LL28

Anyone who falls into the habit of thinking and expecting the best of his subordinates at all times is, for that reason alone, unsuited to command an army”― Carl von Clausewitz

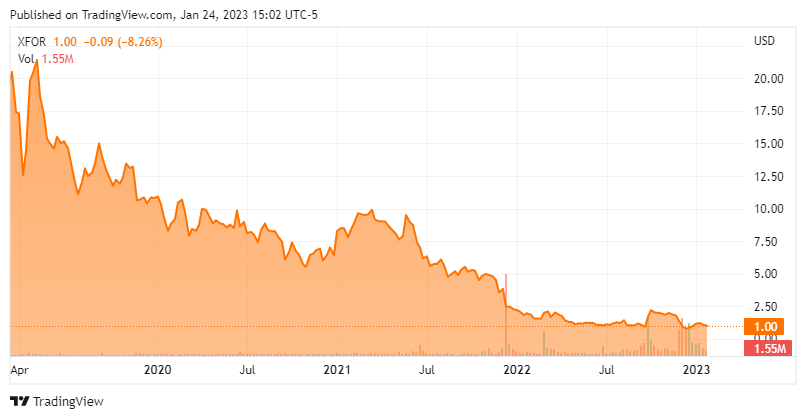

Today, we put X4 Pharmaceuticals (NASDAQ:XFOR) in the spotlight since our initial article on this small biopharma name back in November of 2019. Although the company had some positive attributes at that time, we passed on making any investment recommendation around this equity as it was cash strapped and there were mixed views on it within the analyst community.

That turned out to be the right call as this stock has done little but destroyed shareholder value since our initial piece on it. However, this $1 ‘dart throw‘ does have some potential catalysts on the horizon and analyst commentary has become most positive on the shares at these lower trading levels. An updated analysis follows below.

Seeking Alpha

Company Overview:

X4 Pharmaceuticals is a late-stage clinical biopharmaceutical company that is based out of Boston. The company is focused on development of novel therapeutics for the treatment of rare diseases. The stock currently trades just above a buck a share and sports an approximate $130 million market capitalization.

November Company Presentation

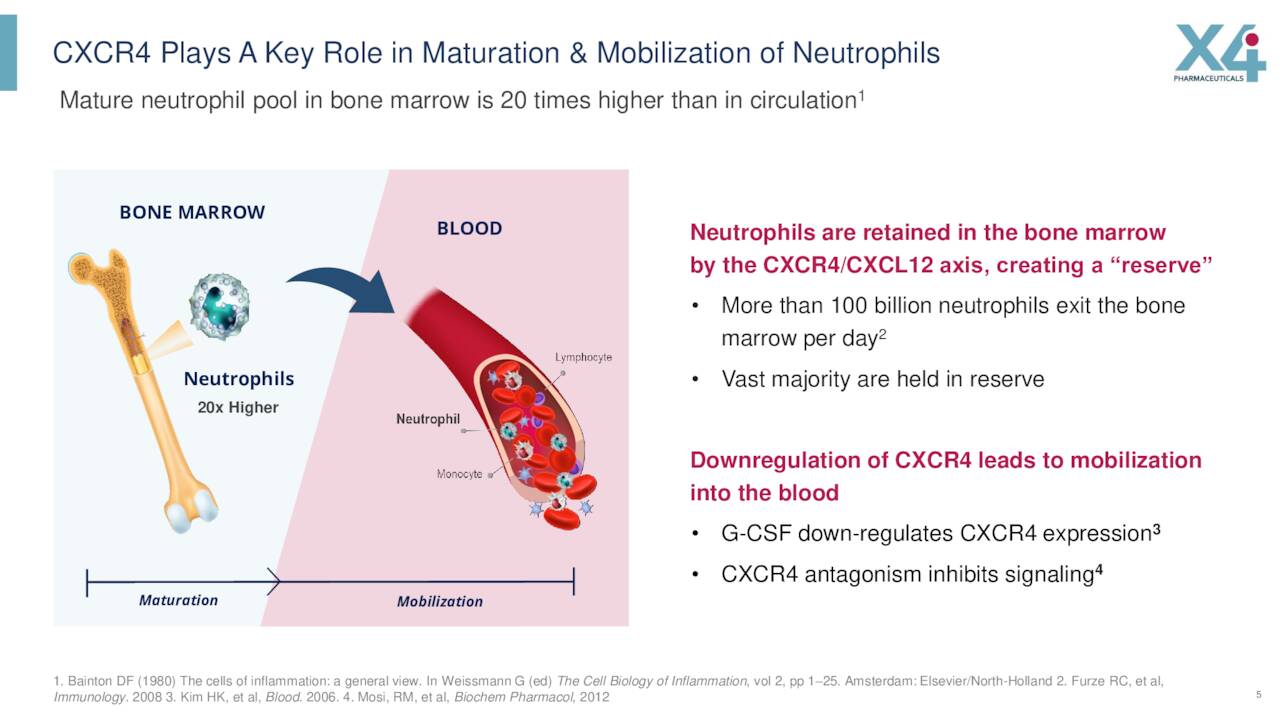

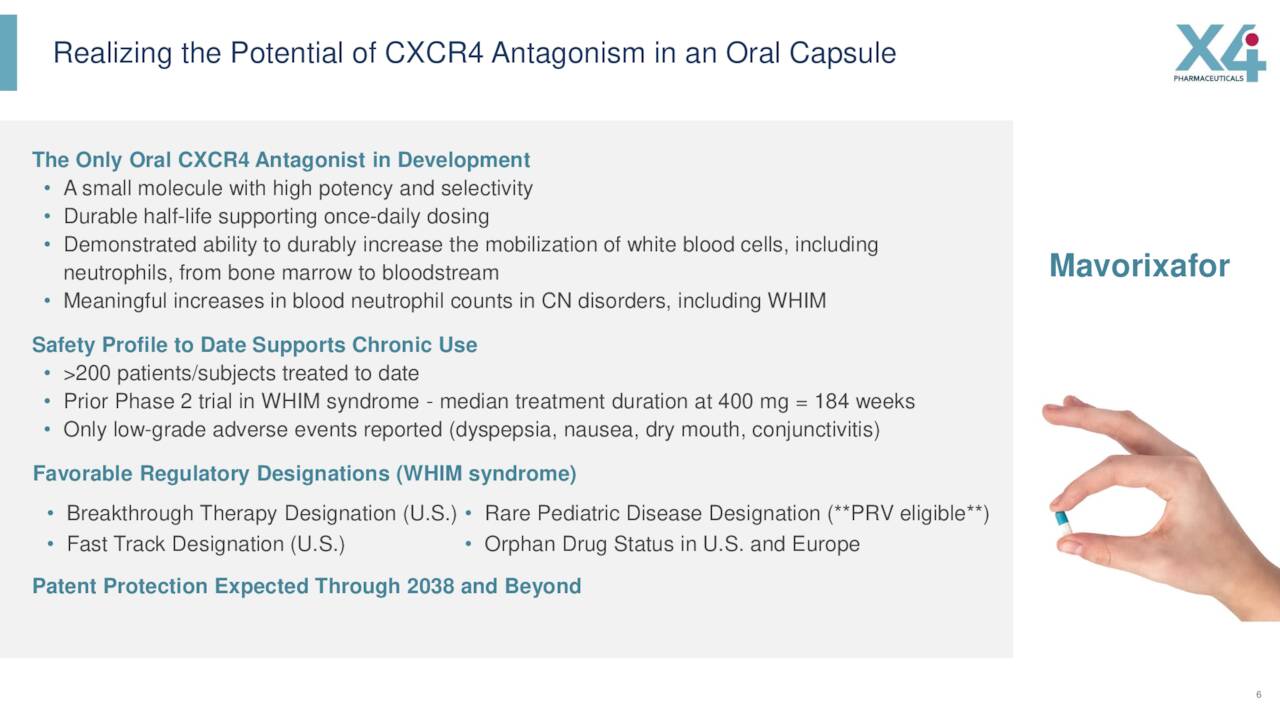

Its lead product candidate is called Mavorixafor, which has patent protection until 2038. This compound is a small molecule inhibitor of the chemokine receptor C-X-C chemokine receptor type 4 or CXCR4.

