stockcam

Introduction

Let’s open up the debate: is Airbnb (NASDAQ:ABNB) a buy right now? Is it a pass? Or is it even a sell? I think there is no better place to discuss this topic thoroughly and in a smart way other than Seeking Alpha. So, please share in the comments what you think and let’s see if we can help each other out once again.

On my side, I am still long Airbnb. Yes, I know: it was – and to some extent it still is – an expensive stock. Yes, I know a recession is coming and people aren’t expected to travel.

However, I believe that 2023 will be a good year to pick up the stock at a better valuation to own a company whose future I believe to be bright, up to the point I think Airbnb will overtake Booking (BKNG).

In summary, I know I am taking more risk than in most other cases with this stock. In fact, I think it is the riskiest stock I own in my portfolio, with a 3% weight. As I am increasing my positions in other stocks, I am planning to keep Airbnb at 3% and I will thus buy some more shares in the following months.

I am long for the very long-term, that is for at least ten years. I am not kidding: all the stocks I buy are stocks I would like one day to leave as a legacy to my children and grandchildren. I know some will be losers and I will have to sell out of them; I also know that some may reach such an extreme valuation that it will be reasonable to sell and lock in some gains. In most cases, I think I have chosen companies whose business has strong fundamentals and strong tailwinds making it very likely for them to be around for the next decades.

Airbnb is one of the companies I picked for this reason. I think it will be around for a long time, generating billions of free cash flow for years.

Summary of previous coverage

I shared my first article on Airbnb on Seeking Alpha after reading the earnings reports of Costco and Target. I was struck by a fact: both retailers reported in the spring that they were seeing exceptionally high sales of luggage and other travel related items. Therefore, I was triggered by this news to share some research in this article (This is what Costco and Target told us about Booking and Airbnb) I had done on Airbnb and Booking, explaining why I am long the former and what I am looking at when thinking about the travel industry. The core idea was that the travel industry is still in recovery mode and that it is seeing a rather enduring spending propensity by consumers who, though feeling the bite of inflation, are still reluctant to give up traveling after the lockdowns experienced during the pandemic. In other words, freedom to travel is now perceived more as a need that can’t be postponed rather than a luxurious treat that one can afford every once in a while.

Secondly, I went back to Airbnb to show how its financials are quite solid, unlike many other “cool” companies that ipoed between 2020 and 2021 but turned out to be money losing machines. This is why I shared an article (Airbnb: When Growth, Low Debt And Profitability Walk Hand In Hand) to underline the quality of Airbnb’s financials. The company, in fact is now profitable and it has probably generated something like $2.5 billion in free cash flow in 2022 thanks to gross profit margins at 82% (yes, eighty-two percent).

My third step was to outline my investment criteria when I pick a growth-stock. In fact, most of my investments focus on compounders that also pay a dividend.

These are the criteria I use:

- The companies have to be ones I have experience with. I put this in the first place because too many a time, investors get excited about the “next Tesla” or the next disruptive healthcare company, without having the possibility to give a valuation of the product or the service the company offers.

- The companies have to have something unique about their business.

- They need to be profitable or on the verge of becoming such in no more than a year from my initial investment. When I look at profitability I consider: gross profit margin, EBITDA margin, ROCE and net income per employee. Besides profitability, the balance sheet needs to be healthy.

- They have ample room to grow either creating a new market or grabbing significant shares from the market leaders.

- The valuation metrics such as PE, EV/EBITDA and price/cash flow can be high at the moment of the investment. However, I try to project the share price 10 years ahead to get an idea of possible exit multiples.

