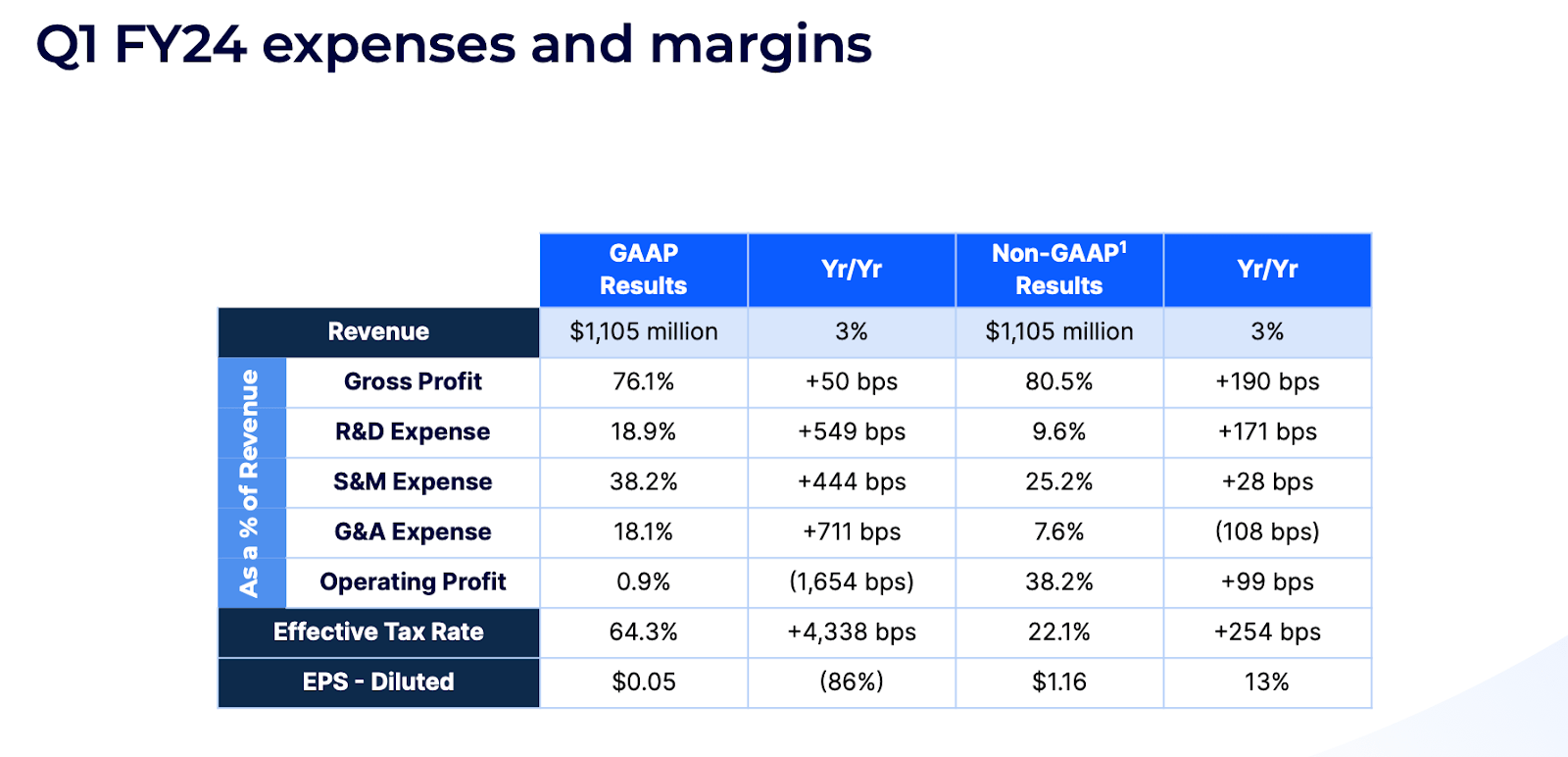

In its most recent quarter, ZM delivered 5% revenue growth to $1.123 billion ($1.105 billion constant currency), ahead of management guidance for $1.085 billion. As typical, enterprise revenue powered the growth, growing 13% YOY to $632 million.

