jiefeng jiang

Cohu (NASDAQ:COHU) trended lower since last summer despite reporting strong first quarter results (Q1/2021). In the first quarter of 2022, the supplier of test and inspection equipment and services for the chip industry posted good results again. Since May, COHU stock is stuck in a trading range of between $25 – $30. The firm even forecasted second-quarter revenue above expectations, a debt repayment, and a strong backlog.

Markets are too wary of exposure to the semiconductor industry. Cohu is a potential exception.

Second Quarter Outlook Raised

In the second quarter, Cohu expects revenue of up to $218 million. This is above the $213.45 consensus estimate. Investors are not reacting to the higher outlook because the Y/Y growth is negative. For the next three out of the four quarters, markets expect negative growth:

Seeking Alpha

In uncertain times, investors should pay a premium for assurances. The company projected a backlog of $342 million. It will substantially raise its shipping rates in the next three quarters. This suggests that analysts will increase their revenue expectations.

In the period, the company bought back 504,100 shares, spending around $14 million. It also bought back $16 million of term loan B debt, cutting total debt to ~ $79 million.

Cohu will issue its Q2/2022 report on July 28.

First Quarter Highlights

On its earnings call, Chief Executive Officer Luis Müller highlighted the company’s strong backlog. With positive business momentum, it expects a 25% midterm non-GAAP operating income on a billion dollars in revenue. In addition, the company managed its supply chain. It will achieve a 49% non-GAAP gross margin, thanks to cost controls and progress with its manufacturing in-sourcing.

During the quarter, Cohu won a key order for the next-generation Micro-Electro-Mechanical System (or MEMS) test platform sensor. Customers need new sensor test platforms for ultrasensitive sensors. They use them in mobility and automotive applications. In addition, the firm is expanding its market by offering Industry 4.0. This is a factory automation initiative. For example, Cohu would provide automation and data analytics solutions to customers.

Although this software solution is completely different, investors seeking automation solutions stocks should look at UiPath (PATH). The firm raised its full-year non-GAAP operating income guidance. UiPath also reaffirmed its revenue forecast of between $1.085 billion to $1.042 billion.

Opportunity

Markets are underestimating Cohu’s expense management lifting gross margins. In Q1, its gross margin was 46.1%, beating its guidance. It reported expenses of $50.9 million, lower than previous guidance. Still, the company shifted items like product development and travel costs from Q1 into Q2. It more than made up for the cost shift by forecasting higher revenue this quarter.

The company has a healthy balance sheet. It ended Q1/22 with $358.6 million in cash and investments.

Cohu’s strong order backlog bodes well for revenue growth in the third quarter. As shown above, analysts already modeled a 2.98% year-over-year revenue growth. But supply chain uncertainties are easing. Semiconductor availability will improve. In the next earnings report, management may issue an upbeat full-year forecast.

Travel restrictions eased. Customer orders are on the rise. This sets up Cohu to raise its revenue forecast for the next two quarters. In addition, the company could announce more design wins. This included ultra-wideband, Wi-Fi, and RF IoT. In Q4, it announced the largest number of design wins. This should result in an increasing volume of orders.

