JHVEPhoto/iStock Editorial via Getty Images

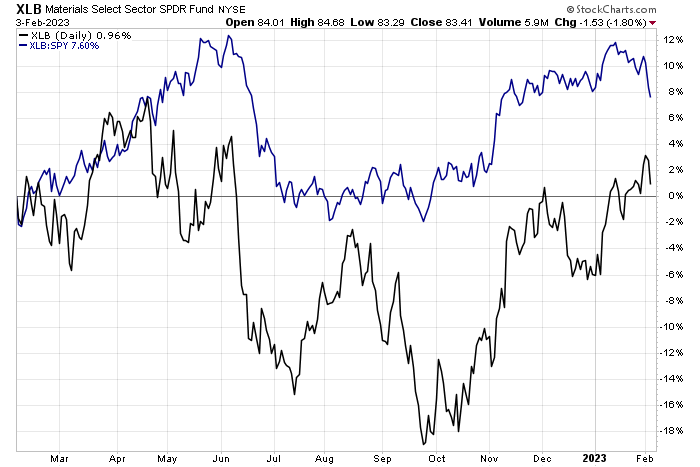

Materials sector stocks have given back some relative gains lately as the dollar has perked up to near one-month highs. The high-growth tech trade has gained steam at the same time, putting high-yield names on the back burner.

One Chemicals industry MLP has also pulled back ahead of an earnings report later this month. Are shares of Westlake Chemical (NYSE:WLKP) now a buy? Let’s check it out.

Materials Sector Falls to a Nearly 3-Month Relative Low

Stockcharts.com

According to Bank of America Global Research, Westlake Chemical Partners is a fixed-rate MLP that owns an interest in three ethylene production facilities with annual capacity of 3.7 billion lbs and a 200-mile ethylene pipeline. Westlake Partners has a long-term sales agreement with Westlake Corp to sell 95% of planned ethylene production at a fixed margin of $0.10 per lb. Westlake intends to drop down additional ownership interest in the OpCo over time.

The Texas-based $835 million market cap Chemicals industry company within the Materials sector trades at a low 10.9 trailing 12-month GAAP price-to-earnings ratio and pays a high 8.0% dividend yield, according to The Wall Street Journal.

Back in November, Westlake missed earnings estimates but beat on the top line. Rising interest rates are a key risk for the firm, but lower commodity prices could help the MLP. A pullback in rates and NG prices could be beneficial for the firm going forward, but another potential headwind is if there’s a reduced drop down of assets from WLK to WLKP per BofA.

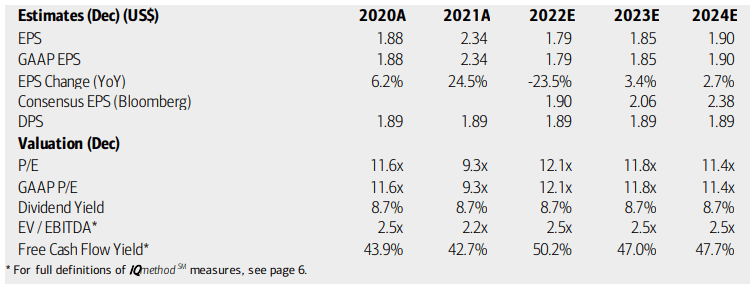

On valuation, analysts at BofA show that earnings are expected to have dropped hard in 2022 amid a rising interest rate environment. Per-share profits on Westlake are seen as recovering just modestly this year and next. The Bloomberg consensus EPS outlook is more sanguine than BofA’s downbeat forecast.

Dividends, meanwhile, are expected to remain at $1.89. Both WLKP’s operating and GAAP P/Es are rather low here given the tepid growth expectation, in the low teens, while its yield should remain high. With strong free cash flow, the dividend should be ok. Overall, the valuation is low but the growth outlook is also weak, so I’m a hold here.

Westlake Chemical Partners: Earnings, Valuation, Dividend Forecasts

BofA Global Research

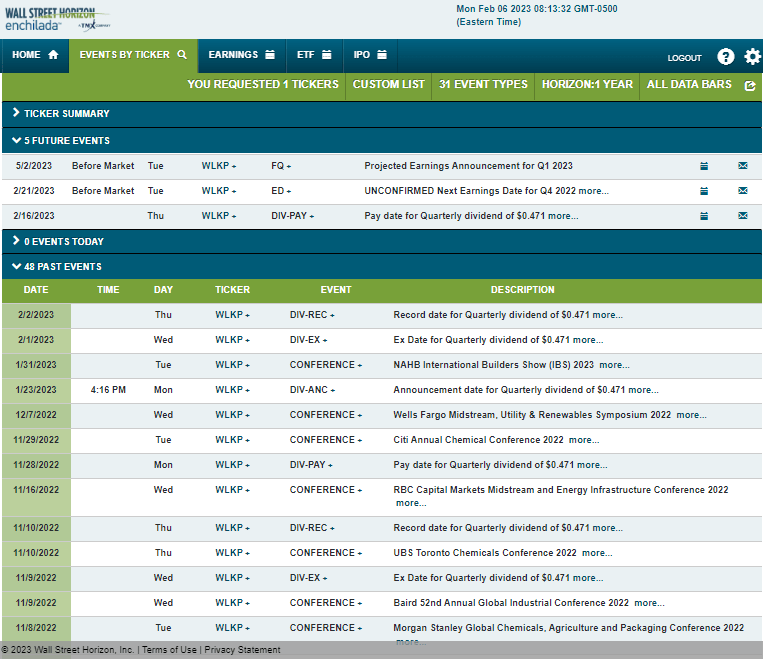

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q4 2022 earnings date of Tuesday, February 21, before the open, with a dividend pay date on the 16th. The calendar is light on volatility catalysts aside from the earnings date.

Corporate Event Risk Calendar

Wall Street Horizon

The Options Angle

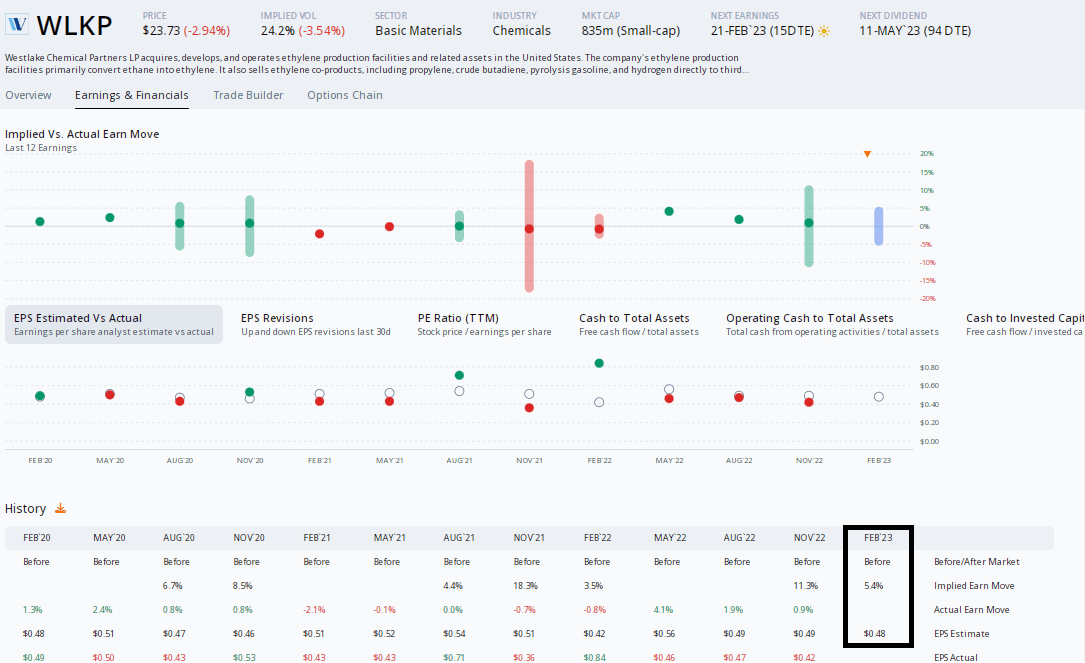

Digging into the upcoming earnings report, data from Option Research & Technology Services (ORATS) show a consensus EPS forecast of $0.48 which would be a sharp 43% decline from $0.84 of per-share profits earned in the same quarter a year ago. Westlake has a poor earnings beat rate history, having topped analysts’ estimates just three times in the last 11 events. Shares have traded higher following the past three releases, though, albeit with muted returns.

