hamzaturkkol

I wrote my first article on the ProShares UltraPro QQQ ETF (NASDAQ:TQQQ) at the end of 2021, where I said I was planning to buy a small piece of the exchange-traded fund (“ETF”) in 2022 if we saw a massive selloff. While we did see a slow grind lower for most of the year, I didn’t see the panic and fear that was my main sentiment indicator to pull the trigger. I also don’t think the valuation of the biggest holdings is attractive today, despite large selloffs in many well-known mega-cap tech stocks. It is still on my watchlist as 2023 develops, but I have been busy buying other holdings in recent months.

Investment Thesis

TQQQ has the potential to provide outsized returns for investors that have to stomach to buy when sentiment is at its worst. The most recent time this happened was in March of 2020, and I’m still looking for the return of a similar sentiment to be the contrarian indicator I’m looking for. The other piece I look at with any investment is the valuation. Since TQQQ is heavy on big tech, the valuation is more attractive today than it was a year ago, but that doesn’t mean I’m a buyer yet. It’s not as simple as valuing a single stock, but because I view the biggest pieces of the index as unattractive today, I’m still on the sidelines.

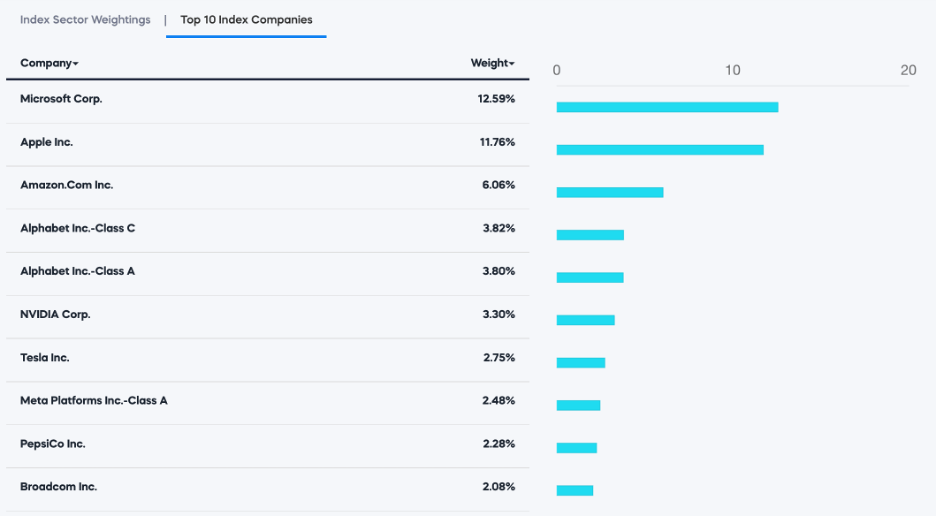

Top 10 Holdings

Despite the selloff in the largest tech companies in 2022, the Nasdaq 100 (QQQ) and TQQQ are still very overweight big tech. Outside of 2022, that has worked well since the financial blowup in 2008, but I don’t think that will be the same for the coming decade. If you look at market cycles, the leadership baton tends to pass from one sector (or a couple sectors) to another sector that lagged in previous cycles.

TQQQ Top 10 (proshares.com)

That has started to play out with energy being the clear leader in the last couple of years, but I think that we will see energy, commodities, and other real asset plays lead this market cycle. The big tech companies have developed good businesses and dominant market positions, but we will see if it translates to continued outperformance moving forward like it has in recent history.

Apple & Microsoft

Any discussion of TQQQ would be incomplete without discussing Apple Inc. (AAPL) and Microsoft Corporation (MSFT). The two companies make up approximately a quarter of the index, so forward returns for these two stocks will be a huge driver of overall returns. There is a lot to like about both companies and their stocks, from their high margin businesses, growing dividends, and massive buyback programs, but I just don’t see forward returns being all that attractive over the next couple years.

