Mohammed Haneefa Nizamudeen

Investment Summary

“It is not certain whether the benefit of [omecamtiv] OM outweighs the risk”.

This is the sentence provided by the FDA’s briefing document regarding the new drug application for Cytokinetics, Inc.’s (NASDAQ:CYTK) omecamtiv mecarbil (“OM”) on December 13th, 2022. For longs of CYTK, this could potentially be a heavy blow for the company’s progress in bringing OM to market.

We have owned CYTK since late FY20′, and even back then, in the publication from November that year, had highlighted challenges with OM in its Global Approach to Lowering Adverse Cardiac Outcomes Through Improving Contractility in Heart Failure (“GALACTIC-HF”) phase 3 trial. At the time, it had missed its secondary endpoint of preventing cardiovascular death. This wasn’t a deterrent at the time, however, and we are adopting a similar approach this time round.

Taking explicitly from our last publication: “We do not feel that the GALACTIC-HF trial results eliminate Omecamtiv’s chances for FDA approval…Therefore, in the short term, the upcoming catalysts to price change in any direction are centred around this. Investors will likely look to this data for any indication in the commercial ability of the drug, drawing on what sub-populations are indicated as candidates. Should the case be made that Omecamtiv will benefit a single or multitude of sub-populations, we feel that shares will make a recovery towards [new] highs.”

Since that time, the stock has re-rated nicely to the upside, securing ~134% in unrealized return. CYTK was also fairly resilient throughout the FY22′ selloff in broad equities, another pleasant surprise. Still, the decision could put a dent in the OM story, and be a meaningful overhang looking ahead.

Despite this, the price response was fairly muted, giving us confidence the market has swiftly priced in the outcome [Exhibit 1]. Question now is, what this means for CYTK looking ahead. Management are still constructive, especially considering it negotiated with the FDA in June to extend the new drug application to February this year. Plus, there’s more to think about in CYTK’s growth engine. Net-net, we reiterate CYTK as a buy.

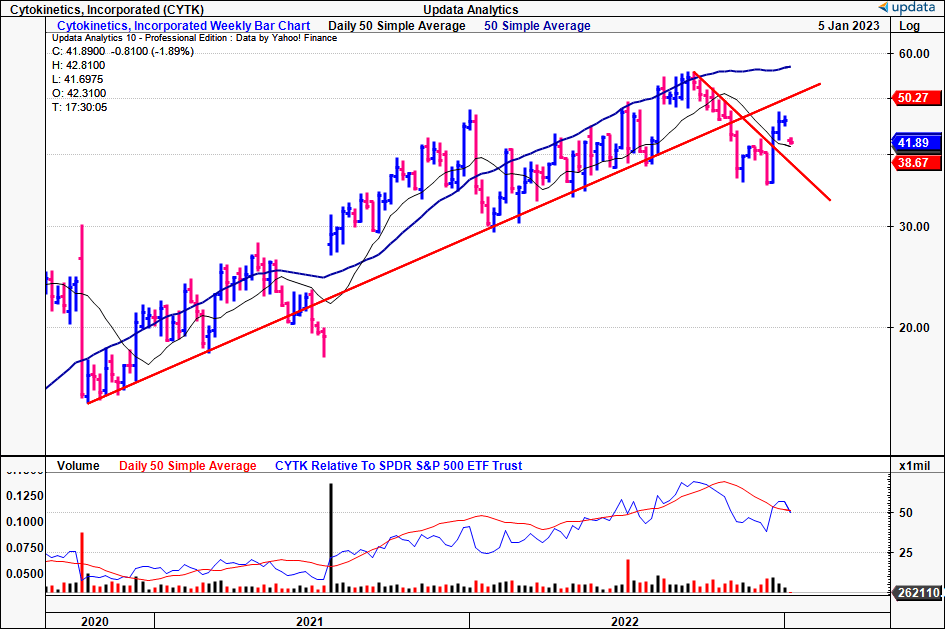

Exhibit 1. Price evolution for the CYTK share price since November FY20′. We’ve maintained an assertive position since then, resulting in a decent equity curve.

Data: Updata

Breakdown of FDA decision for OM

Here I’ll run through the moving parts of the FDA’s decision regarding OM. It should first be noted that CYTK supported its request for FDA approval of a new drug (“NDA”) for OM with data from the Phase 3 GALACTIC-HF trial, which enrolled >8,000 patients with heart failure and reduced ejection fraction (“HFrEF”). These patients were at risk of hospitalization and death despite receiving standard care. The trial demonstrated that treatment with the experimental drug significantly reduced the risk of the primary composite endpoint, comprising cardiovascular death or heart failure events, compared to a placebo, in patients receiving standard care for the condition (hazard ratio, 0.92; 95% confidence interval=0.86, 0.99; p=0.025).

However, the FDA was not convinced by the drug’s risk-benefit profile, citing concerns about both its efficacy and safety. Per the FDA, the results of the GALACTIC-HF trial showed a small treatment effect, illustrated by the 95% confidence interval approaching the null hypothesis line for the primary endpoint and reaching it for the driving endpoint.

Data from the single trial also wasn’t presented with confirmatory evidence, and the treatment effect appeared to favour those with a left ventricular ejection fraction (“LVEF”) <28%; but there was no scientific basis for this differential. The risk-benefit profile is further uncertain because only two further major cardiac ischemic events for every 100 patient-years (“PY”) are needed to negate the potential small net benefit observed in the overall GALACTIC-HF population. This is certainly one of the main factors underpinning the FDA’s voting in our opinion.

The FDA review team also estimated that ~2% of patients may have a maximum concentration (“CMAX”) above 1200 ng/mL following the initial proposed dosing regimen [scheduled, forced titration], which could also roughly translate to ~2 additional major cardiac ischemic events per 100 PY, therefore making OM unfavourable. Importantly, this estimate “does not take into account other potential risks associated with the initial proposed dosing regimen“. We now suspect that the risk estimate for the new [pharmacokinetically-guided, “PK-guided”] dosing regimen will be similar to that presented in the GALACTIC-HF trial.

Regarding the clinical risk with the PK-guided dosing strategy, the FDA noted:

There are limited data to assess the clinical risk of OM with the excessive exposure because the PK-guided dosing strategy used in the clinical trials controlled the PK exposures. A drug concentration threshold beyond which a definitive safety risk is in effect has not been established. However, there were findings from the GALACTIC-HF trial as well as from Phase 2 trials showing correlations between increased concentrations of OM with increased values of troponin-I and/or NT-proBNP in association with cardiac adverse events such as myocardial ischemia and HF. Given the cardiac toxicology profile of OM, the FDA has a concern that the proposed scheduled, forced titration could increase the potential risk of OM-associated cardiotoxicity. The Applicant [CYTK] subsequently agreed to implement a PK-guided dosing strategy that resembles a simplified version of the PK-dosing strategy that was used in GALACTIC-HF.”

As to what it means for CYTK moving forward, we suggest that it’s a waiting game until February, when the NDA application will be finalized. In the meantime, the company is actively engaging with the FDA, As mentioned, the price response has been fairly muted in lieu of the decision, however not surprising given that CYTK is >99% institutionally owned. Moreover, there’s still the CK-136 compound, currently under investigation Phase 1 study, that began dosing in December. Moreover, it has commenced its COURAGE-ALS open label extension, now with >300 enrollments to date, and continues with its FOREST-HCM trial [previously named REDWOOD-HCM OLE].

Moreover, it’s also a chance for CYTK to free up some CapEx and R&D expenditure away from OM, where it can focus on converting its clinical pipeline. We believe this is a factor to be considered heavily, and therefore the OM saga won’t necessarily be a meaningful overhang for CYTK moving forward.

Positioning for the future with CYTK

Gone are the days where we can rely on forward sales multiples in guiding price targets downstream for single equities. The cost of capital is surging to new highs and the additional macro pressures have seen equity markets reprice heavily to the downside.

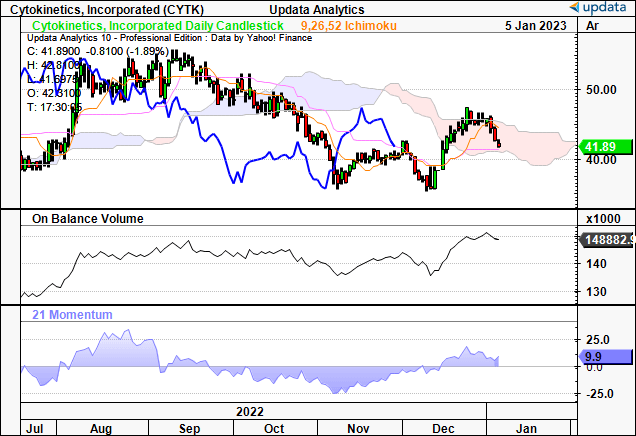

With CYTK, we feel it’s imperative to understand the market’s positioning to guide price visibility looking ahead. Looking at the chart below, you’ll see the stock has faced selling pressure entering the new year, not too long following the FDA’s decision. Despite this, on balance volume and momentum have curled up off previous lows. This divergence tells us that longer-term accumulation is still a pattern in this name.

Remember, CYTK is >99% institutionally owned, and these funds typically make allocations in small allotments, at a certain percentage of the average daily trading liquidity [in dollar terms]. Hence, they will make relatively small, but consistent allotments in order to build a position. We believe this divergence could pull through in the CYTK share price in the weeks to come.

Exhibit 2. Divergence between CYTK price distribution and on balance volume, momentum. This could be a bullish sign.

