AleksandarGeorgiev/E+ via Getty Images

A Quick Take On Yalla Group

Yalla Group (NYSE:YALA) went public in September 2020, raising approximately $140 million in gross proceeds in an IPO priced at $7.50 per ADS.

The firm operates a voice-centric social networking and entertainment service that covers the Middle East and Northern Africa regions.

YALA is producing moderate growth and profits while expanding its product offerings further into gaming.

My outlook is a Buy at around $5.00 per share.

Yalla Group Overview

Dubai, United Arab Emirates-based Yalla was founded to develop an online community service focused on the Middle East and North Africa [MENA] region that is built on voice communication rather than just written texting.

Management is headed by founder, Chairman and CEO Mr. Tao Yang, who was previously manager of ZICT Technology Co and vice president of Beijing Feinno Communication Technology.

The company’s primary offerings include:

-

Voice Chat

-

Social Network

-

Entertainment

-

Online Games

-

Gift Exchange

The firm provides its app to users through major mobile platform operators such as Apple and Google.

Management believes there is a ‘significant imbalance between the supply of, and demand for, online social networking and entertainment options in MENA.’

Yalla’s Market & Competition

According to a 2019 market research report by Wamda, Crowd Analyzer, along with Hootsuite and APCO Worldwide, issued a report that analyzed over 172 million social media interactions and concluded that MENA social media users are ‘becoming more active and engaged online where conversations are taking place about brands, business and services alongside fashion, politics and religion.’

User bases have shown growth on nearly every social media platform, and that growth has been driven primarily by Generation X persons.

Notably, Saudi Arabia registered a social media penetration rate of 75%; in Egypt, users were interested in a ‘much broader variety of topics, including politics, religion, sports and social development.’

Major competitive or other industry participants include:

Yalla’s Recent Financial Performance

-

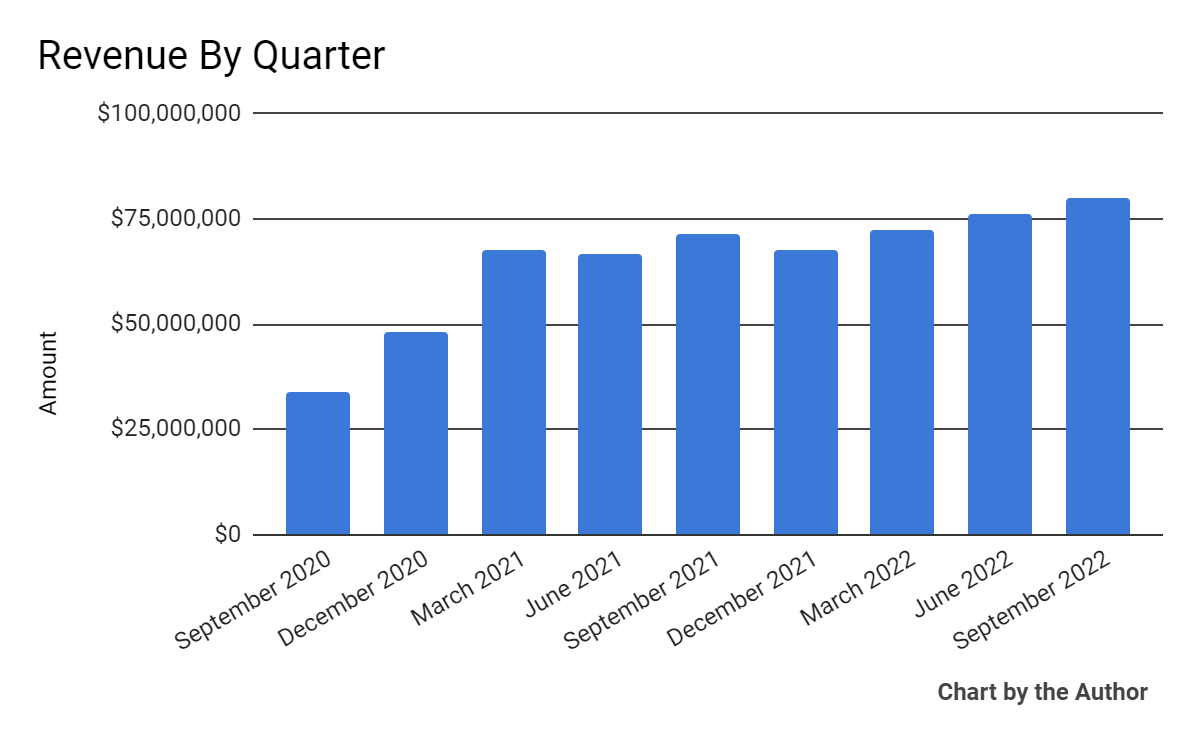

Total revenue by quarter has grown per the chart below:

Total Revenue (Seeking Alpha)

-

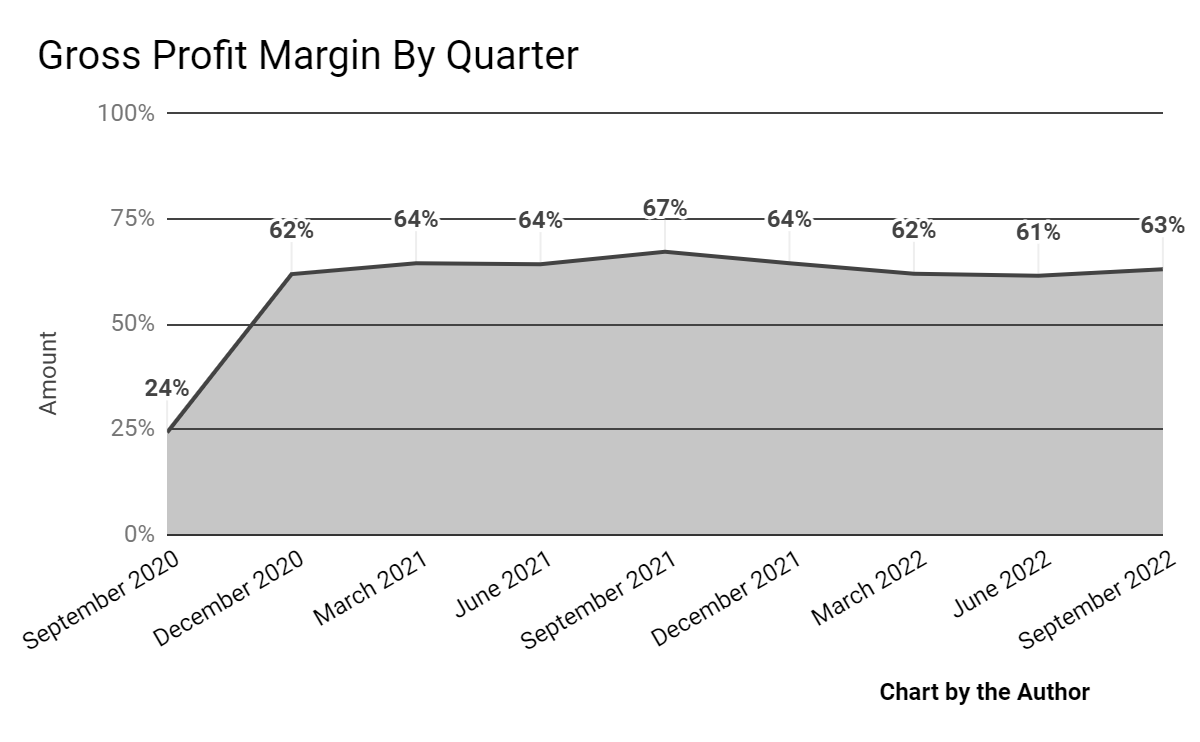

Gross profit margin by quarter has trended lower in recent quarters:

Gross Profit Margin (Seeking Alpha)