The biggest problem for me is the valuation of both stocks. While they aren’t as rich as they were a year ago, I’m not all that interested in buying shares of either company today. Microsoft still trades at a P/E just under 26x, while Apple sits just over 23x earnings. With their massive market caps ($2.2T for Apple and $1.8T Microsoft), I wonder how much they can grow from here. Since I’m assuming both stocks will be more or less flat for a while, that will likely be a drag on returns for TQQQ.

Amazon

Amazon.com, Inc. (AMZN) remains my last holding in the big tech companies. To be honest, I’m kicking myself for not selling a year ago, but hindsight is 20/20, but I think Amazon has more room to grow its $1T market cap. They are still the dominant business in the cloud sector with AWS, and their advertising segment continues to grow. While the ecommerce segment is typically considered the red-headed stepchild of the business by investors, I think the continued capex will pay off in the future. In my last article on the company, I laid out some of my thoughts on a potential spinoff of AWS and why the stock is attractively valued relative to past valuations. Amazon is another 6% of the index.

Google & Meta

Google (GOOG, GOOGL) accounts for more than 7% while Meta Platforms (META) adds another 2.5%. These two advertising giants have fallen out of favor recently after being two of the dominant companies out of Silicon Valley. While both companies are cheap compared to the last decade (with Google at 21.3x earnings and Meta at 15.9x earnings), I think both companies are one-trick ponies, and I am skeptical on both companies’ capital allocation strategies. If I were a shareholder, I would be frustrated with Google’s Other Bets Segment and I would definitely be disappointed with Meta’s push into the Metaverse.

Tesla & Nvidia

I think the valuation on both of these companies is very rich, but it’s not stratospheric like it was near the end of 2021. The two companies account for another 6% of the index. I wrote an article on Tesla (TSLA) yesterday, so I will focus more on NVIDIA Corporation (NVDA) here. I think Nvidia at 58.2x earnings is more likely to sell off than keep rising, but it is another business on my watchlist for several reasons.

The first is that their products will be in high demand for the foreseeable future. While the company has always commanded a premium valuation, a look back at the last decade shows why. They operate in a cyclical industry, so earnings aren’t going to increase consistently, but after a year or two of weaker results, earnings explode higher in the next couple years. I’m not interested in paying the current valuation, but if you get into the 20-25x range, and it would probably be a good entry point.

Pepsi & Broadcom

I recently wrote an article on Coca-Cola (KO), and my outlook for PepsiCo (PEP) is pretty similar. Long history of dividend growth, but the valuation (24.9x earnings) is too rich for the lackluster growth, and the 2.7% yield isn’t enough. Broadcom (AVGO) is probably my favorite individual stock in the top 10 right now for a couple reasons. The valuation is attractive just above 15x earnings and you get a 3.2% dividend with a history of strong dividend growth. It’s a part of the semiconductor industry like Nvidia, but it seems less prone to the big swings in earnings. The earnings growth isn’t likely going to match the last decade, but I still think the stock could produce decent returns for investors from here.

Conclusion

The first criteria I will always look at for any investment is going to be valuation. If it’s not attractive based on the valuation, I will hunt for other ideas, no matter what kind of business (or ETF) it is. Because I find the largest components of TQQQ unattractive today, it doesn’t make much sense to own the ETF. If the valuation continues to get more attractive in 2023, maybe that will change. The other thing I keep an eye on, especially for something like TQQQ, is the sentiment of the broader market.

I still haven’t seen the “Oh, ****” moment (insert your favorite four letter word here) in the market that would mark the sentiment change that would get the contrarian in me excited. The last time I saw that sentiment was when everyone was panicking in March of 2020 as markets were crashing. The sell now, ask questions later attitude provided numerous buying opportunities at the time and put TQQQ below $10 per share. A year later shares were above $40, which shows TQQQ’s potential to provide outsized returns if you choose your entry point well and don’t overstay your welcome. If you had even better timing and sold late in 2021, you could have sold above $80.

Again, this hypothetical using a past selloff is easy to point out because hindsight is 20/20, but it is an example of how a leveraged ETF can perform off a market bottom. It is much harder to do moving forward for many reasons, but TQQQ’s potential to provide outsized returns in a short period of time is why it remains on my watchlist.

Be the first to comment