FY24 Q1 Presentation

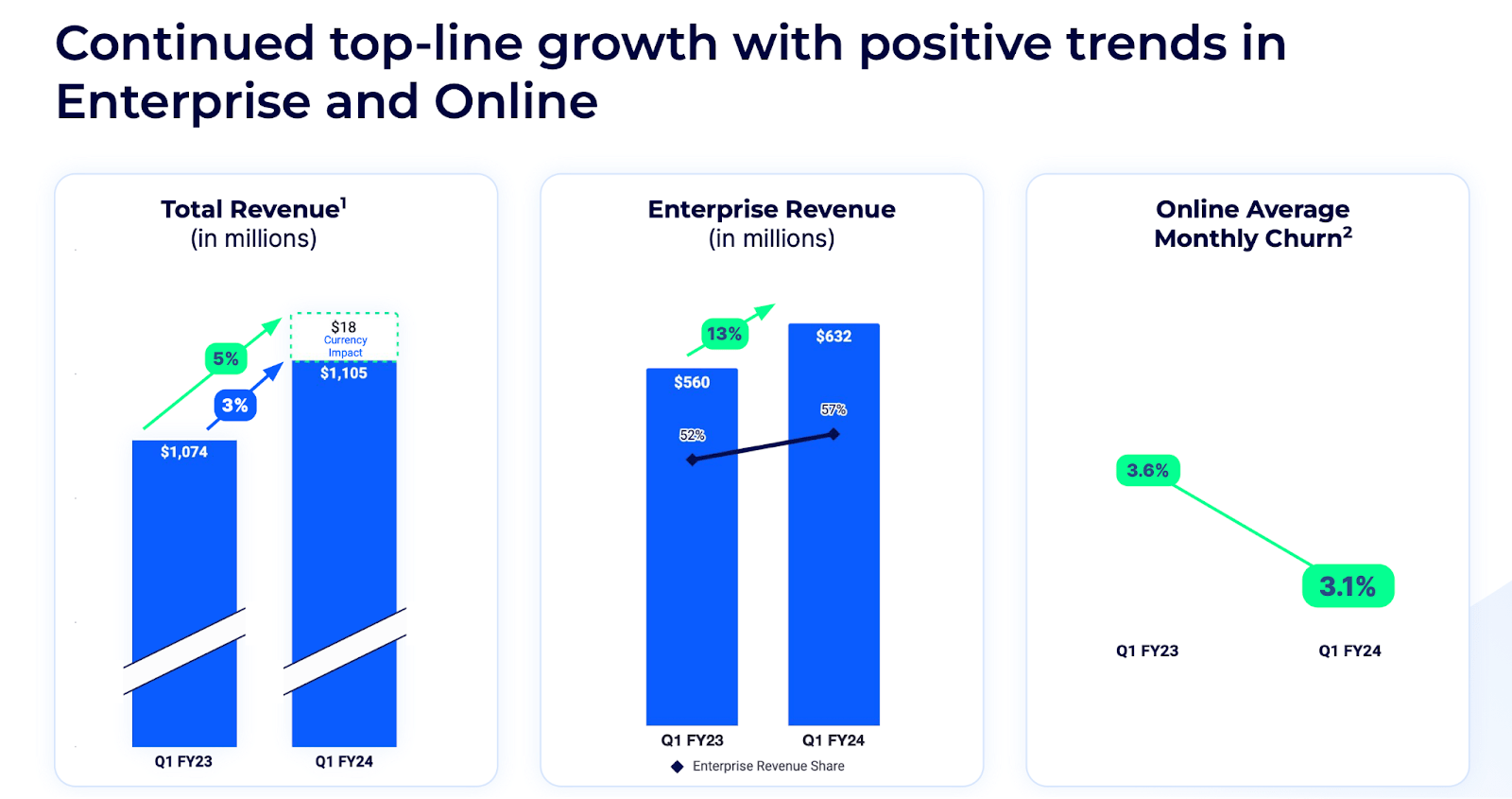

ZM grew its enterprise customer base by 9% YOY and around 1% sequentially. Its net dollar expansion rate declined to 112%, down from 115% sequentially and 123% YOY. Because this is a trailing twelve month metric, this implies a very low net dollar expansion rate in the quarter.

