zorazhuang

The Williams Companies (NYSE:WMB) is an attractive midstream investment for investors that offers stable or growing EBITDA and cash flows. The midstream firm is seeing strong business momentum in its natural gas business and it has recently acquired natural gas transmission and storage assets from MountainWest Pipelines Holding Company. The acquisition was done at an attractive EBITDA multiplier factor and it expands Williams’ natural gas delivery footprint. Williams also has robust dividend coverage and the dividend is most likely going to continue to grow!

Williams: A natural gas pipeline giant

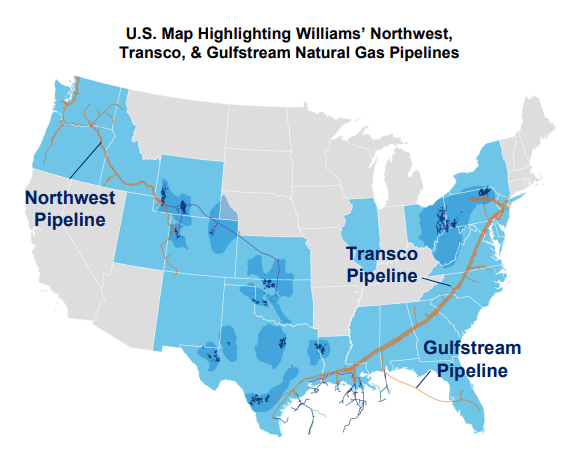

Williams owns and operates more than 30,000 miles of pipelines in 25 states and the company is aggressively expanding its pipeline footprint through acquisitions. A key asset in Williams’ energy portfolio is the Transco pipeline which handles 15% of America’s natural gas and connects Texas to New York City.

Source: Williams

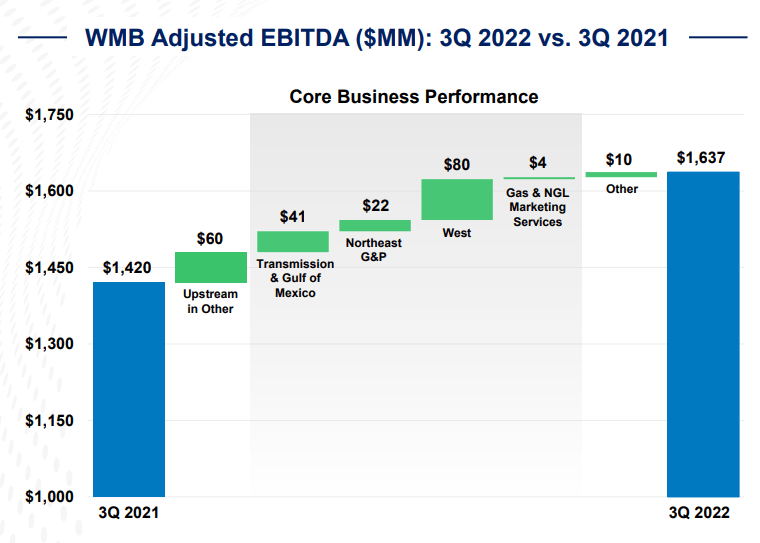

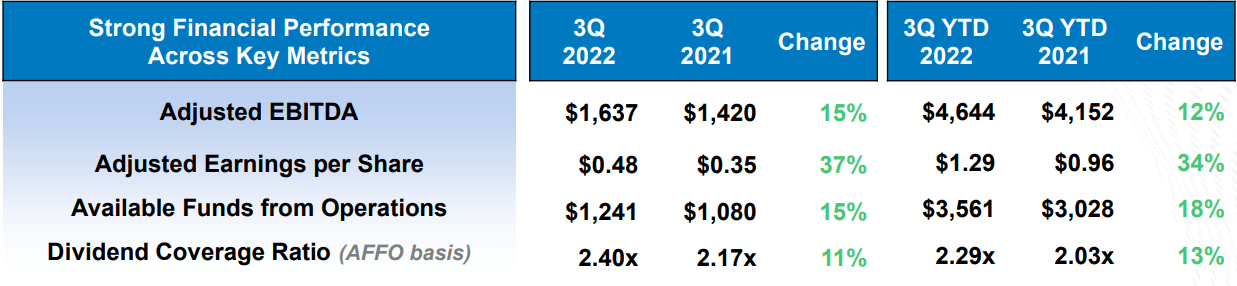

Williams benefits from booming demand for natural gas which has been reflected in strong adjusted EBITDA and cash flow growth… a trend that I believe will continue in FY 2023. Due to higher gathering volumes (+11% year over year) and higher rates in FY 2022, Williams reported 15% year over year EBITDA growth to $1.64B and 37% year over year growth in adjusted EPS to $0.48 per-share.

The business momentum is broad-based and includes all geographical segments in Williams’ portfolio, but the “West” segment did especially well in the third-quarter due to rapidly growing gathering volumes which in large part resulted from Williams’ Trace Midstream acquisition last year. Williams acquired the Haynesville gathering and processing assets of Trace Midstream in FY 2022 in a deal valued at $950M. The deal was done in order to grow Williams’ competitive position in the East Texas region of the Haynesville and the deal is already paying off for the midstream firm. Due to the only recently closed transaction, I expect the strongest growth going forward for Williams to occur in the West region.

Source: Williams

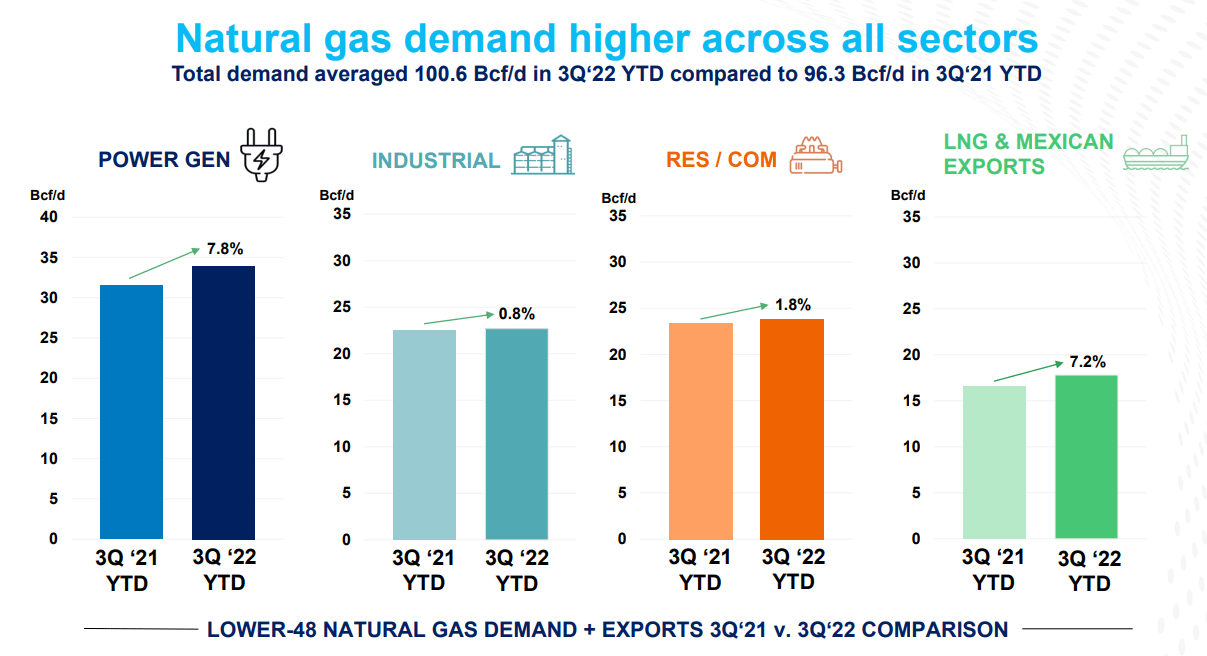

Williams’ results have been supported by growing domestic and international demand for natural gas products. In the first nine months of FY 2022, natural gas demand rose 4.5% year over year to 100.6 Bcf/d, driven primarily by strong demand from the power generation industry. I expect natural gas demand to remain resilient in FY 2023, unless a major recession were to throw the energy market off balance.

Source: Williams

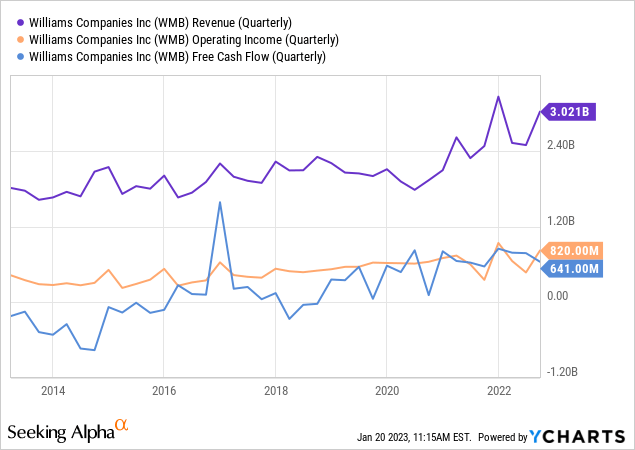

Williams’ service and product revenues, operating income and free cash flows are in a long term uptrend, showing a healthily growing midstream business.

