dbvirago

ZIM Integrated Shipping Services (NYSE:ZIM) has been on investors’ radar, mainly due to its generous dividends in 2022. However, as freight rates collapsed, so did the stock price. The general sentiment towards shipping and containers in particular has been pretty negative lately. However, I think that although the seas will be rough in the short term, ZIM has the necessary characteristics to weather the storm and emerge victorious. New regulations from the International Maritime Organization as well as high average age of the market segment should provide the necessary tailwinds for ZIM and could reward long-term value investors. At the same time, income oriented investors should brace for deep cuts in dividends or even no distributions at all should earnings turn negative in the next few quarters.

Company overview

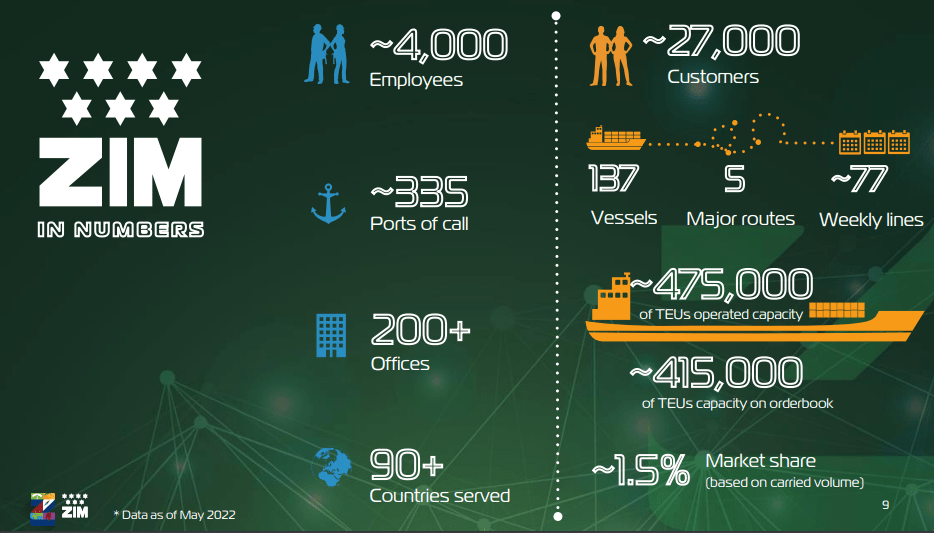

Founded in Israel in 1945, ZIM Integrated Shipping Services is one of the leading container shipping companies with operations in more than 100 countries and tens of thousands of clients. Following its IPO on the NYSE in 2021 caught the wave of rising freight rates and as a result showered its investors with dividends.

ZIM’s business in numbers (ZIM IR)

In 2022, ZIM made four quarterly distributions totaling US$27.55 and bringing the annual gross dividend yield, calculated with the latest share price of around US$17.15 to 160%. It’s very rare to see companies with dividend yields well into the triple digit, so this naturally catches the interest of many income oriented investors.

The changing pricing environment

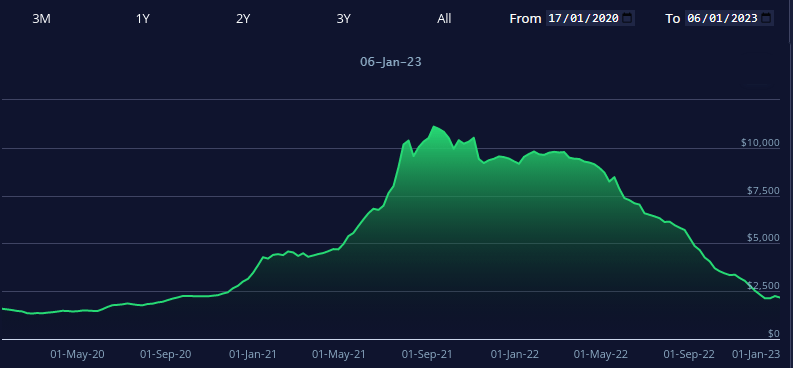

By the end of 2020 and into 2021, the lockdowns introduced by governments to supposedly stop the pandemic and the generous stimulus programs created the perfect storm for container freight rates. On the supply side, many ships were forced to quarantine their staff, due to someone testing positive, while ports were having labor shortages for similar reasons. On the demand side, citizens were using the stimulus checks to make online purchases, which increased demand. As a result, the Freightos Baltic Index skyrocketed x7 from its 2020 levels and reached US$10,800 per 40-foot container.

Freightos Baltic Index (Freightos)

Now that lockdowns alongside stimulus checks, the market is normalizing and freight rates were on a steep decline throughout 2022, especially in H2’22. In the meantime, many shipping companies used the massive cash flows to improve their balance sheets, order new vessels and return capital to their shareholders.