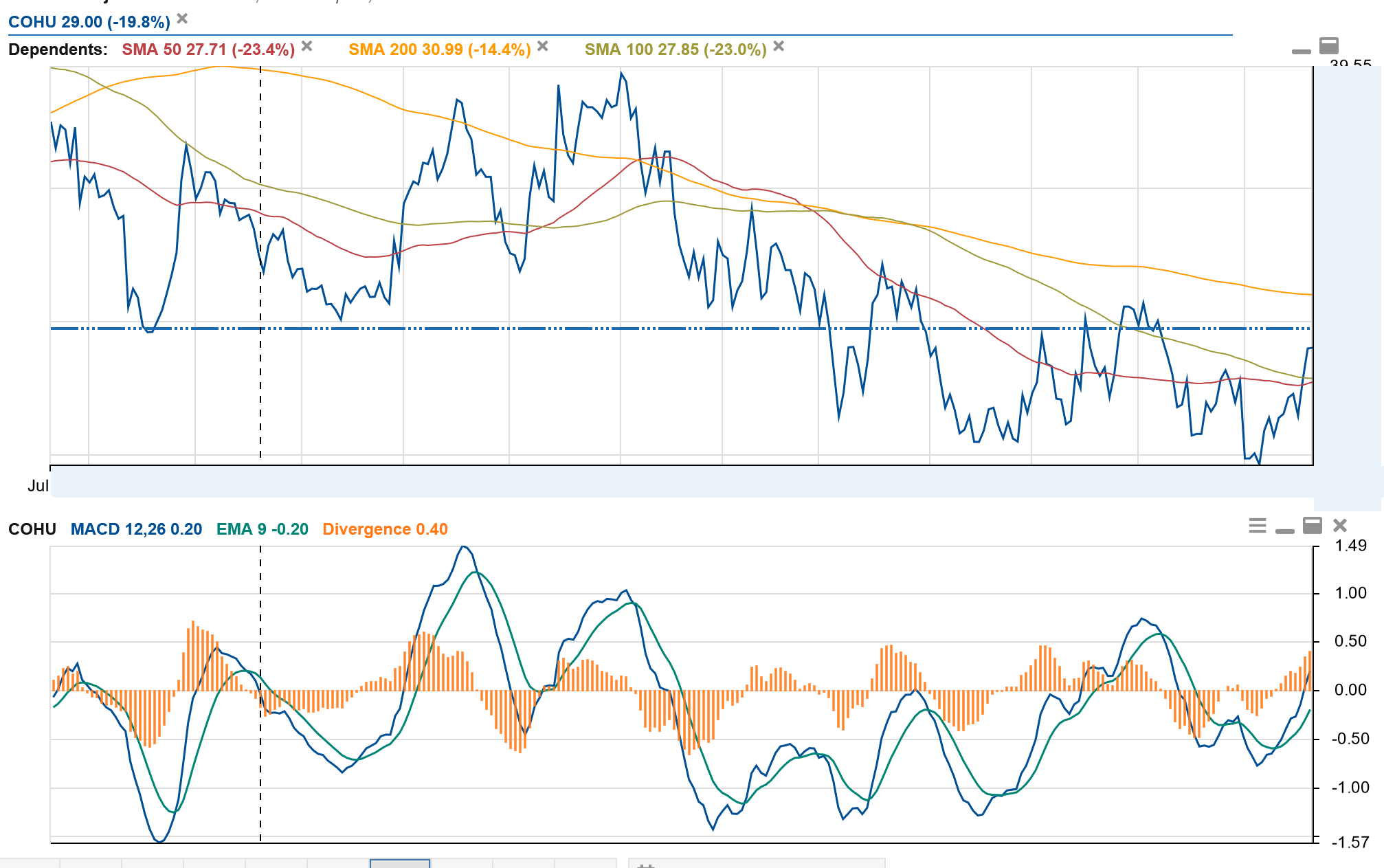

Technical Chart

MACD signals a buy (Stock Rover)

From the chart provided by Stock Rover, Cohu stock rallied above the 50-day and 100-day simple moving average. This is likely due to the Nasdaq (QQQ) rallying as investors scoop up beaten-down technology stocks. The faster-moving blue MACD line crosses over the slower-moving green line. This is a buy signal that implies a potential rally to $30.99, at the 200-day moving average.

Risks

Technology investors are hesitant in committing to chip stocks. Micron (MU) lowered its outlook. However, Micron is unable to sell more DDR5 memory when DDR4 memory is cheaper for consumers. Furthermore, Nvidia (NVDA) slashed prices for its top-end RTX 3090 Ti video card. The graphics card market is saturated.

Fortunately, the chip stocks mentioned face headwinds from lower consumer demand. Cohu supplies testing equipment that customers need.

Your Takeaway

After over a year of trading in a range, Cohu is ready to break out. The automotive and mobility markets are largely immune to the slowdown. Consumers may spend less on those goods as inflation rises. Pent-up demand for automobiles and mobile devices will offset that slowdown.

Be the first to comment