serg3d

Nvidia Corporation (NASDAQ: NVDA) stock is currently down close to 50% as the GPU maker continues to struggle. Nvidia’s struggles come on the back of a few years where the stock continued to outperform, but now it is increasingly struggling due to a number of headwinds, including the decline of cryptocurrency. Management reiterated during the latest quarter that it will take some time for the excess inventory in the market to clear, and until then sales will be under pressure. The excess inventory largely stems from mining rigs, which were bought in excess amounts to mine very profitable crypto coins, operations which are no longer functional.

Where Is The Market Headed?

Meanwhile, GPU prices have been declining as demand continues to falter. Nvidia has not faced any major issues, mainly due to the fact that price declines have largely affected secondary sales. This means that margins have remained more robust than they otherwise would have. On the other hand, a weakening market has meant that revenue has continued to decline. Revenue continued to slide during the latest quarter, as lower sales led to a 12% decline QoQ and a 17% decline YoY. This trend is expected to continue into the next couple of quarters.

New GPUs are expected to come to the market, (mainly the 4000 series), and will largely be targeting the mid-range PC market, more specifically laptops. These might help Nvidia bring in some extra customers, cushioning some of the blow that has resulted from weaker sales.

However, headwinds remain with PC demand, specifically desktop sales hitting 20-year lows, and so GPU sales are likely to continue to be under pressure. Furthermore, older GPUs are becoming increasingly discounted due to the excess inventory on the market. This means that consumers are likely to prefer slightly older versions and second-hand GPUs rather than buying new high-end performance GPUs – or potentially even mid-end GPUs, which could still be more expensive.

Overall, the company’s margins are lower, declining reasonably as increasing costs have continued to weigh on net income, which declined by 50%. Both inflationary pressure and a reduction in demand are now starting to weigh on Nvidia margins, but margins should become steady over the next few quarters. The real issue remains sales, which are not likely to recover anytime soon.

On a positive note, data center sales have also been on the uptrend in recent times, with an expected growth of 12-15% for the year. This means that Nvidia should continue to grow by double-digits, and potentially around 20% for the year. The new H100 systems are increasingly in demand by those running on the cloud, which means that one of the few industries that have weathered the recessionary outlook should continue to be relatively steady in terms of demand in 2023. This bodes well for Nvidia.

The real story for the GPU market is cryptocurrency, and many cryptocurrencies are significantly down, ever since central banks started raising rates. For the foreseeable future, major economies and major central banks are expected to continue to pull liquidity away from the market. This puts the likes of Bitcoin under pressure and could push prices lower to $11,000 levels, which would translate into even more mining rigs coming off the market.

With crypto prices falling and mining unprofitable, the GPU glut is only set to increase. Furthermore, miners are now becoming increasingly consolidated, among a few players, which puts further pressure on the remaining miners and demand for GPUs. Meanwhile, the likes of Ethereum (ETC-USD) have decided that they will remain with GPUs to mine their crypto, which should help demand if prices remain within the current trading range.

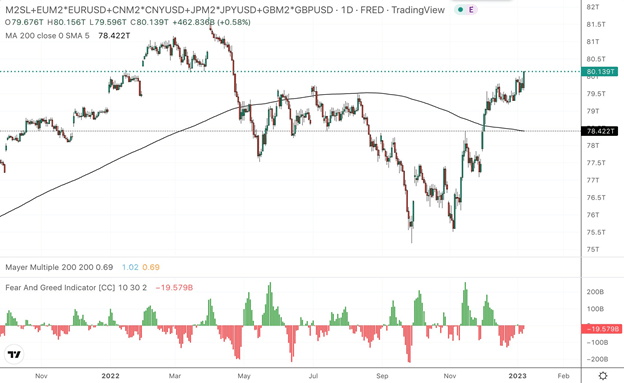

Central banks, specifically the European and Federal Reserve have indicated they will continue to pull liquidity out of the market, and forecasts increasingly are likely to push M2 levels down to $70 trillion levels. This would be a decline from the current levels of around $90 trillion. In order to get back to historical trends, M2 would have to fall back to around $60 trillion levels. This would mean that cryptocurrency is going to continue to be under pressure for the foreseeable future. Money supply remains the key to cryptocurrency prices, and falling liquidity will be a bane for many crypto operations.

Twitter

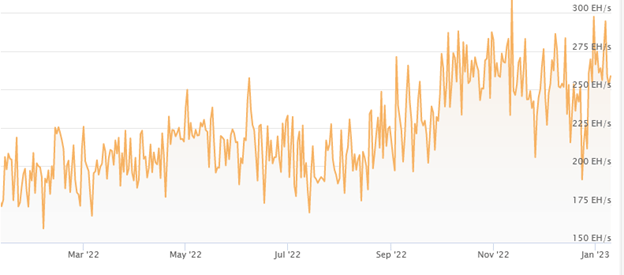

Secondly, the hash rate for Bitcoin has been volatile for crypto, hitting all-time highs before retreating. The falling hash rate, while it may seem like a positive, is only further indicating that the total number of miners is on the decline. This trend of consolidation and improving hash rate will make it harder for mining operations to be profitable at these levels, putting further pressure on overall GPU sales.

Coinwarez

Therefore, Nvidia is highly susceptible to a slowdown in the coming quarters. Already, early indications from channels are indicating that the semiconductor industry is in a bit of a downturn. Revenue for Taiwan Semiconductor Manufacturing Company Limited (TSM) is down, and the extent to which revenue is declining is broadly indicative of the trend.

Where Are The Financials And Valuation Headed?

Nvidia is likely to continue to see a decline in its revenue over the next couple of quarters and may bottom out in the third quarter of 2023. This would mean that revenue could fall by another 10-15%, considering the current demand trend, and that would put further pressure on the valuation.

While a number of analysts have maintained that Nvidia is unlikely to keep witnessing a slowdown, there is very little indication of this. This is likely to push margins further to the downside, and, therefore, means that the forward P/E is likely to be around 50-60x earnings, making the likelihood of the stock heading down further a real possibility. Revenue is likely to come in slightly lower; currently, the average estimate by analysts is around $6 billion, but it could fall below $5.9 billion from the latest quarter.

Beyond revenue, gross income which came in at 53-54% during the latest quarter, could also be under pressure again, falling further and may head towards 50%, as pricing pressure continues to affect the company. Meanwhile, NVDA stock’s technicals show that the market is clearly setting up for further declines, with the put-to-call ratio severely skewed towards puts, at 1.5. This clearly illustrates that Nvidia currently is not favorably viewed by investors and traders.

In conclusion, Nvidia Corporation continues to face a number of issues going into 2023. Considering that a lot of the revenue was built on an unsustainable market, i.e., cryptocurrency, the company will likely find it much harder to get back on track in the near term. This puts pressure on the stock to decline further, and the stock could be heading towards $100-110 over the next few quarters, as interest rates continue to increase and discount rates continue to go higher. Investors that are looking for a long-term play may wish to continue investing in Nvidia Corporation stock, however, provided they are willing to weather the volatility.

Be the first to comment