lovro77/E+ via Getty Images

The new management of Workhorse Group Inc. (NASDAQ:WKHS) has been saying a lot of the right things and presumably doing some of the things needed to position itself to ramp up production when and if its products are proven to be in demand in the quarters and years ahead.

If there was a word that describes Workhouse, it would be “delay.” It seems whenever management in the past and presence communicates to people, there is a sense that momentum and growth are just around the corner, and yet the waiting continues even as more disruptions happen that once more delay progress.

One of the more recent ones was the port delays concerning its cab chassis which ended up having an impact on the timing of its customer shipments. That suggests the moderately downgraded outlook for full-year 2022 for delivering 25 to 100 vehicles that would generate from $5 million to $15 million in revenue will probably be less than that, and it remains to be seen if customers are going to remain patient in waiting for the company to operate in a professional and efficient manner.

It’s not that failing fast, and iteration aren’t part of the package for a company like Workhouse, but the point of that is to quickly adapt and improve things so it’ll bring a company closer to success. So far that hasn’t happened with Workhorse where it counts, and “build it and they will come” isn’t a sustainable business model.

In this article, we’ll look at where the company is at, what it must do to build back confidence in it, and it may be taking on too much too soon in its product development.

Where the company is at

The initial focus is on Chief Executive Officer Rick Dauch. After taking over as head of the company, his mission was to clean house concerning key positions in the company and replace them with people he, for the most part, knew and trusted from working with them at companies he had worked for in the past.

Among some of the housekeeping items he had to fix was the overhang from the lawsuit associated with USPS; streamlining processes including the workforce, cut back on debt and have enough cash to fund operations long enough to implement its vision.