November Company Presentation

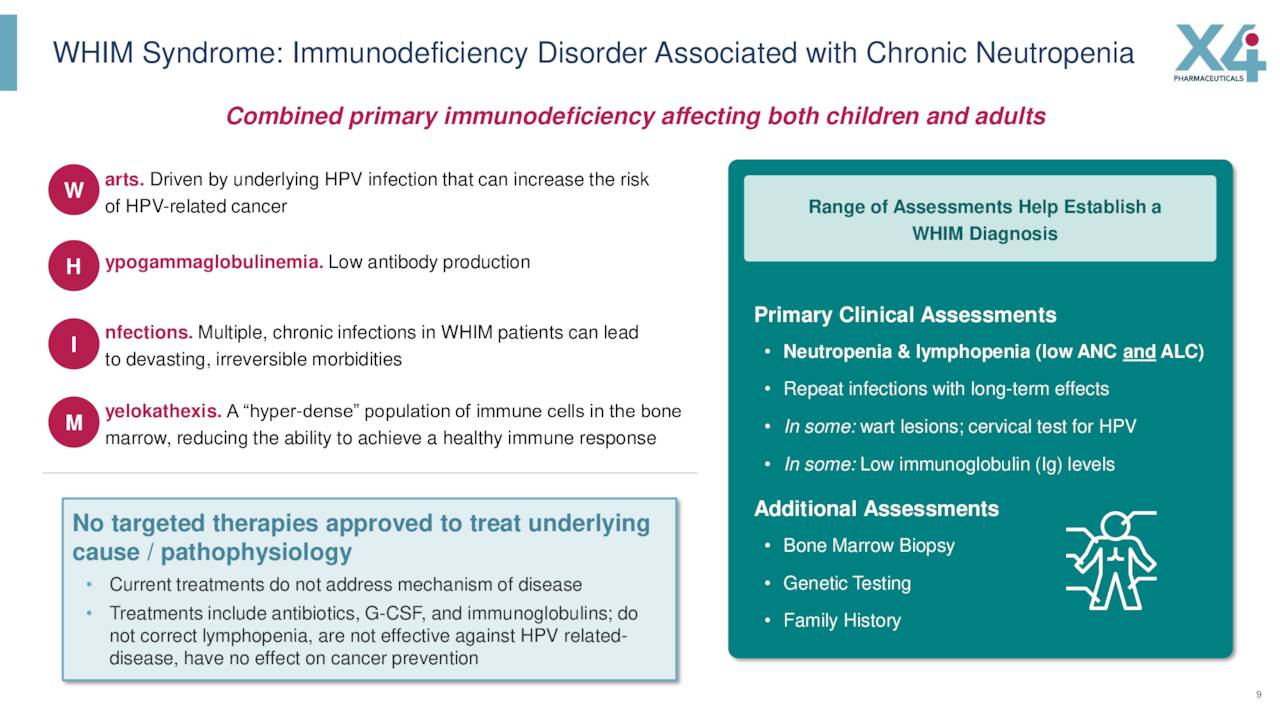

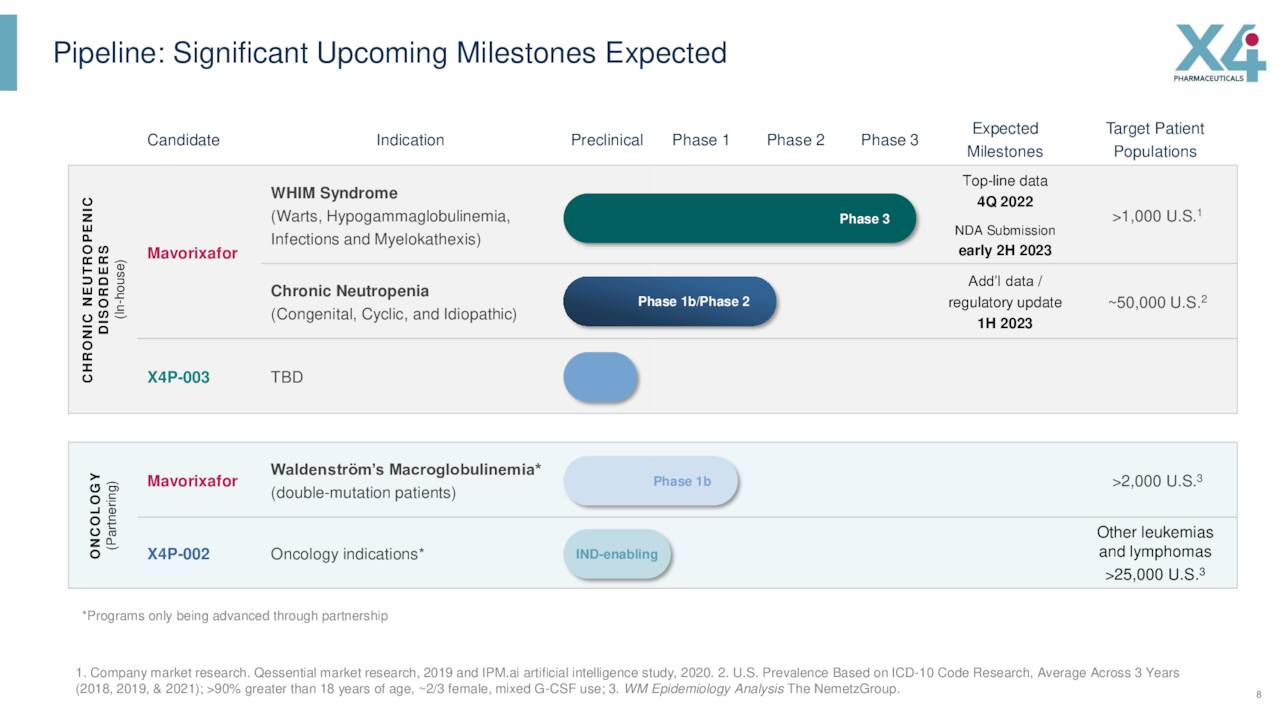

Currently Mavorixafor is in a Phase 3 study to evaluate it for the treatment of patients with warts, hypogammaglobulinemia, infections, and myelokathexis syndrome. This is commonly known as WHIM syndrome and effects at least 1,000 and up to 3,500 individuals in the United States according to the company’s CEO and double that globally. In November of last year, X4 Pharmaceuticals posted positive top-line results from this 52-week Phase 3 study called 4WHIM. Data showed both primary and secondary endpoints were met and mavorixafor was generally well tolerated in the trial. There also were no treatment-related serious adverse events reported. The company plans to file a New Drug Application or NDA for this indication sometime early in the second half of this year after a meeting with the FDA.