FY24 Q1 Presentation

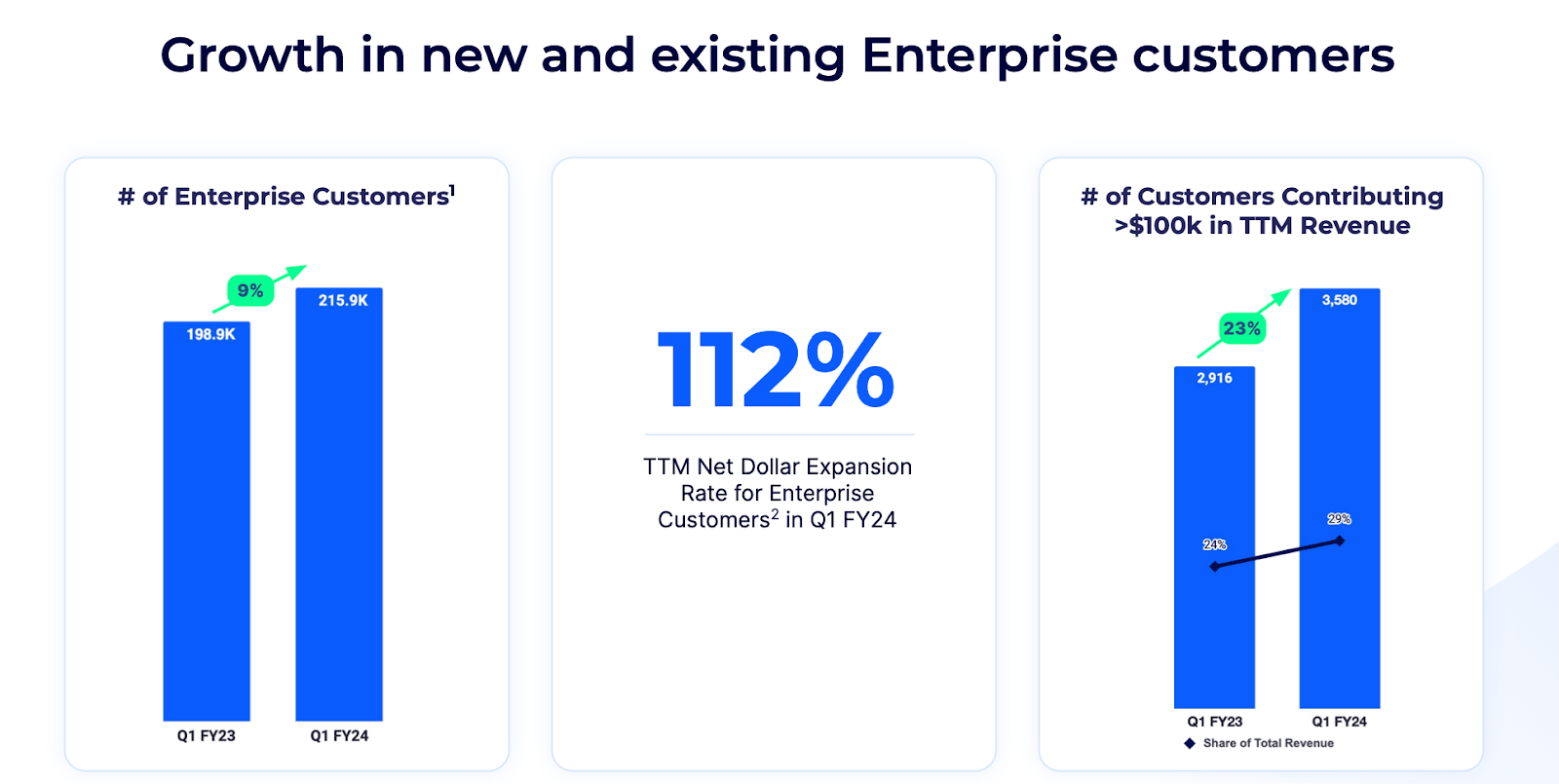

ZM saw its strongest fundamentals in the Americas, suggesting potentially that the company may see tailwinds upon a resolution of the Russian-Ukraine war.

