SDI Productions/E+ via Getty Images

Zoom Video Communications, Inc. (NASDAQ:ZM) is a company that almost every Internet user is now aware of. The massive growth of the company since the pandemic can be seen in how people constantly use “Zoom” as a verb or noun to refer to video conferences. The last time I checked, none of its competitors had achieved this feat, suggesting Zoom has carved out some competitive advantages in the last few years although the company still has a long way to go to thwart the threat of competition. The post-pandemic world, from a market performance perspective, has been ruthless toward Zoom even though the company has continued to grow, launch new products, and attract enterprise customers. This analysis begins with a discussion of Zoom’s operating margins and includes segments on the company’s short and long-term prospects.

Margins Are Declining; Is This A Real Concern?

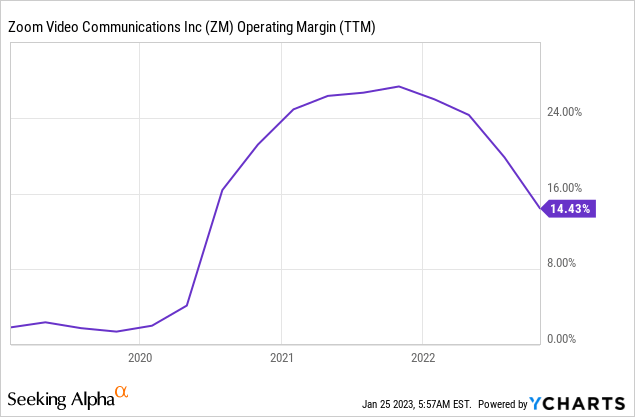

Zoom has continued to grow in the post-pandemic era but its profitability has come into question of late. Although quarterly revenue growth has slowed from over 350% in mid-2020 to less than 5% in late 2022, the company has consistently grown in each of the last 12 quarters. Notably, the return to office has not pushed Zoom’s revenue growth into negative territory. What has happened, rather, is a deterioration of Zoom’s operating margins.

Exhibit 1: Operating margin

As highlighted by a couple of fellow SA authors in the last few months, operating margins have come under pressure as a result of operating expenses increasing at a faster clip than revenue. Sales and marketing expenses grew by 45.6% YoY in the October quarter while R&D expenses almost doubled compared to the corresponding quarter in the previous year. The real problem was the lackluster revenue growth of just 4.8% in the quarter, which indicates higher marketing dollars are not yielding notably promising results in the short run. To identify whether this margin deterioration is a concern for long-term-oriented investors, one has to look deeper into the company’s business strategy.

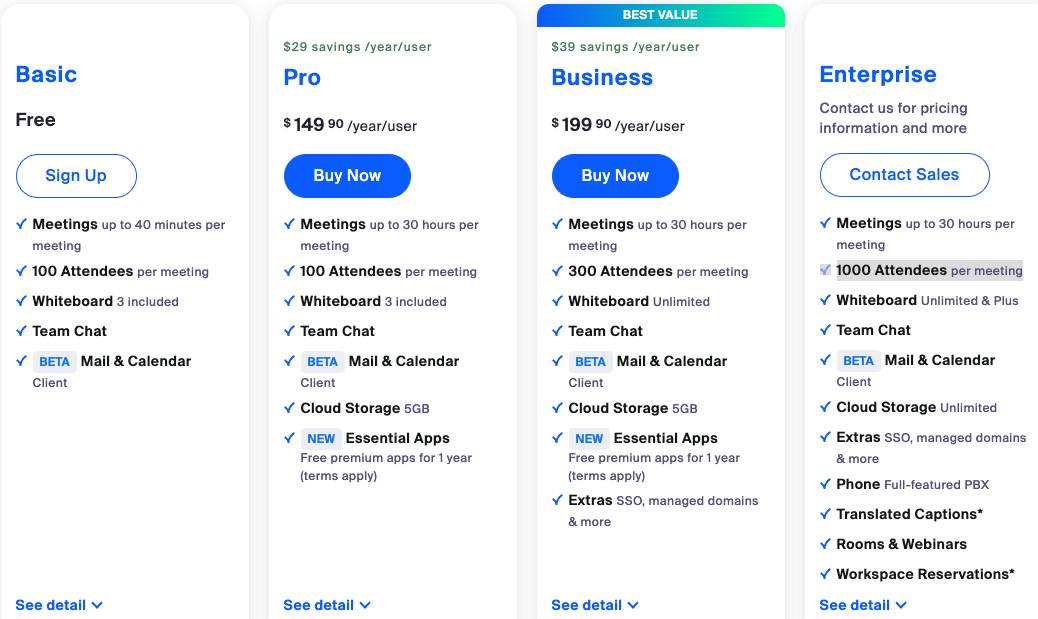

Zoom offers a seamless experience that enables both individual and business users to sign-up in just a few minutes, select their desired plan and get started with video conferencing. The company offers a free, basic plan with a 40-minute limitation per meeting, which is used as a marketing funnel to lure potential paid subscribers.