Competitive advantage

Airbnb proved its resilience because it recovered to 2019 levels sooner than Booking and Expedia. I think Airbnb has a competitive advantage over the other two platforms because it is more than just a platform to find a house to rent for a vacation. It is in fact a community of hosts and guests where guests often become hosts after having used Airbnb for a while. In addition, Airbnb is very flexible and allows almost anyone to rent very different kinds of properties, offering the opportunity to many people to rent rooms, spaces, and houses that they would not have been otherwise able to turn into a second income source. What I think is valuable about the community is that it makes people feel more like members rather than simple consumers. This creates a certain lock-in and, in particular, it enables Airbnb to turn many guests into hosts, thus increasing its supply.

Two words on how the company is managed

Airbnb was one of the companies that actually learned its lesson early in the pandemic, understanding that being in growth mode doesn’t mean that costs don’t have to be managed. At the time of its IPO, its long-term EBITDA margin target was 30% at the ADRs. The company reached this goal quite quickly: while in 2019 it had -5% EBITDA margin, it closed 2021 with a 27% margin and I am sure that once we will see the 2022 annual report we will see EBITDA margin well above 30$%.

In addition, Airbnb’s brand value is very strong and this leads to huge savings. In fact, Airbnb states that 90% of its traffic is direct and unpaid. The consequence is clear: Airbnb doesn’t have to spend as much as other travel companies to acquire new clicks and transactions. This leads to higher efficiency and better margins.

On the other hand, there is one thing I don’t really like. While the company should generate around $2.5 billion of free cash flow, its stock-based compensation expense will be just shy of $1 billion. Though the company is keeping its headcount under control, I think stock-based compensation is something the company needs to address if it wants to be looked at as a true best-in-class one. Otherwise, it is at risk of falling into the issue Google has.

Market Outlook

Another aspect I consider is that, as far as I can find when I research, the outlook for the travel industry is still positive since it is one of the few that is still lagging behind its pre-pandemic level. As the Economist Intelligence Unit writes in its report on 2023 Tourism Outlook:

the depth of the tourism slump in 2020-21 means that strong growth is near inevitable in 2023 now that travel restrictions have been lifted in most countries. Globally, we expect pent-up demand for travel to drive growth of 30% in international tourism arrivals, taking them to 1.6 billion. This follows growth of 60% in 2022, but will still not be enough to take total arrivals to their 2019 level of 1.8 billion. However, the trajectory will differ by region.