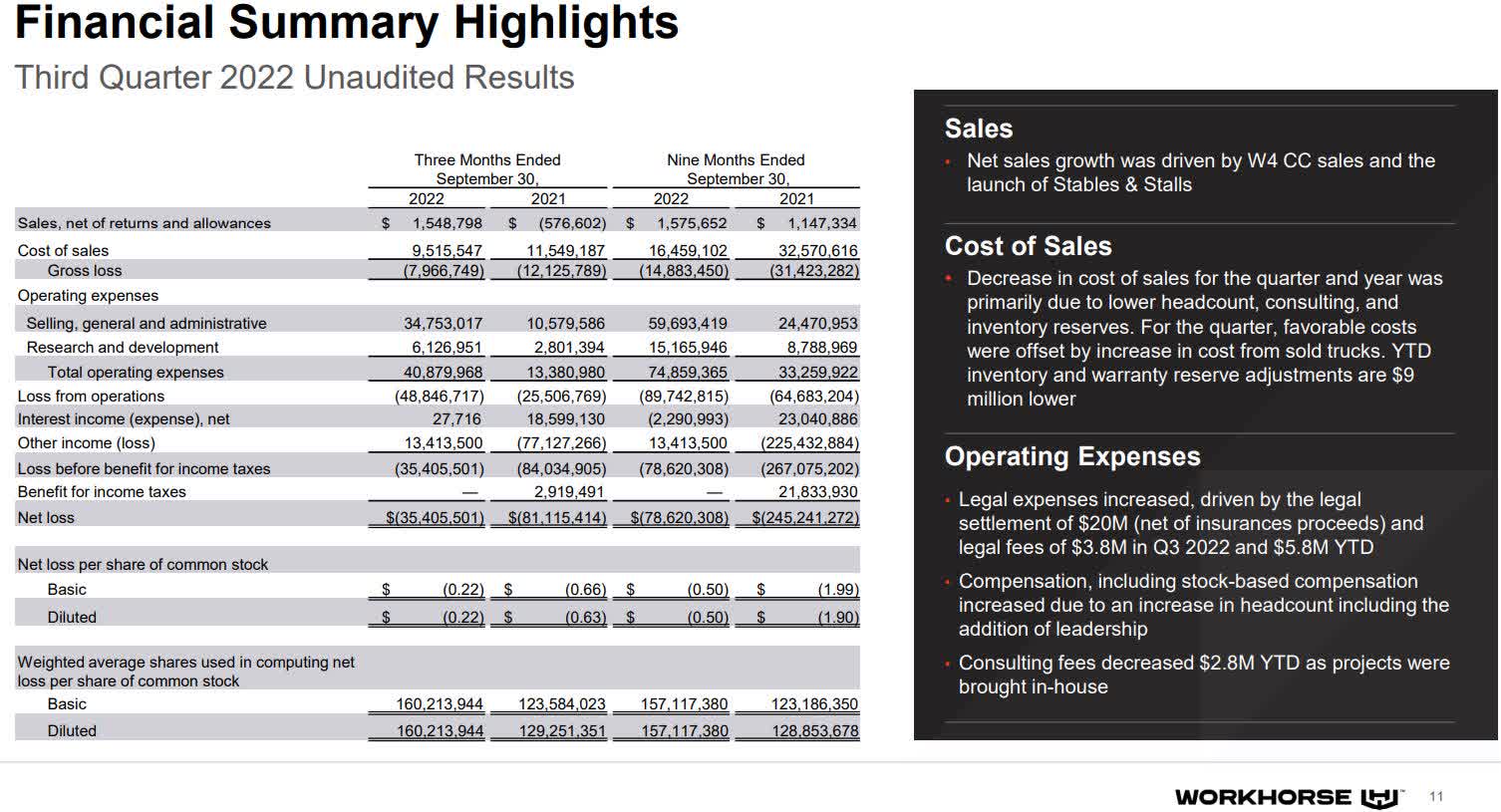

Investor Presentation

So, with its cash burn rate significantly lowered by improving efficiencies in several areas, the company, if it can actually produce products that will go to end users while getting more aggressive with its sales and marketing, could actually start to achieve some of the potential the market thought it has had for a long time.