Exhibit 2: Zoom plans

Zoom

Source: Zoom

The company, in recent years, has shifted its focus to enterprise customers, which I believe is the right strategy given that these customers tend to be sticky. Targeting enterprise customers is the best way to stabilize revenue growth trends in the longer term as well since these customers are likely to keep their Zoom subscriptions active regardless of the state of the global economy as companies will continue to focus on efficiency gains resulting from the familiarity of using a dedicated collaboration software across its business units.

This shift in business strategy is beginning to yield promising results. Zoom, at the end of the last quarter (Q3 FY2023), served 209,300 enterprise clients, up from just over 183,000 clients in Q3 FY2022. The number of customers contributing over $100k in TTM revenue grew from 2,507 to 3,286 in the same period. The bulk of Zoom’s future growth is likely to come from upselling products/solutions to enterprise clients, so to ensure sustainable long-term growth, the company has to onboard as many enterprise customers as possible. Zoom employed around 2,500 full-time employees at the beginning of 2020, and as of the last quarter, the full-time employee count stood at 8,422. Although there are other reasons behind this expansion in headcount, the focus on the expansion of the enterprise business is also a major reason. The growing headcount is an obstacle to expanding operating margins in the short run although these costs seem unavoidable given that the company’s future is tied to the growth of the enterprise business.

Stock-based compensation has also had a negative impact on margins recently, and this is something investors should be wary of. Although it is common practice for American companies to reward employees with stock options/grants, stock-based compensation can have a dilutive effect on shareholders.

In conclusion, I do not believe Zoom’s margin deterioration is a grave concern for now given that the company is incurring costs to create a platform from which it can launch in the future. However, I do believe that the margin profile needs to be monitored closely and carefully in the coming quarters.

The Addressable Market Opportunity Is Expanding

Zoom, when it planned for its IPO in 2019, was purely a video conferencing platform that was yet to gain traction among the masses. Discussing its market opportunity, here’s what Zoom wrote in its S-1 filing:

Video has increasingly become the way that individuals want to communicate in the workplace and their daily lives. As a result, it has become a fundamental component of today’s communication and collaboration market, which also includes integrated voice, chat and content sharing. IDC has defined this market as Unified Communications and Collaboration. Within this market, we address the Hosted / Cloud Voice and Unified Communications, Collaborative Applications and IP Telephony Lines segments. IDC estimated that these segments combined represent a $43.1 billion opportunity in 2022.

At the time of its IPO, Zoom was looking to compete for a share of the video conferencing market which was a single component of the Unified Communications and Collaboration market.

In the last couple of years, Zoom has expanded its product portfolio to include Zoom Phone, Conference Room Systems, Online Webinars, Team Chat, Community Events, Cloud Contact Center, and a host of other features such as Zoom Mail and Zoom Calendar. This portfolio expansion has enabled Zoom to compete for a meaningful share of the Unified Communications and Collaboration market (not just video conferencing), which is expected to hit $100 billion by 2028.

Short-Term Gains Are Unlikely

If the global economy enters a deep recession this year, companies will look for ways to cut costs. One way to do this would be to embrace a hybrid work culture that promotes working from anywhere without coming to the office. Unlike in previous recessions, I believe many companies will follow this path this time around since they are already familiar with the hybrid work culture. Companies, in any case, are continuing to invest in software tools that enable a smooth transition to a hybrid work culture in the long term as the future of work is well and truly changing. Zoom will be a big winner if hybrid work gains traction in the coming quarters.

That being said, there is no reason for investors to be optimistic about what 2023 holds for Zoom. The company’s price plans are based on the number of seats used by a company, and with companies already slashing jobs and pausing expansion plans, Zoom’s recurring revenue might take a hit this year if business conditions do not improve meaningfully.

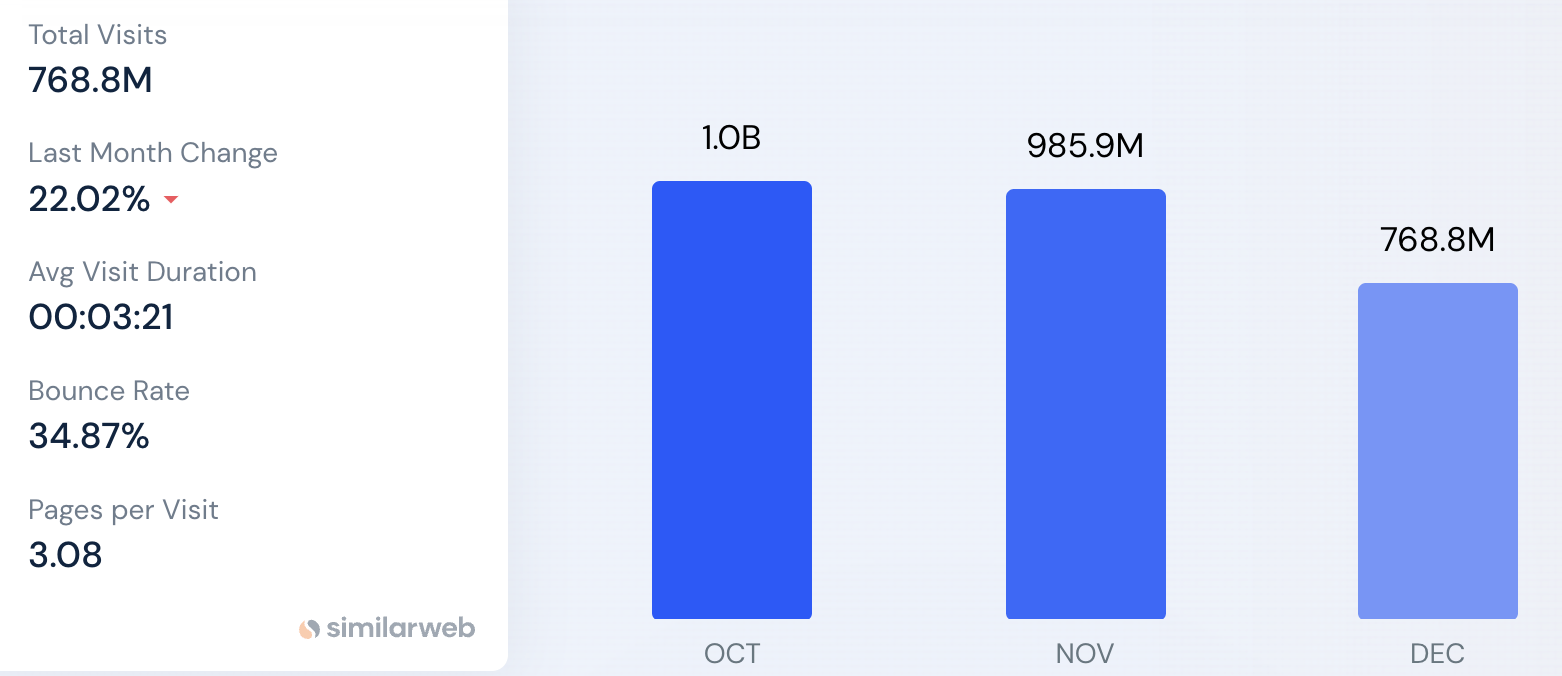

The fallout from pandemic highs, on the other hand, is still not over. In Q2 2022, website traffic to the top 95 companies in the software sector, including Zoom, declined by almost 30% YoY, which was a decline of more than 3.5 billion pageviews according to Similarweb data. At that time, I thought I was witnessing the peak drawdown from pandemic highs only to be proven wrong. As illustrated below, website traffic to Zoom continues to decline.

Exhibit 3: Traffic and engagement statistics for Zoom

Similarweb

Source: Similarweb

To say the least, these are not good signs.

Investors who jump on board the Zoom train by looking at its topline growth are unlikely to see any short-term gains as things are likely to get worse before they get better.

Takeaway

Zoom is making the right business decisions, in my opinion, to achieve sustainable long-term growth. The short-term outlook is not rosy, however, and the company is not necessarily cheaply valued either at a forward P/S multiple of 4.6. I am not comfortable with investing in Zoom stock just yet but this is the most bullish I have been on Zoom’s prospects. I am planning to revisit Zoom in a few months.

Be the first to comment