piranka

What Goes Up

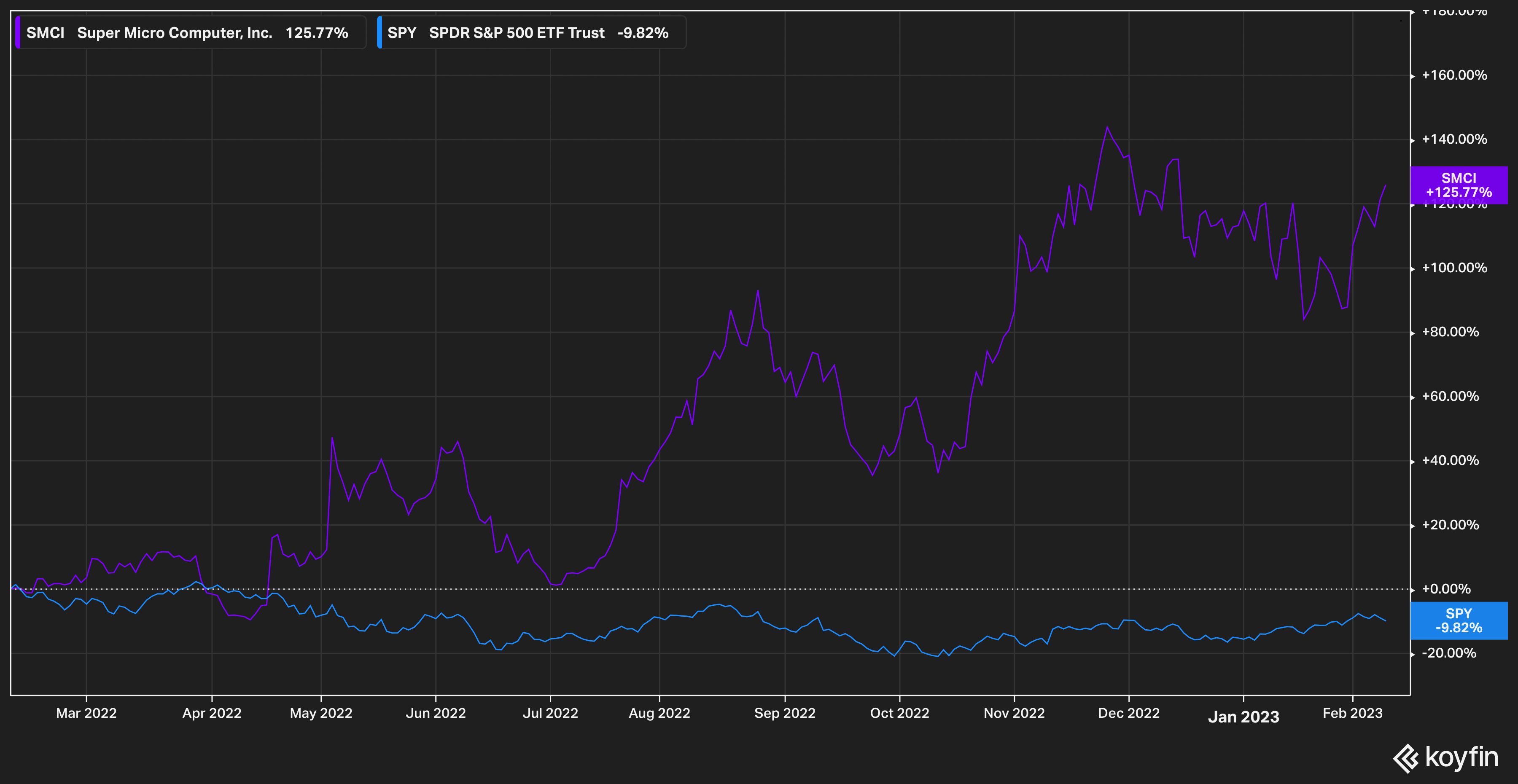

Times have been good at Super Micro Computer, Inc. (NASDAQ:SMCI). Over the past year shares at the server and digital storage solutions company have surged 125%, handily beating the S&P 500 (SPY), in case you couldn’t guess.