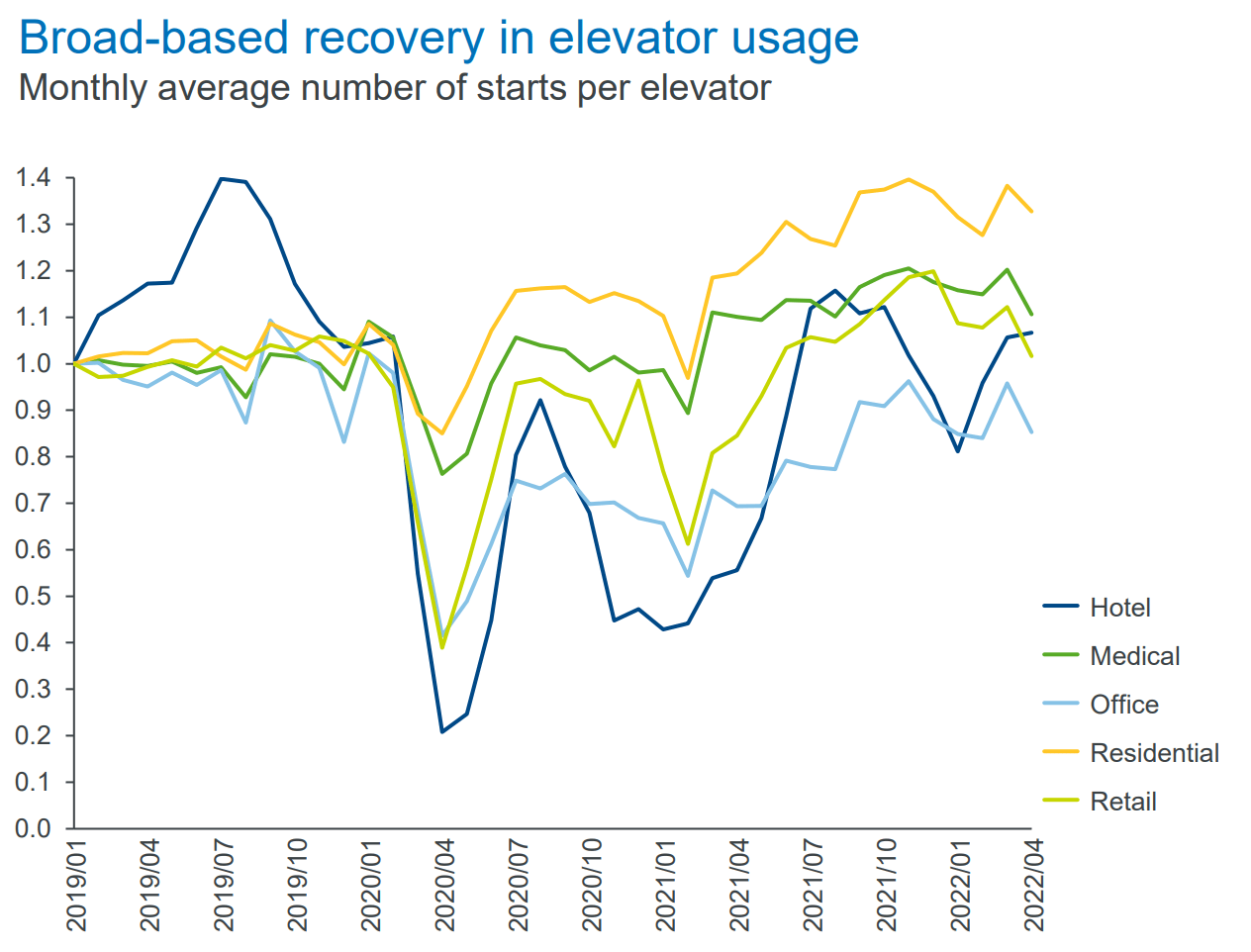

Recently, I published an article on Kone, a Finnish elevator and escalator company. While researching, I came across this graph that is useful for us to understand what we just read. It shows how elevator usage is recovering. We see that hotel and office elevators are still below their pre-pandemic levels, meaning that hotel occupancy is still not at the levels of the summer of 2019.

Kone Capital Markets Day 2022 Presentation

True, Airbnb doesn’t deal with hotels, but I think this graph sheds some light on the travel industry as a whole, confirming that there is still a gap to fill.

Opposed to these considerations, the bear thesis explains that during a recession, travel and leisure, being part of the consumer discretionary industry, takes a big hit. In addition, with interest rates rising, many tech companies are being discounted at a higher rate and are consequently sold off. Regarding the latter, I think it is understandable why companies such as Airbnb are being discounted. However, I would like to point out that Airbnb’s balance sheet is very strong, with almost $10 billion in cash and just $2.3 billion of debt, meaning that its net debt negative. This allows the company to be free from needing to take on new debt, defending it from the current high interest rate environment.

Regarding the first objection, I would like to share what Ellie Merz, Airbnb VP Finance, said during the Evercore ISI 2nd Annual Technology, Media & Telcom Conference 2022:

So, Brian would tell you that he founded the company at the height of a recession over 10 years ago when he and Joe needed to find income to pay rent. And so, when we think about that side of the equation, we would say anytime is a good time to start hosting because there’s great economic empowerment that you can derive from being a host. But when the macro conditions are bad, it’s even a better time to start hosting. And so, from that perspective, we think that there’s certainly not an upside to having poor economic conditions. But from a host perspective, it does give us incremental opportunity to really share with prospective hosts the benefits of coming to Airbnb and starting hosting.