FY24 Q1 Presentation

ZM continued to be a cash cow, generating $1.16 in non-GAAP EPS, well ahead of guidance for $0.98 in earnings per share.

FY24 Q1 Presentation

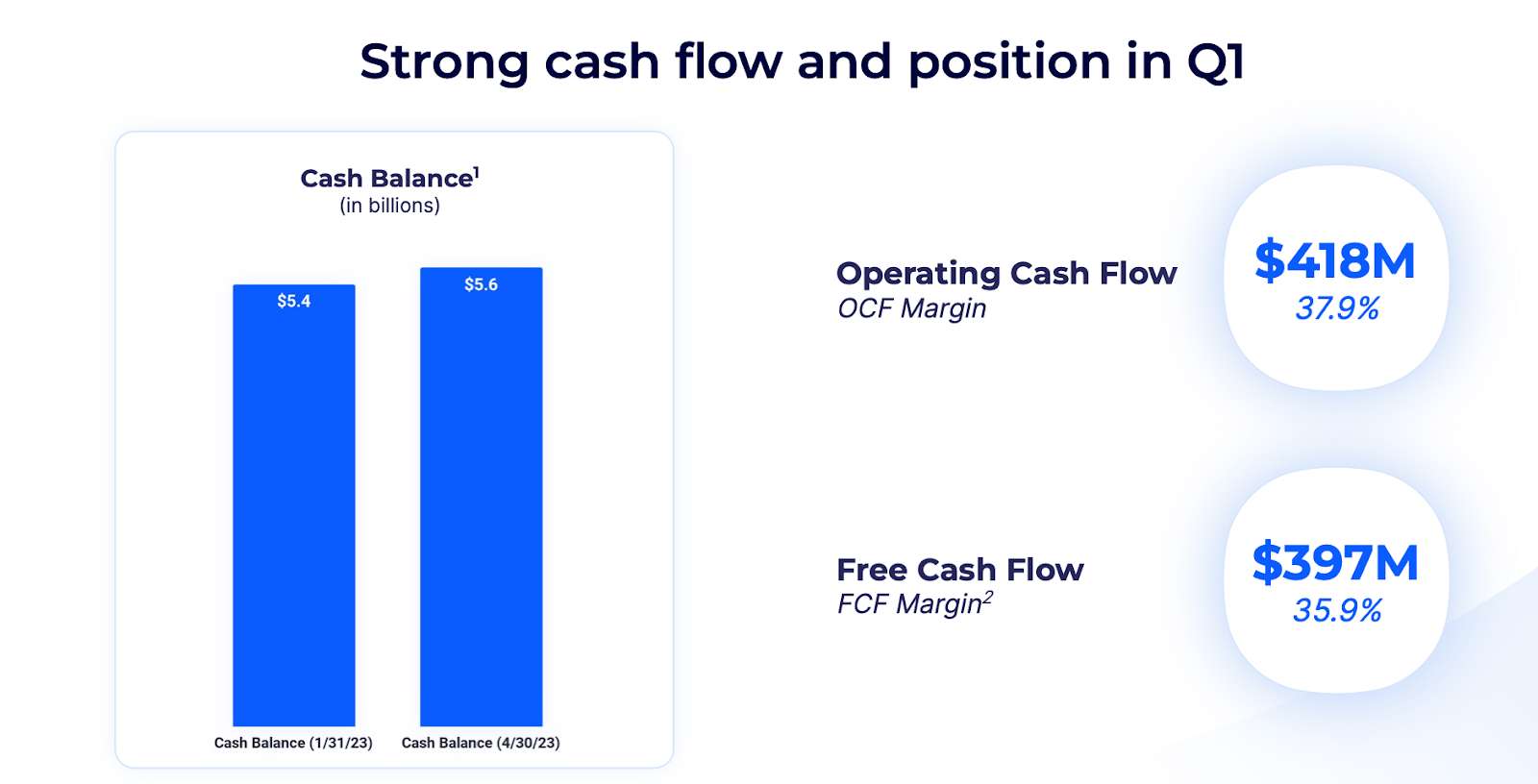

ZM ended the quarter with $5.6 billion in cash and no debt, giving it a “bulletproof” balance sheet amidst the tough macro environment.

