Jack Taylor

Investment Thesis

Monster Beverage Corporation’s (NASDAQ:MNST) price has had a great run-up in the past few years. Its price has literally doubled since the end of 2019. We believe recently its sales growth showed signs of stalling or slowing down while its cost and expenses continued to rise. When combined with the overall backdrop of the energy drinks market, we believe its current price is too high for a long-term valuation.

Company Overview

Monster Beverage, founded originally as Hansen’s Juice in 1935, is based in Corona, California. Currently, Monster Beverage Corporation is a holding company and conducts no operating business except through its consolidated subsidiaries. The subsidiaries develop and market energy drinks. It has three operating and reportable segments as of Q3 of 2022, Monster Energy Drinks, Strategic Brands, and Other.

Strength

When you look at Monster Beverage’s presentation, you would be forgiven for mistaking it as a pure advertisement for the company. It is colorful, energizing, and full of images of all the marketing and promotional activities the company has participated in. If you are new to the stock as an investor, you will quickly realize that one of the company’s strengths is its brand. The unmistakable claw print on its aluminum bottles definitely leaves an impression on the consumers even if they didn’t buy the beverage. Most investors probably don’t know that Monster Beverage has more than 16,400 registered trademarks and pending applications in various countries worldwide. Below is a list of its core brands of energy drink beverages shown in its 10-K.

MB (Company 2022 10-K)

The Monster brand’s strength can be seen in its market share. The company stated in its Q3 earnings call that it is one of the two dominating brands in the U.S. energy drink market, with 36.9% ending on October 22, 2022, while Red Bull takes 36.1%.

mb (Calculated and Charted by Waterside Insight with data from the company)

While in the coffee plus energy drink category, the company takes 52.1% market share, and Starbucks (SBUX) Energy takes 46.9%. The U.S. and Canada sales accounted for approximately 56% of its overall sales. The company also has a global reach that helps establish its dominant place in energy drinks, in which the U.S. and Canadian markets contributed 65.7% of the total net sales in 2021.

Monster Beverage Net Sales by Region (Calculated and Charted by Waterside Insight with data from the company)

Look at its history; Monster Beverage has always had a gradual growth in its sales and revenue. But it really jumped from 2016 to recent years, as its earnings from operation have safely exceeded its operating expenses, making it more profitable than ever.

Monster Beverage Operating Expenses vs Earnings (Calculated and Charted by Waterside Insight with data from the company)

In its 10-K, the company attributes its success to the ability to innovate and introduce different new beverages that receive positively by the consumers. In its Q3 earnings call, its CEO said it has a robust launch pipeline coming in the first half of 2023 in energy drinks, alcoholic beverages, and still/sparkling water. Of the company’s three business segments, energy drinks are the most important, taking up 94.2% of the total net sales. Although starting in 2023, it could add another segment of alcoholic beverages, we guess. It’s also where most of the innovative beverages take place. It anticipated launching its first alcohol-based product line in Q1 of 2023 based on the acquisition of CANarchy Kanok, a craft beer and hard seltzer company, last year. CANarchy’s net sales were estimated to be $134 million in 2021, which is about 2.7% of Monster Beverage’s 2021 total net sales of $5.5 billion.

Monster Beverage Net Sales by Segment (Calculated and Charted by Waterside Insight with data from the company)

Weakness/Risks

Monster Beverage stated that during 2020 and 2021, it experienced a shortage of supply that impacted its operation and sales. Perhaps that is the reason that it was accumulating large inventory at hand. However, its days of outstanding sales have also risen.

Monster Beverage Inventory vs Sale Pace (Calculated and Charted by Waterside Insight with data from the company)

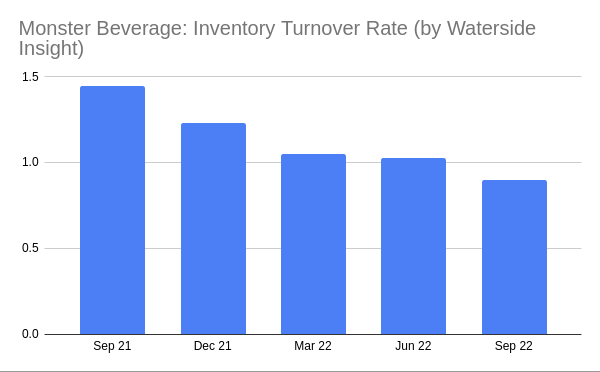

And since 2021, its inventory turnover rate has decreased by more than 30%.

Monster Beverage Inventory Turnover Rate (Calculated and Charted by Waterside Insight with data from the company)

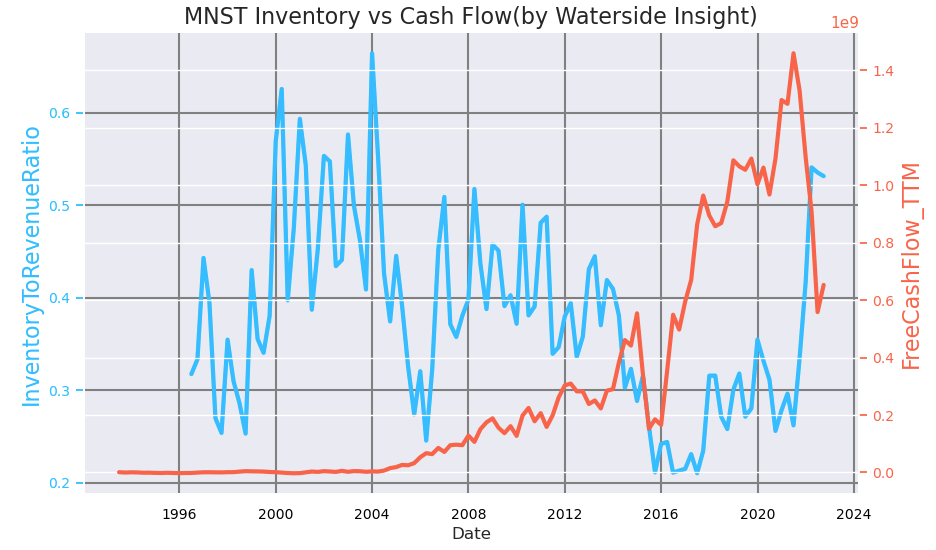

Would this inventory level be appropriate, or is the company experiencing some unexpected slowdown in sales that makes the inventory level become a mismatch? Looking back at its history, the inventory-to-revenue ratio seems to be negatively correlated with its free cash flow. And this ratio has risen sharply and once again crossed the 50% mark.

Monster Beverage Inventory vs Cash Flow (Calculated and Charted by Waterside Insight with data from the company)

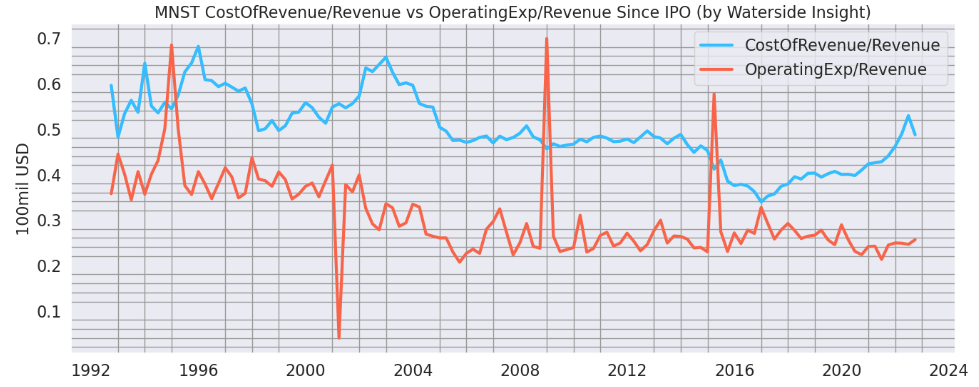

Its revenue has increased by almost 30% compared to 2019, which is a strong sign of growth. Perhaps high inventory could help ease the supply chain problem to help it keep the operating expenses as a portion of revenue roughly the same level compared to pre-pandemic. But its costs of revenue as a percentage of revenue have continued to rise.

