zhengzaishuru

We downgraded our previous Hold calls on the Energy Select Sector SPDR ETF (NYSEARCA:XLE) to Sell in early December, seeing the opportunity for investors flushed with significant profits to cut partial/full exposure.

Accordingly, the XLE has slightly outperformed the S&P 500 (SPX) (SPY) since then, posting a total return of 0.92%. As such, the XLE has remained incredibly resilient, bolstered by the leading oil and gas companies’ record free cash flow generation, providing significant visibility for their capital allocation policies.

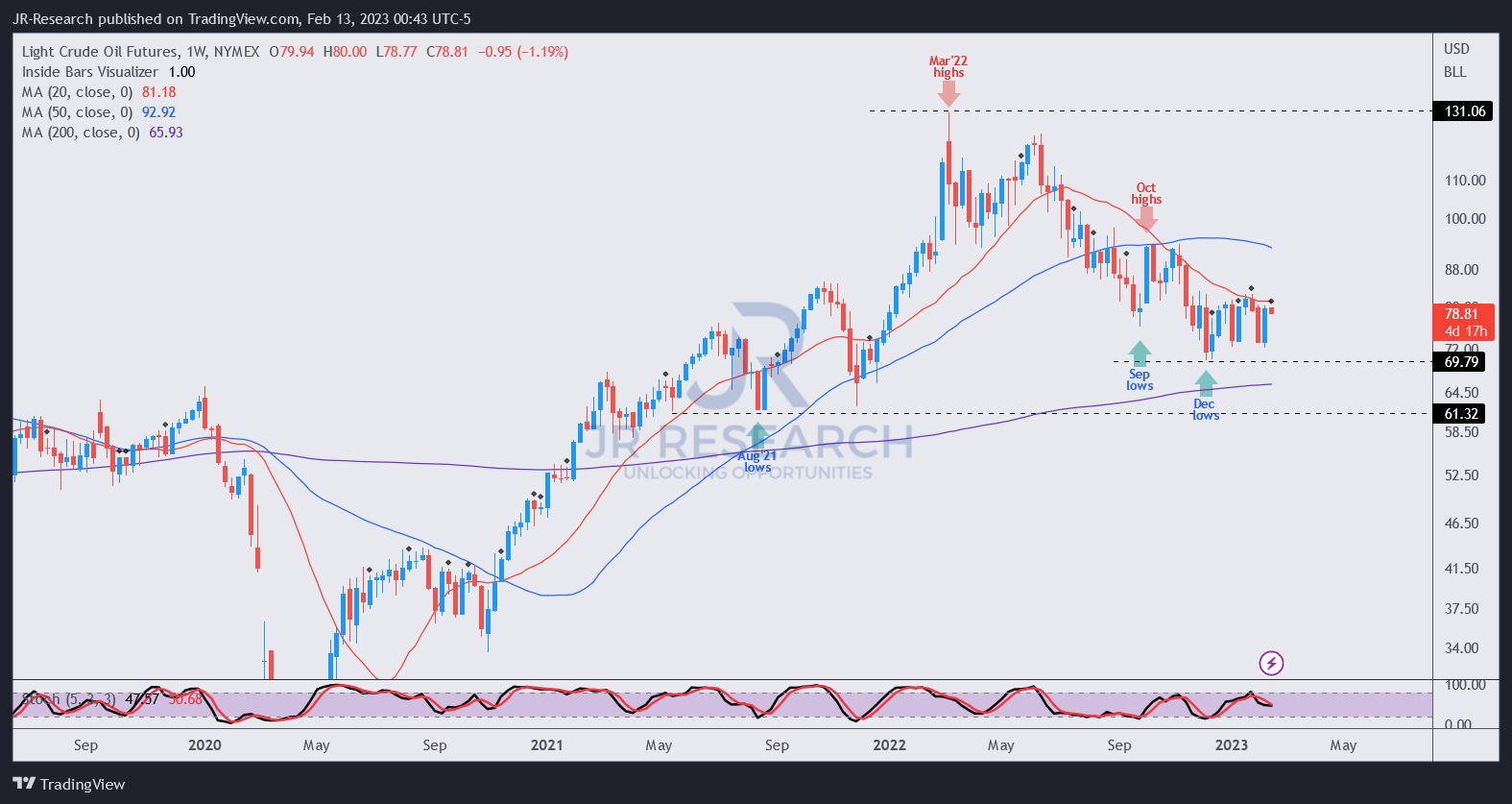

WTI futures price chart (weekly) (TradingView)