Koyfin

For all that, however, the stock still looks cheap. In this article we will outline why we believe Super Micro deserves the attention of investors.

Company Background

Super Micro operates in the competitive field of server and storage systems for diverse markets such as data centers, cloud computing, artificial intelligence, and particularly 5G applications (the company seems to have made considerable inroads with Verizon (VZ) on this front). This $4.6 billion market-cap company operates in Silicon Valley and has a presence in the Netherlands and in Taiwan. Super Micro develops products fully in house, from design to manufacture, and the company specializes in modular, highly customizable digital storage solutions for clients.

Interestingly, the company maintains a majority of its manufacturing in the United States. The company operates a 1.3 million square foot manufacturing facility in San Jose, while only 36% of its long-lived assets (manufacturing operations) are outside the U.S. The company also owns 36 acres of prime real estate in San Jose, on which it has recently completed a new 209,000 square foot manufacturing and storage facility.

The fact that the company has the ability to complete the full spectrum of work from design to delivery in the United States is critical. In a time where critical industries are looking to re-shore their supply chains from overseas, and when technological manufacturing capability seems to remain hyper-concentrated in Taiwan and thus subject to extreme geopolitical risk, Super Micro stands out among the rest.

Consider management’s note from their latest 10-K:

We manufacture the majority of our systems at our San Jose, California headquarters. We believe we are the only major server, storage and accelerated compute platform vendor that designs, develops, and manufactures a significant portion of their systems in the United States.

It should be noted that in 2021 the company was subject to a Chinese hack of its systems, which resulted in a prolonged Investigation by the United States government. It should be noted that neither Super Micro nor any of its employees were accused of wrongdoing.

The company’s customer base is also diverse, with over 1,000 customers in 100 countries. In a relatively niche B2B segment of I.T., it’s not atypical to see a vendor like Super Micro somewhat ‘captured’ by a major client who controls large swaths of its sales. Super Micro has successfully avoided this trap, however, with none of its clients representing more than 10% of its sales.

Super Micro’s competition is heavy-hitting. This relative David competes with Goliaths like Dell (DELL), Cisco (CSCO) and Hewlett Packard (HPE) for market share.

