NicoElNino

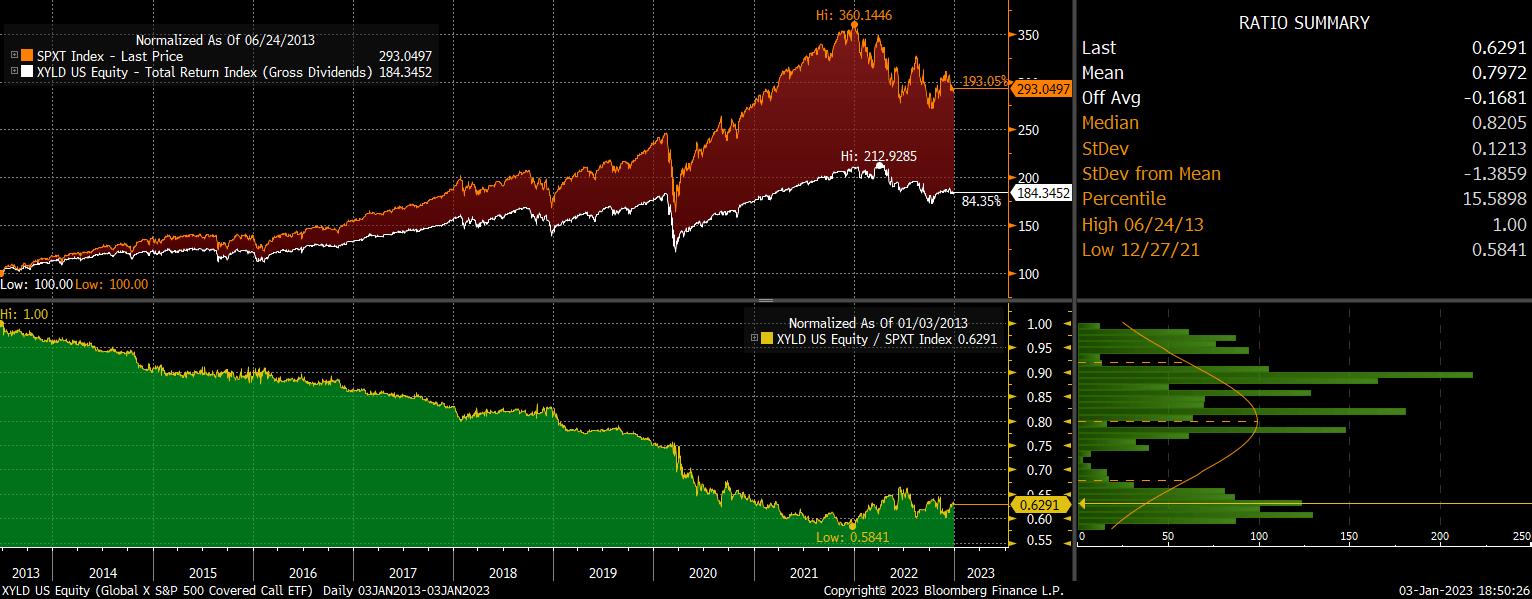

The XYLD ETF is for U.S. focused investors who are happy to miss out on potential upside in favor of generating regular income, and now could be a great time to enter. I have previously recommended the ETF as an alternative to the S&P 500 (see ‘XYLD: A No-Brainer Alternative To The SPX‘), and continue to expect significant outperformance. Not only is the S&P 500 likely to perform poorly over the coming years due to macroeconomic and valuation pressures, but volatility is relatively elevated. Both of these factors suggest the XYLD will outperform significantly over the coming months and years.

The XYLD ETF

The Global X S&P 500 Covered Call ETF (NYSEARCA:XYLD) tracks the performance of the CBOE S&P 500 BuyWrite Index, which holds the S&P 500 and writes calls against it in order to earn the option premium. The XYLD tends to underperform the S&P 500 when the returns it received from option sales underperform the combined returns of the dividend yield, the growth in dividends, and the impact of rising valuations (or falling dividend yield). The main reason for the underperformance in XYLD over recent years has been the significant increase in U.S. dividend payments as well as the rise in equity valuations, which has more than outweighed the impact of higher income on the XYLD. As dividend growth slows and equity valuations decline, the XYLD should outperform, particularly if implied volatility remains at current levels or rises. The fund charges an annual expense fee of 0.6%, which, although high, is likely to be lower than the cost of personally engaging in a covered call strategy.

XYLD Vs SPX Total Return Performance (Bloomberg)

A Good Time To Sell Covered Calls

The first thing to note here is that I continue to believe U.S. stocks are overvalued and will underperform most of the world over the coming years, and so do not outright recommend the XYLD. However, I fully recommend anyone who wants exposure to the S&P 500 to consider shifting to this ETF or one that follows a similar strategy.

Selling call options on an index that one already owns is a good way to generate sustained income but it comes at a cost of missing out on significant bull runs, hence the XYLD’s underperformance since 2009. With that in mind, the best time to sell calls is when you expect there to be a selloff or period of sideways trading. Furthermore, as returns from option sales track implied volatility, a high level of implied volatility is something else to look out for.

Currently, U.S. stocks remain overvalued, with the S&P 500 trading at 17.5x forward earnings despite profit margins being over 50% above long-term averages and real bond yields remaining near decade highs. These are the conditions for weak future returns, and I would not be surprised to see 2023 be a repeat of 2022 as the Covid bubble continued to unwind.

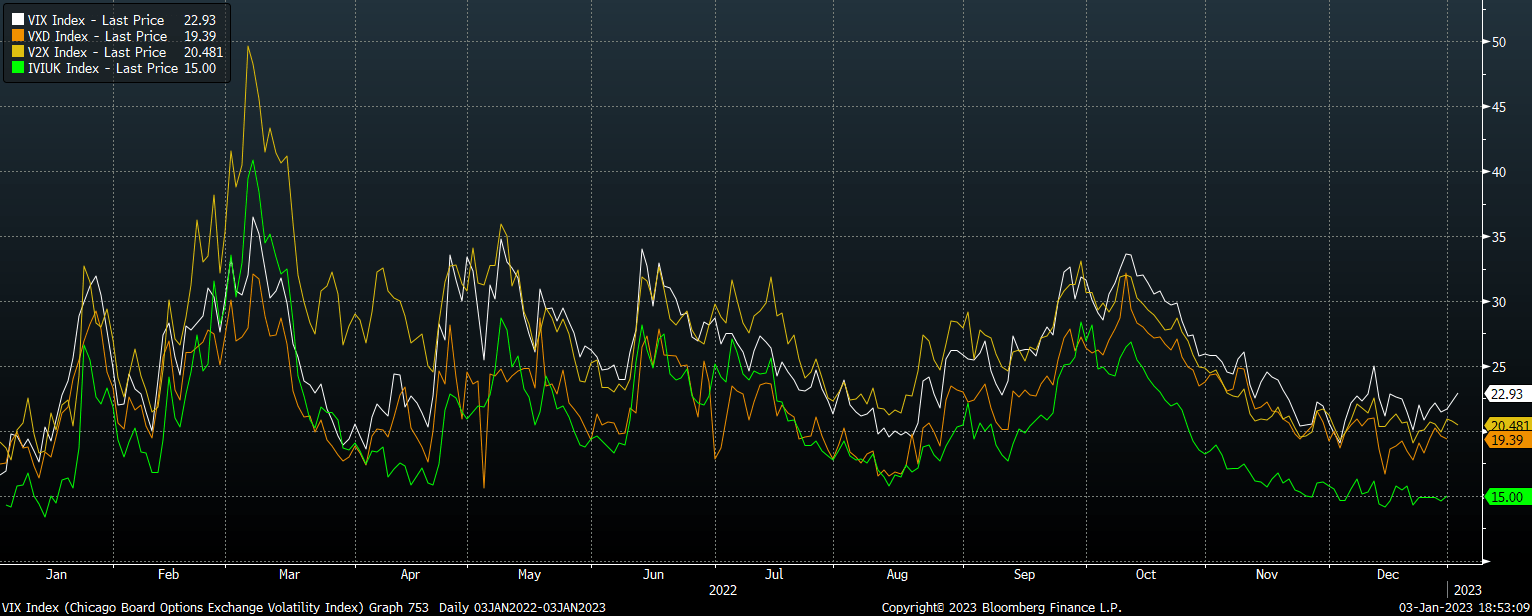

As for implied volatility, the CBOE Volatility Index is trading at 22.9, which compares to a mean figure of 19.7 and a median of 17.8 going back to 1990. This above-average level of implied volatility is significantly higher than European markets at present as shown below and suggests that option premiums will be proportionally high.