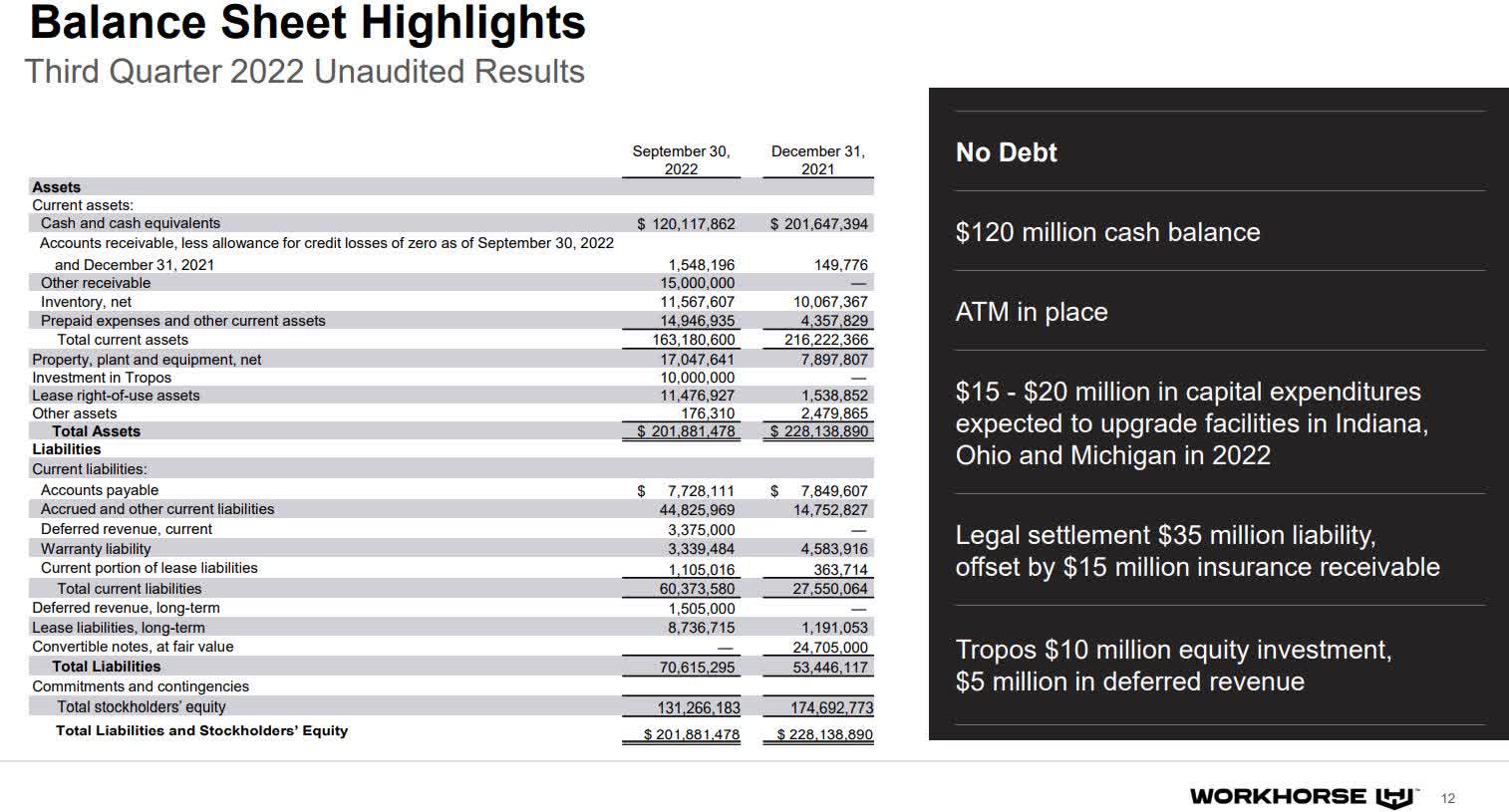

At the end of the third quarter, Workhorse Group Inc. had cash and cash equivalents of $120 million with no debt.

Investor Presentation

In the recent earnings report Dauch stated that the “most significant differentiators in our industry today is the ability to produce OEM quality vehicles at scale from a full size and modern plan.” My immediate response when I read that was, “what does that have to do with Workhorse?”

In the case of Workhorse, the company needs to figure out how to successfully deliver numbers that move from double digits to triple digits, before thinking in terms of the scale potential of the overall electric vehicle (“EV”) industry.

I also believe it’s being to aggressive in the near term in regard to product development. I understand the attraction of having more to throw at the wall to see what sticks, but with most tech and/or EV companies, they usually develop one product that has market demand and expand the product line from there.

To start with several products in the EV sector, and then work on another in its Aerospace segment, doesn’t make a lot of sense to me. When taking on this many projects the result is that they grow much slower than if the focus was on one product that has legitimate market demand.

If Workhorse were in a much better financial place it wouldn’t be as much of an issue, but with limited resources and cash burn, even after being reduced, still a factor, the company needs a sustainable win. At this time, it doesn’t exist.

Price movement and potential

The share price movement as many readers know, has dropped from a high of approximately $43.00 per share on February 1, 2021, to a 52-week low of $1.56 per share on December 22, 2022. It is currently trading a little above that, but there’s no catalyst at this time that would drive its share price higher, other than the promises and possible potential of the company if it’s able to actually deliver products that have enough demand to grow revenue to higher levels.

TradingView

While the company has the pieces in place on the operational side of the business, it must improve its efficiencies and unleash its sales and marketing team in order to build a real business.

Sitting on nice facilities isn’t a business, selling products in response to market demand is a business. In other words, offering solutions to a problem people and businesses have are what drives growth and success. As this relates to its share price, it remains to be whether or not the firm has hit its bottom at $1.56, or it has a lot further to drop before it does. A lot of that depends upon the commentary from its next earnings report in regard to progress its making on sales.

If it’s all pushed out to the future again, which I suspect it may be, then we’ll probably see its share price test the $1.00 per share mark or lower.

Conclusion

From the last earnings report it appears he has the team in place he wants, and so now it’s a matter of executing on the strategy of the company based upon its business model.

In other words, we always hear about how how sales are increasing and are about to break out in the near term, and that’s no different with the company now, as it has stated it learned to crawl in 2022, suggesting in 2023 it’s getting ready to run.

Like I mentioned earlier, WKHS is developing several delivery vehicles it’s close to ramping up for production, yet it continues to struggle with producing one of its vehicles, let alone several. With little communication from the company concerning the progress it is making ramping up production for its EV delivery trucks, and ongoing issues with delays, it’s getting harder and harder to think this company is close to turning things around.

What’s puzzling is, if it has truly readied its production facilities, all it has to do is successfully execute on ramping up production and start delivering vehicles to the end user. If it was successfully doing so at this time, I think there would have been word from management concerning the progress. In this case, silence isn’t golden, and it only makes me think there are more disruptions in the process that is resulting in further potential delays.

In the end, Workhorse Group Inc. does in fact have a lot of potential, but weak execution and delays seem to continue to be embedded in its culture, even under new management, and until that is solved, along with proof there is actual demand for its EV delivery products, the Workhorse Group Inc. share price really has nowhere to go.

Be the first to comment