Spencer Platt

Introduction

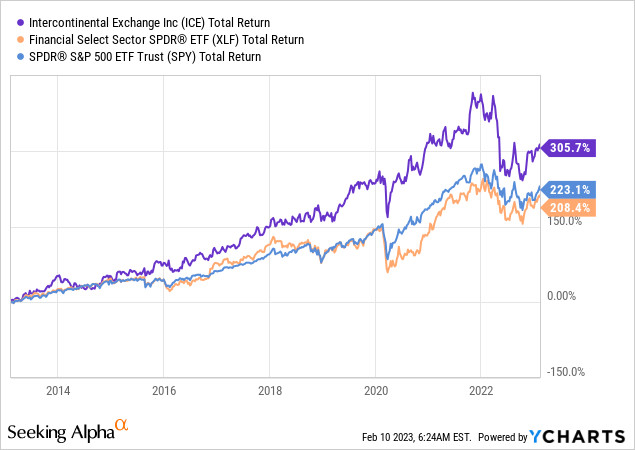

It is my pleasure to delve into the Intercontinental Exchange (NYSE:ICE), a company that has been on my radar for years as a premier dividend growth stock. While it is not currently a part of my portfolio, I believe it deserves a closer examination. In this article, I aim to highlight the factors that make ICE a standout company, especially in light of its recent dividend increase of over 10%, impressive quarterly results, resilience in the mortgage sector, and favorable valuation.

I understand that some investors prioritize a high yield, but for those seeking consistent and high-quality dividend growth in the financial sector, ICE may be an ideal choice. Through this article, I hope to provide insights into the exceptional qualities of ICE and what makes it a valuable investment consideration.

So, let’s begin.

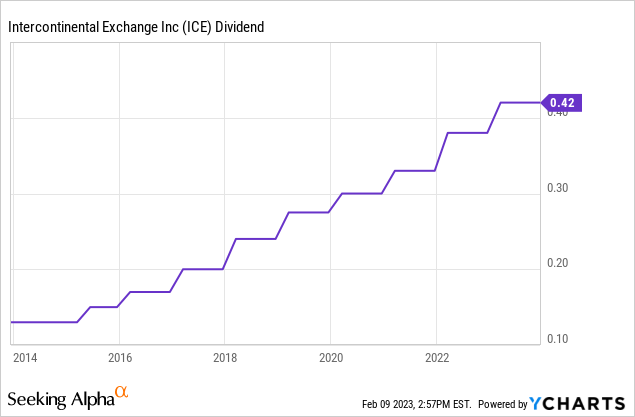

Another Hike! Assessing ICE’s Dividend

Assessing the driving forces behind the company’s dividend growth

In a recently published article focused on ICE peer CME Group (CME), I briefly highlighted my view on dividends in the financial sector.

Dividend investors seeking financial exposure often end up owning banks. Banks, both regional and money center banks, often have high yields and somewhat decent dividend growth. The problem is that banks are often very mature and barely growing.

Investors looking for dividend growth in the financial sector often face low yields, as dividend growth is often found in fintech niches. For example, companies like Mastercard (MA) and Visa (V) are terrific dividend growth stocks, yet their yields are low.

Atlanta-GA-based Intercontinental Exchange is somewhat in the middle.

ICE shares currently get you $0.42 in quarterly dividends. That’s $1.68 per year or 1.6% of the current stock price. This yield is in line with the S&P 500’s yield and slightly below the yield of the Vanguard dividend growth ETF, which I like to use as a benchmark.

The company started to pay a dividend in 2014. Adjusted for splits, it was barely above $0.10 per share back then.

ICE has maintained steady dividend growth over the past few years. The 5-year compounded annual dividend growth rate is 13.7%.

The most recent hike was announced on February 2, 2023, when management hiked by 10.5%. I was pleasantly surprised, as I expected dividend growth to be subdued due to the pending acquisition of Black Knight (BKI), but more on that later.

What makes ICE such a beautiful dividend growth company is its ability to grow free cash flow, the backbone of any sustainable dividend. The company has a payout ratio of just 29%, which is below the sector median of 31%.