Monster Beverage Cost of Revenue vs Operating Expense Over Revenue (Calculated and Charted by Waterside Insight with data from the company)

Last but not least, there has been more health awareness of the high sugar and caffeine intake in energy drinks, along with artificial ingredients, in recent years. The company stated in its 10-K that it believed the whole category of energy drinks had taken a hit because of these health concerns, including more regulatory scrutiny and disclosure requirements. Also, coming back to brand differentiation, Monster Beverage disclosed that it spent $417.6 million in 2021 on advertising and promotion. That is about 32% of its operating expenses that year. It had spent a similar percentage on brand promotion in the past few years. Each drink product that the company introduces has a lifecycle. Some of them can be limited to only a few years. Constant promotion and continued product innovation to develop different beverages are a must for the company to maintain its competitiveness and success. The cost and expenses associated with all of it could hardly come down, in our opinion.

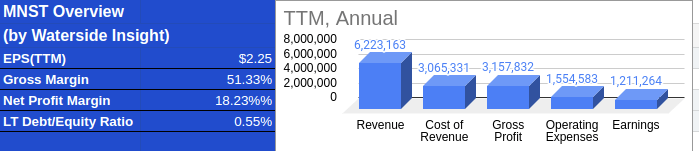

Financial Overview

Monster Beverage Financial Overview (Calculated and Charted by Waterside Insight with data from the company)

Valuation

To assess the fair value of Monster Beverage, we include all our analysis above and use our proprietary models to estimate with a ten-year projection forward. Looking ahead, the energy drink market is expected to continue its growth trajectory into 2030. It was estimated to be an 8.4% CAGR growth for the U.S. market through that time. Although, as the health concerns stated earlier, we believe this market’s growth may not be as smooth, we are willing to take this estimated growth as the upper end of the forecast range. Assuming the company maintains its market share and its revenue grows with the whole pie at 8.4% per year for the next ten years in its revenue. By the most optimistic assumption, we also assume the same growth rate for its free cash flow, which generally grows with more volatility and slower than the revenue, then we reached a fair price of $42.48. For it to have the current $100 valuation, it will need to grow 20% per year in its free cash flow for the next ten years. Even if we factor in faster growth in its alcoholic beverage offering, that it might double its net sales from 2021, it still only accounted for about 5% of revenue contribution. We couldn’t reach such an elevated growth rate to match the current market price. Unless Monster Beverage is going to decimate Red Bull and Starbucks to take over the market shares in trove, we see the current prices to be too rich in valuation.

In our bullish case, we estimated Monster Beverage Corporation would grow in high double-digits most of the time, but with some bumps along the way, it reached a valuation of $70.98. In our bearish case, where the company incurs more volatility in its growth but still largely maintains a strong growth momentum that eventually reaches over double its current free cash flow, it is valued at $49.58. In our base case, we see it maintaining modest growth in 2023 and 2024 due to the economic slowdown while resuming stronger growth afterward with some volatility; it was valued at $63.90.

Conclusion

Monster Beverage has had a great execution in its revenue growth and profit generation, despite the challenges brought by the covid. Its sales growth continued throughout the past three years, but so did Monster Beverage Corporation’s expenses and costs that we don’t see being easily mitigated in the near term. On top of this, there are signs of sales growth stalling. Although Monster Beverage Corporation has strong brand recognition among consumers with multi-channel marketing promotions, there is still overall health awareness concerning the energy drinks market as a whole in the long term. We chalked up our valuation and deemed the current price to be too high to be sustainable. We recommend a sell on Monster Beverage Corporation at this level.

Be the first to comment