VioletaStoimenova

Article Thesis

The tobacco industry is attractive for income investors and offers reliability during times of crisis. With a potential recession coming, that could be of interest to investors. In this article, we’ll look at British American Tobacco (NYSE:BTI)(OTCPK:BTAFF) and Philip Morris (NYSE:PM) in order to gauge which one is the more attractive investment at current prices.

BTI Versus PM: Recent Performance

Both companies reported their most recent quarterly earnings this week, which is why we have relatively current data about their performance.

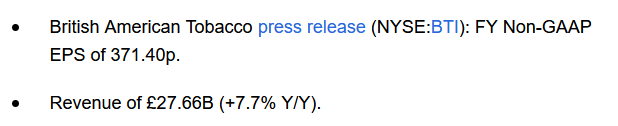

British American Tobacco’s headline numbers for the year looked like this:

Seeking Alpha

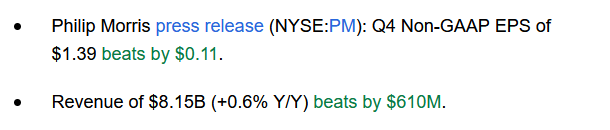

An 8% revenue increase is pretty attractive, although it should be noted that this was in Pound Sterling — at constant currency rates, revenue growth was less pronounced, but still far from bad, at 2.3%. Philip Morris, meanwhile, reported the following data for its most recent quarter:

Seeking Alpha

While currency rate movements were a tailwind for reported results for BTI, which reports in Pound Sterling, currency rate movements were a headwind for PM, which reports in USD. On a GAAP basis, revenue was up by less than 1%. At constant currency rates, PM’s revenue performance was better, though, as constant-currency revenue was up 7.9% year over year. We can thus say that Philip Morris operated better in the very recent past on an operational basis, due to strong demand for its products in many markets, while substantial price increases also were a major contributor to Philip Morris’ underlying growth. On the other hand, the fact that Philip Morris generates almost all of its revenue in foreign currency (due to not being active in the US), while the company reports its results in USD, makes it vulnerable to currency rate movements. These have been a major hindrance for Philip Morris in the recent past — while the company is doing well operationally, it is not able to turn this into actual GAAP profit growth of a similarly compelling magnitude. PM’s underlying performance is more compelling, but if that is not beneficial for shareholders as it is eaten up by currency rate movements, I’d say this is a tie.

BTI Versus PM: Reduced Risk Products

Cigarettes are the cash cow businesses for both British American Tobacco and Philip Morris. But cigarettes are not a growth business, as the smoking rate is declining in many countries around the world. Tobacco companies can offset this by increasing the price per pack of cigarettes, which has worked well in the past, but the core cigarette business does nevertheless not offer a lot of growth potential. In order to offset risks from growing regulation for cigarettes and other smokeable products, and in order to improve their growth profile, many tobacco companies have moved into the reduced-risk products market.

This includes a range of products, such as heat-not-burn alternatives to cigarettes, vaping products, and so on. Both British American Tobacco and Philip Morris have been spending heavily on their respective assets in the reduced-risk products markets, via R&D expenses and via marketing spending to improve the uptake rate for their new product introductions.

When it comes to the current revenue contribution of reduced-risk products, Philip Morris looks better. The company generates around 31% of its revenue from smokeless products, mainly via its iQOS/Heatsticks business. That’s close to one-third of the overall company-wide revenue generation, which is pretty attractive, considering that the iQOS business has been launched just a couple of years ago. British America Tobacco, on the other hand, generates around 10.5% of its overall revenue via the sale of reduced-risk products, as the so-called New Categories business contributed £2.9 billion out of £28 billion in revenues that the company generated in 2022. When it comes to the current market position, PM thus has the stronger reduced-risk product portfolio.

But the relative growth of these businesses should be considered as well, and that is where British American Tobacco outperforms Philip Morris: PM’s smokeless revenue grew by 18% year over year, as volume growth was partially offset by lower device revenues. British American Tobacco saw its New Categories sales grow by 41% year over year, which is more than twice the growth rate of the respective business unit at PM. In other words, PM has a larger but slower-growing reduced-risk portfolio, while BTI’s reduced-risk portfolio is smaller but growing at a way higher pace. Overall, both companies seem to be relatively well-positioned when it comes to reduced-risk products, and since one company has a better growth profile while the other has a larger current market position, I’d rate this as a tie.