Implied Vol for SPX, DOW, FTSE, and STOXX (Bloomberg)

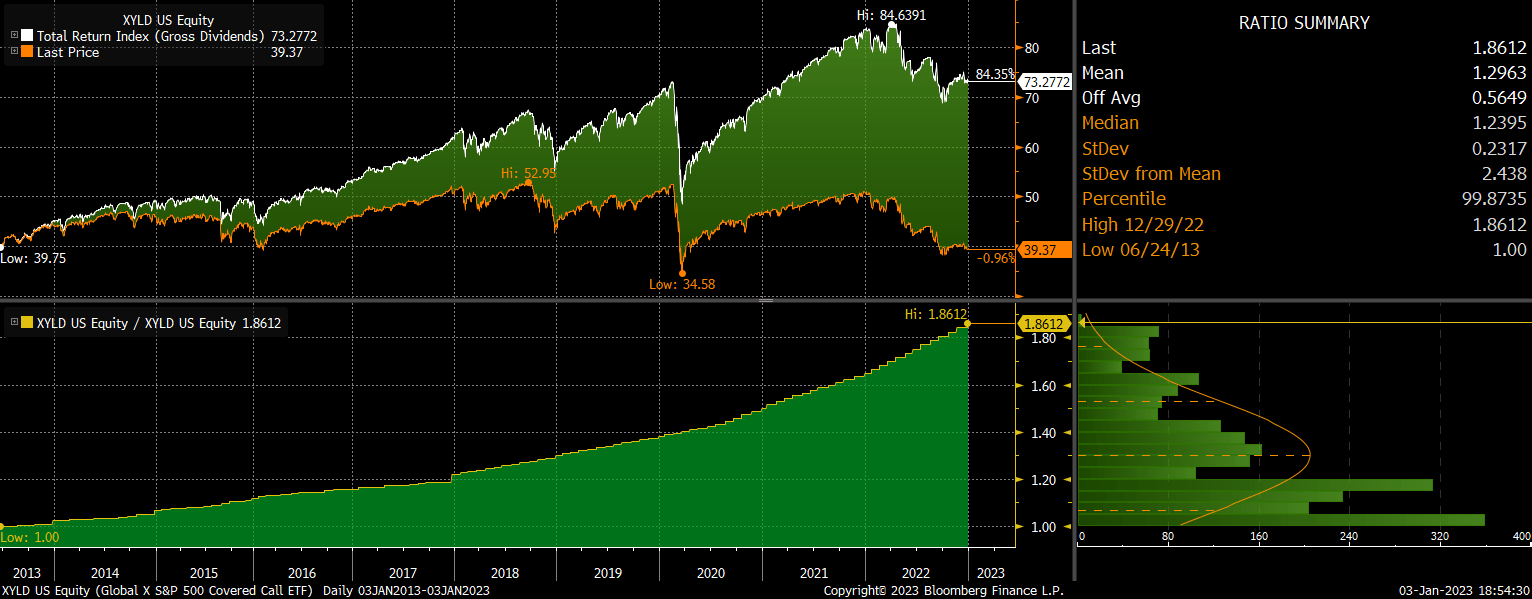

Since its inception in 2013, the XYLD has generated 6.5% annual returns, entirely from its income from call selling. Over this period, the mean and median VIX levels were 17.9 and 15.9 respectively, suggesting option sale returns should be even higher than 6.5% going forward. This is likely to see the XYLD significantly outperform the S&P 500, and depending on how the S&P 500 itself performs, the XYLD could easily also outperform Treasuries.

XYLD Returns From Capital Gains And Income (Bloomberg)

Summary

The days of XYLD’s underperformance relative to the S&P 500 are likely over as the latter faces growing headwinds from elevated valuations, weakening growth, and rising real borrowing costs. The income provided by the XYLD call selling strategy is likely to far outweigh any positive returns that the S&P 500 manages to eke out, particularly with the VIX at above-average levels.

Be the first to comment