SDI Productions

SPDR S&P Health Care Equipment ETF (NYSEARCA:XHE) is an exchange-traded fund that provides investors with exposure to health care stocks, specifically stocks whose underlying companies/businesses operate in the health care equipment space.

The last time I covered XHE was at the end of May 2022, at which point I believed the fund was dramatically overvalued. Usually when I spot an overvalued ETF, it does tend to under-perform materially thereafter, however in this case I was wrong. The fund has risen 3.08% on a price-only basis (and about the same on a total-return basis) vs. the S&P 500 index’s move of -1.44% over the same time frame. So, there has been some material out-performance, even if only by a few percentage points on a price-only basis. It is worth revisiting the fund to see if such performance is deserved.

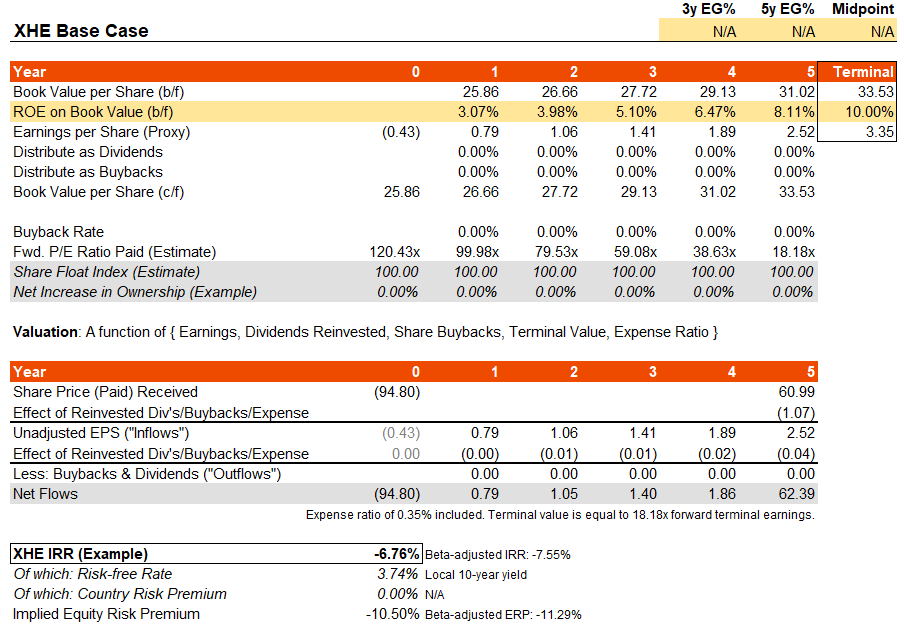

XHE only invests in U.S. stocks; its benchmark index that it seeks to track is a sub-set of the S&P Total Market Index. XHE’s benchmark’s most recent factsheet, as of January 31, 2023, provides some useful information. The report offers trailing and forward price/earnings ratios of -220.77x and 120.43x, respectively, with a price/book ratio of 3.7x. These figures indicate very poor (more specifically negative) earnings on a trailing basis, and low earnings on a forward basis. The problem with these earnings is that they are clearly low quality: if bottom-line portfolio-weighted earnings are negative and/or low, one should pay less for those earnings.

Morningstar have a three- to five-year average earnings growth rate (prediction) of 10.93% as of present, which provides us with some directional optimism, but these are to be applied (at least in the first instance) against our low earnings base. Using the benchmark index data, the fund’s return on equity on a forward basis is only 3.07%. Since Morningstar’s long-term earnings growth figure is based on adjusted operating earnings, I am willing to be “generous” and assume larger subsequent growth, such that the lower quality earnings and “noise” is accounted for, resulting in a more normal return on equity of 10% by year 6 (the terminal year). Bear in mind Morningstar’s adjusted figures imply an adjusted return on equity of about 11% on a forward basis today, so this would be in the right ballpark.

Given the noisiness of the forward 120.43x forward earnings multiple as referenced above, we would also want to gradually reduce this to a fairer multiple: assuming a 3% 10-year at maturity in five years’ time, and an equity risk premium of 4.5%, plus a long-term earnings growth rate of 2% to perpetuity, I calculate a forward earnings multiple of 18.18x as being fair. For the sake of simplicity, I will assume no dividends or buybacks for now. The result of the model is a negative IRR of -6.76% per year.

Author’s Calculations

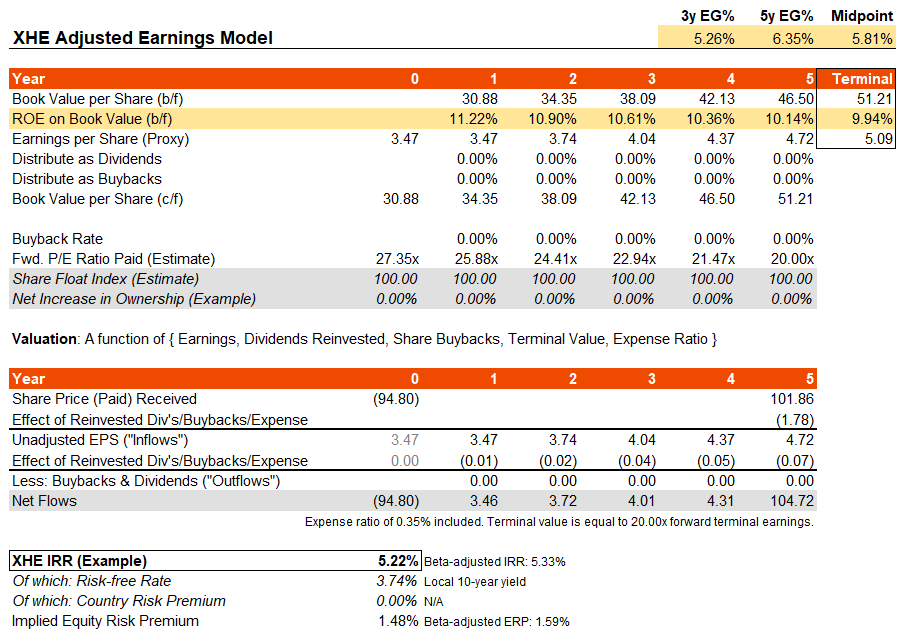

This is consistent with my prior conclusions, that the market is giving the fund the benefit of the doubt that the earnings noise problem (i.e., low quality portfolio earnings) will be solved rather quickly. Perhaps more accurately, we could say the market is simply ignoring the poor quality earnings. For the sake of being informative, I will reproduce the above model using adjusted earnings figures from Morningstar, beginning with a forward price/earnings ratio (on an adjusted basis) of 27.35x. In this case I’ll also give the model the benefit of a 20x forward earnings multiple by year six, because evidently the market seems to think health care equipment stocks are worth holding onto. The generous model output below indicates an IRR potential of 5% per annum.

Author’s Calculations

So, even with adjusted operating earnings, and a roughly constant 10-11% portfolio return on equity (including retained earnings, in this model) still only lends to an IRR of about 5.22%. That is also given a healthy 20x earnings multiple in the terminal year, which I would argue is probably too generous, as well.

Health care stocks are conventionally defensive, but XHE doesn’t pay a high dividend yield on a trailing basis (barely above zero when scaled by price) and the fund’s earnings quality is extremely poor. The market is disregarding that. I think XHE is still fundamentally overvalued. Even by using adjusted operating earnings, which basically ignore the low quality earnings problem, XHE is still overvalued; a healthier IRR would be circa 8% (at least). This suggests that XHE is overvalued by at least 50%.

Indeed, the only way I can reach a healthy IRR of about 9% is by assuming much higher earnings growth of about 10% per annum on average over the next five years, while also completely ignoring the earnings quality problem. In this way, I get to a beta-adjusted ERP of 5.62%. This could potentially indicate fair value on this basis. However, given negative actual earnings on a trailing basis, poor quality earnings on a forward basis, and a very low dividend yield (which is probably a further indication of the poor quality of earnings), I think XHE is clearly overvalued.

In summary, I would continue to advise against investing in XHE until the fund’s underlying, portfolio-weighted earnings are normalized.

Be the first to comment