Pgiam/iStock via Getty Images

The Financial Select Sector SPDR® ETF (NYSEARCA:XLF) is a massively capitalised ETF designed to follow the full-service financial services companies in the US. This mainly includes full service banks, so both retail, commercial and investment banking exposed companies, and insurance companies. We think that more stable economic conditions where improvements can start to be anticipated are coming in 2023, and that XLF will be quite levered to those improvements in terms of performance. For investors looking for broad exposure ETFs, XLF shouldn’t be a bad choice.

XLF Breakdown

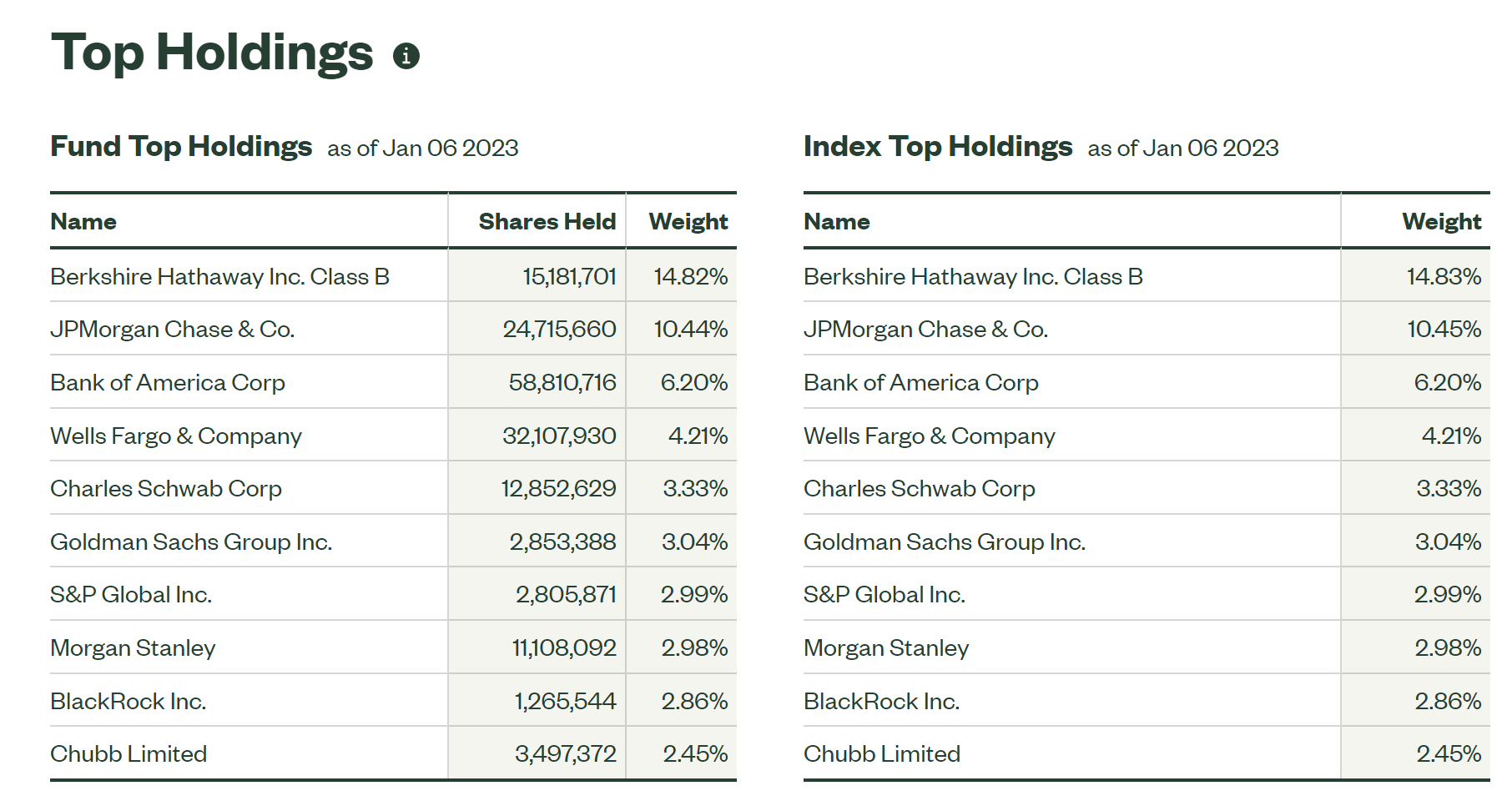

XLF’s top holdings are the following:

XLF Top Holdings (ssga.com)

The exposures here are clearly towards large-cap insurance and banking companies. Berkshire Hathaway (BRK.B) is an investment holding company, but a lot of its economics come from its insurance business. JPMorgan (JPM) from both retail banking but also corporate facing businesses and market facing businesses. Of a slightly different profile is Charles Schwab (SCHW), which is a broker and is mostly levered to volume of secondary market activity, as well as volatility of secondary markets. Finally, there are companies like S&P Global (SPGI) which depends on research services but also volume of DCM activity, because they rate bonds, and companies like BlackRock (BLK) whose KPIs are growth in AUM, driven by net inflow as well as by performance.

2022 has been a year where businesses like equity and debt capital raising, asset management, and investment banking and advisory have been under considerable pressure. On the flip side, insurance broadly has done well both on the underwriting and investment side, and retail banking and trading businesses have been doing well within full-service banks and brokerage businesses. On net, the banks on this list with substantial exposure to corporate activity have been seeing some degree of pressure on their businesses, including capital markets, advisory and asset management which a company like JPM deals with comprehensively.

Bottom Line

In terms of ECM and DCM, which can be a decent proportion of these business’ income, around 10% for a typical full service bank in the US, revenues have been under pressure to the tune of 50% declines or more. Advisory and investment banking revenues have been down about 30% across most of the companies that we cover in the independent IB space. Advisory and IB represent more revenue typically than ECM and DCM.

The economic prognosis is the following: rates will remain elevated for a while and not return to pre-hike levels, but inflation should ease and provide certainty to the markets. With certainty to the markets, that is all that is needed for conservative corporates to reinitiate M&A. Moreover, sponsors will be able to move forward without risking track records in the PE markets, since 2021 investments are all performing badly mark-to-market in PE. Finally, underwriting income shouldn’t be affected, especially in P&C where hurricanes have likely increased flexion on pricing power, and certainly on the asset management and investment side of banks and insurance companies, performance should be stronger in both fixed income and in equities.

XLF has gained slightly YTD, which is better than the general market, and expense ratios are really low at 0.1%. While a more beaten down ETF might be better value, financials remain with pretty high earnings yields at slightly over 7%, and their prospects should improve in 2023. Overall, XLF is a good exposure for conservative ETF investors looking for sector tilt.

Thanks to our global coverage we’ve ramped up our global macro commentary on our marketplace service here on Seeking Alpha, The Value Lab. We focus on long-only value ideas, where we try to find international mispriced equities and target a portfolio yield of about 4%. We’ve done really well for ourselves over the last 5 years, but it took getting our hands dirty in international markets. If you are a value-investor, serious about protecting your wealth, us at the Value Lab might be of inspiration. Give our no-strings-attached free trial a try to see if it’s for you.

Be the first to comment