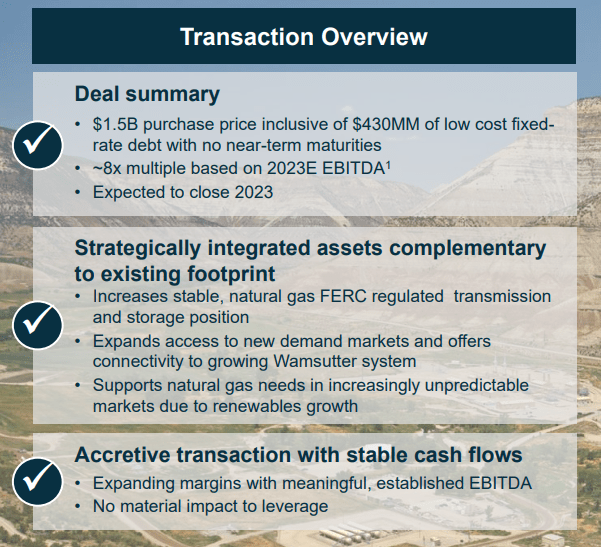

Recent acquisition of MountainWest

The acquisition of Trace Midstream’s Haynesville gathering and processing assets is not the only deal the midstream firm did lately. Williams also announced the acquisition of MountainWest from Southwest Gas Holdings in December in a deal valued at $1.5B (including assumed debt). The acquisition includes about 2,000-miles of interstate natural gas pipelines running through Utah, Wyoming and Colorado. The deal allows Williams to expand and increase the density of its natural gas pipeline network and adds 56 Bcf of total storage capacity to the company’s portfolio of energy assets. Williams is paying 8 X next year’s expected EBITDA for the deal which is an attractive multiple in my view.

Source: Williams

The MountainWest acquisition was more expensive than the Trace Midstream asset acquisition which cost Williams 6 X 2023 EBITDA. But MountainWest offers Williams access to new demand markets that the midstream firm has not yet served. I believe the deal is strategically sensible for Williams and since the transaction is expected to be leverage-neutral, MountainWest’s assets should soon contribute to Williams’ EBITDA and cash flow growth.

Outlook for FY 2023

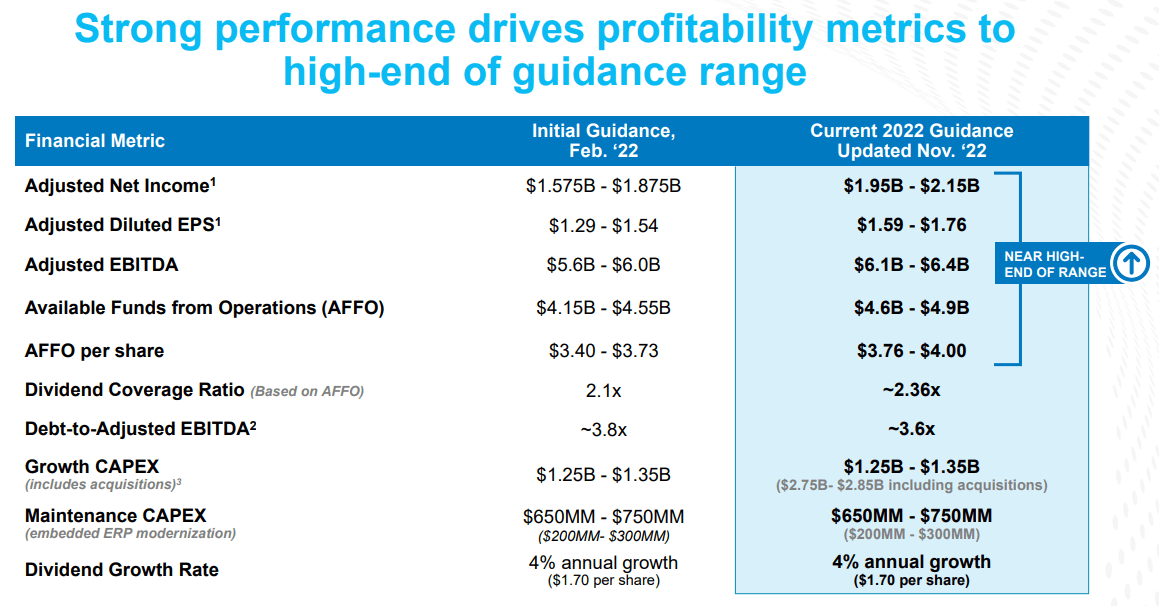

Williams’ strong performance in the natural gas business is driving record results for the midstream. The company guided for $6.1-6.4B in adjusted EBITDA this year, implying 11% year over year growth. The forecast for available funds from operations is $4.6-4.9B, implying 17% year over year growth. In the third-quarter, Williams confirmed that it expects its actual results to meet the high end of its guidance.

