xavierarnau/E+ via Getty Images

By Dewi John

The pattern of UK share ownership has changed significantly over the years. Until the early 1960s, UK individuals owned more than half the UK stock market. Three decades later, pension and insurance funds held the overwhelming majority.

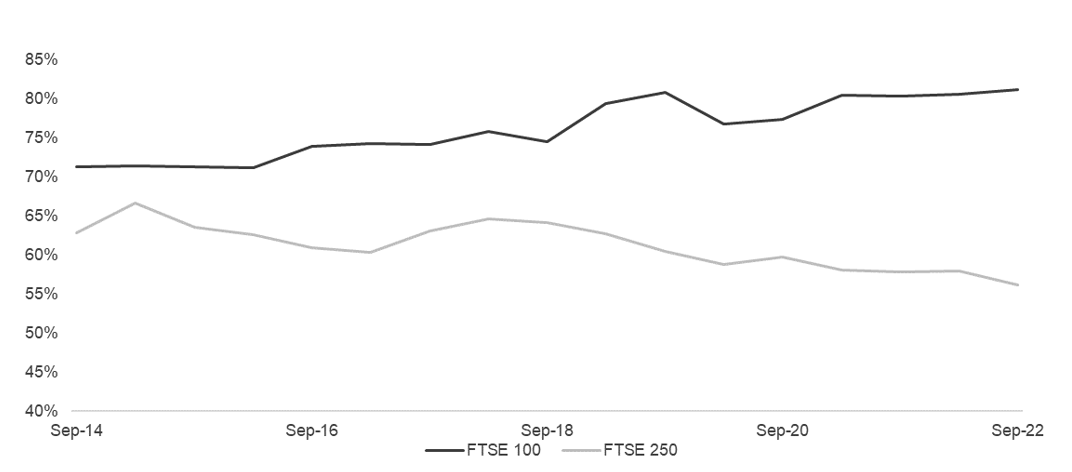

For more than a decade, foreign investors have owned most of the UK market. Given the international nature of the UK-listed large caps – 81.2% of the sales of which were ex-UK in September 2022, up from 71.2% in September 2014 – that’s not particularly surprising. (Though what is perhaps surprising is that the FTSE 250 has headed the opposite direction: from 62.8% to 56.2% global sales over the same period. And before anyone throws the ‘B’ word in, this trend was well in place before the summer of 2016). While the UK market has definite characteristics, with skews to financials, energy, and value, it’s not particularly “British” in terms of where it earns its crust.

Chart 1: Global Sales of FTSE 100 and FTSE 250 Companies, 2014-2022

Source: FTSE Russell

However, in tandem with the increased ownership of UK equities by overseas investors, UK investors have pulled back their exposure to these assets. For example, according to one report, UK pension funds have cut their equity allocations from about 73% in 1997 to 27% in 2021, with domestic equity exposure from 53% to just 6% over the same time. This is no doubt in part because of pension funds’ liability-driven investing, which has systematically lowered these funds’ equity exposure over the course of this century.

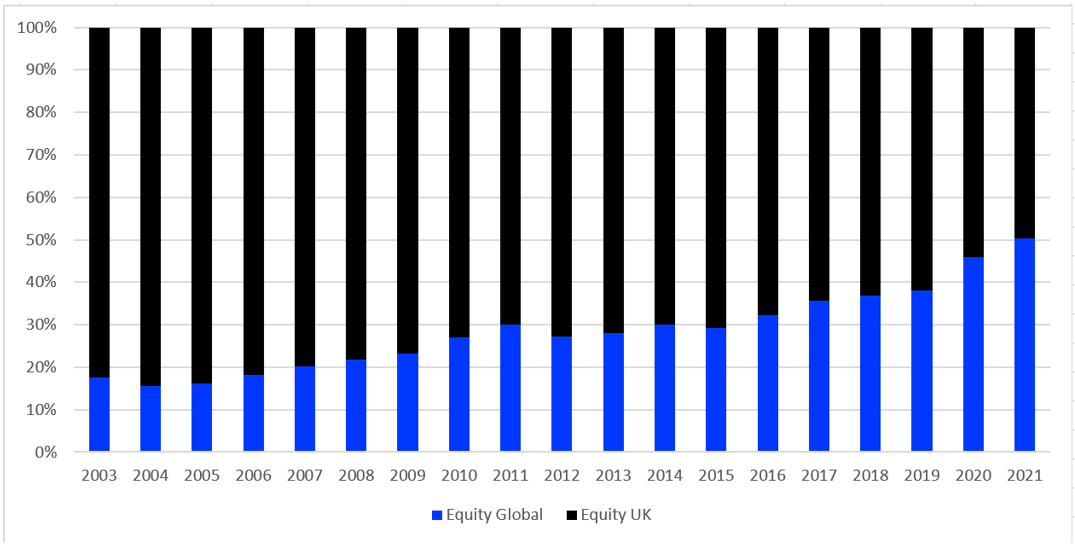

Another (quite logical) driver has been that UK investors at some point around the turn of the millennium started to listen to what their advisors had been telling them for some time: that they were systematically overweight domestic assets. As a result, we have seen global equity funds go from 17.7% of UK and global equity funds combined. By 2021, global assets were slightly more than half of the total held by UK investors.

Chart 2: Global versus UK Equity Fund Relative Net Assets Held by UK Investors, 2002-2022

Source: LSEG Lipper

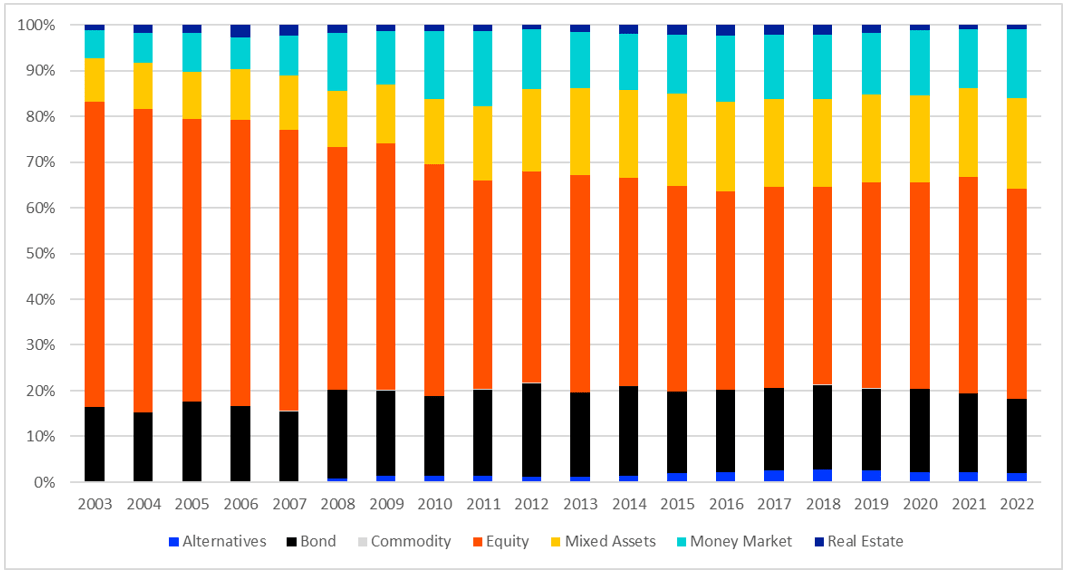

So domestic ownership of UK equities has declined over the course of this century. What’s interesting is that UK investors’ exposure to equities overall has declined over the period – going the opposite direction of the global trend.

For example, while the percentage of equities held across ETFs and mutual funds increased from 37.3% in June 2003 to 45.4% by April 2023, UK equity exposure has fallen from a whopping 66.5% to 46%. European mutual fund and ETF holders had 40.4%.

Chart 3: Relative Net Asset Allocation UK Investors, 2002-2022

Source: LSEG Lipper

Which, of course, begs the questions: are investors globally converging on a golden mean that, all things being equal, is somewhere around 40-something-percent, or is this just happenstance? Is it the growing internationalisation of capital markets that is driving this and, if so, what are the primary levers?

It does seem, then, that in shifting away from domestic equities, UK investors may be behaving rationally, excepting the LDI-driven behaviour of pension funds, where the drivers are different.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment