Guido Mieth

Apartment Income REIT Corp (NYSE:AIRC) was formed at the end of 2020 when Apartment Investment and Management Company (“Aimco”) completed a spinoff of their multifamily portfolio.

AIRC or AIR, as is referred to in company filings, is now a competitive publicly traded operator of multifamily properties containing a collective total of over 20K apartment homes. This portfolio averages B/B+ in quality and is diversified across eight core markets in the U.S. with “A” and “B” price points.

In the “A” portfolio, tenant rent-to-income stands at about 17%. In the “B” portfolio, it is not that much higher, at 19%. The lower ratios are due to average and median tenant household incomes of $251K and $170K, respectively. This is well above national averages. In addition, their residents have average FICO scores that are 90 points higher than the national renter average.

The stronger financial profile of their tenant base has contributed to a stable portfolio marked with high occupancy levels and low turnover.

Though the stock is up over 6.5% over the last month, shares are still down about 30% over the past year.

Seeking Alpha – Basic Trading Data Of AIRC

For long-term investors, AIRC offers upside at a reasonable cost. In addition, their current dividend payout is on the higher end than other peers within the sector. And while the uncertain market environment poses hurdles on future rental rate growth, the company is anchored by solid portfolio metrics and an upgraded financial position that boasts of a newly attained investment-grade debt profile.

Recent Performance

AIR delivered strong results in Q3FY22. In the same-store portfolio, net operating income (“NOI”) was up 13.3% YOY and 4.6% sequentially. On this, the company earned margins of 74.3%, which was up 240 basis points (“bps”) from Q3FY21, due in part to a 400bps decrease in controllable operating expenses.

Rate growth continued to drive results during the period. On new leases, rates were up 17%, while spreads on renewals were 11.8%. Together, this was 14.5% on a blended basis. While overall occupancy levels held up at 97%, average daily occupancy (“ADO”) declined 90bps sequentially to 95.9%. On a YTD basis, however, ADO is still 120bps higher than last year.

Additionally, portfolio turnover remains low at 38.5% on a trailing twelve-month basis. This is 320bps improved from the same period last year. Also contributing to the lower turnover is the higher household incomes of their tenant base.

Average and median household incomes in Q3, for example, were +$251K and +$170K, respectively. And with a rent-to-income ratio of less than 20%, their tenant base is clearly not rent burdened, despite the higher rates.

In the acquisition market, AIR is expected to have closed on approximately +$2.1B in transactions by year end, with another +$300M in closures in January. Management also noted the possibility of capitalizing on distressed opportunities arising out of the current market environment.

In addition to remaining active in acquisitions, AIR is also selectively disposing of properties. Subsequent to quarter end, the company completed the sale of their New England portfolio of six communities for +$500M, representing a trailing cap rate of 4.4%.

Liquidity And Debt Profile

AIR has a debt load of approximately 6x EBITDA. This is not only on the higher end of their targeted range, but it is also higher than their peers, who typically run between 4x-5x.

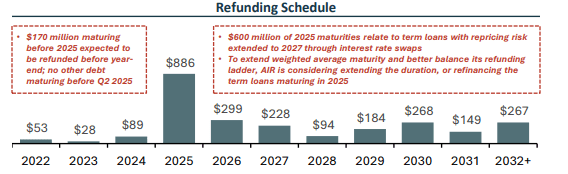

Offsetting this credit negative is their accommodative debt ladder, which, though at 6.4yrs to maturity is still lower than the peer average of 7.6yrs, nevertheless provides ample breathing room for the repayment of their debt.

Their nearest significant maturity, for example, is not before mid-2025.

November 2022 Investor Presentation – Debt Maturity Schedule

In addition, the company has limited floating rate exposure, which reduces risks relating to volatile interest rates.

Significant liquidity that includes +$100M in cash, availability on their revolving credit facility, and an essentially unencumbered portfolio further provides confidence of their balance sheet health. And this is reinforced by their stable investment grade rating from S&P Global, in addition to their newly attained rating from Moody’s.

Dividend Safety

AIR currently provides a quarterly payout of $0.45/share. At current pricing, this represents an annualized yield of nearly 5%. Compared to other multifamily peers, this is on the higher side.

Seeking Alpha – Current Dividend Yield Of AIRC Compared To Peers

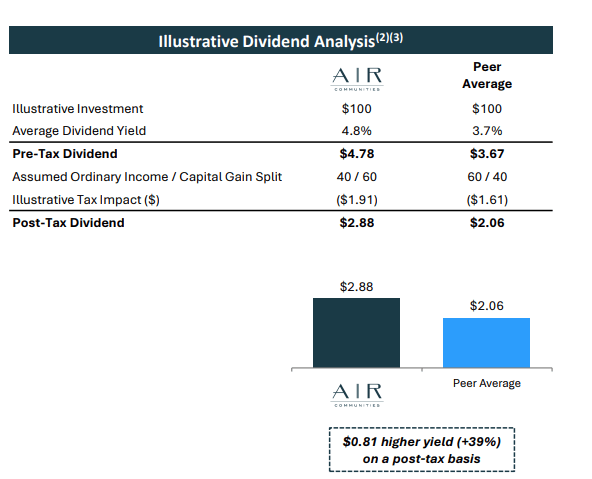

In addition to a higher yielding payout, investors also benefit from the favorable tax treatment of AIR’s dividends. In 2021, for example, about 67% of their dividend was treated as a tax-free return of capital, with 33% treated as capital gains. Their peer set, in contrast, averaged around 28% in capital gains. The greater share attributable to capital gains is notable since the rates are typically lower than those assigned on ordinary income.

November 2022 Investor Presentation – Post-Tax Dividend Analysis Of AIRC Compared To Peers

Overall, AIR’s dividends follow a 40/60 ordinary/capital gain split, while their peers run at 60/40. Even in a hypothetical scenario in which AIR’s dividends are characterized with a 50/50 split, AIR’s after-tax dividend would be about 35% higher than their peer average, assuming the payouts of their peers are characterized consistently with 2021.

In terms of safety, the company targets a payout ratio of approximately 75% of anticipated full-year funds from operations (“FFO”). While the payout was higher than that in the current quarter on a non-pro-forma basis, they are still on track to be in-line by the end of the year.

There is also adequate coverage through reoccurring cash flows. Through nine months of the year, for example, they have generated over +$350M in operating cash. Over the same period, they’ve paid out +$210M in common dividends, leaving with them +$140M to apply to other priorities, such as capital expenditures and share repurchases.

To date in 2022, they have in, fact, directed significant capital to share purchases. YTD, they have over $300M in share repurchases at an average price of $39.77/share, representing an unlevered internal rate of return (“IRR”) of over 10%. And over the past two years, they’ve deployed nearly 20% to share repurchases.

Main Takeaways

AIR doesn’t trade far off their spinoff price in late 2020. And at 15x forward FFO, shares appear competitively priced compared to many peers. Most closely, its multiple is in-line with that sported by NexPoint Residential Trust (NXRT). While the stock isn’t down as significantly as NXRT, it is still trading towards the bottom end of their 52-week spectrum.

A modest reassessment wouldn’t be unreasonable, considering their strong operating performance and the lower risk profile of their tenant base. In addition, though leverage is on the top end of their targeted range and higher than their overall peer set, their total load is still largely de-risked from the current market environment. A newly attained investment-grade rating from Moody’s provides further confidence of their ability to readily access debt markets in later periods.

Their current dividend payout is also more tax advantageous and is higher yielding than most others in the multifamily space.

While a significant run higher in shares may be unlikely in the current market environment, the long-term outlook of AIR is promising. Current Wall Street estimates value shares at just above $40/share, implying upside of about 13%. In addition to a reoccurring payout yielding just shy of 5%, that would provide investors with a modest return in an otherwise challenging environment. With earnings due out in early February, AIR is one worth further attention.

Be the first to comment