eholhos/iStock via Getty Images

Investment Thesis

XPEL (NASDAQ:XPEL) is an automotive surface and paint protection film company, and their products protect painted surfaces from rock chips, bug acids, and road debris. They are the leader in the industry, and their business has been growing rapidly. Meeting demand to protect passenger vehicles from slight abrasions, scratches, stone chipping, and bugs, I expect XPEL to continue its growth trajectory in the future. I believe XPEL is a great option for a growth-oriented investor because:

- XPEL management’s strategic expansion plan is working great, and their revenue will continue to grow at a healthy pace.

- Revenue from the high-margin service segment has been growing, and the overall margin has been improving.

- Macro tailwinds from improving new car production and collaboration with Rivian (RIVN) will positively contribute to growth.

Rapid Growth and Expansion Plan

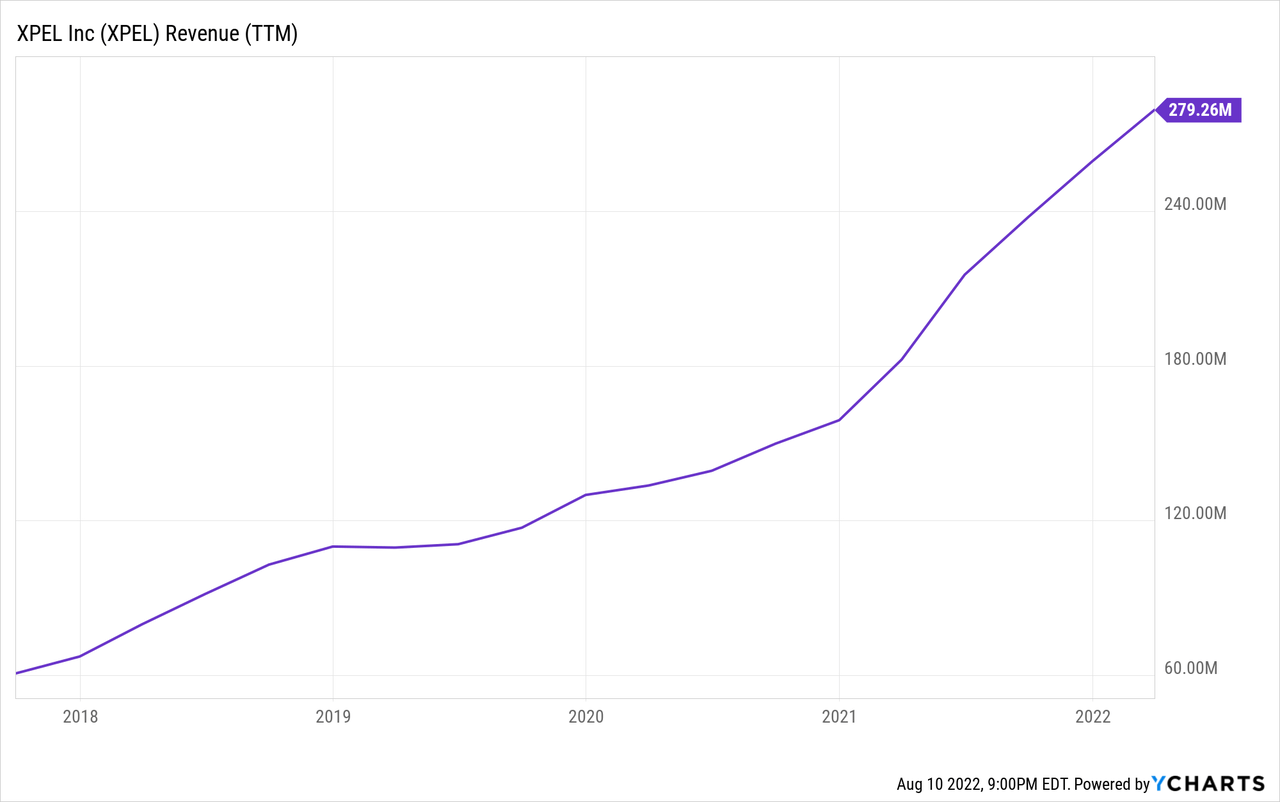

XPEL has been organically growing at a rapid pace in the past several years and has also added key acquisitions (7 acquisitions in 2021 alone). XPEL’s management is executing on several key strategic initiatives. The first one is to establish a local presence at global locations. The presence of physical locations will allow them to better control the delivery of products and services. The second one is to expand delivery channels through an international partnership. This expansion enhances their global reach while allowing them to tailor their distribution model to their target markets. Lastly, they continue to expand their non-automotive product portfolio, geared towards films for architectural windows, solar, and bikes.

Thanks to this strategic expansion plan and their superb products, their revenue has been rising rapidly. Also, XPEL has been establishing their presence around the globe, and all of their locations have been growing nicely (except for China due to the Covid lockdown). The strong performance around the world resulted in 22% revenue growth YoY in 2Q 2022, and I expect the positive trend to continue well into the future.

Revenue Breakdown by Region (SEC Filings)

Improving Margin

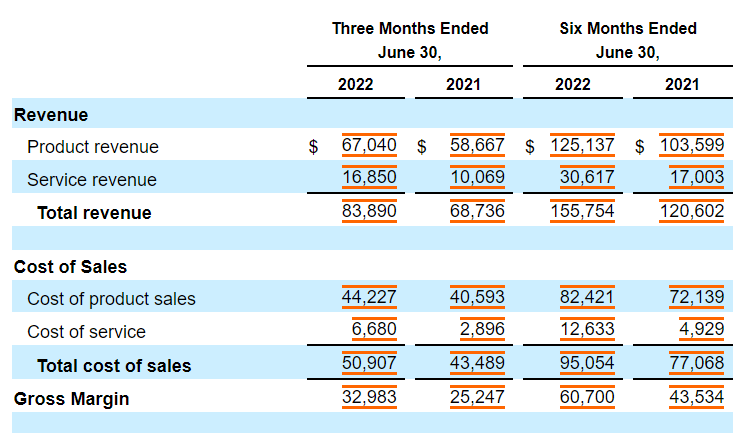

Not only has XPEL been growing rapidly, but they have also been improving margins as well. On the product side, management mentioned in SEC filings that the improvements came from a favorable product mix as well as lower product costs. Improving margins on the product side is certainly a great sign and will contribute positively towards their goal of a 40% gross margin. However, in my opinion, the biggest contributor to their overall margin improvement is the expansion of their service segment.

As mentioned before, XPEL has been busy acquiring key businesses, and the acquisition of PermaPlate and Tint Net acquisitions in 2021 allowed XPEL to add a third-party labor option to their service portfolio. Thanks to this addition, XPEL’s service revenue (particularly the installation labor segment) more than doubled in 2021 compared to 2020 ($24 M in 2021 and $10 M in 2020), and this trend continued into 2022. The service business is a higher margin segment, so this significant growth in services resulted in an overall margin improvement.

Income Statement of XPEL (SEC Filings)

Macro Tailwind and Rivian Deal

In the past couple of years, XPEL has been dealing with severe headwinds. One major one is the Covid lockdowns. Especially, the recurring lockdowns in China (their #2 market) have significantly impacted their revenue. Sales outside of China have recovered nicely so far, so I expect the Chinese market to start improving as Beijing and Shanghai start to ease their lockdowns. Also, new car production has been low, due to chip shortages and supply chain issues, bringing another heavy headwind to XPEL. Now, supply chains are showing some signs of improvement, so I expect the new car production rate to rebound.

In other news, XPEL and Rivian recently announced that XPEL will be the exclusive supplier of protective paint films for Rivian. Rivian is on track to produce 25,000 vehicles this year, and this number should only increase in the coming years. Also, this is a high-profile deal that should generate publicity and customer awareness for XPEL products, bringing future deals to the table.

Intrinsic Value

I used a DCF model to estimate the intrinsic value of XPEL. For the estimation, I utilized EBITDA ($51.3 M) as a cash flow proxy and current WACC of 8.0% as the discount rate. For the base case, I assumed EBITDA growth of 50% (current seeking alpha estimate) for the next 5 years (zero-growth for the terminal value). For the bullish case and very bullish case, I assumed EBITDA growth of 52% and 54%, respectively.

The estimation revealed that the current stock price represents 60-80% upside. Given their well-managed growth trajectory and improving macro conditions, I expect XPEL to achieve a nice upside in the future.

|

Price Target |

Upside |

|

|

Base Case |

$128.62 |

59% |

|

Bullish Case |

$136.86 |

69% |

|

Very Bullish Case |

$145.54 |

80% |

The assumptions and data used for the price target estimation are summarized below:

- WACC: 8.0%

- EBITDA Growth Rate: 50% (base case), 52% (bullish case), 54% (very bullish case)

- Current EBITDA: $51.3 M

- Current Stock Price: $80.99 (08/10/2022)

- Tax rate: 20%

Separately, I performed a downside calculation based on XPEL’s beta (1.59) using S&P 500’s standard deviation (~6%, past 12 months). This calculation suggests a potential downside of -19% (with 95% confidence level). XPEL is a small cap growth stock, so the potential downside is rather large. However, the upside is much greater than the downside over the long run.

Cappuccino Stock Rating

| Weighting | XPEL | |

| Economic Moat Strength | 30% | 4 |

| Financial Strength | 30% | 4 |

| Growth Rate vs. Sector | 15% | 5 |

| Margin of Safety | 15% | 5 |

| Sector Outlook | 10% | 4 |

| Overall | 4.3 |

Economic Moat

XPEL has a pretty clear economic moat in the protective film industry. 3M and XPEL are considered leaders in this industry, and, through an aggressive growth plan and acquisitions, XPEL has been strengthening their economic moat. Their profit margins (EBIT, EBITDA, and Net Income margins) are clearly higher than the sector median.

Financial Strength

XPEL has a pretty solid balance sheet. Their long-term debt to total capital ratio (31.25%) is quite low, and covered ratio of 88.58x shows that they are managing their debt level very well. Altman Z-score of XPEL (16.18) clearly demonstrates that they are nowhere close to financial distress (below 2).

Growth Rate

The business has been rapidly growing. Covid lockdowns and supply chain issues have slowed their growth a little bit in the past couple of years, but I expect them to resume superb growth in the future.

Margin of Safety

Being a small cap growth company, their stock price will go up and down with the market. However, the upside far outweighs the downside created by the sensitivity to market volatility.

Sector Outlook

The automotive protective film industry is growing every year, and increasing demand for surface protection should drive further gains. It is expected to grow 6.2% CAGR until 2028. The industry won’t see explosive growth like some tech companies, but it will add enough market space for XPEL to continue its growth for a while.

Risk

XPEL’s product is a consumer discretionary item, so consumers’ level of disposable income affects company revenue. As all of us know, inflation is running high, making consumer sentiment very jittery. Also, some economists are predicting a recession later this year. An economic slowdown will impact spending in consumer discretionary segments more severely than others.

In China, and other regions, lockdowns are easing, but the pandemic is, by nature, hard to predict. Also, some states have declared a state of emergency due to Monkeypox, which may result in travel restrictions in the future. Travel restrictions and lockdowns will reduce demand for new cars, and, therefore, negatively impact XPEL’s business.

Conclusion

XPEL has been growing rapidly in the past several years. Covid lockdowns and supply chain challenges slowed their growth some, but they are about to resume their explosive growth again. With a well-defined economic moat and strategic growth plan, I expect them to continue their well-managed growth trajectory. Overall, I expect 60-80% growth from XPEL in the long run.

Marketplace In Preparation

Thank you all for reading my article. I’m in preparation for a Marketplace launch soon. Please get excited! Also, let me know the types of analysis or information you would like to see more of in my articles. I will take that into consideration for the marketplace. Thank you all for your support!

Be the first to comment