November Company Presentation

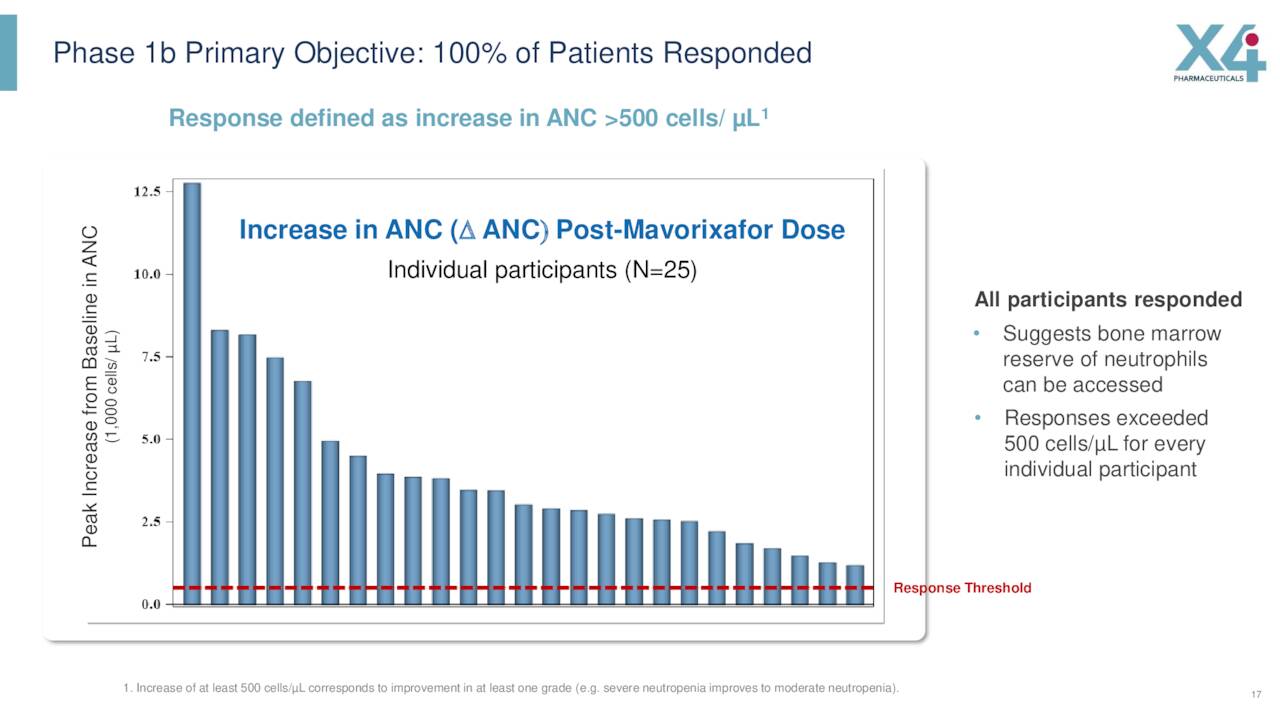

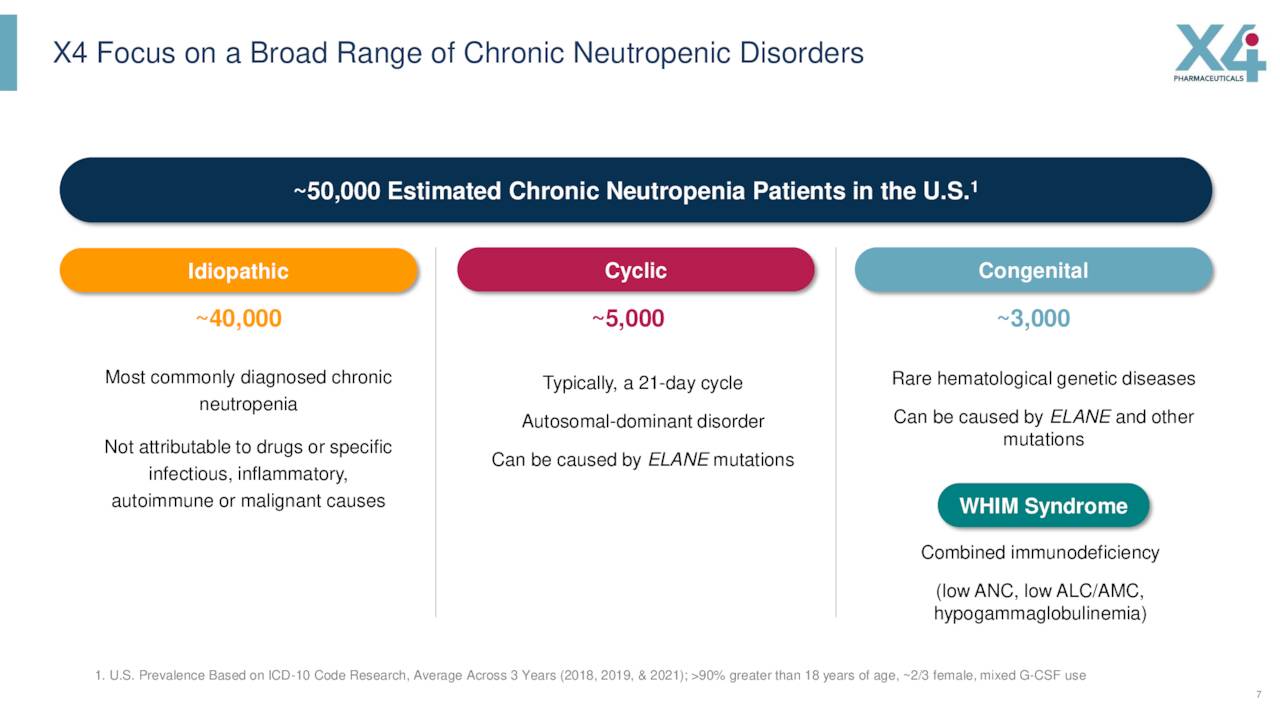

In addition, this drug candidate completed a Phase Ib clinical trial to treat chronic neutropenia or CN and Waldenström macroglobulinemia last summer.

November Company Presentation

Data from this early stage trial showed that all of the 25 study participants achieved robust responses to mavorixafor for chronic neutropenia.

November Company Presentation

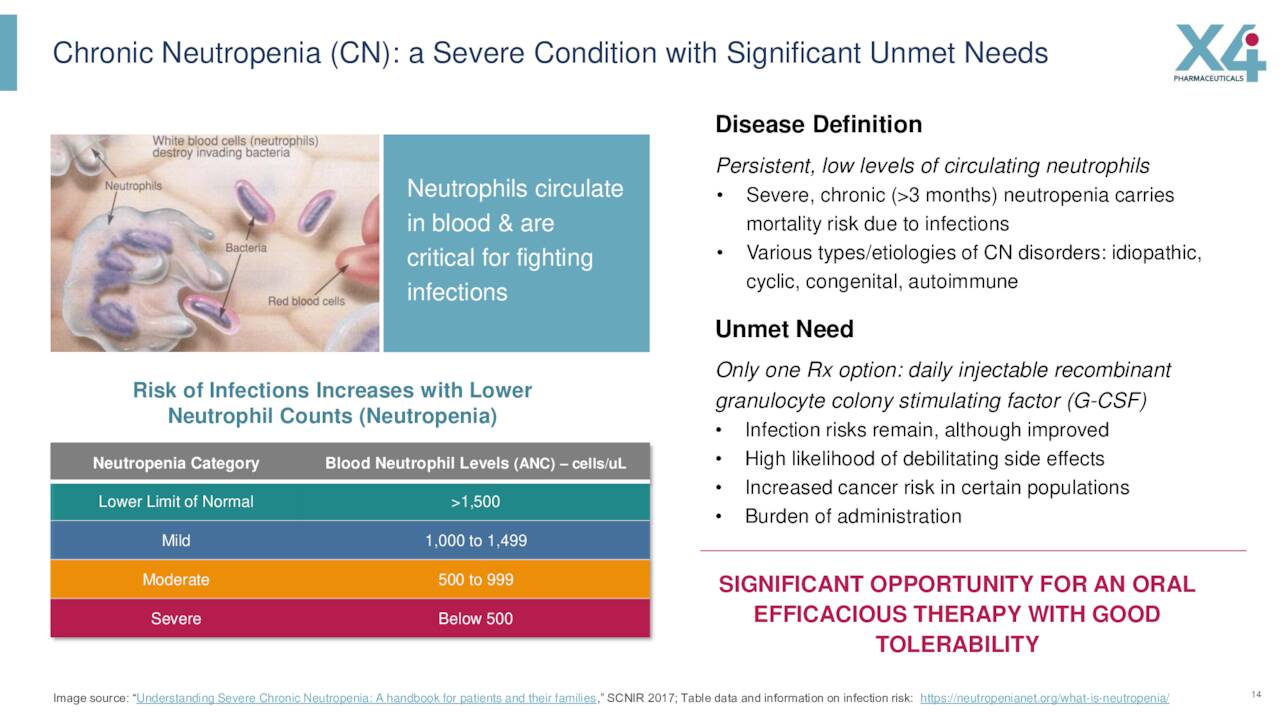

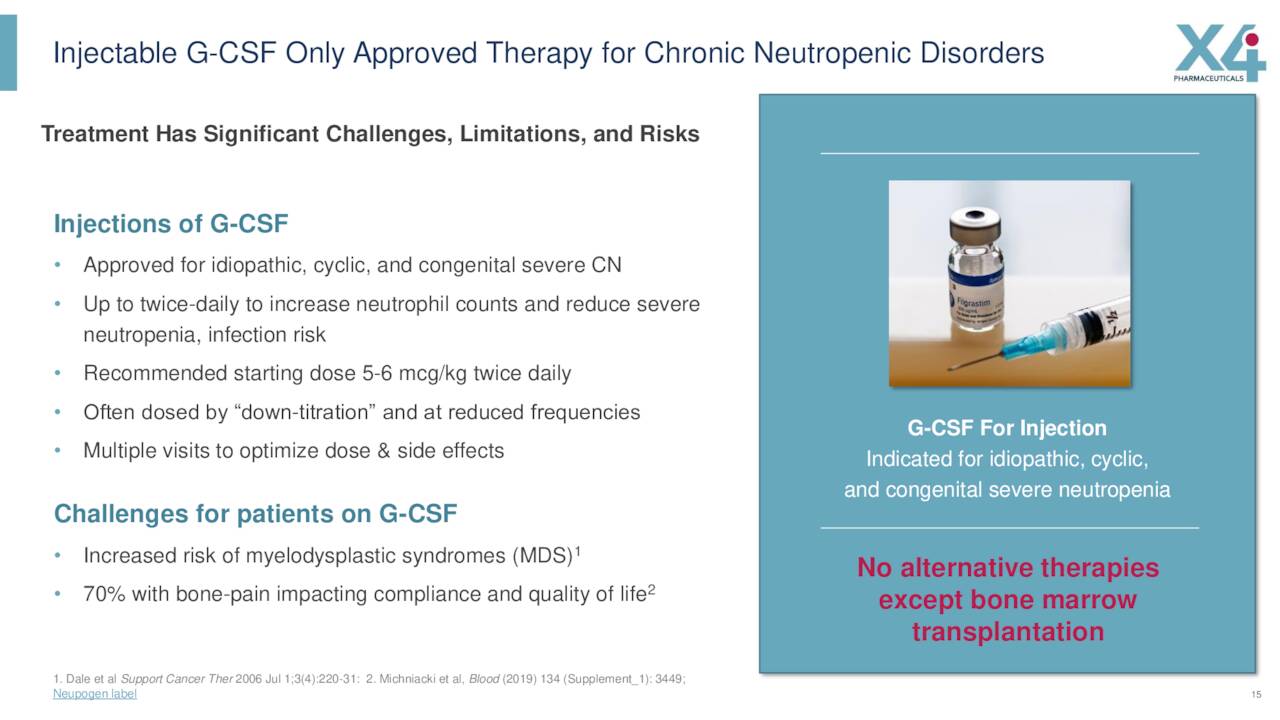

Individuals with chronic neutropenia are usually treated with granulocyte colony-stimulating factor or G-CSF. This is an injectable therapy which unfortunately has some burdensome side effects which include severe bone pain and myalgia. The company recently kicked off a Phase 2 study for this indication that will evaluate the safety and efficacy of this candidate with or without G-CSF in people with chronic neutropenic disorders.

November Company Presentation

The phase 1b trial also showed good responses for mavorixafor to Waldenström’s macroglobulinemia or WM. This affliction is a rare blood cancer. It also is a type of B-cell non-Hodgkin’s lymphoma which is characterized by the accumulation of malignant B-cells in the bone marrow. While data was supportive and mavorixafor has Orphan Drug status for this indication, the company has halted development against WM until it finds a strategic partnership to do so.

November Company Presentation

Analyst Commentary & Balance Sheet:

Since early November, a half dozen analyst firms including Piper Sandler and Cantor Fitzgerald have reissued or initiated Buy/Outperform ratings on the stock. Price targets proffered ranged from $3 to $7 a share. There were very minute insider sales in the stock in 2022. Less than two percent of the outstanding float is currently held short.

X4 had just over $80 million of cash and market securities on hand at the end of the third quarter. Leadership stated at the time that was sufficient to fund operations until the third quarter of this year. Management then executed a secondary offering to raise some $65 million of additional funding in early December. At the company’s current burn rate, that should fund X4 until mid-2024.

The company has just over 100 million warrants outstanding exercisable right at current trading levels as well as nearly 30 million worth of warrants exercisable at $1.50 a share. This will remain a significant overhang on the stock. The company also has just under $20 million of long term debt.

Verdict:

The company seems marching towards its first FDA approval mavorixafor to treat WHIM. It should be noted this compound has Breakthrough Therapy Designation, Fast Track Designation, and Rare Pediatric Designation in the U.S. for this indication as well as Orphan Drug Status both here and in the European Union. Importantly, FDA approval will garner a valuable Priority Review Voucher. These vouchers have generally fetched between $100 million to $125 million on the open market in recent years, which would go a long way to shoring up X4 Pharmaceuticals’ finances.

November Company Presentation

With potential approval for mavorixafor to treat WHIM early in 2024 and a regulatory path forward for CN hopefully clarified by the end of this year, the company has some significant potential catalysts on the horizon. The company’s balance sheet is still a concern, but with strong analyst support and significant events approaching, a small investment in XFOR seems a worthy, if speculative bet at current trading levels.

If I have learned anything in this long life of mine, it is this: in love, we find out who we want to be; in war, we find out who we are.” – Kristin Hannah

Be the first to comment