BTI Vs. PM: Dividends

Both companies have a large following among income investors, and rightfully so: They offer reliable dividends during good times and during bad times, and their dividend yields are way higher than what one can get from the broad market today.

British American Tobacco has announced a dividend payment of 231 pence for the current year, paid in four installments of 57.7 pence each. At current exchange rates, that pencils out to $0.71 per share per quarter. Annualized, that’s $2.84, which results in a dividend yield of 7.7% based on BTI trading at $37 today. A dividend yield of close to 8% is highly attractive, of course, but additional factors should be considered, such as the safety of the dividend and the dividend growth rate.

Based on the profit that was generated last year, British American Tobacco’s dividend payout ratio is 62%, using the dividend per share of 231 pence and BTI’s adjusted earnings per share of 371 pence for the last twelve months. A dividend payout ratio in the low 60s is far from high for a tobacco company — competitors such as Altria (MO) regularly pay out around 80% of their net profits. BTI’s dividend is up 6% year over year, which is a solid growth rate in absolute terms and which is pretty attractive when combined with a dividend yield of close to 8%.

Philip Morris, meanwhile, is currently paying out $1.27 per share per quarter, or $5.08 per year. That translates into a dividend yield of 4.9% with shares trading for $104 right now. While a 4.9% dividend yield is still pretty solid in absolute terms, and way higher relative to what is available from the broad market, it’s way lower than BTI’s dividend yield — with BTI, investors get a 57% higher income stream, all else equal.

Philip Morris has generated adjusted earnings per share of $5.98 in 2022, including profits generated in Russia and Ukraine. When we back those out, earnings per share are significantly lower, at $5.34. Going with the higher of these two results, the dividend payout ratio is 85%. That does not mean that a dividend cut is particularly likely, but the dividend payout ratio clearly is elevated versus BTI’s dividend payout ratio. In other words, BTI has way more wiggle room, whereas things can’t go wrong for PM, due to an already somewhat stretched dividend payout ratio. As a result of a pretty high payout ratio, PM does not offer considerable dividend growth for now — the company has increased its dividend by just 1.6% in 2022.

Since British American Tobacco beats Philip Morris easily when in all three sub-categories — dividend yield, dividend payout ratio, and dividend growth — I see BTI as the better income investment today.

BTI Vs. PM: Profits And Valuation

Tobacco companies are oftentimes held for their dividends, but total returns matter as well. This, in turn, means that valuations are important, as they can have a large impact on share price appreciation (or lack thereof).

Based on earnings per share of 371 pence (equal to $4.52 at current exchange rates) in 2022, British American Tobacco trades at just 8.2x trailing adjusted net profit. Philip Morris, meanwhile, trades at 17.4x 2022’s adjusted earnings per share of $5.98. In other words, Philip Morris trades at more than twice the valuation British American Tobacco trades at — which seems like a pretty hefty difference in valuation. Both companies are geographically diversified, both have growing reduced-risk products, both are active in the same industry, and yet PM is trading at a more than 100% premium to BTI. I do not believe that this is justified. While one can argue that PM’s larger reduced-risk product portfolio justifies a premium (although others might argue that this is not true due to BTI’s higher RRP growth), I highly doubt that a premium this high makes sense. I thus see BTI with an earnings yield of 12.2% as way more attractive than PM with an earnings yield of 5.7% from a valuation perspective.

Final Thoughts

Tobacco companies tend to do well during recessions, relative to other industries: Demand for cigarettes and other tobacco products is not really dependent on the strength of the economy. In fact, some studies suggest that recessions could influence smoking rates positively, i.e. more people smoke during recessions. That makes PM, BTI, MO, etc. interesting in the current environment, where a recession seems quite possible, although a recession is not guaranteed.

Between British American Tobacco and Philip Morris, I believe that BTI is the significantly better choice right here: A way higher dividend yield, better dividend growth, better dividend safety, and a way lower valuation make it look favorable.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment