FOTOGRAFIA INC./iStock Unreleased via Getty Images

Elon Musk looks like the Grinch who is trying to steal our Santa Claus rally, as his stock plummets into the end of the year and takes the rest of the megacap technology-related names with it. Tesla (TSLA) cratered 10% yesterday after reports that it would be pausing production in Shanghai, which is odd considering that Chinese stocks have been outperforming in anticipation of the end of the President Xi’s Covid-Zero policies. For example, Alibaba has rallied 20% over the past month. Aside from the discount being inflicted on Tesla shares, due to what I think is the unpredictability of its CEO, the stock’s 70% decline this year is not far off from what has occurred to the rest of the technology behemoths since the market’s peak.

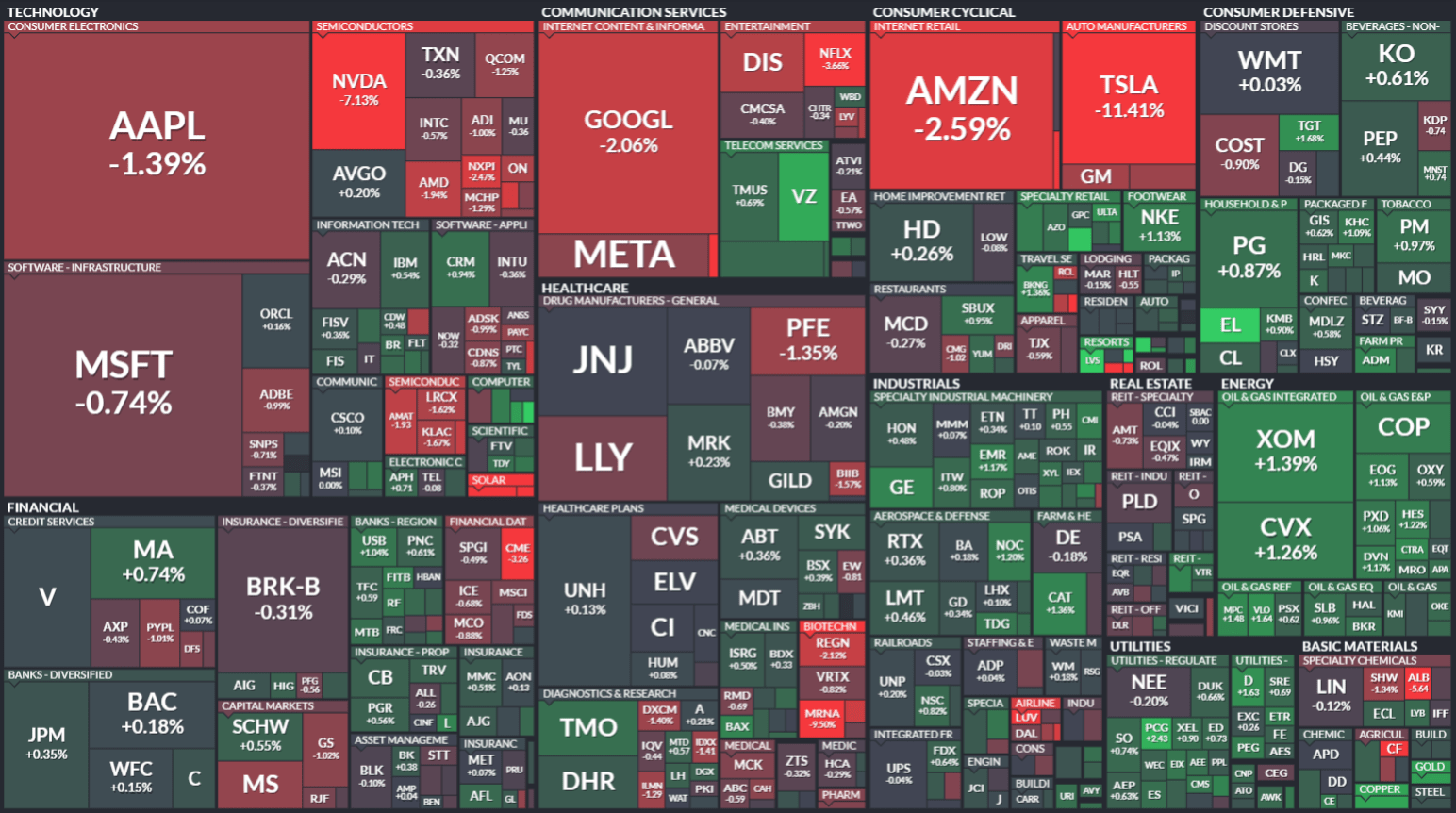

Finviz

Facebook parent Meta Platforms is also down 70% from its high last year, while Netflix is down 60%, Nvidia has cascaded 57%, Amazon has fallen 55%, and Google has suffered a 42% decline. This makes Apple look like a superstar with just a 27% pullback. It reminds me that the generals are typically the last to fall during a bear market, which is what I think we are seeing in spades today.

