S&P 500 Talking Points:

- The S&P 500 futures contract set its current all-time-high a year ago, on January 4th.

- While the Fed started to open the door to rate hikes in September of 2021, the Nasdaq topped in November of that year but the S&P continued to drive-higher until the calendar turned into 2022. Last year saw the Fed get much more hawkish throughout the year and this sunk stocks in waves and phases, with a net move of approximately 20%.

- The analysis contained in article relies on price action and chart formations. To learn more about price action or chart patterns, check out our DailyFX Education section.

Recommended by James Stanley

Get Your Free Equities Forecast

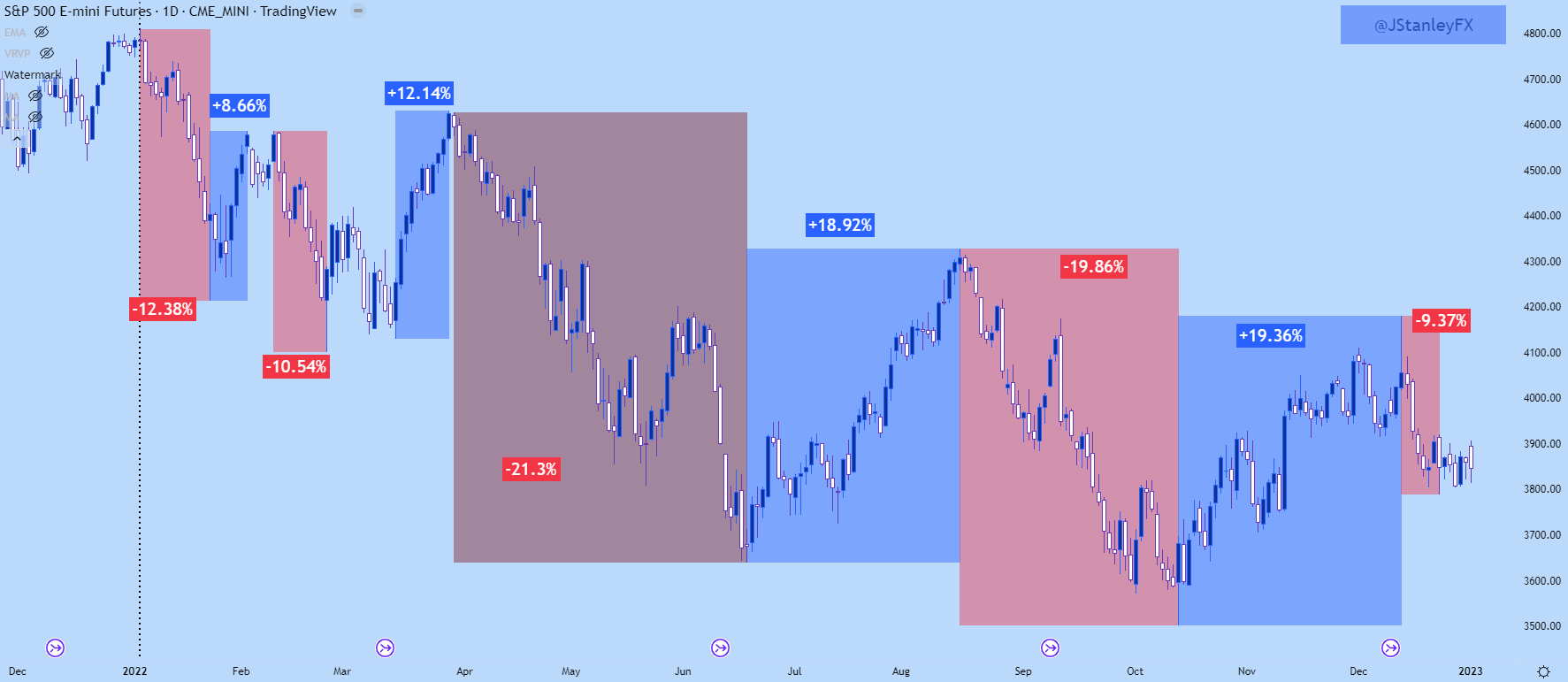

It was a rough year for stocks but, you probably know that already. The bigger question is whether there’s more pain to follow or if the worst is over. I’ll just say it up front, I don’t think that the lows are in yet. One of the reasons that I think that’s the case is because of how the sell-off last year came in to markets. To be sure, there were periods of violence, with prices posing massive moves in short periods of time. But, really this pertained to both sides of the matter, with bullish swings in June and October but, to a lesser degree, similar moves in January, February and March.

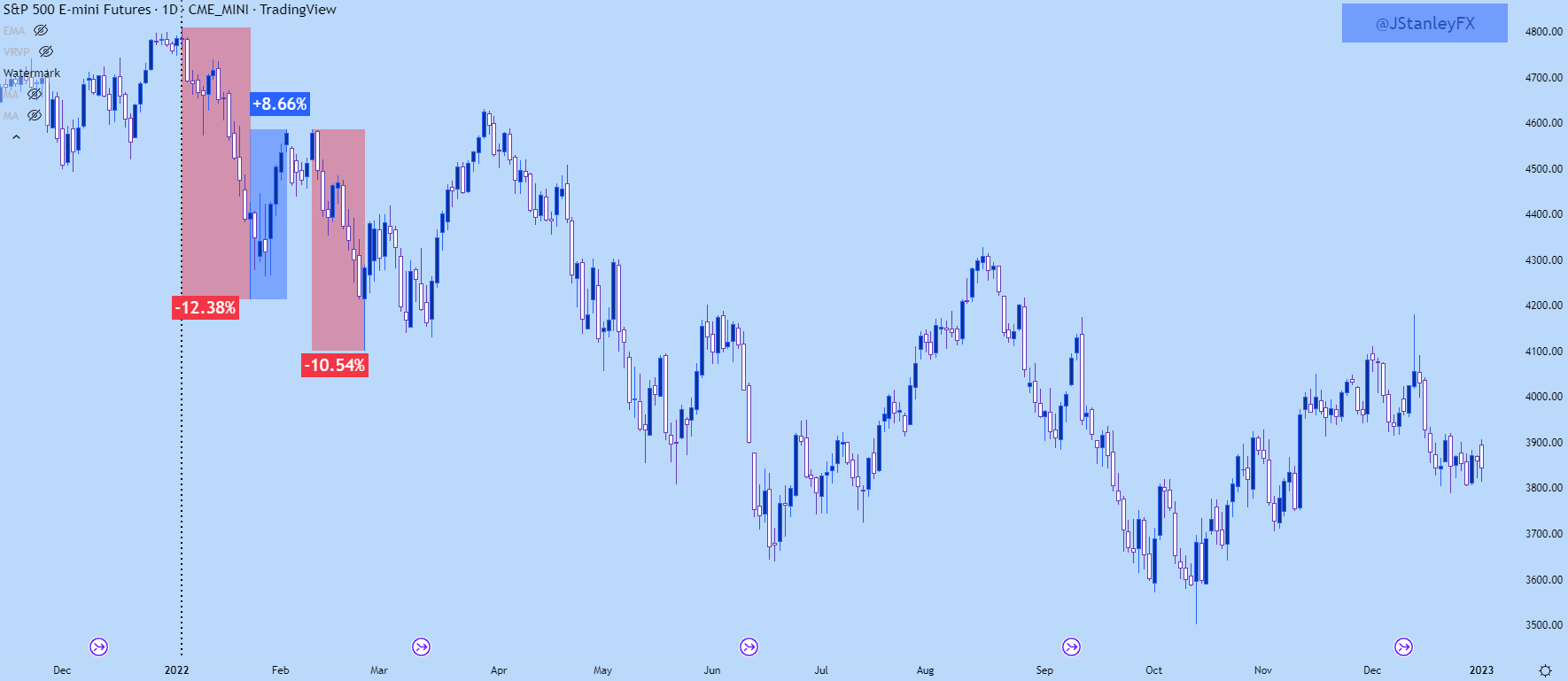

The S&P 500 topped on January 4th of last year. This was the second trading day of 2022 and at the time, the S&P 500 set a fresh all-time-high. The Nasdaq had already-topped a couple of months later but, at this point, fear was starting to show from a couple of different factors.

First and foremost, the Fed was hawkish. They had said as much in September and then reiterated at the rate decision in December. In September of 2021, the Fed opened the door to one hike in 2022. In December, they ramped that up to two to three. By January, it became obvious that two to three wouldn’t get the job done, with inflation having already up to 7%. And that’s when another risk started to rear its ugly head when Russia began to line the Ukrainian border with tanks.

From the January 4th high to the Jan 24th low, the S&P 500 dropped by -12.38%. And then rallied by 8.66% into the February open, before falling again by -10.54% into the February 24th low, which, ironically, was the day that Russia actually invaded Ukraine.

S&P 500 Daily Price Chart

{kind=link}

Chart prepared by James Stanley; S&P 500 on Tradingview

Fed Lift-Off

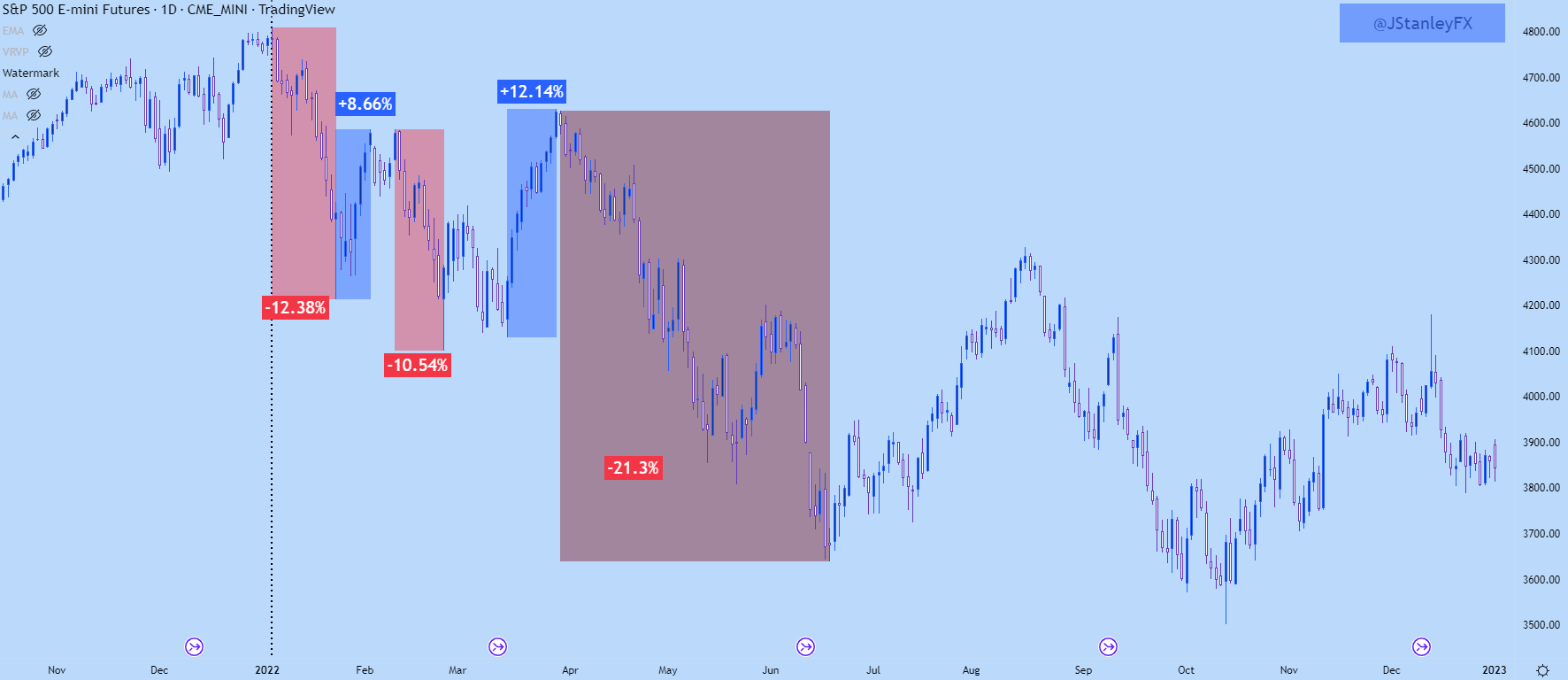

The Federal Reserve finally started hiking rates in March. Inflation at the time had just printed at 7.9% for headline CPI in the month of February. So, the Fed’s 25 basis point rate hike didn’t carry much hope for arresting that inflation and during the rate decision, the bank warned of more hikes to come.

The S&P 500 rallied around that meeting, with the low being set on the Tuesday before the rate decision. The rally continued for a couple of weeks after, totaling a bullish bump of 12.14% in a very short period of time.

It was the Q2 open that really brought the bears out, as the S&P 500 fell by 21.3% from the late-March high down to the June low.

Recommended by James Stanley

Traits of Successful Traders

S&P 500 Daily Price Chart

Chart prepared by James Stanley; S&P 500 on Tradingview

75 and Go

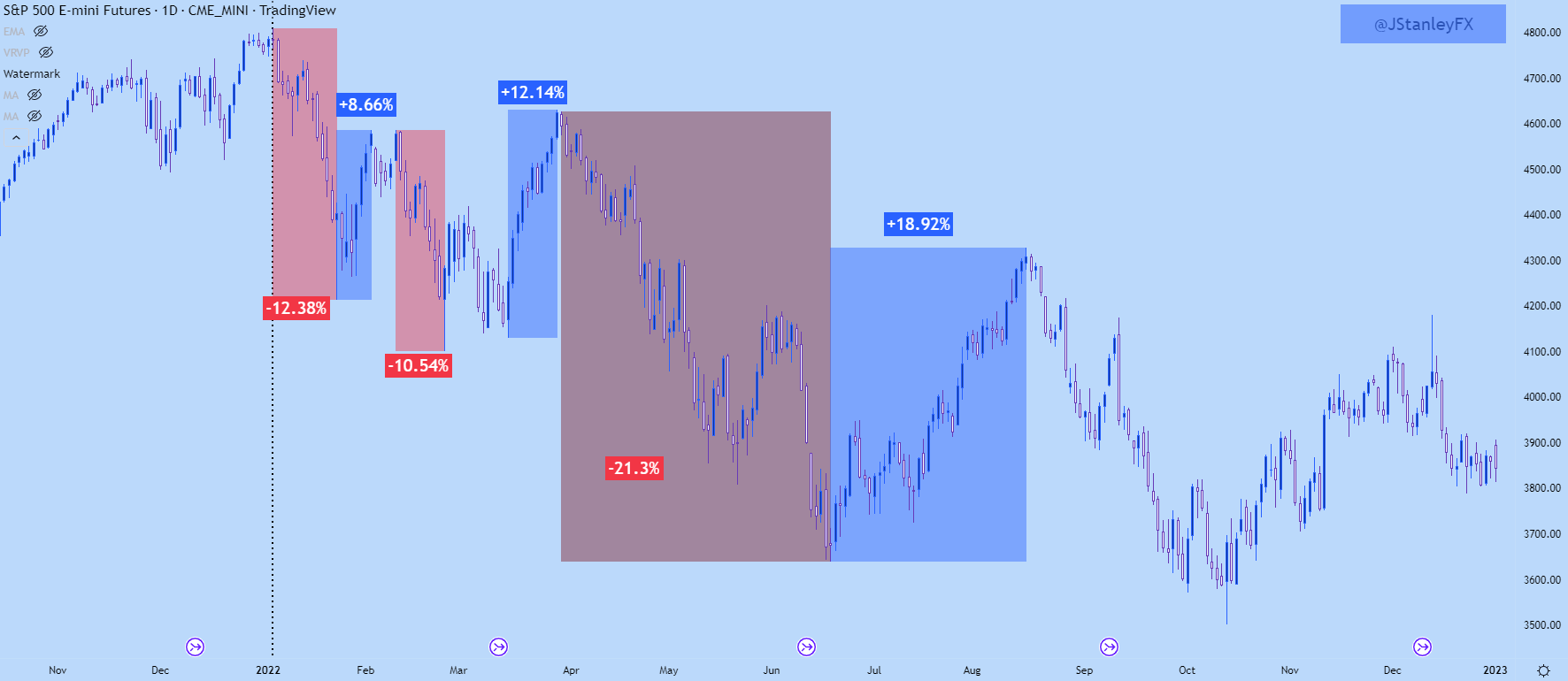

That June rate decision was a peculiar one. Not only did the Fed hike rates by 75 basis points, they also warned that they might do it again; and that rates were going to continue to move-higher.

Stocks did probably the opposite of what you would’ve expected. At least the opposite of what I expected. The held the low and then started to rally, adding a whopping 18.92% over the next two months until finally finding resistance in mid-August.

That’s around the time that Jerome Powell really wanted to get his message across…

S&P 500 Daily Price Chart

Chart prepared by James Stanley; S&P 500 on Tradingview

Powell at Jackson Hole

The Jackson Hole Economic Symposium is not usually on my top 10 must watch events. It’s not usually even in my top 100 but I’m digressing here. This year it was a must watch as this bubbling rally was holding into the summer’s most watched macro event and Jerome Powell had an open stage to send a very direct message to markets.

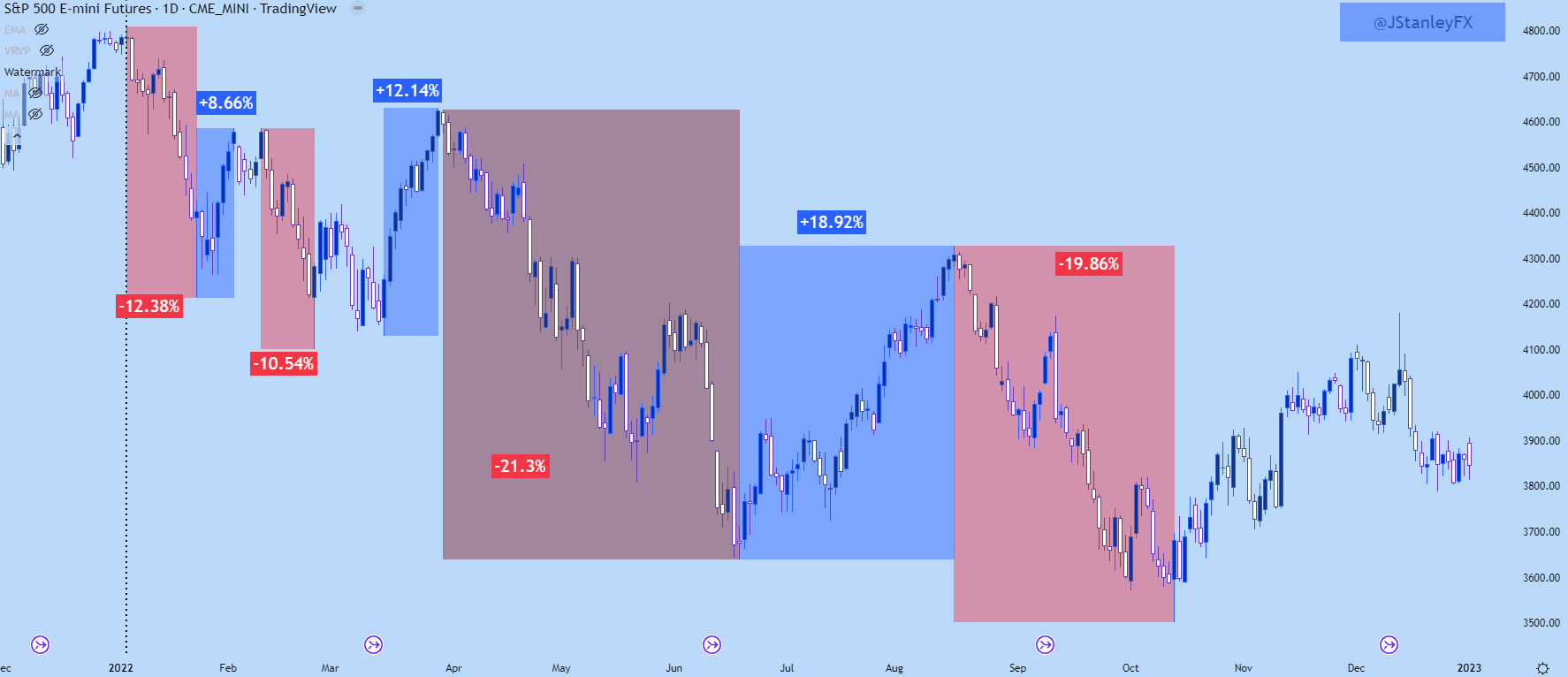

When we finally got there on August 26th, Powell didn’t beat around. He spoke to the elephant in the room and said the Fed’s aim is to temper inflation and they weren’t near finished with the job yet. Bears were brought out in droves and this led to a fast move that continued a couple of weeks into Q4.

That’s around the time that another counter-intuitive theme began to show…

S&P 500 Daily Chart

Chart prepared by James Stanley; S&P 500 on Tradingview

CPI Still Driving Headlines but in the Other Direction

On October 13th another disappointing CPI report was released to markets. Markets were looking for inflation to have softened down to 8.1% from a prior read of 8.3%. It actually printed at 8.2%, so a hair above the expected. When a similar scenario happened in September, stocks were smashed but, in October, that smashing was a fleeting observation.

S&P 500 futures hurriedly broke down, set a low just above the 3500 level, and then started to rally ahead of the US open. That rally continued… and continued and continued. Eventually, the move tacked on a total of 19.36% – running for two months to the day – when another CPI report was released.

On December 13th, an optimistic report was released with CPI printing at 7.1% versus a forecast of 7.3% and a prior print of 7.7%. So, all in all, something that seems positive an optimistic. The response in equities was anything but…