-

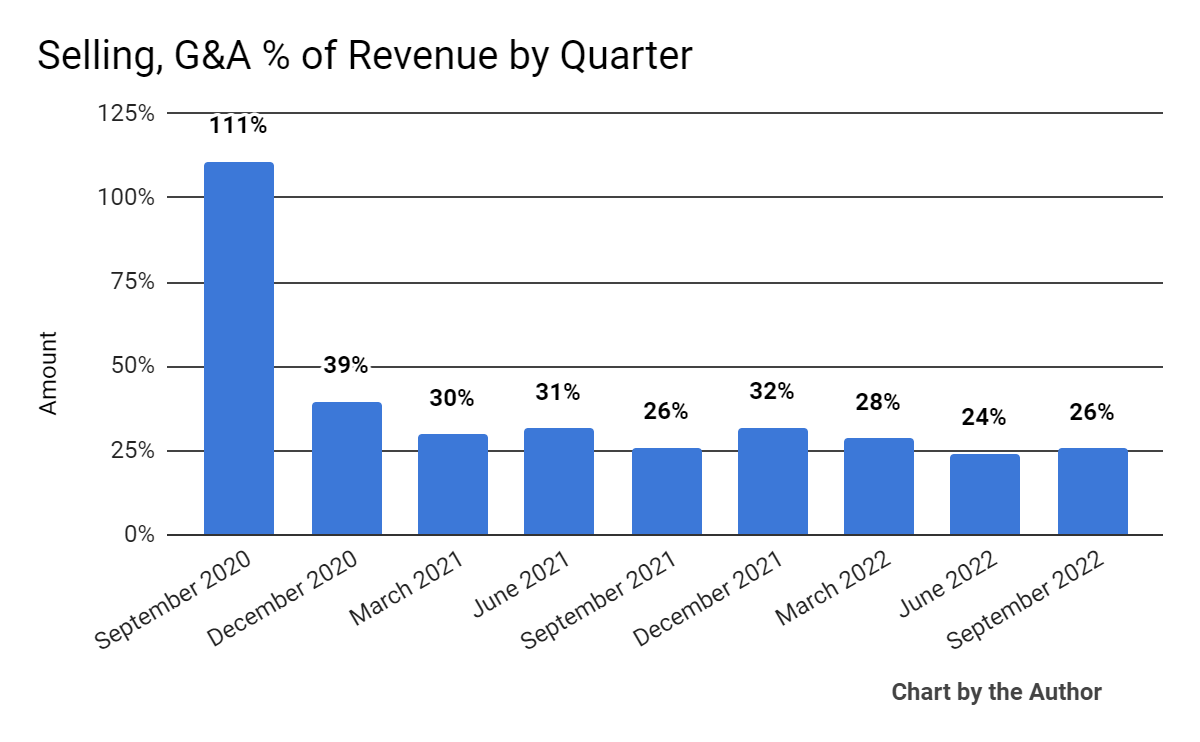

Selling, G&A expenses as a percentage of total revenue by quarter have also trended lower more recently:

Selling, G&A % Of Revenue (Seeking Alpha)