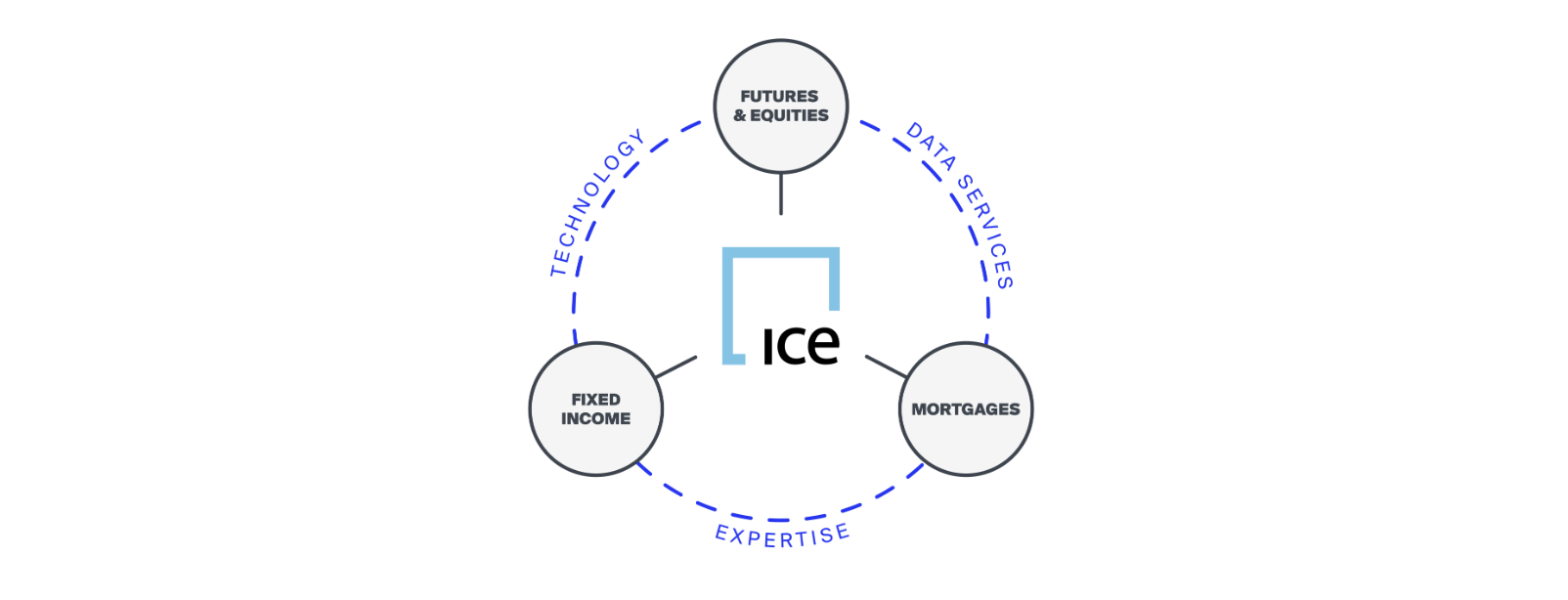

ICE is an asset-light provider of financial products and services. The company operates exchanges, like the New York Stock Exchange. In this segment, the company makes money on transactions and recurring streams like listings revenues. The company owns products in key asset classes like energy (ICE Brent oil), Dutch TTF natural gas, Northwest Europe LNG, and related. In agriculture, it owns cocoa, cotton, and sugar futures and options, among others. Products also include Euribor futures, gilts, SONIA, and others.

Intercontinental Exchange

In fixed income, the company offers fixed income data and analytics, fixed income execution through ICE Bonds, CDS clearing, and other multi-asset class data and network services. Their prominent fixed-income pricing and reference data offerings serve as the cornerstone for a comprehensive fixed-income network, providing customers with solutions that cover the entire workflow, including pre and post-trade analytics, various execution protocols, and indices.

In its mortgage segment, ICE has built a network designed to address inefficiencies in the U.S. residential mortgage market. The network spans the entire mortgage origination process, from application to closing and the secondary market, connecting key stakeholders and providing customers with data services and technology that promote greater transparency and drive efficiency gains. The Mortgage Technology segment of the company generated $1.1 billion in revenue in 2022 and accounted for 15% of the company’s overall revenue, excluding transaction-based expenses.