Finviz

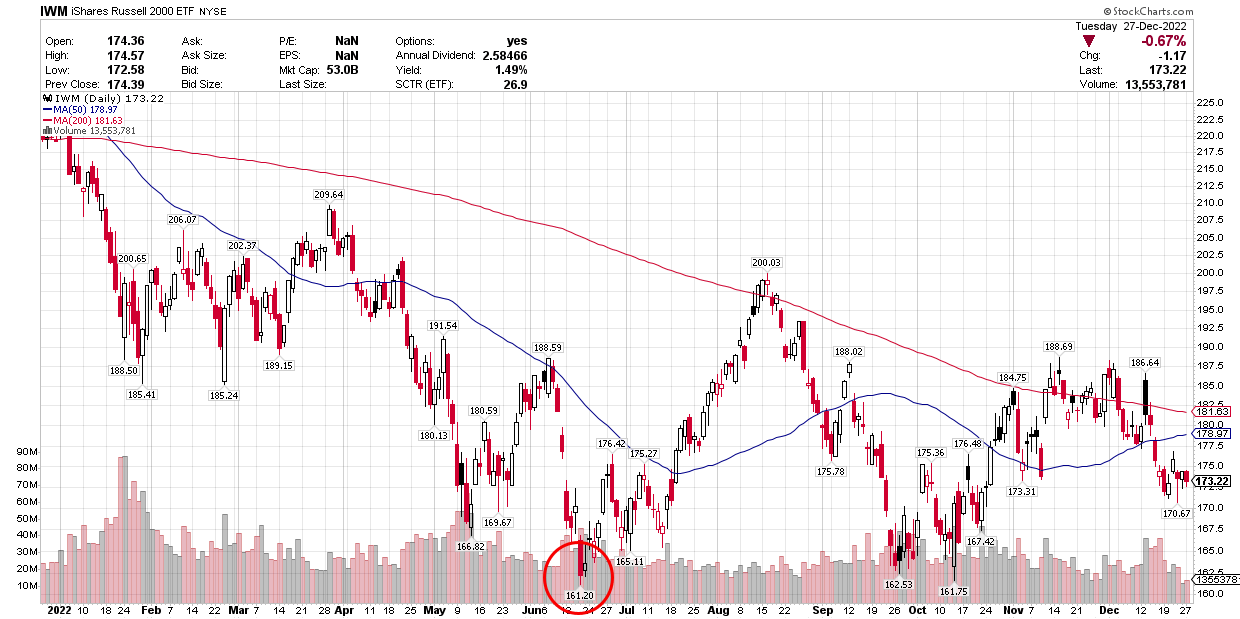

It is also notable that the Russell 2000 index of small cap stocks, which could be considered the foot soldiers on the front lines of the economy, bottomed in June. This is not unusual, as bear markets typically beat up the constituents from the bottom up, as lower quality falls first. Yet that also suggests the broad market decline is coming to an end rather than being in its middle or early innings.

Stockcharts

We see a similar story in valuations, as pointed out in Ed Yardeni’s most recent Stock Market Briefing, which shows the differential between market caps.

S&P 500 – forward Price/Earnings 17.3x and forward Price/Sales 2.22x

S&P 400 – forward Price/Earnings 13.2x and forward Price/Sales 1.17x

S&P 600 – forward Price/Earnings 12.8x and forward Price/Sales 0.88x

There are bargains to be had in mid- and small-cap stocks that cannot be found in the largest companies. Therefore, a further decline in the major market averages is more likely to be a function of rotation from expensive growth to more reasonably priced value than a broad decline in all stocks.

I am still holding out hope for the Santa Claus Rally, but it may be dependent on investors seeing value in the largest companies that dominate the indexes.

Lots of services offer investment ideas, but few offer a comprehensive top-down investment strategy that helps you tactically shift your asset allocation between offense and defense. That is how The Portfolio Architect compliments other services that focus on the bottom-ups security analysis of REITs, CEFs, ETFs, dividend-paying stocks and other securities.

Be the first to comment