piranka

The ZeroFox Holdings (NASDAQ:ZFOX) SPAC deal with L&F Acquisition Corp. just closed in August and the stock is already trading far below $10. Not all SPAC deals are horrible, with ZeroFox having a solid business model in the cybersecurity space. My investment thesis is Neutral on the stock trading at a large discount to the $10 SPAC price, but the company needs to better explain updated FY23 estimates.

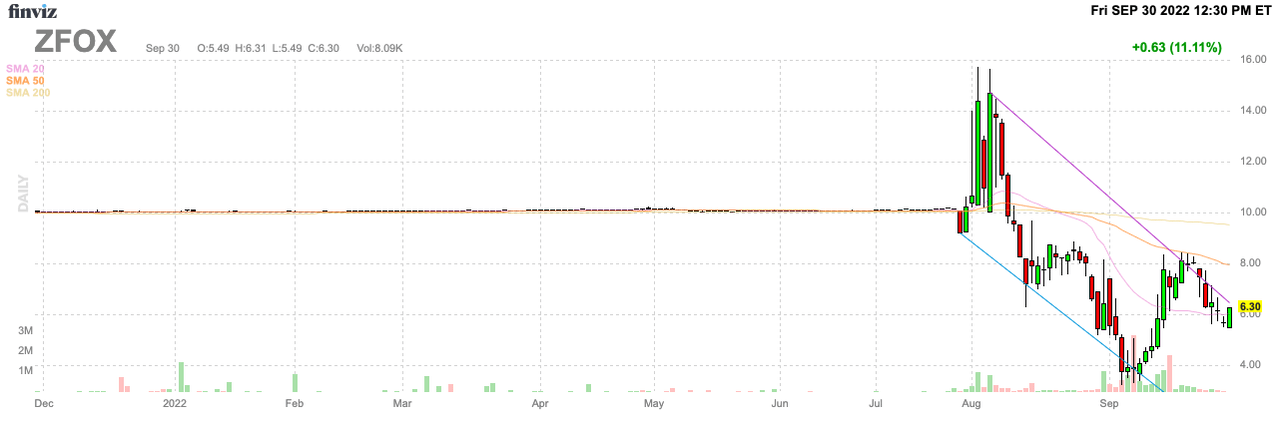

Source: FinViz

Enterprise Cybersecurity SaaS

ZeroFox is a leader in the enterprise cybersecurity space. The company focuses on external threat protection and response capabilities to protect enterprises against the entire lifecycle of external cyberattacks.

All enterprises are in the midst of digital transformations, but the moves expose companies to external security threats. Everything is in the cloud and accessible via mobile along with social media and remote work leading to a business operating far beyond the traditional corporate walls.

ZeroFox uses computer vision and machine learning powered by 20 AI patents to attack the problem at its source. All of the digital platforms from social media to e-commerce and digital currencies are used to transmit malicious payloads.

The company has a blue-chip customer base and forecasted 2022 revenues reaching $150 million and jumping to $195 million in 2023. ZeroFox has a strong retention rate and over 90% of revenues are part of the recurring SaaS model.