The options market has priced in a 5.4% earnings-related stock price swing using the at-the-money straddle expiring soonest after the reporting date. With small prior moves and low overall implied volatility, that premium pricing could actually be on the low side, but it’s not too cheap. I would rather play the shares rather than the options here.

WLKP: A Weak EPS Beat Rate History

ORATS

The Technical Take

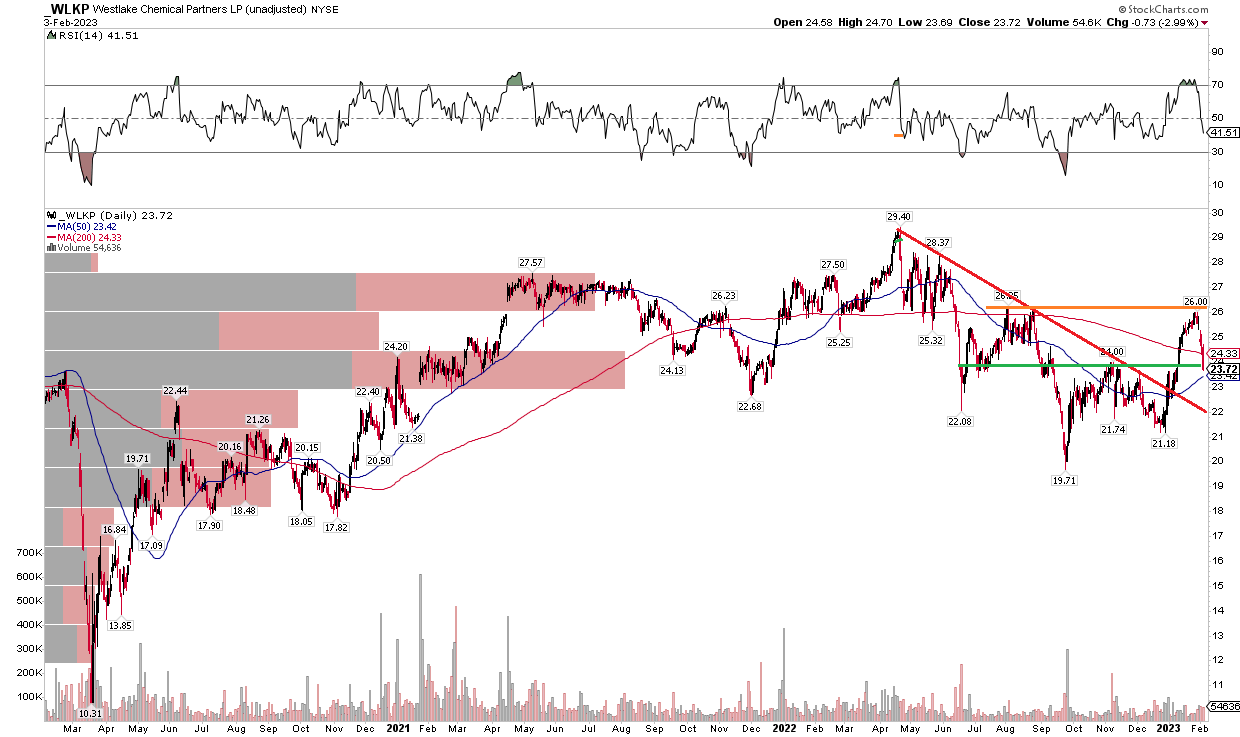

With a fair valuation and soft earnings beat rate history, how does the chart look? I see some headwinds here. Notice in the chart below that shares have found resistance around $26 after a breakout above a downtrend resistance line in January. It’s now at what could be an important point on the chart near $24. That’s where WLKP pulled back from in November. I would like to see the stock rally above $26 to help support the narrative that the $19.71 low was indeed the bottom.

WLKP: Falling Back from Resistance, Above A Downtrend Line

Stockcharts.com

The Bottom Line

I’m a hold on Westlake Chemical. The Materials-sector MLP has traded sideways for quite some time while maintaining a high yield. With a muted growth outlook but with some possible tailwinds, shares appear priced right with a low teens valuation ahead of earnings later this month.

Be the first to comment