Source: Williams

Exceptional dividend coverage and growth potential

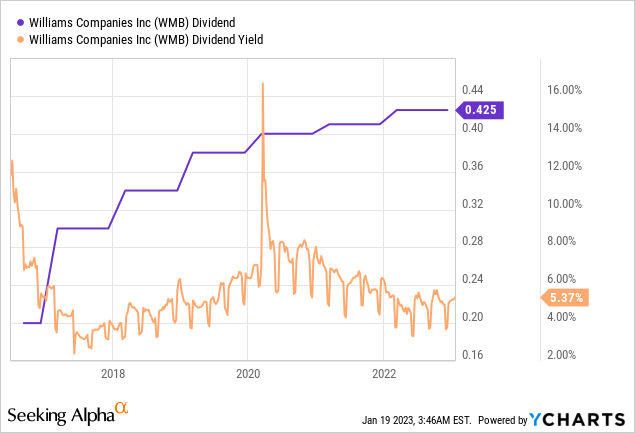

In the first nine months of FY 2022, Williams showed a distribution coverage ratio of 2.29 X, based off of available funds from operations. Other midstream firms I have worked on, like Enterprise Products Partners (EPD), have distribution coverage ratios of 1.8 X, so Williams’ dividend coverage is exceptionally good. This means that the dividend is more than just well covered and has potential to grow going forward. Williams has guided for 4% annual growth in its dividend and is currently paying $1.70 per-share which translates into a 5.4% dividend yield.

Source: Williams

Williams’ dividend is in an uptrend and has consistently grown since 2016.

Williams’ valuation

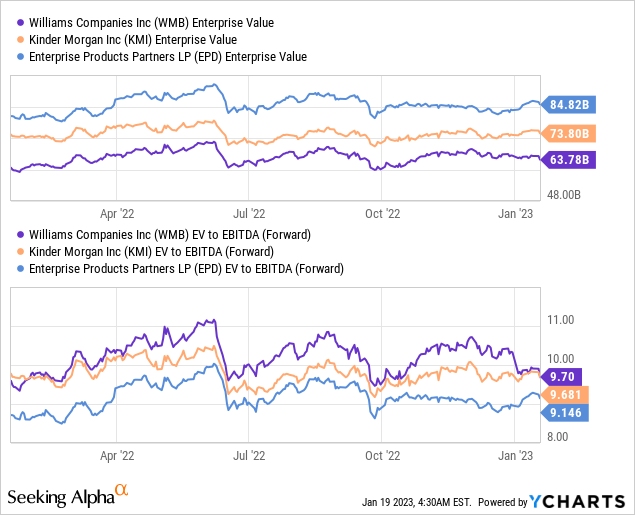

Williams expects $6.1B to $6.4B in adjusted EBITDA in FY 2022 and has an enterprise value of $63.8B which implies an EV/EBITDA ratio of 10.0 X. On a forward EBITDA basis, Williams is trading at 9.7 X EBITDA. Kinder Morgan (KMI) has the same EV/EBITDA ratio. Enterprise Products Partners, a top midstream firm I like a lot for its distribution growth, trades only at a slightly lower EV/EBITDA ratio of 9.2 X.

Risks with Williams

Williams is growing its dividend and the company is aggressively acquiring new pipeline assets in order to increase its reach, access new markets and diversify its business. However, the US government may decide to limit the expansion potential of midstream companies over the longer term or decide to place additional taxes on the production, transportation and use of fossil fuels in order to support green energy sources. This would likely hamper Williams’ growth opportunities in the natural gas transmission and storage business.

Williams’ dividend, however, is not at risk. The dividend coverage ratio strongly implies that the dividend can grow in the mid-single digits without limiting the growth budget or the company’s ability to service its debt. What would change my mind about Williams is if the midstream firm saw a drop of is dividend coverage ratio below 1.5 X.

Final thoughts

Williams is a growing midstream business with strong momentum in its core natural gas business, driven by increasing natural gas demand and higher gathering volumes. The MountainWest acquisition adds further transportation and storage capacity to Williams’ portfolio and could further improve the firm’s dividend coverage if the transaction is accretive to EBITDA and cash flow. I believe buying new pipeline and storage capacity at 8 X 2023 EBITDA is a good strategic decision for Williams and it could result in strong EBITDA and available funds from operations growth going forward. Considering that Williams is operating in a booming business, I believe the valuation is very attractive based off of adjusted EBITDA and so are the prospects for continual dividend growth!

Be the first to comment