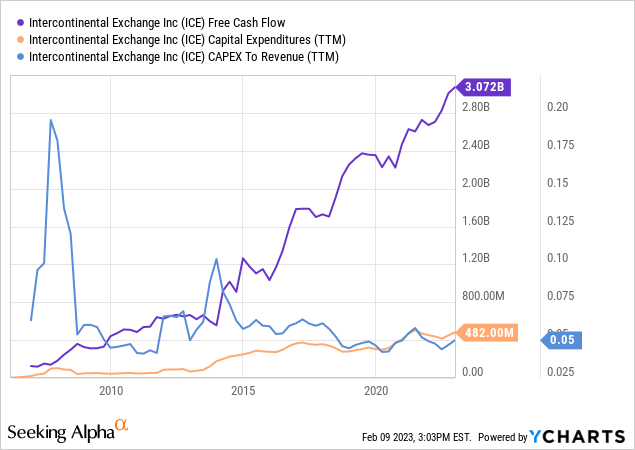

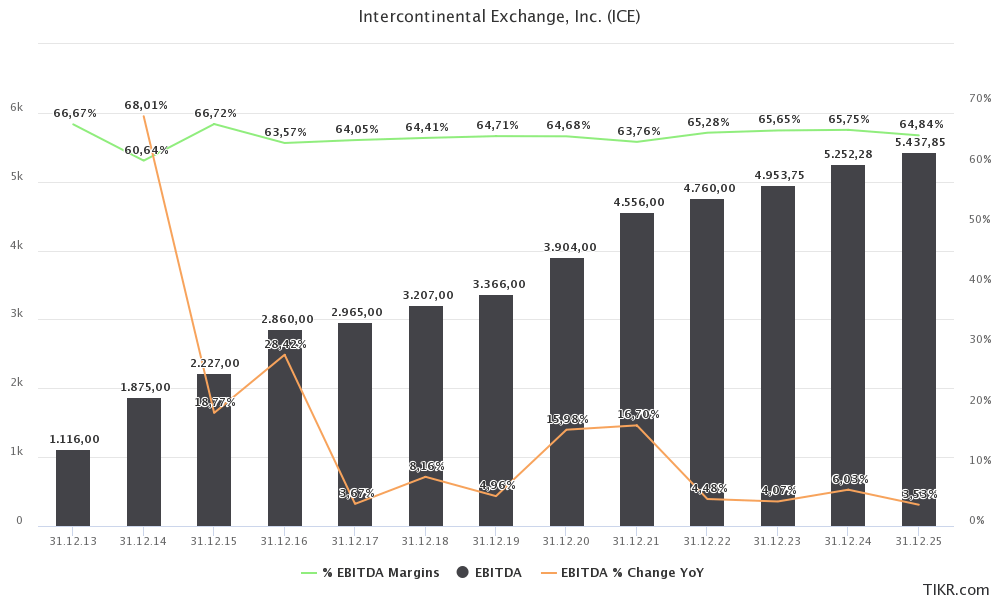

As the graph above shows, the company spends just 3% of its annual revenues on CapEx. It has an easily scalable business model, which has allowed the company to consistently grow its free cash flow.

Over the past 12 months, the company has generated more than $3.0 billion in free cash flow. This translates to an FCF yield of roughly 5.1% based on the company’s $60.1 billion market cap. That’s a big deal for two reasons.

- It protects the current dividend and offers more long-term growth opportunities.

- It allows the company to protect its balance sheet and engage in M&A to grow its business more rapidly.

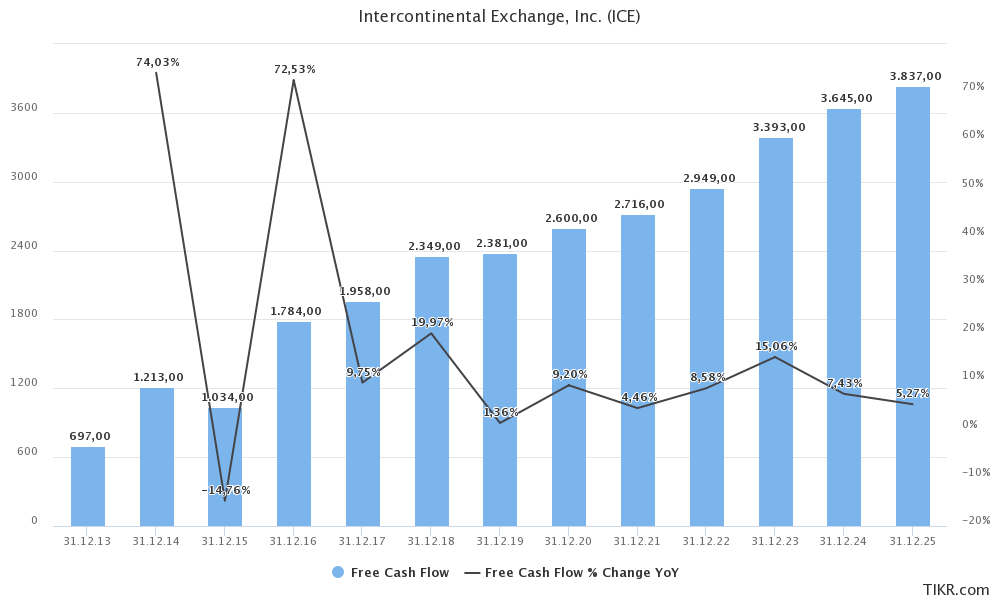

Between 2013 and 2025E, the annual compounded growth rate of free cash flow is 15.3%. This growth rate is extremely high and a result of high post-Great Financial Crisis growth. More recently (and going forward), the growth rate is (expected to be) in the 5% to 10% range.

TIKR.com

So far, we have established the following things:

- ICE pays a decent yield in line with the market yield.

- The company has high historical dividend growth, which is likely to be maintained thanks to…

- … high and consistently growing free cash flow.

Even better is that there’s more to ICE than its dividend.

ICE’s Fast-Growing Business

Sustainably M&A-fueled growth

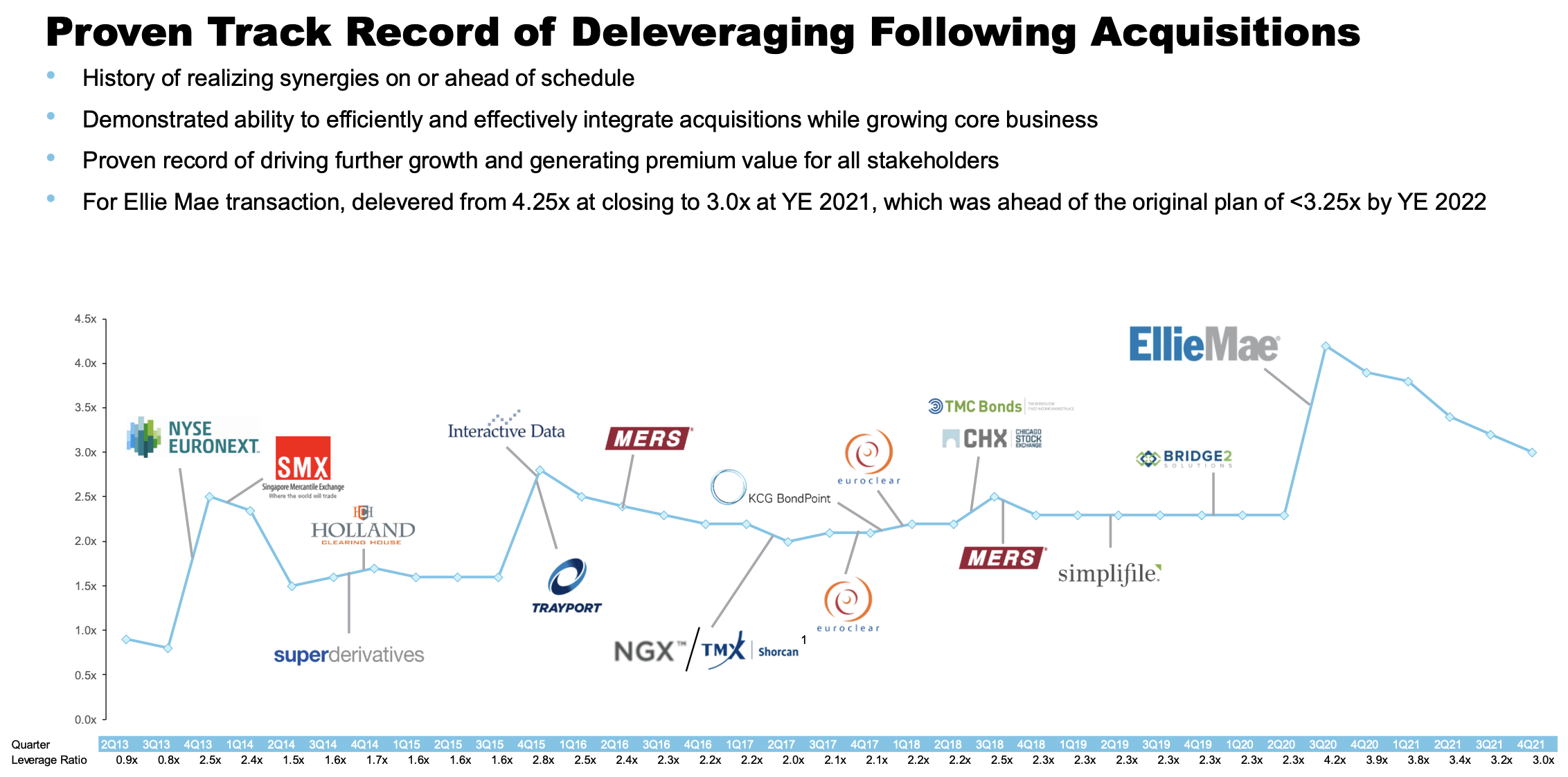

Intercontinental Exchange is an aggressive growth company. It uses M&A deals to grow its capabilities and create synergies. Moreover, when I say that M&A is sustainable, I don’t mean that it’s environmentally friendly or anything (maybe it is, I don’t know), but that free cash flow supports a quick debt reduction.

The most aggressive M&A stock I own is Danaher (DHR). It generates high free cash flow, which has resulted in a healthy balance sheet. When it buys a new company, it quickly creates synergies, which boosts free cash flow even more. Hence, it reduces debt again. It then buys another company, which creates new synergies. I’m painting with a very broad brush here, but I think you get the idea.

The graph below perfectly shows that the company has always maintained a healthy balance sheet, despite engaging in some major deals. The biggest one, EllieMae, boosted the net debt ratio to more than 4.0x EBITDA. However, in the quarters after the deal, that number was rapidly reduced to less than 3.0x.