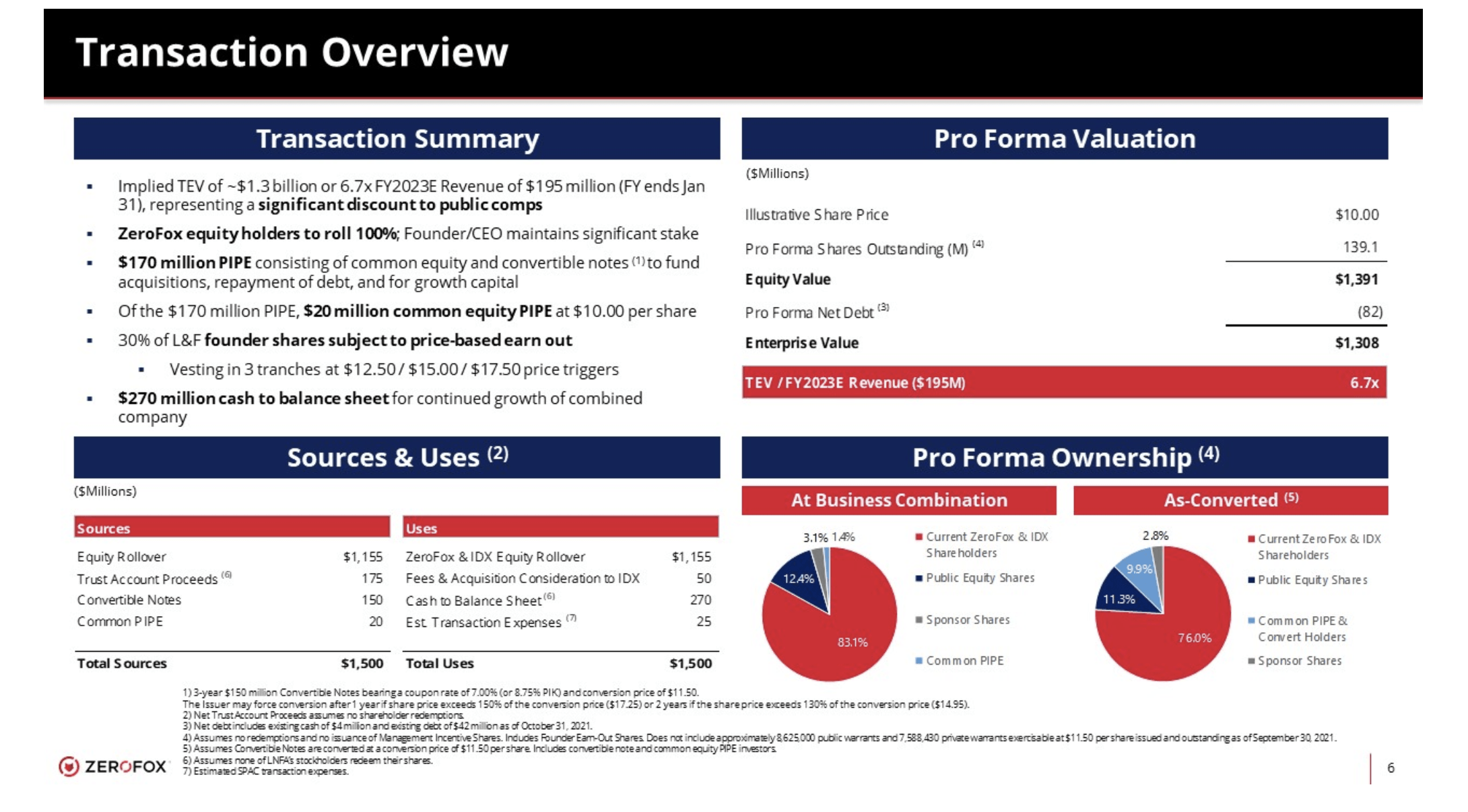

Source: ZeroFox SPAC presentation

As with any cybersecurity firm, ZeroFox is projected for gross margins to reach 70% with strong cash flows down the road. The company remains relatively small, but at least the goal is to generally be cash flow neutral at the start of public life, with a strong cash balance of $270 million.

Along with an SEC filing, ZeroFox lowered the 2H’23 revenue target to a range of $82 million to $86 million. The company blames the timing of investments in growth due to a delay in completing the SPAC deal and the macro environment.

Deal Price Break

ZeroFox had an initial equity value of $1.3 billion based on 139 million shares outstanding. The EV was closer to only $1.0 billion, and of course, these amounts are before including the ~16 million warrants exercisable at $11.50 per share (far out of the money now).

Source: ZeroFox SPAC presentation

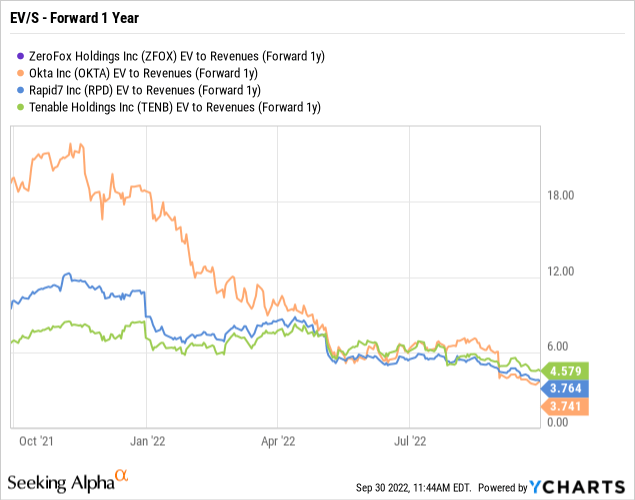

The stock traded above $10 when the deal closed, but ZeroFox quickly plunged below $5. The stock has rebounded slightly now, but the new price has the stock only worth $850 million for an EV/S multiple of just 3x now.

Unfortunately, a lot of the public cybersecurity stocks used by L&F Acquisition in the SPAC presentation of peer stocks fall into similar valuations after the large sell-offs. Okta (OKTA), Rapid7 (RPD) and Tenable Holdings (TENB) have all fallen to around the 4x forward EV/S multiples.

As a newly public company and part of a SPAC deal, the market definitely isn’t going to pay a premium for ZeroFox. The good news though is that these stocks all provide solid values from historical multiples where 10x forward sales were appealing.

Since ZeroFox just completed the deal in early August and is newly public, investors are sometimes wise to watch the company from the sidelines. The going public process can cause management teams to lose focus and disrupt operations.

Along with closing the SPAC deal, ZeroFox discussed identifying 5.8 million attacks and escalating nearly 272K high or critical incidents to customers. The company saw a 125% boost in external attacks and 521% growth in phishing attacks in the quarter.

What the company hasn’t provided investors are updated financials and a complete financial picture outside of updating revenue guidance. As ZeroFox provides more details on expectations going forward, investors can better judge the financial picture of the cybersecurity firm.

Takeaway

The key investor takeaway is that ZeroFox has a compelling investment opportunity, but the company needs to clean up the financial picture before investors can jump into the stock. ZeroFox is up strong on the company lowering revenue targets for FY23 suggesting the stock is too beaten down, but a better understanding of the plans is needed before investing in this tough environment.

Be the first to comment