Data: Updata

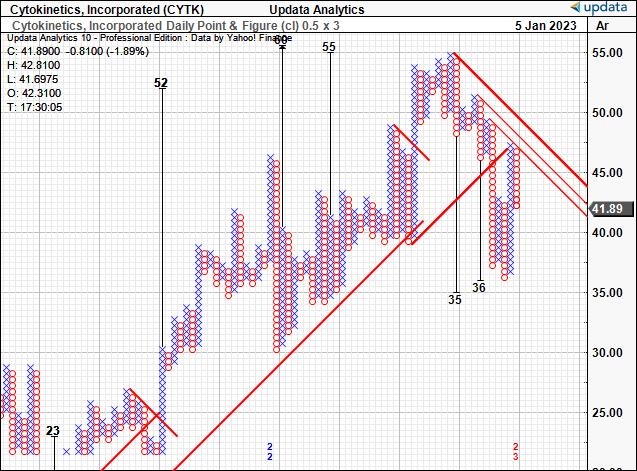

You’ll also see in the point and figure study below the presence of two downside targets to $35 and $36, given off in September and October, respectively. In November, it took out these levels, and also bottomed in December at this range following the FDA outcome.

Since then, the CYTK share price has lifted from this base, but it is yet to overcome the inner and outer resistance lines shown on the chart. We’ve yet to see new price targets form, however, price distribution on the chart is at a key junction point, calling for CYTK to rally further in order to achieve this.

Exhibit 3. Downside targets of $36 taken out in November and December. We’re now awaiting confirmation on directional price objectives.

Data: Updata

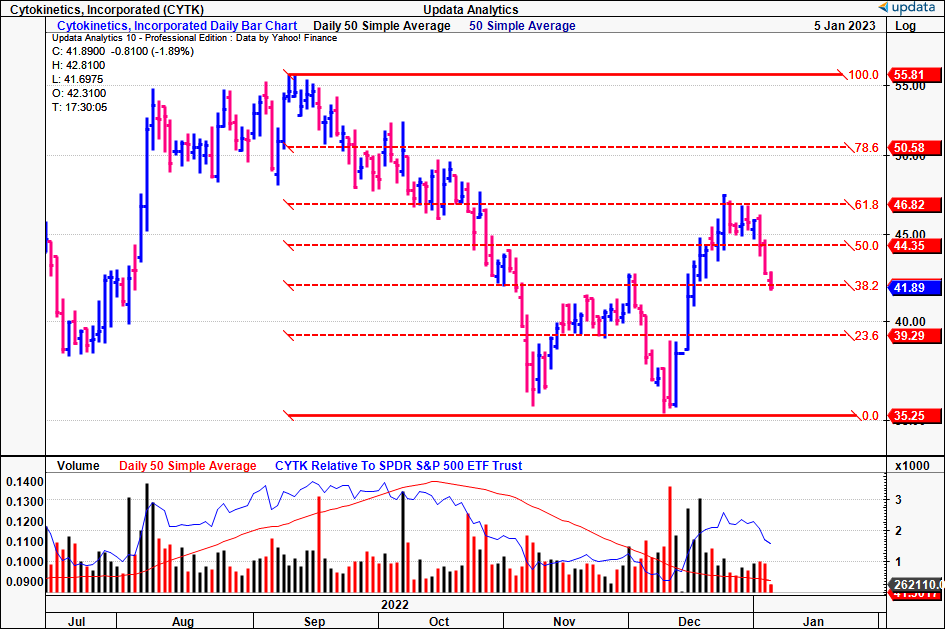

Tracing the fibs down from the September FY22′ highs, you’ll notice that CYTK already retraced ~62% of the downside move. Take note of the confirmation to each mark along the fibonacci ladder, and how each mark has acted as a key point for price change.

It tested and failed at the 62% retracement mark and is now back testing the 38% tab, and this is a key point in time for the stock by estimation. A reversal off this point is highly needed in order to see the stock catch a bid back to its previous highs. There’s really no saying in what could cause this to happen, other than its upcoming earnings print for Q4 and FY22, or a more positive outcome from the FDA in February. Taking this information in, we believe there’s scope for CYTK to re-rate to the $55 mark, and are searching for a price objective at this level.

Exhibit 4. CYTK has tested key levels on a fibonacci retracement drawn down from the September FY22′ highs to the November/December lows. Need a bounce from this current mark, and the stock can’t break below the 23% mark on the price ladder in order to remain bullish.

Data: Updata

Conclusion

The FDA’s decision regarding OM has dealt CYTK longs a heavy blow, however investors seem to have regained some confidence in pricing the misdemeanour in quite swiftly. The next few weeks are critical for the company’s growth story, but, we’d also point out that it’s not all downside for CYTK either. It can redirect capital flows to the remaining segments of its pipeline, and there’s always scope to address the FDA’s findings further down the line. The question really is what this means for its share price. We believe that, for patient investors, there’s long-term value to be made in this name. It’s withstood the post-pandemic market turbulence quite well, and we believe there could be a more positive outcome from its OM segment. Net-net, we retain a CYTK as a buy, searching for a price objective of $55.

Be the first to comment