Show Me The Earnings

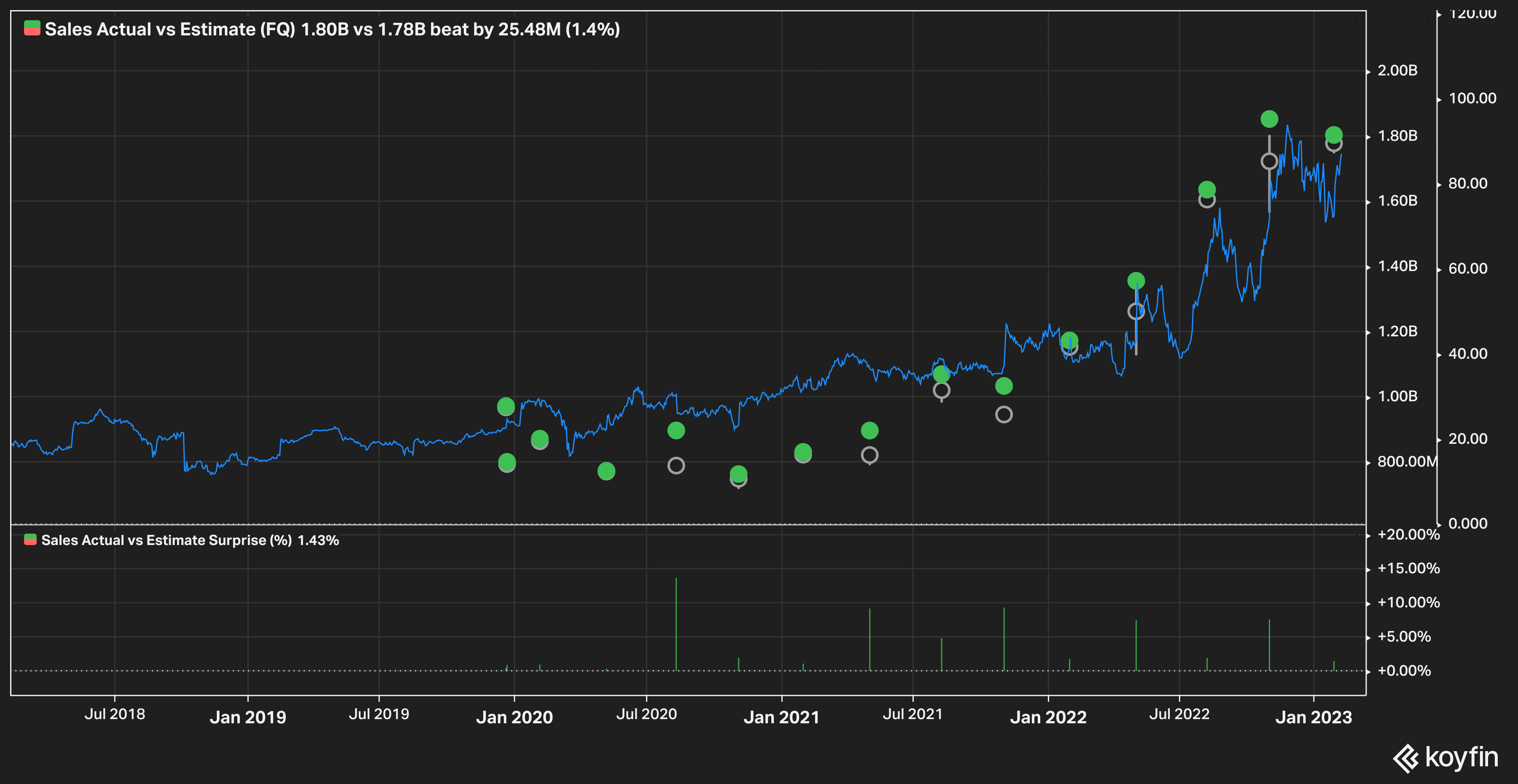

Super Micro is on a tear when it comes to earnings, posting 14 consecutive top-line beats versus analyst expectations, and 12 consecutive beats for EPS.

Super Micro Revenue (Koyfin)

The outlook for the company is positive as well. Analyst estimates peg revenue for Super Micro growing 20% year over year, from $5.2 billion in FY 2022 to $6.7 billion in FY 2023. Expected EBITDA for FY 2023 is $789 million, a shocking 93% increase year over year.

Returns on capital are also on the rise, a healthy sign for any business, with Super Micro posting an ROC of 27% in Q2. We like to see a healthy ROC in businesses we follow. If a company does not out-earn their cost of capital via their return on capital, it could mean things are taking a turn for the worse as the company cannot effectively put its cash to work.

Balance sheet health is similarly outstanding. The company is barely leveraged, with just a 0.2x total debt to EBITDA. On net-debt to EBITDA basis, the company is negatively leveraged. In our experience we have seen few balance sheets as fortified as Super Micro’s.

The health of the balance sheet serves, in our mind, as a counterweight to a potential downturn in business if macro conditions continue to deteriorate. The amount of ‘dry powder’ available for the company’s use would be critical in a challenging economic environment, and we like that Super Micro has a lot of runway here if needed (though hopefully it wouldn’t be).

Valuation

Now for the good part. Despite the massive run-up in shares over the last year, Super Micro still remains a relative bargain.

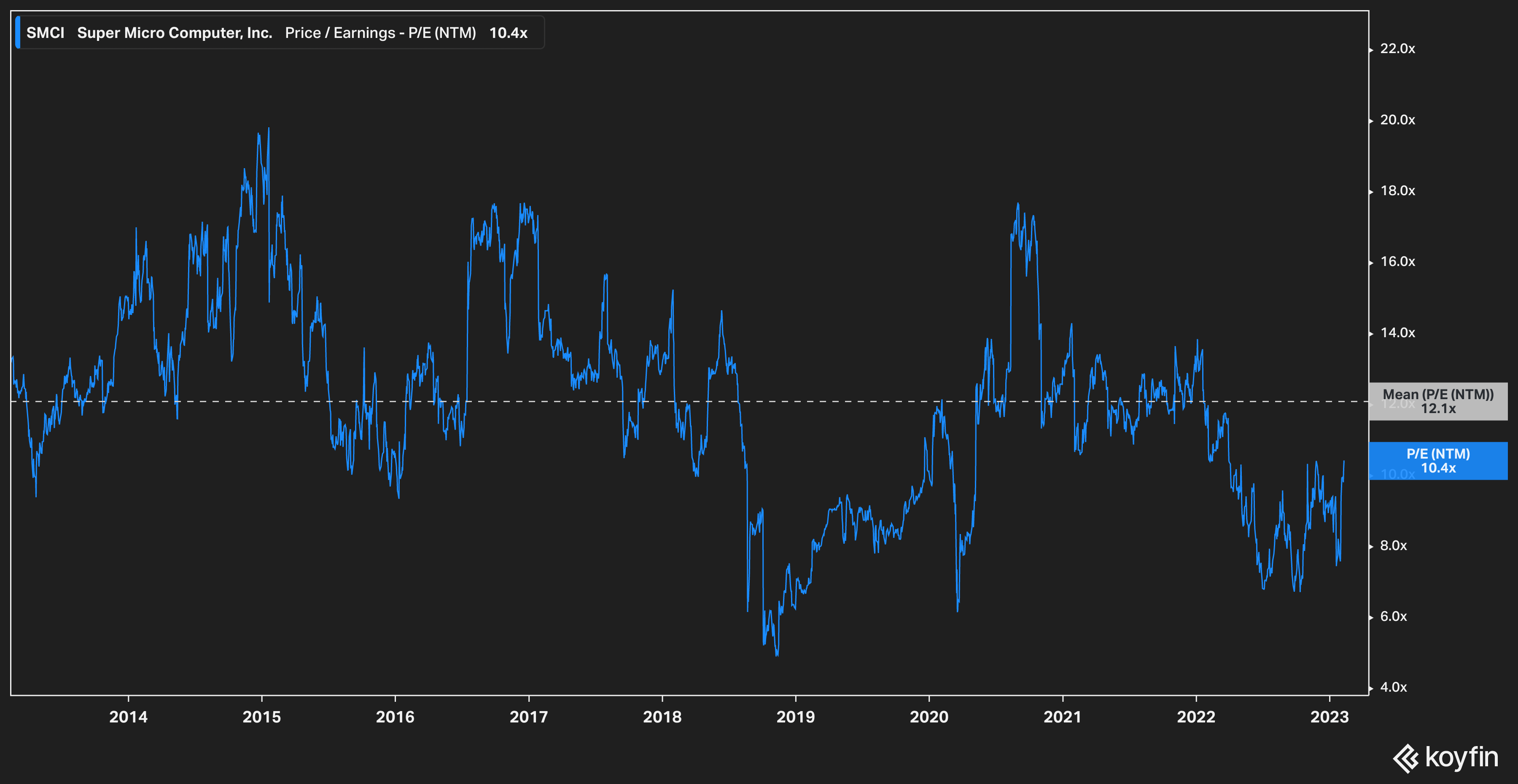

SCMI NTM PE (Koyfin)

Super Micro has had an average forward P/E of 12x over a ten-year period. Today the stock trades at 10x forward earnings.

Given the company’s history of excellence when it comes to operational execution, we believe that the likelihood of mean reversion in this particular metric is more likely than not.

In our view it’s reasonable to ascribe a 13x metric to the company. Utilizing FY 2024’s estimated earnings, this gives us a price target of roughly $120, a 28% potential upside from current levels.

The Bottom Line

Super Micro has a long track record of delivering excellent results for shareholders. Its servers are near best-in-class, and the company’s ability to compete in the space with companies many times its size is a testament to management’s ability.

Given the currently undervalued nature of the shares, we believe that investors should strongly consider Super Micro as it deserves a place in their growth portfolio.

Thank you for reading our article.

Be the first to comment