Scott Olson

I have owned Berkshire Hathaway (NYSE:BRK.A) (NYSE:BRK.B) for most of my investing career. It is the company I’ve written about most extensively on this website. I’m amazed at what Warren and Charlie have built, and feel personally indebted to them for sharing so much knowledge through their writing.

Berkshire warned investors long ago that forward returns would not be as impressive as in the past, since the company had grown so large. In recent years, I considered Berkshire the “bond” portion of my portfolio because I felt fixed income offered little return for substantial risk.

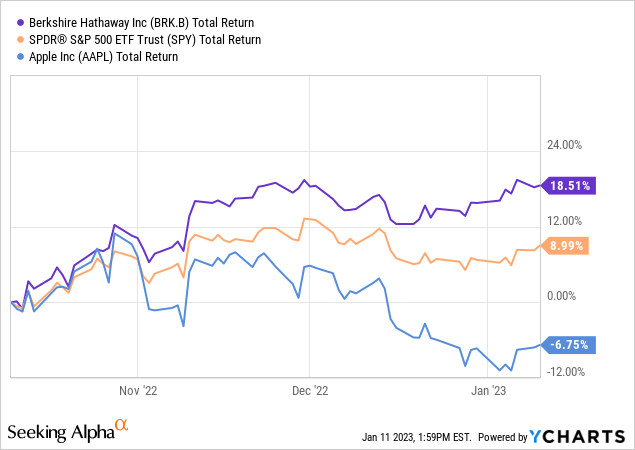

This has changed, as fixed income now offers a higher return than it did a few years ago. Coupled with a recent surge in Berkshire’s share price and a decline in its largest holding, Apple (AAPL), I feel Berkshire is now fully valued, or perhaps overvalued, for the first time in years.

Current Valuation – Book Value

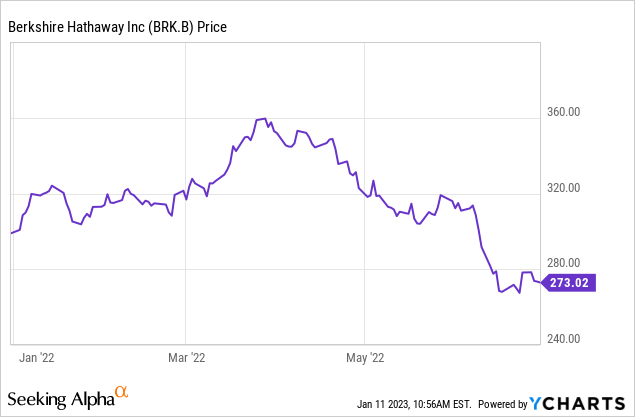

Given the opportunity, would you have sold Berkshire at $360 last March before it crashed down to $260? I would have.

What if I told you that Berkshire is just as expensive now near $320 as it was last year at $360?

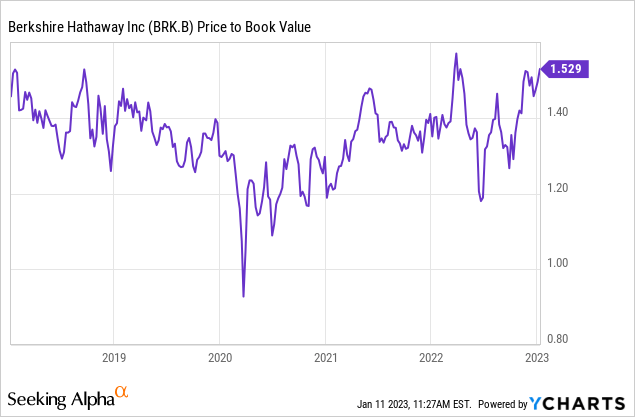

Berkshire’s market cap on March 31, 2022 was $780 billion. Shareholder’s equity was $508 billion, for a Price/Book Value of 1.54x.

Berkshire’s current market cap is $702 billion. Shareholder’s equity as of Q3 was $455 million. The equity book since then is roughly flat, with weakness from Apple and Bank of America (BAC) offsetting strength from Chevron (CVX), Coca-Cola (KO) and American Express (AXP). Adding $5 billion in Q4-22 operating earnings (my estimate) leaves a Price/Book Value of 1.53x.

This is the top of the range shares have traded over the past 5 years. Nearly every time it has reached this level, it has reverted back to the ~1.3x level in short order.

Current Valuation – Earnings Per Share

Berkshire’s operating businesses are having a good year as the economy further normalizes. Berkshire owns businesses with pricing power that are inflation resistant, so it is not a surprise that they have done well this year.

Berkshire has had a record year and I believe we’ll see another $5 billion in earnings in Q4, down from Q3 due to seasonality in their energy business currency gains in “Other” reverse due to the weaker dollar. BNSF rail traffic has also weakened in Q4, with total Intermodal & Carloads off 8.5%.

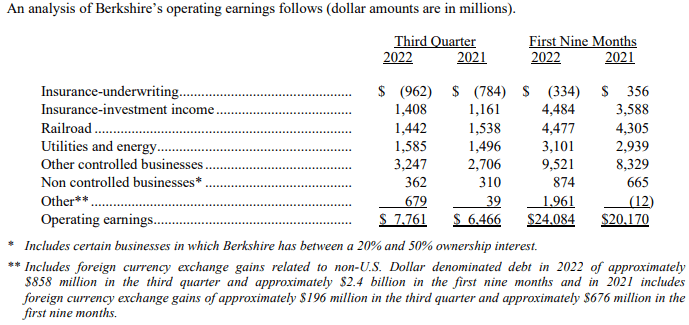

Berkshire Q3 Operating Earnings (Berkshire Hathaway’s website)

At the current $702 billion market cap, $29 billion in net earnings implies a 24x P/E before any consideration of “look through” earnings from the equity book.

The $325 billion in equities, at a P/E of ~16, adds another $20 billion in “look through” gross earnings. We need to subtract the $5 billion in dividends received (Q3-22 dividend income was $1.28 billion) from this, leaving $15 billion net.

Adding $29 billion in Operating Income to $15 billion in “net” look through earnings, assuming we do not apply any discount to it (and I’d argue that we should) implies at 16x P/E.

More reasonable, for sure. But hardly cheap.

Optionality of Cash and Share Repurchases

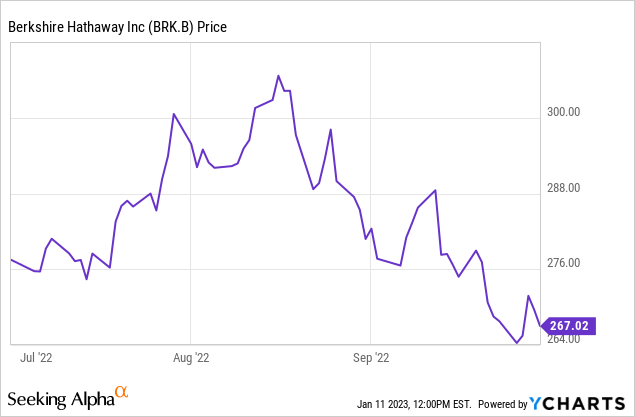

Despite Berkshire’s share price being under $280 for much of Q3, Berkshire only repurchased $1.05 billion worth of shares in the quarter, a huge drop off from last year.

Berkshire had $109 billion in cash as of September 30th. The $11.6 billion Alleghany acquisition closed a few weeks later, likely leaving the cash balance today around $100 billion.

This is low relative to recent history and the size of Berkshire’s float. I do not think Berkshire will go much lower than this level. Coupled with the higher share price, I think share repurchases and opportunistic acquisitions are off the table for the near future.

Should we value Berkshire’s holdings and associated look through earnings at 100%?

When considering equity valuations and associated earnings, I believe it’s appropriate to apply a moderate discount, perhaps in the 10-15% range, since Berkshire cannot sell most of its holdings without significantly impairing their price. Even with Apple, its largest and most liquid holding, what would happen if Berkshire announced it was selling? I believe Apple could drop 15% on the news.

Buffett has often talked about “Mr. Market” swinging from overly optimistic to overly pessimistic. But Berkshire largely loses out on the ability to capitalize on Mr. Market’s jubilant moods.

Would Berkshire sell Coca-Cola, a company that’s had flat operating income for a decade yet still trades at 25 times earnings, if they could exchange all 400 million shares for the current market price? I suspect they might.

There’s no absolute “correct” answer here, and each investor will have different feelings about it based on their goals, timeframes, and feelings about Berkshire’s specific holdings. But it reminds me of an old lesson from my father when I was bragging about the “value” of the individual cards in my baseball card collection. He asked “which one of your friends would buy them” at the prices I was quoting. I didn’t have an answer.

Berkshire largely can’t sell its holdings at the prices they’re quoted at, and I believe that merits a small discount when thinking about Berkshire’s valuation.

Conclusion – what should investors do?

While I believe Berkshire has gotten ahead of itself, it’s far from a crazy valuation. For many investors, the best course of action may simply be to do nothing, especially if Berkshire is held in a taxable account with a low cost basis.

If I had offsetting tax losses, I may have sold Berkshire here, hoping to buy it back lower in the future. The way I look at it, even with some optimistic assumptions, Berkshire is trading at an earnings yield of ~6.5%, and I see many other opportunities to earn more than that safely.

Instead, I chose to buy a January 2024 $310 protective put for $17, to add some general downside protection as part of an overall portfolio strategy, as I’m more heavily invested now than much of the last 18 months. If Berkshire continues higher from here, it likely means I’m having a very good year! If Berkshire drops back as part of a broader market sell off, having this hedge will allow me to be more aggressive in using my remaining cash.

Best of luck to all Berkshire investors and thank you for reading!

Be the first to comment