Chalabala

In a previous report, I discussed the prospects of Woodward (NASDAQ:WWD) and concluded that given the current price of the stock and the forward projections for earnings, there is little reason to assign a buy rating. The stock, however, did see its stock appreciate by 3% compared to 1.8% for the broader markets. In this report, I will be discussing the Q4 2023 earnings as well as the full year earnings, discuss the guidance and update my stock price valuation.

A Stellar Year For Woodward

For the full year, net sales increased 22% to $2.91 billion, while adjusted earnings grew 48.9% on top of which share repurchases layered providing growth of 53% to the adjusted earnings per share while free cash flow even grew 65% to $144 million.

Woodward

For the full year, aerospace sales which include both the commercial and defense sales grew 16% with segment earnings growing 25.5% helped by better productivity, high utilization of airplanes spurring aftermarket demand, higher OEM build rates and better pricing.

In the fourth quarter, sales were up 11% to $455 million driven by the commercial airplanes business which saw 19% growth in OEM sales and 21% growth in aftermarket sales which is a very consistent performance throughout the commercial aerospace business. Admittedly, it is lower than the 41% growth for Commercial OEM and 28.5% growth rates observed in the previous quarter but that is also in part a comp effect. Defense aerospace performance was less appreciable with Defense OEM sales down 13% for the quarter due to loser guided weapon system sales while aftermarket sales were up 18%. So, the story of Q4 for Aerospace was: Strong commercial aerospace and aftermarket performance offset by Defense OEM.