Recommended by James Stanley

Improve your trading with IG Client Sentiment Data

S&P 500 Daily Chart

Chart prepared by James Stanley; S&P 500 on Tradingview

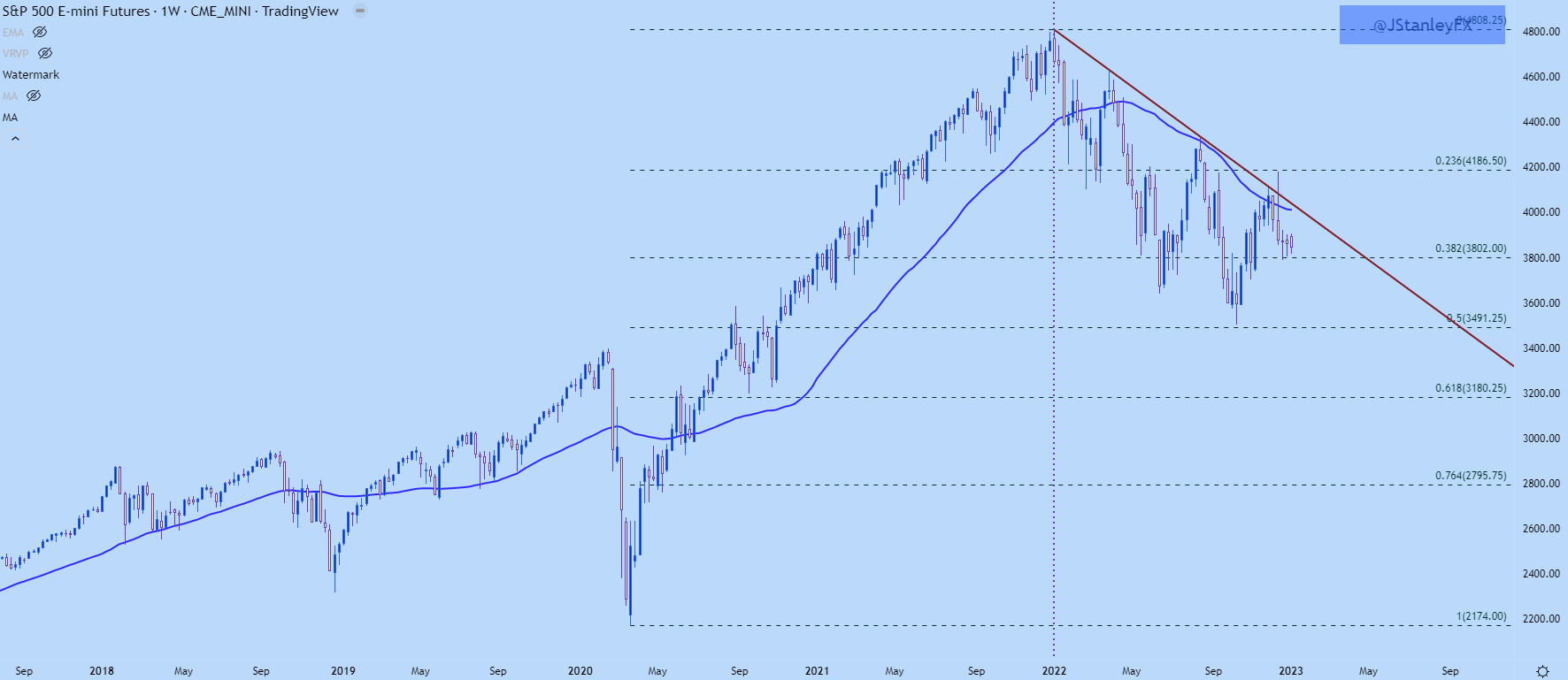

Now for 2023

Markets rarely pose linear moves, and the reason or at least one of the more operative reasons is that they are controlled by human beings. And humans are imperfect, particularly when part of a group. It can take time to make a turn but at no point is the market 100% bullish or bearish, which is illustrated well in the swings on the above charts.

It’s important to note that through most of last year the fundamental backdrop was utterly pitiful. Inflation was too high, rates were quickly being adjusted to try to offset that because, well, 10% inflation during a recession is a really bad thing because now Central Banks can’t even go back to QE or ‘liquidity programs’ because that risks even more inflation.

Yet, stocks put in two massive rallies in the second-half of the year, with an 18.92% move and a 19.36% move from the June and October lows. This was as the Fed kept telling us that they were going to keep hiking rates because the job of tackling inflation was not yet over.

Inflation can kill an economy and, in-turn, a democracy (or constitutional republic if you want to be pedantic about it). There’s no clearer sign of a failure of leadership than a lack of economic consistency and this is the type of thing that can lead to challenges for power or political turmoil. If you have 10% inflation as you enter into a recession, such as the backdrops showing in Europe or the UK at the moment, and the range of possible outcomes widens dramatically.

S&P 500 Weekly Chart

— Written by James Stanley

Contact and follow James on Twitter: @JStanleyFX

Be the first to comment