However, the price action for Brent (CO1:COM) and WTI futures (CL1:COM) remain well below their 2022 highs, emphasizing the clear bifurcation between the performance of the XLE and its underlying futures markets.

Bulls could argue that investors remain confident that the leading energy companies could continue their disciplined capital expenditure spending by focusing on share buybacks, dividends, and cutting down debt. As such, it should continue to improve these companies’ ability to sustain their capital allocation policies without undue concern over unsustainable CapEx increases.

In a recent commentary, Bloomberg highlighted that the majors’ CapEx in 2023 is “only getting back to 2018 levels,” and the “balance between reinvestment and dividends and buybacks is now even.”

President Biden’s recent State of the Union address underscores the importance of “oil and gas for at least another decade and beyond.” Furthermore, with energy security dominating the geopolitical landscape, “energy security is no longer just about oil or gas but about the energy that serves as the backbone of economies and the energy transition.”

Therefore, bulls could argue that it’s becoming increasingly clear that the potential for a “supercycle” in the energy sector is manifesting, potentially pushing Brent back above $100 subsequently.

Moreover, OPEC stressed that the world needs to “invest more in oil” to sustain and secure our energy requirements. Accordingly, OPEC sees “$500 billion of investment annually until 2045.”

Despite that, crude oil bulls appear to lack the conviction and momentum to recover the underlying futures price action back higher, despite the threat from Russia’s recent 5% production cut (500K barrels per day).

The move has been downplayed by some analysts so far as a likely attempt to curb excessive discounting, as Russia’s oil exports faltered recently after the price caps by the G7 that extended to petroleum products.

Therefore, with the underlying crude oil futures still in the doldrums, could China’s reopening bets mitigate the potential reduction in global demand in 2023 to lift XLE back higher?

The energy sector performed tremendously well in 2022, leading all sectors in the S&P 500, posting 57.7% YoY earnings growth in Q4’22.

However, we have consistently urged investors to remember that the market is a forward-discounting mechanism. As such, it’s critical to assess whether that momentum could carry on moving ahead and whether the price action supports the underlying sentiments underpinning the optimism.

As such, some caution is warranted. Analysts’ estimates on the energy sector have continued to fall through 2024 after a record year in 2022. As a result, the sector’s EPS estimates are expected to decline by 14.8% in 2023, followed by another 6% drop in 2024.

Moreover, upward net earnings revisions have also reversed into downward revisions in January, as analysts have started to reverse some of their significant bullishness from 2022.

Notwithstanding, the bullish sentiments bolstering the XLE’s upward advance have not fallen off a cliff, suggesting that sellers have not followed through on the weakness in the underlying futures market.