On the consumer side, it’s a different equation. […] Just looking at the average ADRs (average daily rates) on our platform compared to comparable hotel ADRs and what we find is that, historically, there’s been a huge value gap, meaning that the value derived from an equivalent or the same size urban Airbnb listing has historically been materially higher than the average ADR when you look at a like-for-like market comparison.

And what we see today is that there still continues to be that gap, despite the fact that ADRs on our platform have risen. And so, as we think about kind of the go forward, to the extent that there’s pressure on consumer spending, we believe we continue to add or provide considerable value for the costs as compared to other accommodation providers.

What do these words mean? On one side, during a recession Airbnb is set to increase its host count, which is crucial for its business model. These hosts would be driven by the need of extra income, but usually keep on hosting even after a recession, having seen the financial benefit of this choice. On the other side, Airbnb is set to intercept some demand of consumers who still want to travel but who choose not to pay a hotel anymore in order to save a bit.

A recession should not be all fun and games for Airbnb, but I wouldn’t expect the company to be devasted by it. In addition, Airbnb just proved how the worst situation ever for its business – a pandemic – turned out to be the chance to rethink its focus and come out even stronger for the travel rebound, as Ellie Merz remarked:

The history of Airbnb over this last couple of years is that we’ve returned – several quarters ago, we returned to 2019 levels and now are seeing compounding growth. It’s important to put that distinction out there, to give you a sense of kind of where we have been in this recovery relative to the rest of the industry. If you look at our last quarter results, our nights were up 24% relative to 2019. And more importantly, the spending on our platform was about 70%. So 70% more consumer spending on Airbnb as of Q2 as compared to the pre-COVID period. And so, what that tells you a little bit about is there was the travel rebound of the century, as we call it, and we did see it play out. And where we are today, we’re seeing nice, stable compounding growth.

No one should expect Airbnb to keep on having unit economics such as these. Airbnb, too, knows that ADRs should moderate. However, while North America and EMEA are performing really well, Airbnb is still waiting to recover in the APAC region, where the market keeps on being depressed due to China’s zero-Covid policy.

Q3 Results and Expected FY2022 Results

While we wait for Airbnb’s 2022 annual report, we can look at its Q3 results and we can forecast a rough estimate of what numbers the company has achieved in 2022.

Let’s start with Q3:

- Nights and experiences booked grew 25% YoY, coming in just shy of 100 million (99.7)

- Gross booking value was supported by higher ADR and reached $15.6 billion, up 31% YoY

- Revenue increased 29% YoY and came in at $2.9 billion.

- Adj. EBITDA was $1.5 billion, up 32% YoY

- Net income was up 46% YoY at $1.2 billion, making Q3 the most profitable quarter ever for the company. This is a net income margin of 41%. This is true profitability

- Free cash flow was $960 million, the highest ever for the company and up $545 million YoY which is a 131% increase YoY.

I would like to point out how, as we move from revenue to net income, the YoY increase goes up. This proves once again that Airbnb is working a lot on its efficiency, making every dollar of revenue more valuable than before. In addition, Airbnb seems to have reached such a scale that it is now printing a lot of cash, with enormous increases compared to just one year ago.

Now, with the strong backlog the company reported, I believe Airbnb can reach $8.5 billion in revenue for 2022 with a net income that will be above $1.8 billion for the year. This should give EPS roughly around $2.8 (current estimates are at $2.57), which is quite a jump from the 2021 result of $-0.28.

The free cash flow I expect the company to reach should be around $2.8 billion. If this is true, the stock is currently trading at a free cash per share around between $4.4 and $5, depending on the number of outstanding shares at the end of the quarter. Given the current share price, we are talking of a free cash flow yield in the range between 4.4% and 5%, which is high.

All of these numbers show to me how Airbnb has coupled it focus on growth with a real commitment to profitability. This makes it stand out from the crowd of many “cool” pandemic IPOs whose profits still remain uncertain.

Valuation

If Airbnb achieves EPS of $2.8, then its current PE is 35. Assuming the company will grow its EPS just by 10% in 2023, the fwd 2023 PE is 32. If the company EPS will grow by 20% in 2023, the fwd 2023 PE is 29.

In both cases, I see no way around it. The company is still expensive compared to the general market. However, when we look at other estimates the consensus sees the company earning $11.1 a share by 2030. This lead to a fwd PE of 9.

I think this is enough to clarify one thing: Airbnb at today’s price is a stock worth owning only if an investor thinks the company will be able to grow at about 20% for the next 7-8 years. If this is the case, then 2023 can be a good year to pick up some shares as there are reasons to believe that we may still see some volatility and some weakness in the market.

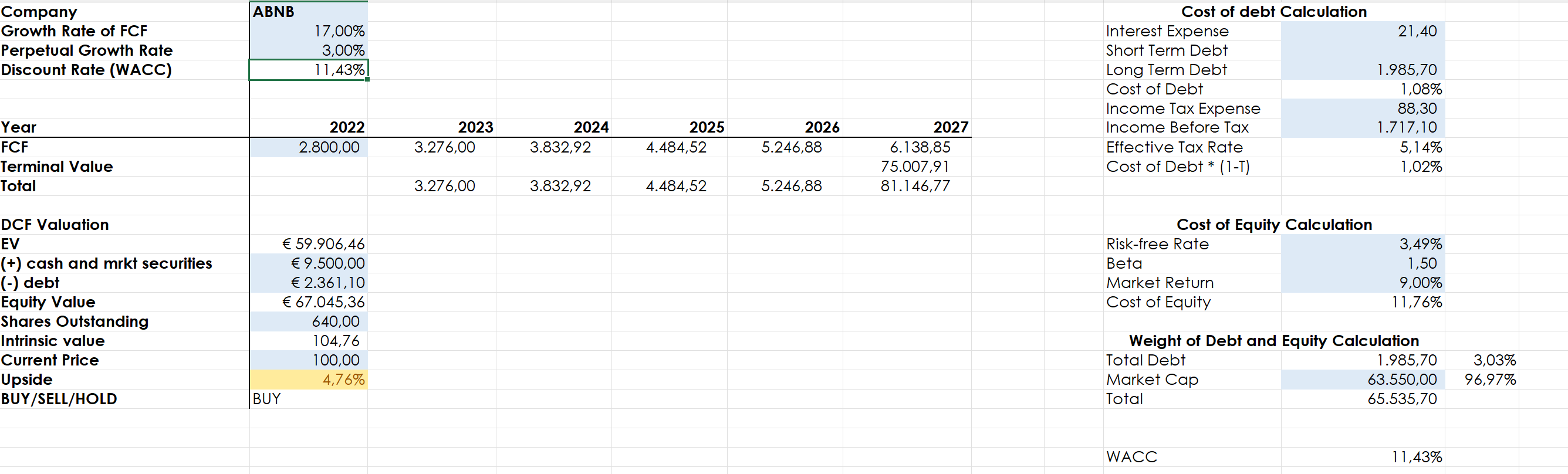

In my past articles, I shared a discounted cash flow model I used to make my forecast and my valuation of Airbnb. Some months ago, I used a FCF 5-year growth rate of 21%, combined with a cost of equity calculation where the expected market return was 8% that made me use a WACC of 9,78%. The result was a target price of $127.

Now, I have made it more conservative. I lowered the expected FCF growth rate to 17%. In the meantime, the 24 month beta is up to 1,4 and the risk-free rate of the 10 year treasury bond is up to 3.5. The consequence is that the WACC is higher: 11.43%.

This leads to a fair price of $104.

Author, with data from SA and personal forecast

Conclusion

To me, when one can buy a good company that compounds well at a fair valuation then the deal can be done. This is why I am a buyer already below $100, with the plan of holding the stock for many years to let it compound.

This is my case. Now, let’s have some fun debating this controversial stock.

Be the first to comment