-

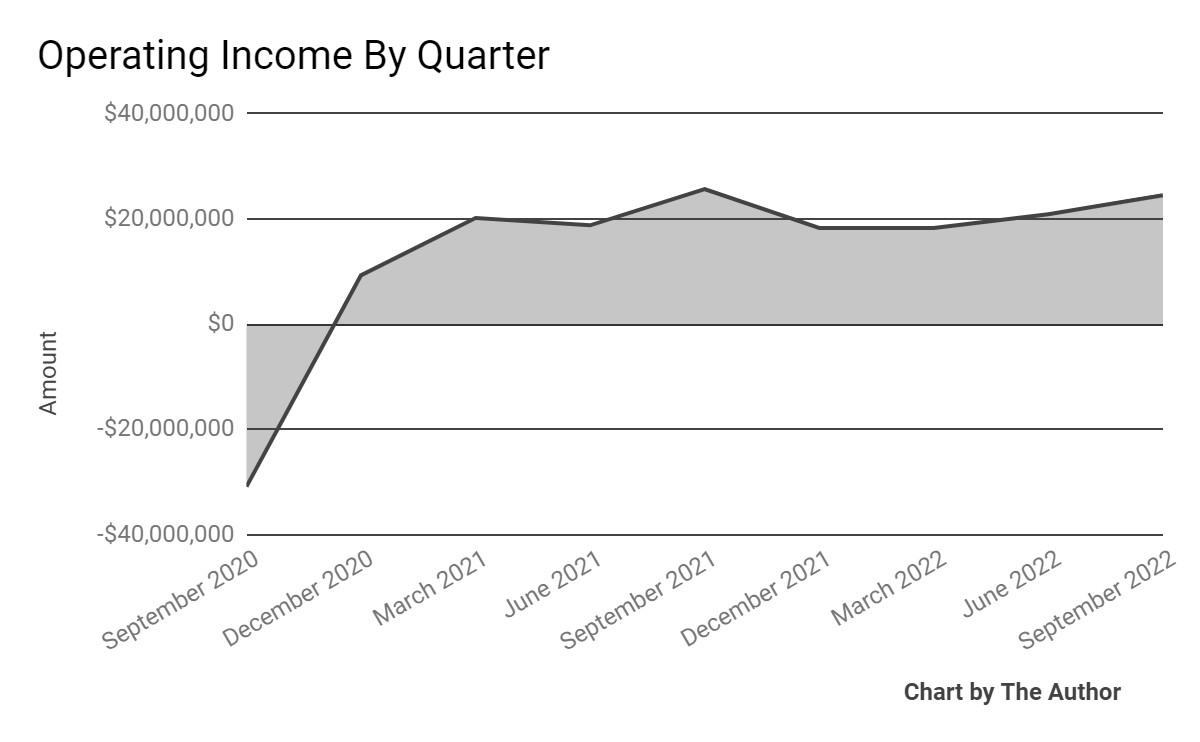

Operating income by quarter has risen in recent reporting periods:

Operating Income (Seeking Alpha)

-

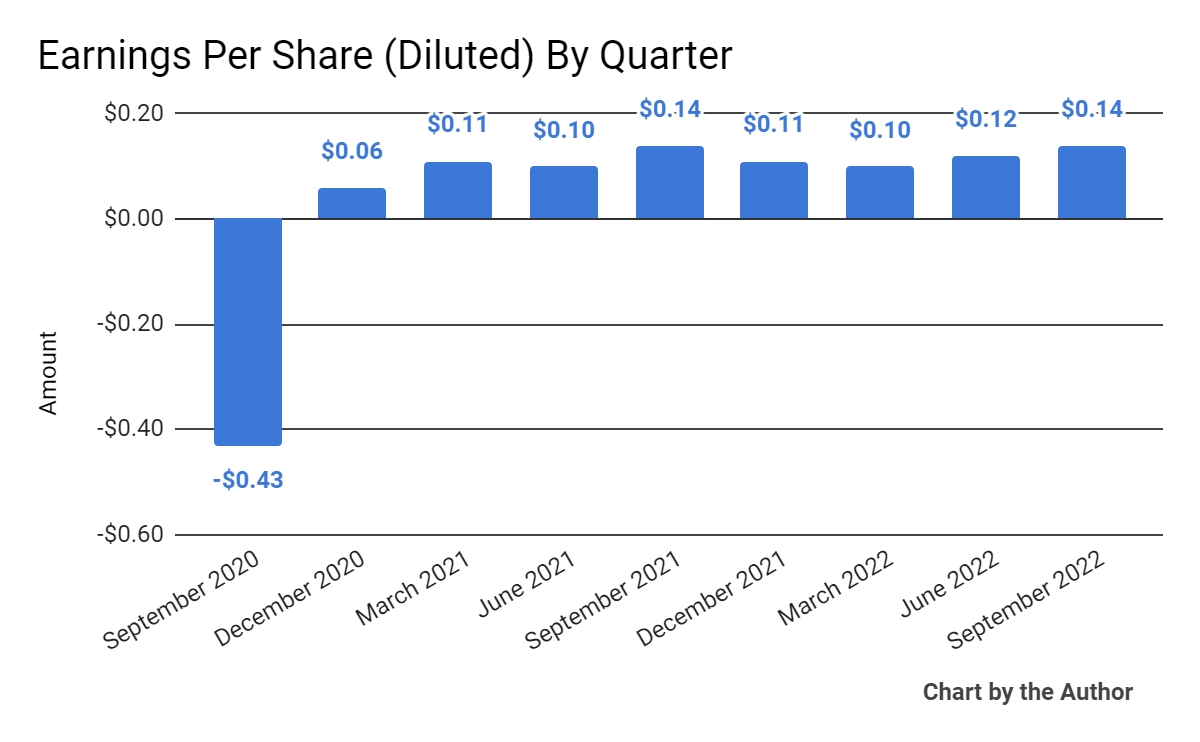

Earnings per share (Diluted) have trended slightly higher recently:

Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP)

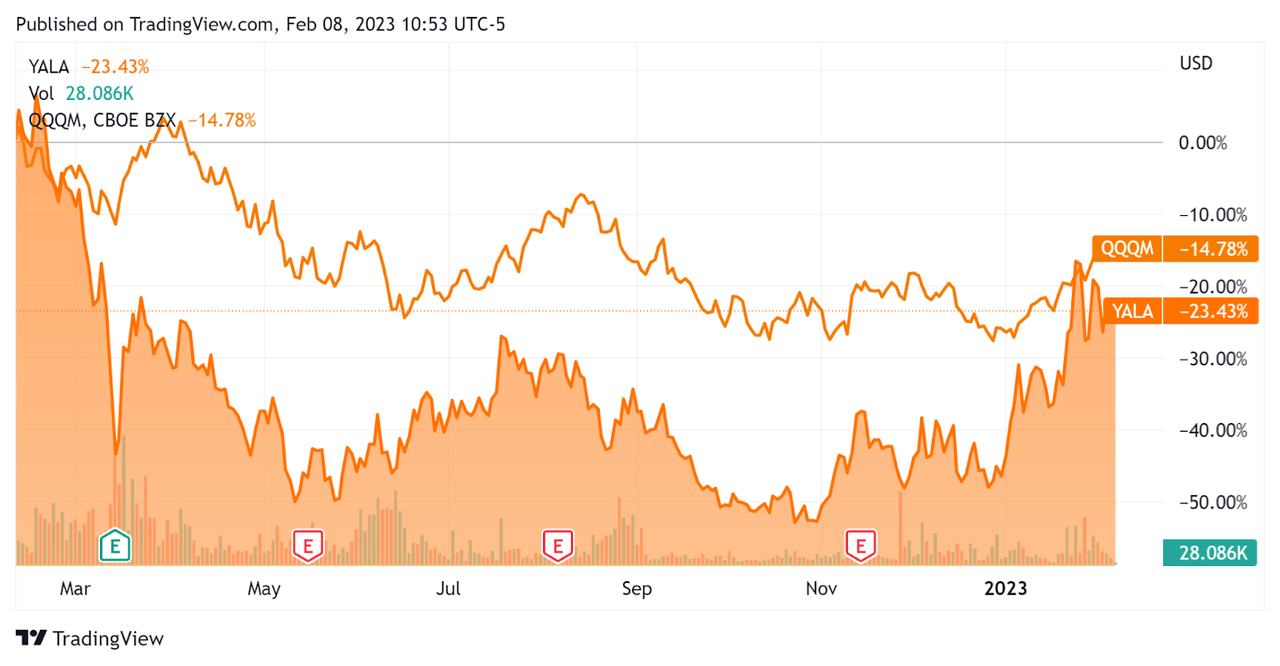

In the past 12 months, YALA’s stock price has fallen 23.4% vs. that of QQQM’s Nasdaq 100 index’s fall of 14.8%, as the chart below indicates:

52-Week Stock Price Comparison (Seeking Alpha)

Valuation And Other Metrics For Yalla Group

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

1.1 |

|

Enterprise Value / EBITDA |

4.0 |

|

Price / Sales |

2.6 |

|

Revenue Growth Rate |

16.6% |

|

Net Income Margin |

27.7% |

|

GAAP EBITDA % |

28.1% |

|

Market Capitalization |

$744,336,830 |

|

Enterprise Value |

$329,164,544 |

|

Operating Cash Flow |

$144,240,944 |

|

Earnings Per Share (Fully Diluted) |

$0.47 |

(Source – Seeking Alpha)

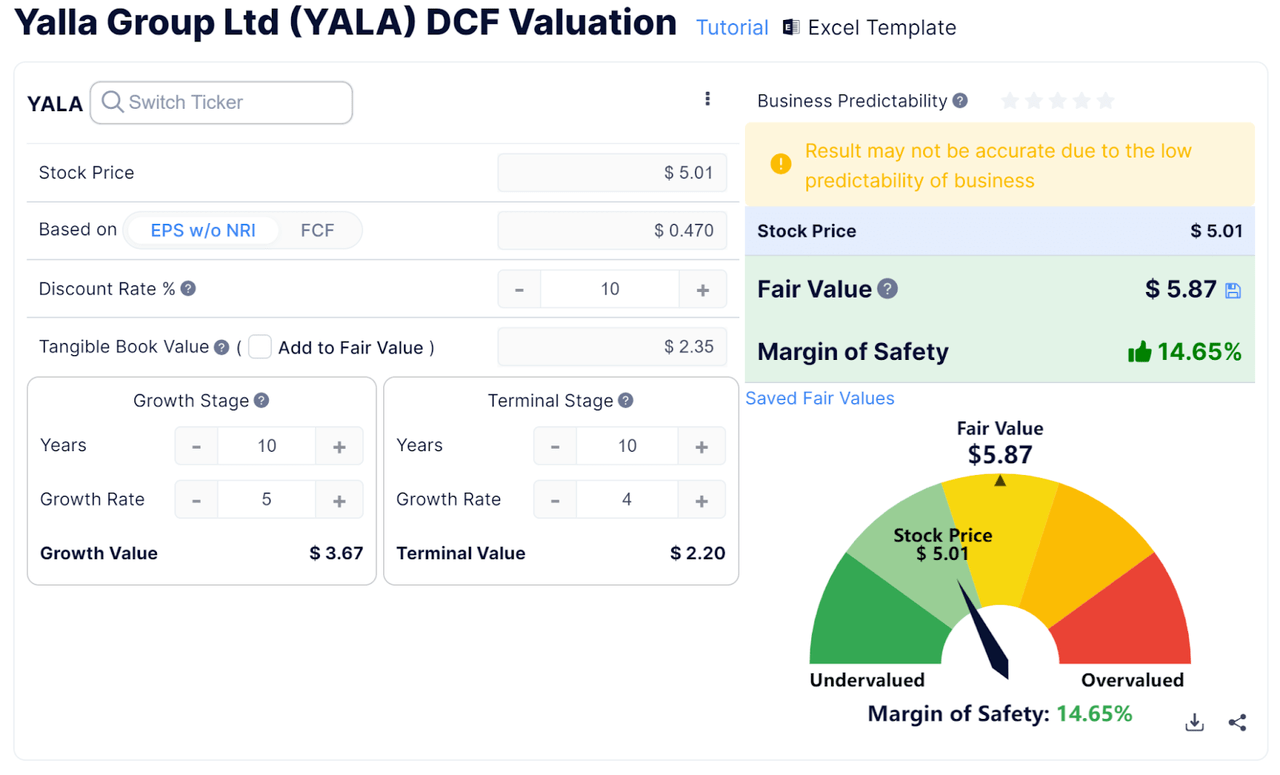

Below is an estimated DCF (Discounted Cash Flow) analysis of the firm’s projected growth and earnings:

Yalla Group Discounted Cash Flow Calculation (GuruFocus)

Assuming generous DCF parameters, the firm’s shares would be valued at approximately $5.87 versus the current price of $5.01, indicating they are potentially currently undervalued, with the given earnings, growth, and discount rate assumptions of the DCF.

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

Yalla’s most recent GAAP Rule of 40 calculation was 44.7% as of Q3 2022, so the firm has performed well in this regard, per the table below:

|

Rule of 40 – GAAP |

Calculation |

|

Recent Rev. Growth % |

16.6% |

|

GAAP EBITDA % |

28.1% |

|

Total |

44.7% |

(Source – Seeking Alpha)

Commentary On Yalla Group

In its last earnings call (Source – Seeking Alpha), covering Q3 2022’s results, management highlighted its revenue growth exceeding the high end of its previous guidance and the third quarter in a row of record revenue for the firm.

The company also featured its Yalla Game offering, ‘to explore the mid-core hard-core game distribution business as a complement to our casual game portfolio.’

Yalla also recently launched its own ‘hard-core mobile game, Merge Kingdom’ in the MENA region.

As to its financial results, total revenue rose 12.3% year-over-year, while monthly active users [MAU] grew 19.1% to 30.9 million.

Management did not disclose any company or revenue retention rate metrics.

Gross profit margin has trended lower in recent quarters, as has SG&A % of revenue costs.

Earnings per share continued to rise sequentially.

For the balance sheet, the firm finished the quarter with cash, equivalents and short-term investments of $416.6 million and no debt.

The company did not provide any cash flow figures for the quarter.

Looking ahead, management expects Q4 2022 revenue to be $73.0 million at the midpoint of the range.

Regarding valuation, the market is valuing YALA at an EV/EBITDA of 4.0x and my discounted cash flow calculation suggests that the stock may be undervalued at around $5.00.

I have previously been bullish on Yalla at around $6.50 per share, and that opinion has been punished by the market.

However, the stock has risen sharply in recent months as the ‘tech penalty’ has begun to diminish.

I believe this will continue to be the case as the year progresses, despite fears of a macroeconomic slowdown.

Technology-centric companies like Yalla that are producing moderate growth along with profits have shown themselves to be more resilient to stock market downturns.

Accordingly, I reiterate my Buy outlook for YALA, at around $5.00 per share.

Be the first to comment