Woodward

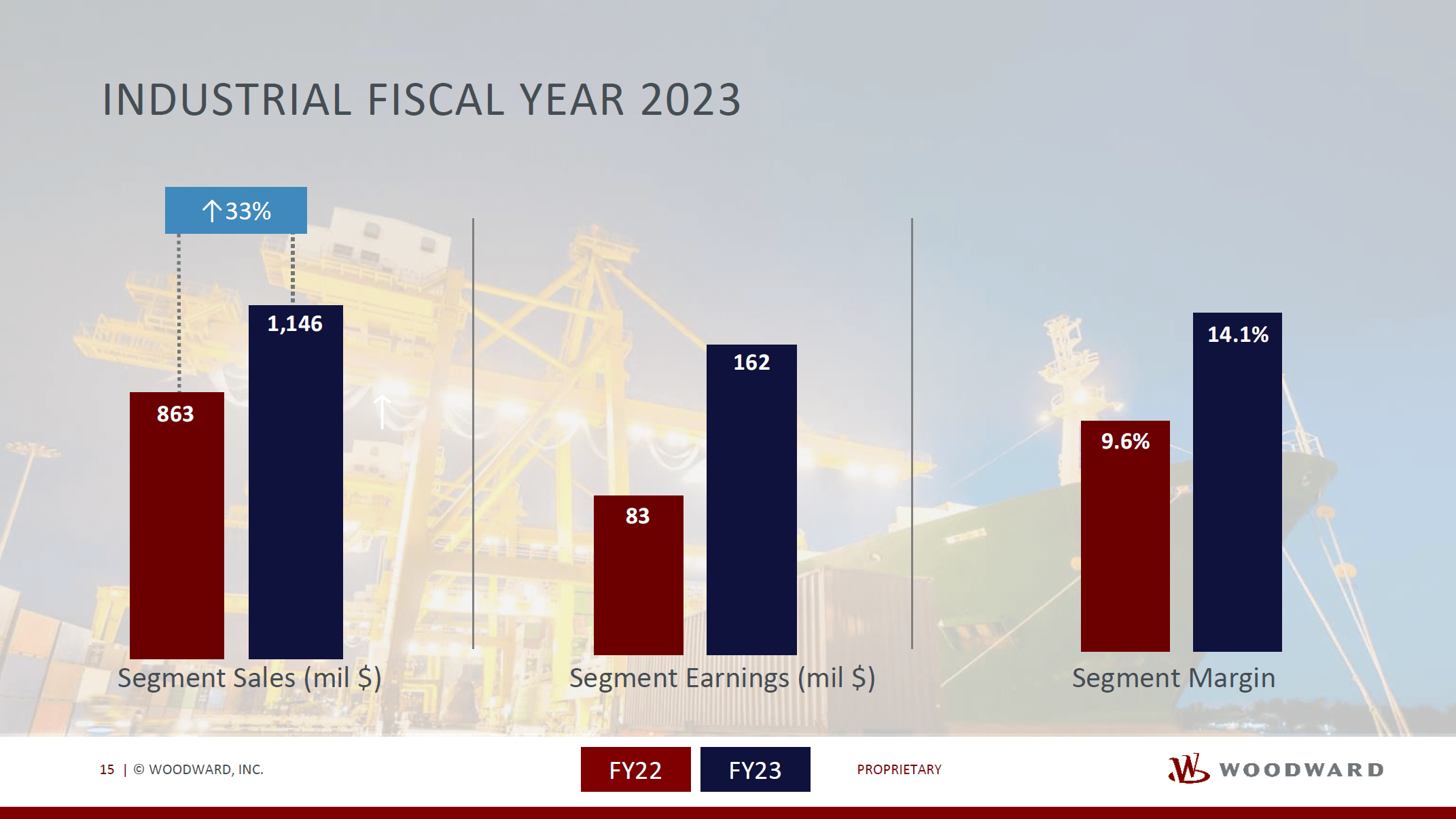

Industrial sales grew 33% driven by better pricing, demand for backup power for data centers for example, global aftermarket sales and demand from Asia sending Power Generation revenues up 21%. Global marine market dynamics balanced shipyard capacity and higher utilization drove Woodward sales for Transportation up 49% while Oil & Gas sales were up 23% driven by continued investment in LNG projects and LNG heavy duty truck demand from China persisting.

The Q4 2023 figures were even better with 39% growth in sales and segment earnings growing 157% compared to full year earnings growth of 95% for the segment.

All with all, Woodward’s results for the year were strong carried by demand, productivity gains and better and better pricing.

What Are The Growth Drivers For Woodward?

Going forward, Woodward can count on continued growth in OEM rates to increase output as well as higher aftermarket sales. Those growth rates will be tapering as the industry is gradually increasing production providing a more challenging comp. I also expect Woodward to be able to benefit from the growing demand for defense equipment while energy transition trends offer opportunities in marine and Oil & Gas. The high LNG heavy truck demand for China could also provide some solid growth in case strength is maintained throughout the year, but this is a very volatile market dependent on the diesel-LNG spread.

Woodward

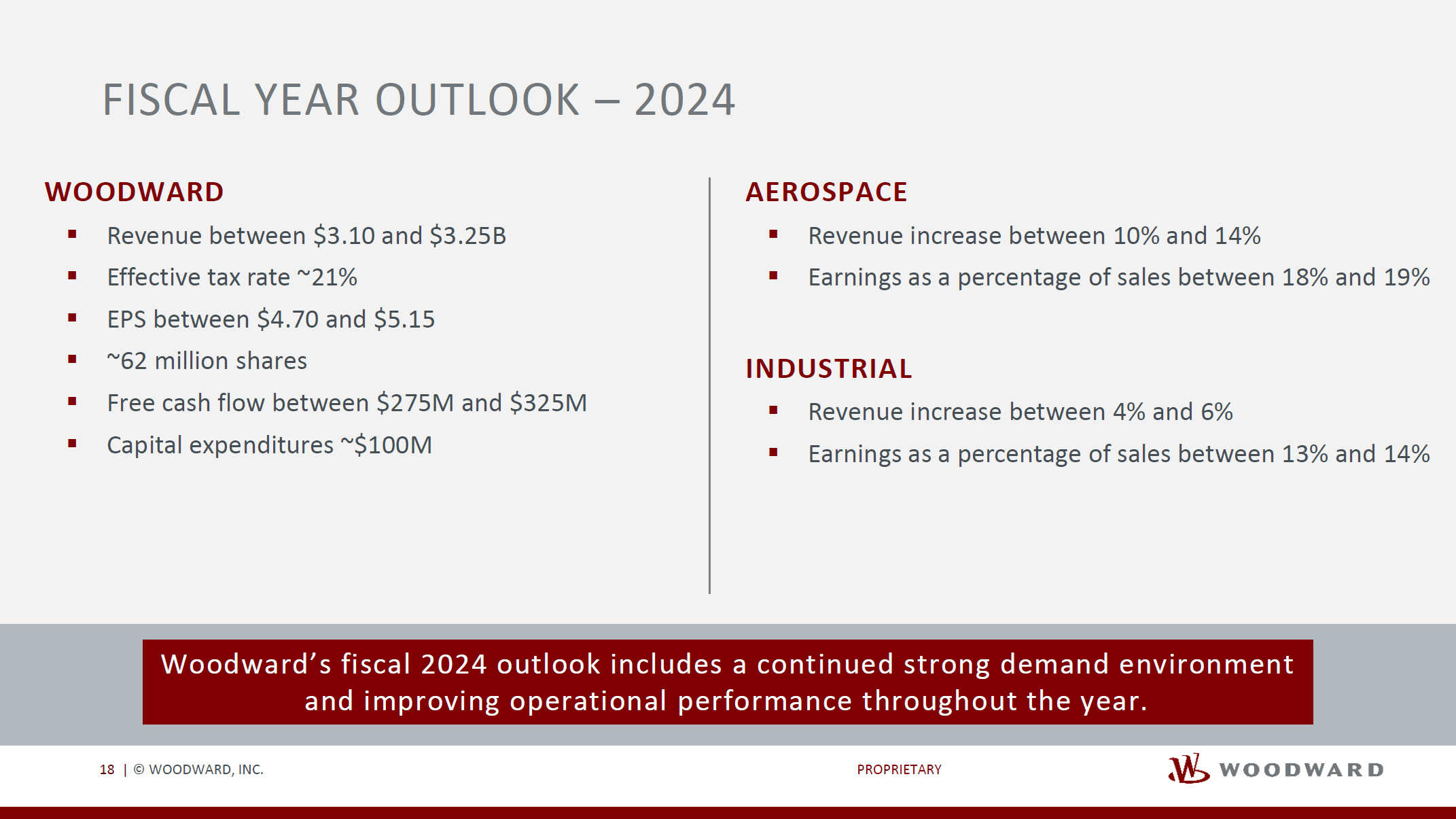

For FY2024, Woodward is expecting 6 to 12 percent growth in revenues driven aerospace growth, which in turn is driven by defense opportunities, higher OEM build rates and higher defense sales on top of better pricing and efficiency with margins of 18-19 percent while Industrial revenue growth is expected to be between 4 and 6 percent. While the growth rates are tapering, that is not what I am extremely focused on as Woodward’s end market should be able to show long-term sustained growth. What I am liking is that on 6 to 12 percent growth, Woodward is guiding for $275 million to $325 million in free cash flow generation which indicates around 90% to 125% growth in free cash flow.

What Is Woodward Stock Worth?

The Aerospace Forum

Generally, I am looking for market outperforming upside and while I do like Woodward’s business and its execution, they forward growth figures do not point at that. However, that does not mean that over the longer-term this could be a pretty nice hold or even a buy and hold or put differently: Every sign of weakness in stock price unrelated to changing business fundamentals should provide a nice entry point.

The stock is also one notch away from flipping to a buy rating due to its appreciable 3-year alpha value and we see that the estimates for EBITDA and free cash flow towards 2025 have become more positive with EBITDA estimates for 2024 and 2025 having increased by 10% and free cash flow estimates are up low single digits. On the wings of longer-term demand trends in commercial, aerospace, defense as well as trends in energy transition I do think there is a lot to be positive about and while my rating remains Hold, it is inching closer and closer to a buy rating.

Conclusion: Woodward Stock Benefits From Long-Term Tailwinds

Woodward showed strong FY2023 earnings and while growth rates might be tapering, the demand trends in its end markets are positive with long-term growth envisioned. So, I do consider the stock a nice hold in your portfolio and based on the forward projections I believe that the stock is inching closer and closer to a buy rating.

Be the first to comment