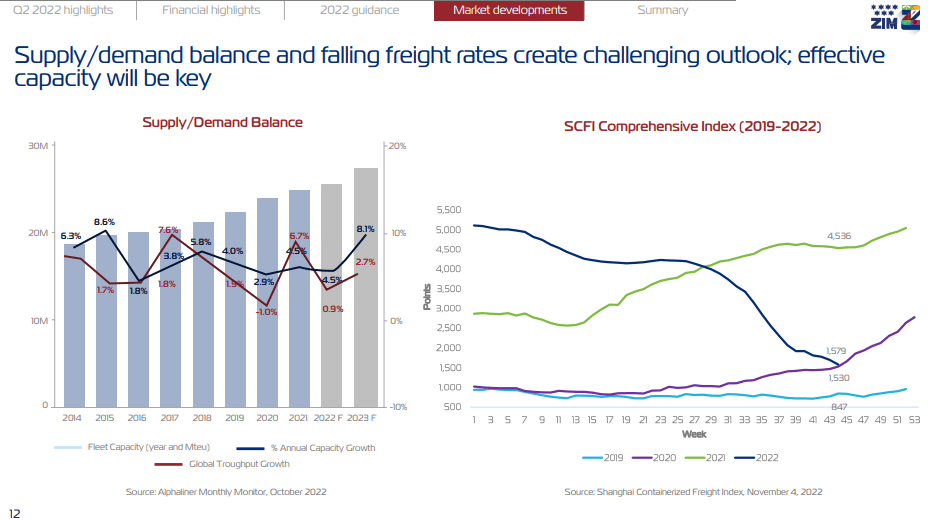

The supply/demand dynamics (ZIM)

As a result, the supply on the container shipping market is expected to increase significantly in 2023, while demand may suffer from global economic slowdown. In light of this, tough times are expected for container shipping companies.

Brace for a dividend meltdown

Looking at the steep decline of freight rates, it’s very obvious that the dividend from 2022 is not sustainable at all. ZIM has indicated that it intends to distribute 30% of its earnings.

Earnings projections (Seeking Alpha)

Looking at analysts’ projections for 2023 and 2024, this implies dividend of around US$0.51/share from 2023’s net income. Note, that the first quarterly payment in 2023 will be made out of Q4’22 net income so the actual distributions in 2023 may be higher. As for 2024, earnings are forecasted to go into the negative territory, which could mean no distributions at all.

ZIM is in a solid position

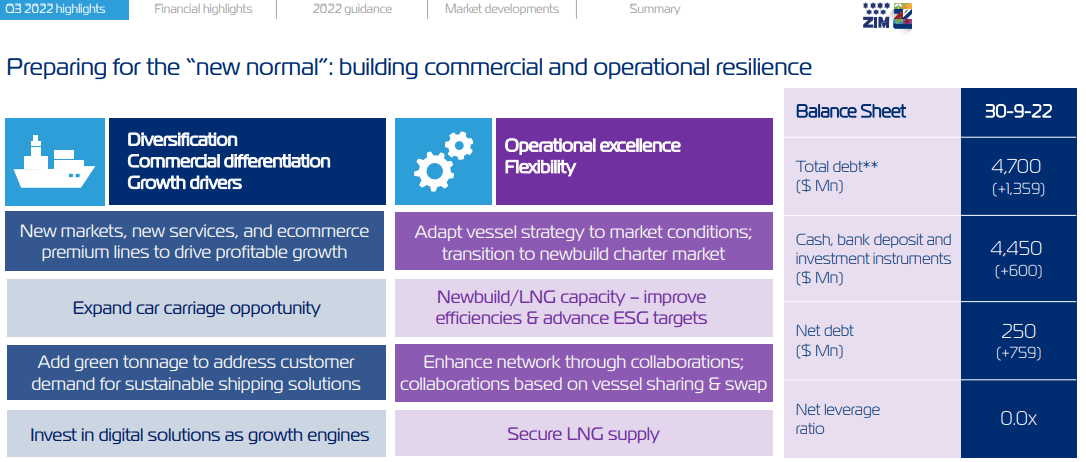

In cyclical industries, when the economic environment worsens it’s crucial for a company to enter the downturn in a strong position in order to weather the storm. I believe this is exactly the case with ZIM as it enters into 2023 in a great shape. As of Q3’22, net debt is standing at only US$250M and the figure may fall further as Q4’22 results are released.

ZIM’s strategy and financial position (ZIM IR)

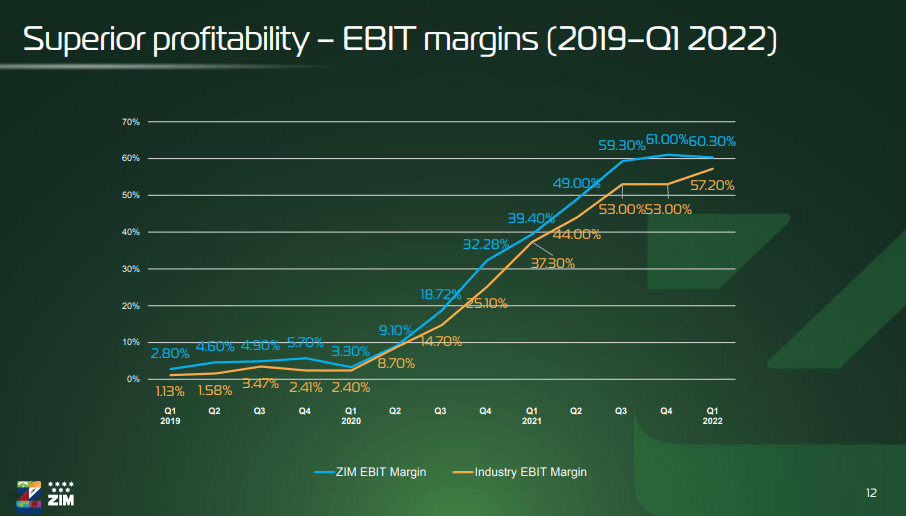

At the same time, management has been very proactive in ensuring that ZIM stays ahead of its peers and is investing into modernization of the fleet with LNG powered vessels, which are superior from an ESG standpoint. A focus has been put also towards utilizing digital solutions to support the main business. In light of this, a few days ago ZIM extended a US$100M credit facility to 40Seas – a fintech company aiming to improve cross-border trade financing. Management’s efforts to stay ahead of the industry have been yielding fruit as ZIM’s margins have been consistently better than the sector even before the sharp rise in freight rates.

ZIM’s EBIT margin Vs peers (ZIM IR)

Tailwinds on the horizon

As part of the global push towards decarbonization, the shipping industry should reduce its emissions by 40% by 2030, using 2008 as a base year. According to Lloyd’s List Intelligence the most effective way to cut emissions will be to reduce the sailing speed of vessels. They estimated that a 10% speed reduction will yield 27% less carbon emissions on average. However, this will effectively reduce the effective capacity on the demand side of the market balance as it will take longer for ships to reach their destinations.

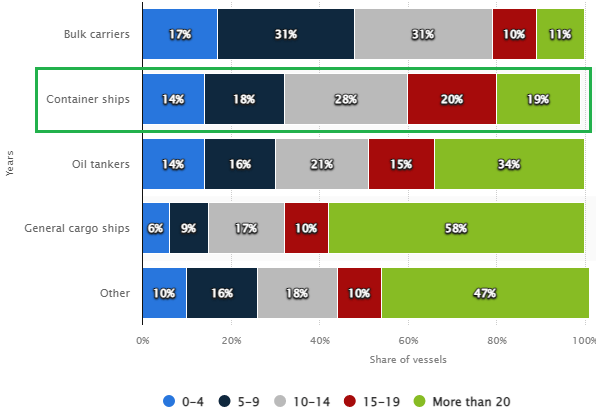

Age distribution of the world merchant fleet in 2022 (Statista.com; Martin Placek)

In addition, older ships will generally have tougher time meeting the carbon targets. At the same time, the container fleet has almost 40% of its ships older than 15 years. As ESG regulations tighten and in a low freight rates environment, those ships may prove to be a burden and some of them may end up being scrapped, reducing supply.

Share price and valuation discussion

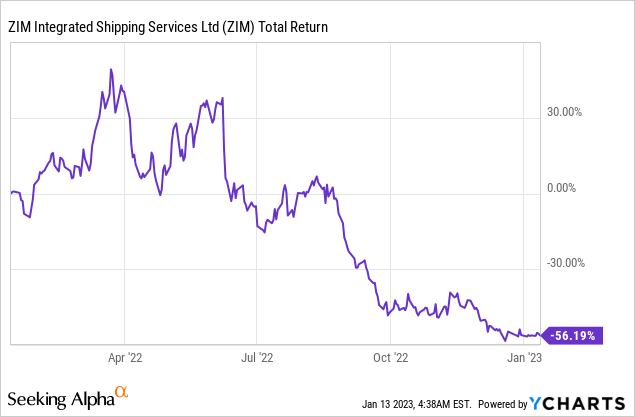

In the last year ZIM’s shares have been on a freefall and shareholder have lost more than 56% even when accounting for the dividends. At the same time the EV of the company is around US$2.3B and using the “normal” 2019’s EBITDA of US$399M, the EV/EBITDA ratio is around 5.75. However, ZIM’s fleet now is larger and freight rates are still considerably higher than in 2019. I think this justifies some upside, which could be achieved once the dust settles and the sentiment towards shipping shifts from the current very negative state. The tailwinds I mentioned should help for this.

Risks

The biggest risk for ZIM is connected to the freight rates. A deep prolonged recession could suppress international trade and reduce demand for container shipping services. Another threat of a similar consequence could be a trend towards deglobalization. While a recession would be temporary and may even lead to higher rates in the aftermath as some of the smaller and weaker companies could go bankrupt and/or scrap their ships, deglobalization could have long-term effects. That being said, as I believe that global trade is of a mutual benefit of the participating parties, it should continue, despite some political pushback towards deglobalization.

Be the first to comment