designer491/iStock via Getty Images

I write this from Italy, so it’s going to be short. Today, the CPI surprised to the upside. On a year-over-year basis, the CPI rose 9.1% vs. an expected increase of 8.8%. The Core CPI (ex-food & energy) was a lot less scary, rising 5.9% year-over-year vs. an expected 5.7%.

Despite there being some rather strong prints (over the past six months, the CPI is up at an annualized rate of 11.1%), the dollar so far is unchanged, 10-yr T-bond yields actually fell a bit (and at 2.9% are still far below inflation), and gold rose only $19/oz, and it is still way below its all-time high of $2032/oz two years ago. Moreover, inflation expectations today are unchanged from yesterday and are relatively modest: 5-yr breakeven inflation rates are 2.5%, and 10-yr BE inflation rates are 2.3%. And as I write this, the stock market is down only 0.5%.

Why is the market so nonplussed? My friend Don Luskin and I both believe it’s due to the dramatic deceleration of the M2 money supply since late last year.

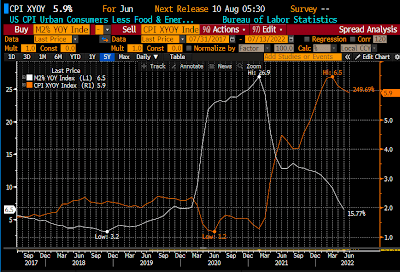

The above chart plots the year-over-year growth of M2 (white line) and the year-over-year change in the Core CPI index (orange line). Note in particular that there is about a one-year lag between big changes in M2 growth and big changes in inflation. M2 surged beginning in March 2020, and the CPI started surging about a year later. Then M2 growth started decelerating in March 2021, and the CPI started to fall in April 2022.

Note: I think it’s legitimate to use core CPI, because energy prices have been an order of magnitude more volatile than just about any other prices in recent years.

Given that M2 growth has been almost zero for the past 5 months, this exercise would suggest a strong likelihood that we will continue to see Core CPI inflation decelerate in coming months. None of this, of course, is a secret; anyone can run these numbers, and you can bet there are lots of folks in the bond market that have been watching these numbers like hawks for months. That would explain today’s lack of surprise.

This theory is also consistent with what I’ve been suggesting in recent months, which is that this round of Fed tightening will be unlike any other in the past. Why? Because the surge in M2 was a one-off event and it is already history. The market is adjusting to the expectation that the Fed is doing the right thing (i.e., not panicking but adjusting short-term rates higher in a prudent manner).

Furthermore, this all suggests that the Fed won’t need to tighten dramatically or strangle the economy, as it has in the past. My recent posts provide more grist for all of this.

The economy is likely going to survive this bout of inflation without serious consequences. It will be painful for many, to be sure, but the economy needn’t collapse.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment