AsiaVision

Main Thesis / Background

The purpose of this article is to evaluate the Consumer Discretionary Select Sector SPDR ETF (NYSEARCA:XLY) as an investment option at its current market price. This is a fund that seeks to “provide precise exposure to companies in retail, hotels, restaurants and leisure, textiles, apparel and luxury goods, household durables, automobiles and auto components, distributors, leisure products, and diversified consumer services.”

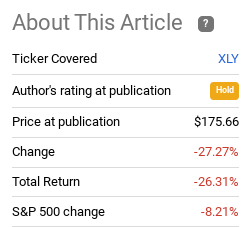

I have generally taken a cautious approach to XLY. While it has been a while since I last covered it, I suggested back in mid-2021 that readers avoid this ETF. In hindsight, I was correct in this outlook, although I should have been even more bearish!

Fund Performance (Seeking Alpha)

With 2023 right around the corner, I thought it was time to take another look at XLY. The fund has performed very poorly in 2022, but that can often mean a turnaround is going to be in the near future.

In my view this is precisely what is going to happen. Consumer stocks face some serious headwinds – from inflation, a weakening job market, and recessionary threats – but the value has started to materialize for those who can withstand the risk. I do not see this as an ideal option for everyone, but for those who are into contrarian plays this definitely fits the bill. Therefore, I am upgrading my rating to “buy” and will explain why in detail below.

Buying The Unloved

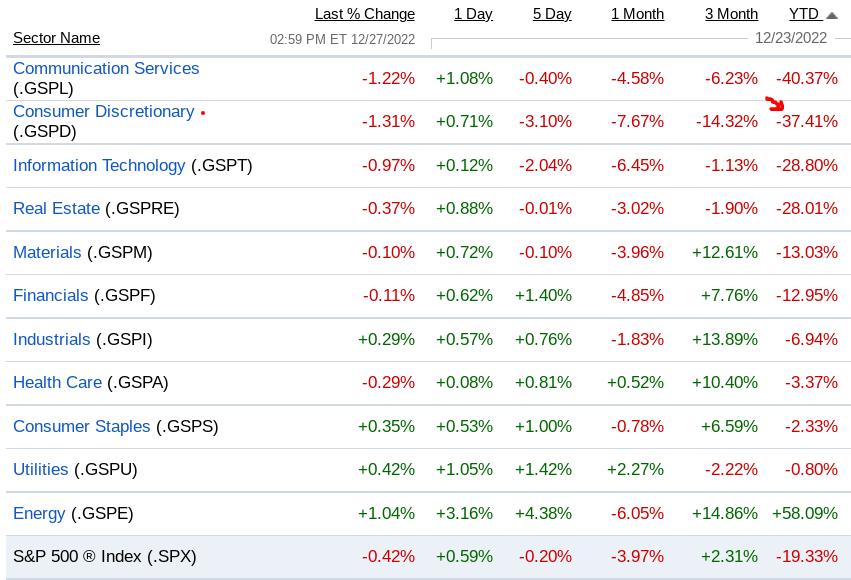

An initial look at XLY should consider where we stand as 2022 comes to a close. Simply put, this is tracking one of the worst performing asset classes of the calendar year. With consumers pressured by war in Europe, rapid inflation across the board, and declining household sentiment, it should not be too surprising that retail/consumer discretionary plays came up short. But it is the how short that really tells the story. Consumer Discretionary was the second worst performing sector, only behind Communication Services, and has seen a loss double that of the S&P 500:

Sector Performance (2022) (Fidelity)

The unfortunate reality is XLY followed this trend very closely, dropping by over 39% since January 1:

YTD Performance (XLY) (Seeking Alpha)

This may be enough to scare some readers away. Truth be told – I wouldn’t blame them. Such sharp losses can unnerve even the most sophisticated of investors and it reminds us quite clearly how money can evaporate in a short time period. This is a point to emphasize because while I am bullish on XLY now, recent history shows that losses can be large and can come quickly. If this is something you are not prepared for, then perhaps it is best to avoid this sector going forward.

For me, and I would suspect many others, such large drops begin to pique the mind’s interest. Looking back at history most sectors do not stay “unloved” forever. Seeing such sharp under-performance often results in an “alpha” generating contrarian play. That is what I expect here. Bear markets can be hard to time the end of, but buying along the way often leads to out-sized gains once the trade ultimately reverses. I see the potential for this to repeat in the case of XLY, so I see this weakness as a buying opportunity.

Retail Sales Were Solid This Holiday Season

Let us now examine the why behind a more bullish outlook. After all, I’m sure readers are viewing the same news headlines I am – most of which are quite negative. There is the strong probability of a recession ahead, inflation remains high, and consumers are cautious. How can this be good for retail?

In short, it isn’t, but I don’t believe the story is as bad as most believe. This is an important distinction. I don’t see this sector as a stellar opportunity inherently. The key is I think there is opportunity because the sector has dropped 40% while at the same time there is some good news we can focus on. There is a disconnect (in my view) between how the shares of XLY have performed compared to how bad the retail/consumer outlook really is. That is the point of emphasis.

This begs the question – where is this supposed good news? One place we can look is U.S. retail sales this holiday shopping season. According to a report from Mastercard Inc. (MA), retail sales rose 7.6% from Nov. 1 – Dec. 24, a timeframe that encompasses most of the holiday season. This is a good representation of how seasonal shopping fared as a whole in America:

Retail Sales Snapshot (YOY) (Mastercard)

This report shows broad gains in 2022 compared to last year. More high-end products like electronics and jewelry did see declines. So that is something to watch closely in the new year. But total retail sales were up strongly and in many different categories. It shows consumers were willing to go out and spend, albeit many were lured by some sharp discounts at major retailers. Still, it sets us up well for 2023 in the fact that things were not as bad as some market participants feared. We have not seen much of a post-shopping “bump” in consumer share prices, suggesting to me there is still time to invest in this sector without overpaying.

Job Seekers Still Have The Upper Hand

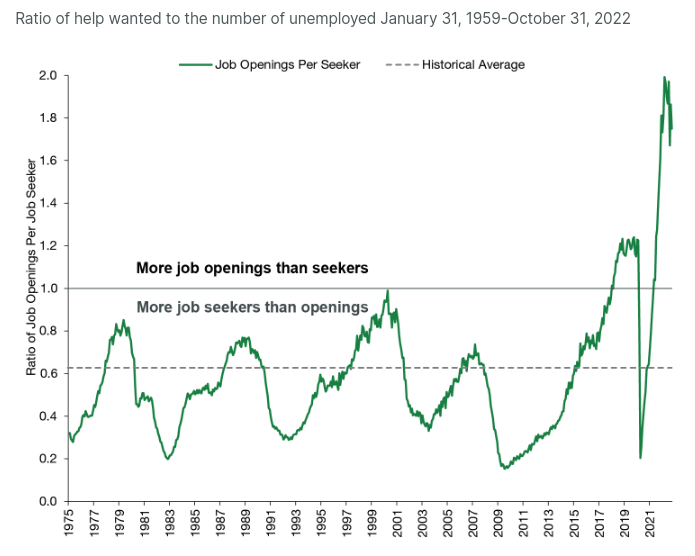

Another bullish point relates to the labor market. The dynamic here could impact how households in the U.S are able to cope with inflation next year. This is part of a broader trend that has remained in place since the early onset of the Covid pandemic. The labor market has become disconnected in a way that actually favors job seekers and those currently employed. Historically, the number of jobs available and the number of job seekers has moved in a fairly defined range. However, over the past year, a drop in labor force participation has pushed the number of jobs available per job seeker to a historic high. While this figure has cooled a bit recently, it is still well above the norm:

Ratio of Job Seekers To Job Openings (St. Louis Fed)

Now, I am not suggesting this is inherently a “good” thing. In my opinion a healthy labor market should be trending more in-line with historical averages so that neither employers nor employees have too much leverage. But we are where we are. This means employees have a bit more negotiating power when demanding pay raises in their current jobs or when contemplating switching employers. This should put wage gains in a strong spot in early 2023, supporting continued retail sales growth like what we have experienced in the last two months.

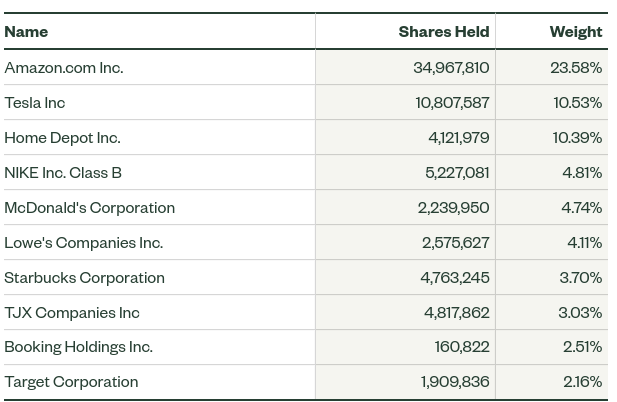

Remember This Is A Top Heavy Fund

I have shared a few reasons why I am bullish on XLY in the short-term. But I want to remind readers that this is a very top-heavy fund. This is one of the attributes that has turned me off in the past, but I think the top names here have enough inherent value that buying them (and XLY by extension) make it worth it. But concentration risk remains a key consideration, so it bears repeating that this make-up might not be for everyone:

XLY’s Top Holdings (State Street)

Fortunately there are plenty of other names in the fund besides the top two. McDonald’s (MCD) happens to be one of my top recession picks and Nike (NKE) just reported strong earnings. So there are pockets of positively within the top holdings even if we look past Amazon (AMZN) and Tesla (TSLA).

Be that as it may, I don’t want to give any illusions here. XLY is heavily exposed to AMZN and TSLA, especially AMZN, both of which have been poor performers this year. That could very well continue into January, so readers need to evaluate this product carefully before buying in.

XLY Actually Saw Strong Dividend Growth YOY

My last topic on XLY looks at the fund’s dividend. This is generally not a subject of much concern when looking at consumer-oriented sectors. Investors have plenty of places to look if income is their objective. Still, I always contemplate the dividend story for any fund I cover. With respect to XLY, I was quite surprised to see such a favorable backdrop in 2022:

| 2021 Distributions | 2022 Distributions | YOY Growth |

| $1.09/share | $1.28/share | 17% |

Source: State Street

My takeaway here is there is more strength in the underlying companies in XLY’s portfolio than perhaps investors may realize. This was a difficult year for many reasons, but the underlying holdings still pumped out strong dividend growth. This highlights some prudent cash management skills and also a willingness to return this cash to shareholders. XLY is by no means an “income play” – I am not suggesting that. But the strong level of dividend growth gives me confidence in the companies within this ETF. That is often more important than the actual income itself.

Bottom-line

With all the global headwinds facing the market it may seem counter-intuitive to recommend XLY. I would generally be in the “avoid” camp on this one myself, but the drop near 40% for the year is too large to overlook. Yes, the outlook is extremely cloudy, but there are bright spots to consider too. This tells me an upswing could be on the way.

Among the positives are strong retail sales figures for this holiday season, continued strength in the labor market that is benefiting job seekers and wage-earnings, and also a decline off the peak in inflation figures:

Inflation Rate (Bureau of Labor Statistics)

When I factor all this in, I believe we could see a push higher in XLY in the coming months. As a result, I am shifting my recommendation to “buy” on this ETF, and suggest readers give this idea some consideration at this time.

Be the first to comment