FY24 Q1 Presentation

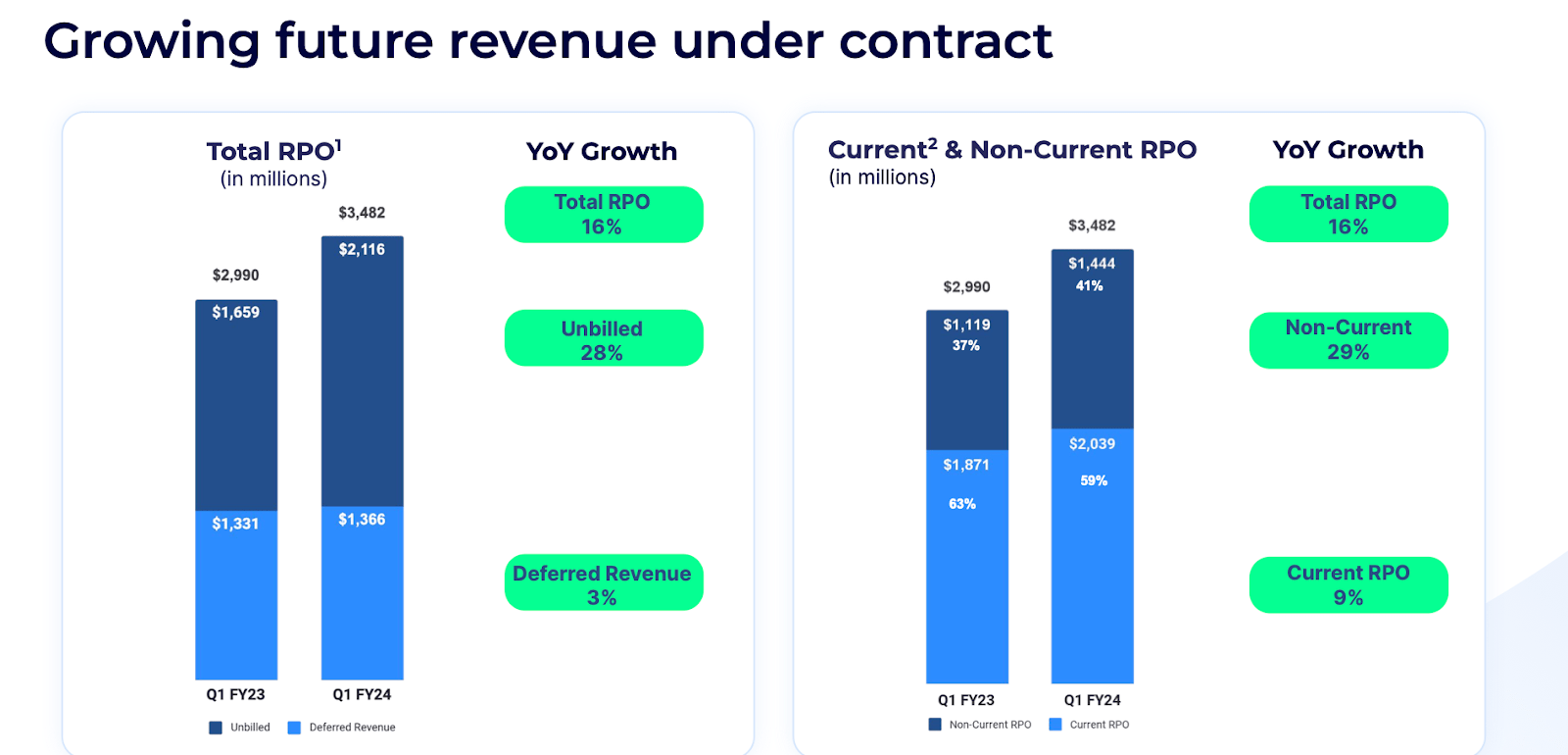

ZM also delivered strong 16% YOY growth in remaining performance obligations (‘RPO’).

FY24 Q1 Presentation

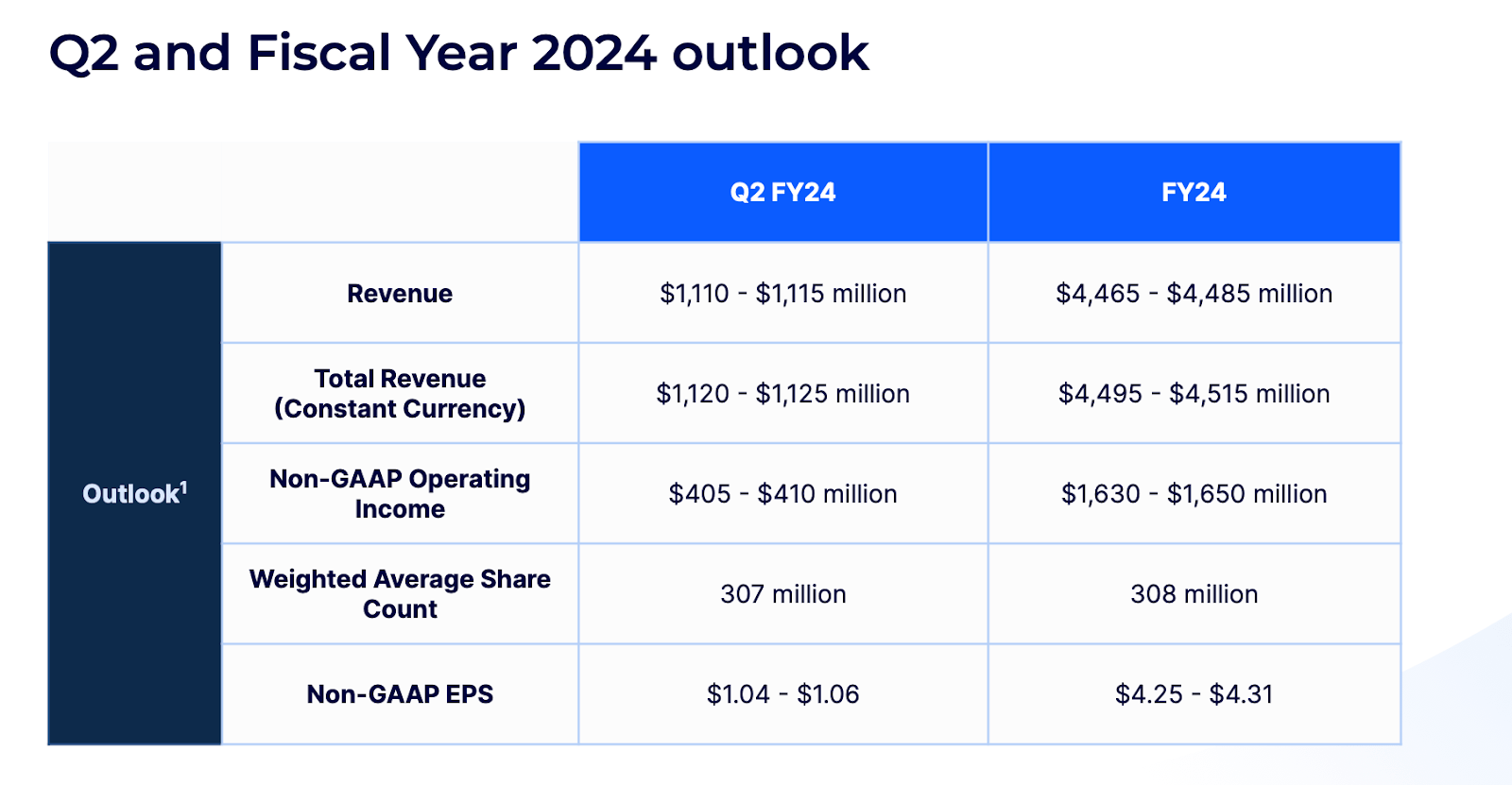

In spite of that strong RPO result, management guidance for the next quarter was modest, with revenue expected to grow by 1% YOY to $1.112 billion. A bright spot is that non-GAAP operating margin is expected to expand from 35.8% to 36.8%. For the full year, management slightly increased full-year revenue guidance to $4.485 billion at the high end, up from the prior guidance of $4.455 billion, as well as earnings guidance, with non-GAAP EPS expected to come in at $4.31 (prior guidance was $4.18).

FY24 Q1 Presentation

On the conference call, management noted that its online business is “stabilizing sooner than expected” with its churn down to 3.1%. Management stated expectations for approximately $480 million in Online revenues in the second quarter and “relatively flat thereafter in FY ’24.” Some may consider this good news, but those looking under the surface may question the implications this has for the Enterprise business. Indeed, based on that guidance, enterprise revenue growth is expected to total just a 0.004% rate in the fourth quarter of this year. That would represent a steep deceleration from the healthy double digit growth rates of the past many quarters. Management blamed “distractions” from its headcount reduction and reorganization initiatives. Management did however reiterate expectations “to see reacceleration of growth as we exit FY ’24 and having that continue into FY ’25.” Like many tech peers, the tough macro is clearly taking its toll on revenue growth.

Is ZM Stock A Buy, Sell, or Hold?

ZM trades at a reasonable valuation of around 4.8x sales. Consensus estimates call for modest growth moving forward.

Seeking Alpha

The undervaluation is better highlighted by the price to earnings multiple, which stood at around 17x as of recent prices.

Seeking Alpha

Throw in the net cash making up around 25% of the market cap, and ZM looks like an attractive bet here. ZM’s recently closed acquisition of Workvivo aims to bolster the company’s ability to improve employee communication.

Workvivo

Workvivo has an impressive client list and I expect ZM to benefit from being able to cross-sell both products to existing customers.

Based on a return to 10% revenue growth, 40% long term net margins, and a 1.5x price to earnings growth ratio (‘PEG ratio’), I could see ZM trading at 6x sales, implying 25% potential upside. The stock would still be reasonable priced at around 21x earnings. The main catalyst would be a share repurchase program, though the company has not repurchased any stock for many quarters. I would not be surprised if the company eventually authorizes a new share repurchase program to make use of its ample free cash flow to address the low valuation.

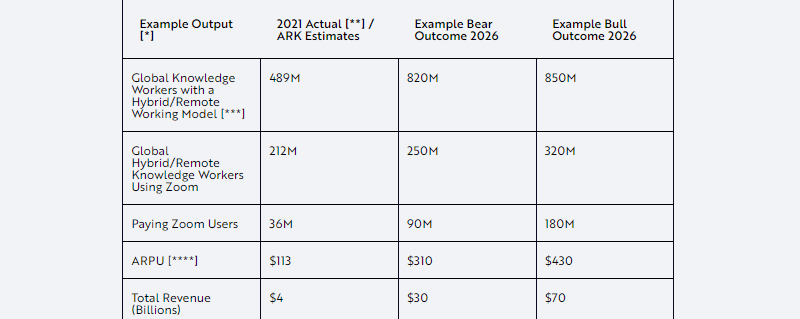

What are the key risks? While I am bullish the stock in part due to my positive view of the product, it is possible that customers begin to gravitate towards cheaper competitors such as Microsoft Teams (MSFT). It is also possible that competitors eventually catch up in terms of technological proficiency. I must also note that ZM is one of the largest holdings in Cathie Wood’s Ark ETFs (ARKK). It is possible that Wood eventually sells off her stake – in particular her growth estimates for the company look extremely aggressive (ZM is guiding for $4.5 billion in revenues this year).

Ark Invest 2026 Zoom Model

For ZM to come close to those targets, there would need to be yet another accelerated shift towards a remote working model (and even then, the target is very aggressive), but I am of the view that the pandemic already resulted in a dramatic pull-forward of that growth. It is possible that growth never accelerates again, at which point the valuation would be OK, but nothing special.

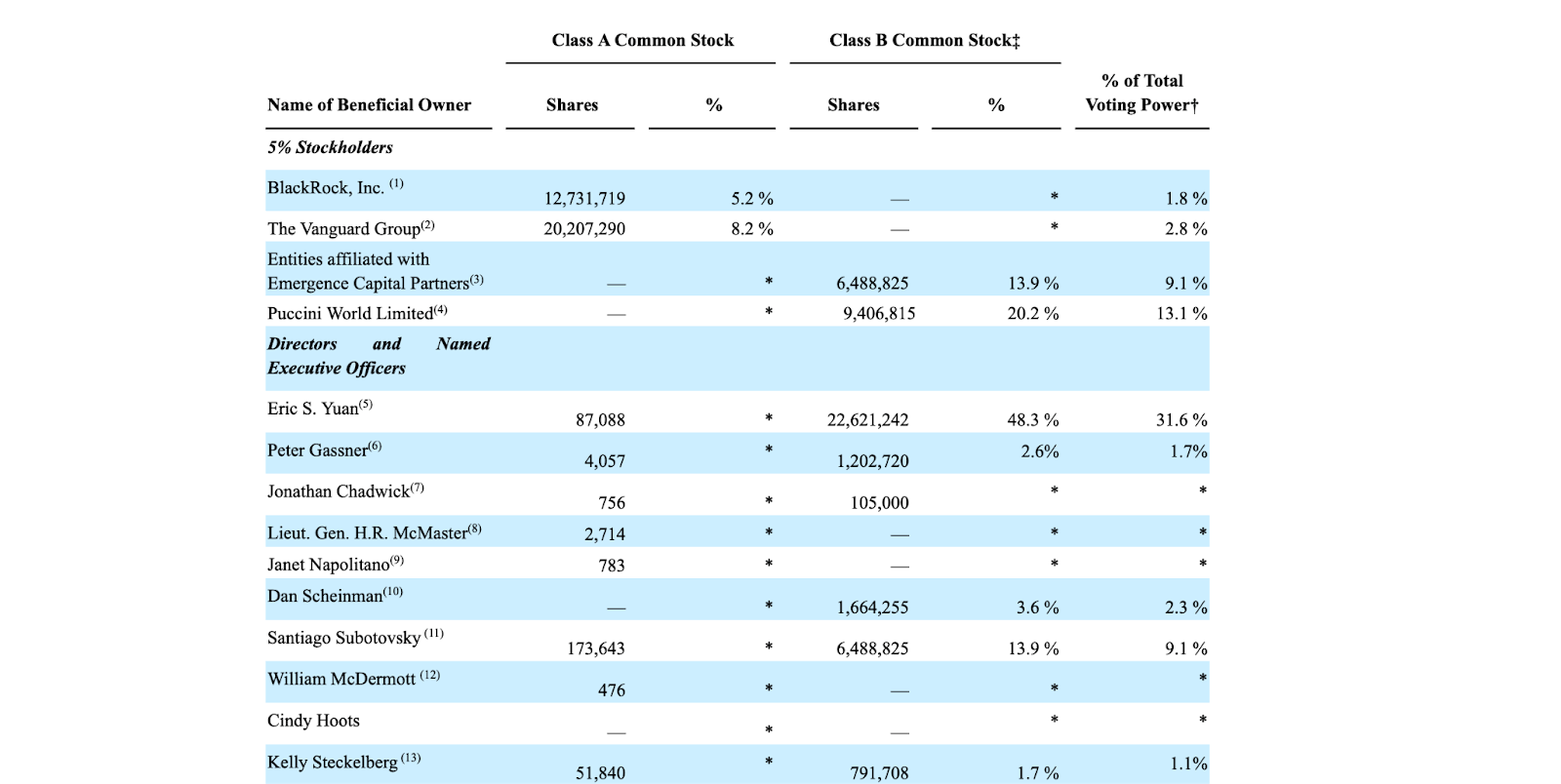

It is worth pointing out that the management team still retains ample “skin in the game.”

2023 DEF14a

That high insider ownership may suggest that management is eager to drive long term shareholder value. I reiterate my buy rating for the stock as the share repurchase thesis is easy to understand and offers a direct to tangible upside.

Be the first to comment