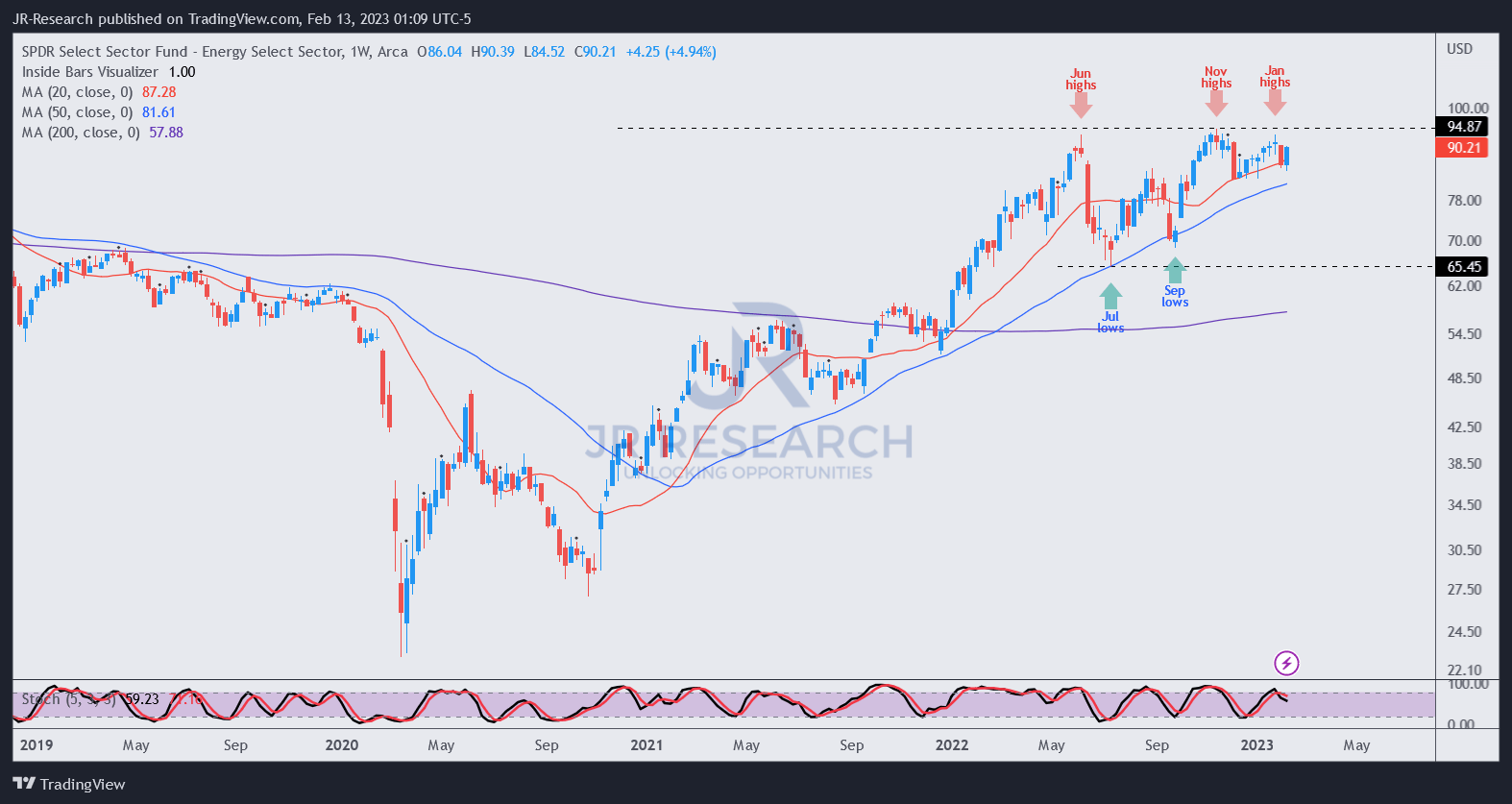

But, could the buyers muster enough momentum to finally push through in its third potential re-test of its June 2022 highs, which failed in November 2022 and January 2023 previously?

XLE price chart (weekly) (TradingView)

XLE buyers have faced significant resistance at the ETF’s June 2022 highs, as seen above.

Buyers failed to overcome selling pressure in November and January, even though XLE’s price action could potentially approach the critical resistance level for another pivotal re-test.

However, XLE’s price action has undoubtedly diverged from the robustness of its 2022 upward momentum, as buyers quickly overcame selling pressure, creating highly profitable dip-buying opportunities.

Hence, we assessed that caution is still warranted, suggesting some profit-taking to take some risks off the table is prudent. Investors should also watch for a third potential re-test failure, corroborating the opportunity to cut more positions before a steeper pullback could follow.

Also, be wary of false upside breakouts or bull traps by resisting the urge to follow through with daily momentum surges. Instead, have some patience by analyzing its weekly price action, and do not fall for the market operators’ traps, like in natural gas (NG1:COM), as we cautioned previously.

Rating: Sell (Reiterated).

Be the first to comment