Intercontinental Exchange

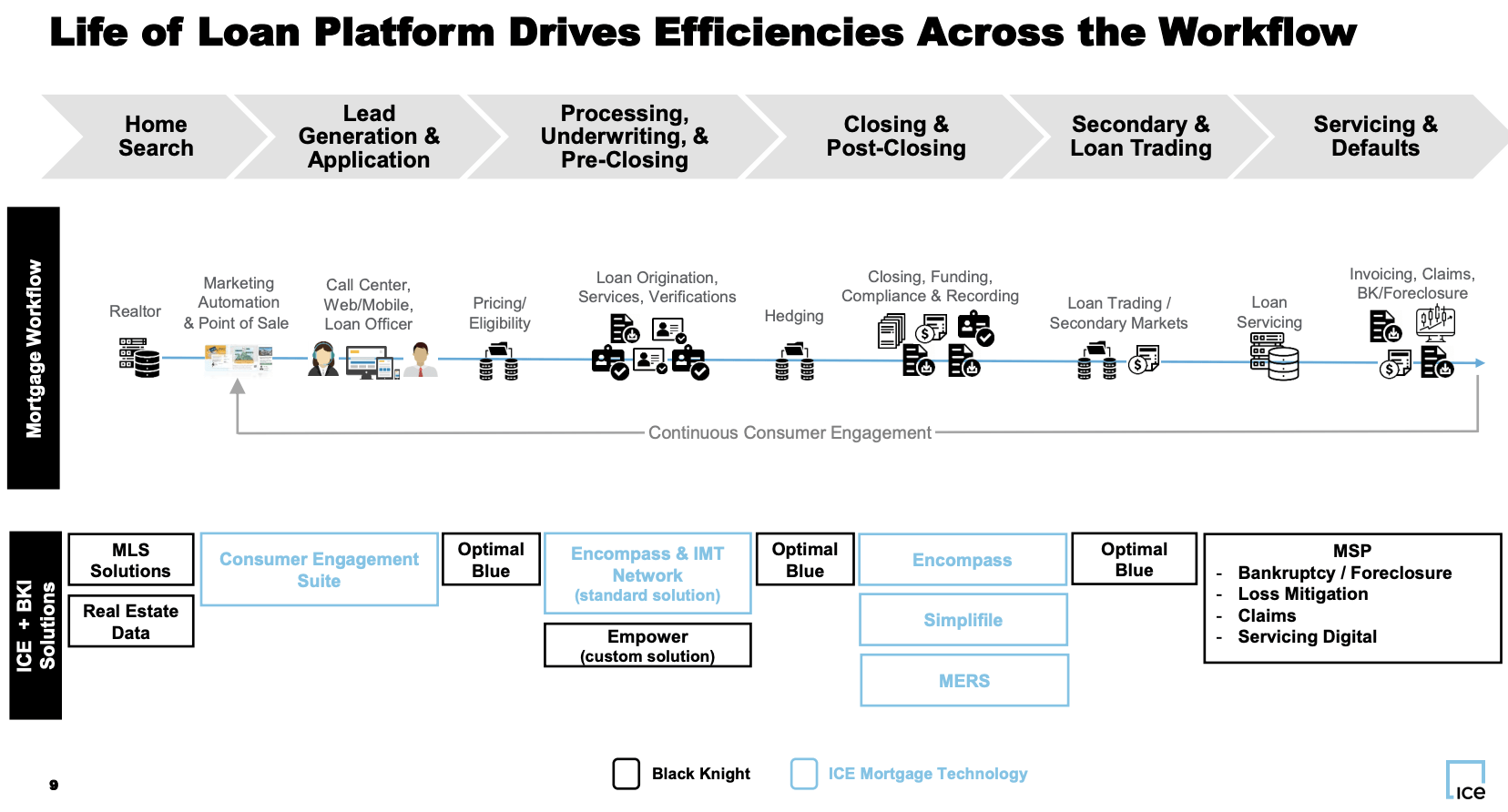

Its most recent acquisition target is Black Night, which is a major operator in the mortgage technology sector. The company would complement ICE’s existing capabilities, giving it a footprint in the entire life of a loan, from searching for loans to servicing existing loans. The overview below clearly shows these capabilities.

Intercontinental Exchange

While I believe that the $16 billion enterprise value deal will close eventually, the market doesn’t seem so sure, as fellow Seeking Alpha contributor Bram de Haas explains in a recent article (aimed to benefit from merger arbitrage).

If the deal closes, Black Knight shareholders would receive $68 per share in cash and 0.144x ICE shares. At ICE’s current share price of $102.57, that means another $14.77. If you add it up, you get to $82.77. Possibly, some of the share value can be received in cash (it gets prorated). Meanwhile, BKI currently trades at $59.93. If the deal were to close as planned, that means 38.11% upside from here.

I like this merger situation because: 1) it has received a lot of regulatory attention and the market is doubting it will close; 2) the downside may not be as pronounced as is typically the case IF it doesn’t close, and 3) there’s a lot of upside if it does close.

That said, the existing mortgage segment suffered in 4Q22 and on a full-year basis. Mortgage revenues were down 28% in 4Q22 and down 20% on a full-year basis. This was driven by the weak housing market, which lowered mortgage demand by 60%.

Nonetheless, the company remains optimistic that it can grow, as it benefits from secular demand growth, thanks to its advanced portfolio of products and solutions.

- The company believes that the trend of increased workflow efficiency through electronification in the mortgage business will persist.

- The recurring revenues in the mortgage business increased by 16% in 2022, reflecting the company’s success in capturing this trend.

- The strength of the recurring revenues is attributed to the company’s strategy of leveraging its technology and data expertise to accelerate the analog-to-digital conversion in the mortgage market.

- The fourth quarter of 2022 was the strongest quarter of the year in terms of sales to new customers of the company’s loan origination system.

- There is increasing interest in the company’s data and analytics products, which saw a 31% increase in the quarter and a 24% increase for the full year in 2022.

- The company’s AIQ solution and analyzer tools are helping customers save thousands of dollars per loan by automating the loan manufacturing process.

- The value of the company’s offerings continues to resonate with lenders, and the company remains optimistic about the long-term opportunity to accelerate the analog-to-digital conversion in the mortgage market.

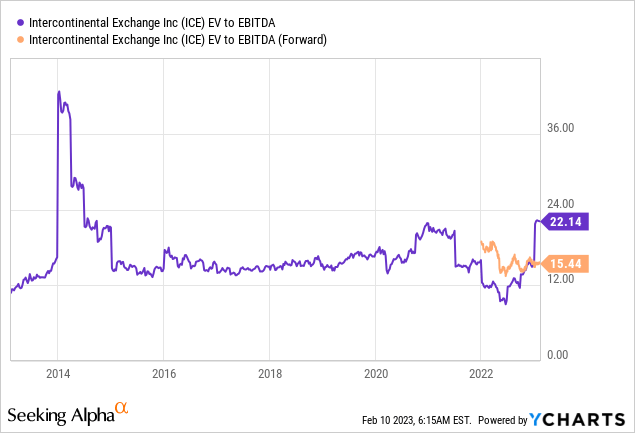

With that said, the company is expected to maintain solid EBITDA growth this year and beyond. EBITDA margins are expected to remain consistent, which is not something to take for granted in a high-inflation environment.

TIKR.com

On a side note, inflation also comes with opportunities, as it drives growth in certain areas. According to the company:

[…] in 2022, inflationary concerns and market speculation of central bank activity benefited our European and U.K. interest rate business, driving a 33% increase in revenues for the full year. These conditions also contributed to record full year revenues in our credit default swap clearing business, up 61% year-over-year, as rate volatility drove increased demand for risk management and credit protection.

Valuation-wise, ICE is trading at a very fair valuation. Using its $60.1 billion market cap, $17.6 billion in 2023E net debt, and $200 million in pension liabilities and minority interest, we get a forward multiple of 15.6x EBITDA.

Based on current projections for the next two years, I estimate a potential 20% increase in the value of the company’s shares. Additionally, I anticipate sustained, long-term outperformance of the company’s shares compared to the overall market.

That said, it is my belief that investors could potentially reap benefits from a future market correction in the coming quarters. While it is well known that I maintain a cautious outlook on the market, I anticipate that it will continue to experience volatility and oscillate within a range between 3,000 and 4,000 points. I hold the view that the market is overly optimistic, and the threat of inflation has not yet been effectively addressed. Achieving a smooth transition and bringing inflation to 2% may prove to be a challenging objective. As such, I plan to take advantage of market corrections to make strategic stock purchases.

Takeaway

The Intercontinental Exchange is a premier dividend growth stock that provides consistent and high-quality dividend growth in the financial sector. With a 5-year compounded annual dividend growth rate of 13.7%, a quarterly dividend of $0.42, and a payout ratio of just 29%, the company is an attractive investment consideration for those seeking growth in their financial exposure. ICE operates exchanges, fixed-income data and analytics, mortgage services, and other financial products and services. The company’s asset-light model allows it to consistently grow its free cash flow, which offers protection for its current dividend and potential for long-term growth. The company’s mortgage segment generated $1.1 billion in revenue in 2022 and accounted for 15% of its overall revenue. The recent (pending) acquisition of Black Knight will likely bring in even more growth opportunities for the company.

(Dis)agree? Let me know in the comments!

Be the first to comment