Massimo Giachetti/iStock Editorial via Getty Images

Investment Thesis

A rational investment seeks to buy today the future cash flows a company can produce. The higher the growth rate, the more a rational investor should be willing to pay in order to participate in the improved fundamentals in future. High growth rates come with a build-in optimism into the future, and the possibility of disappointment. When companies are stagnating and/or growth is negative, the markets tend to punish this with low or extreme low multiplies. Understandably, then, how much are you willing to pay for an investment that will produce no cash in 10 years? For such an extreme situation, I would be willing to pay the discounted cash flows of those 10 years.

The Western Union Company (NYSE:WU) is a leader in global money movement and payment services, providing people and businesses with fast, reliable, and convenient ways to send money and make payments around the world. The Western Union brand is globally recognized. The Company’s services are available through a network of agent locations in more than 200 countries and territories and also through money transfer transactions conducted and funded through websites and mobile applications marketed under the Company’s brands and transactions initiated on websites and mobile applications hosted by the Company’s third-party white label or co-branded digital partners.

The business model of Western Union is under threat by incumbent fintech’s, crypto-payments and is at risk of being disrupted. As such, we want to rationally see if an investment is rationally justifiable under these circumstances because it seems there is a large risk premium priced. I think, and I hope you come to the same conclusion as me, that this might be a low risk investment that offers a cheap valuation at the current time.

Article Agenda

We will look at the past 10 years of financial data to analyze three key attributes of the business.

- 1) Growth (Top-Line, Bottom-Line, Cash Flow)

- 2) Debt Ratios

- 3) Valuation & Return Prospects

Through the historic performance of the business we project cash flow and earnings into 2032. By utilizing realistic multiplicators, we establish a share price for 2032. Subsequently, we calculate the internal rate of return of an investment in WU stock over the next decade.

The ideal situation would be a combination of i) earnings growth, ii) multiple expansion, iii) share count reduction. Companies that pull off these three levers have the potential to be 10 baggers in a decade. Unfortunately, WU will probably not hit point i), but there are plausible arguments to be made that point ii) and iii) can be achieved.

1) Growth

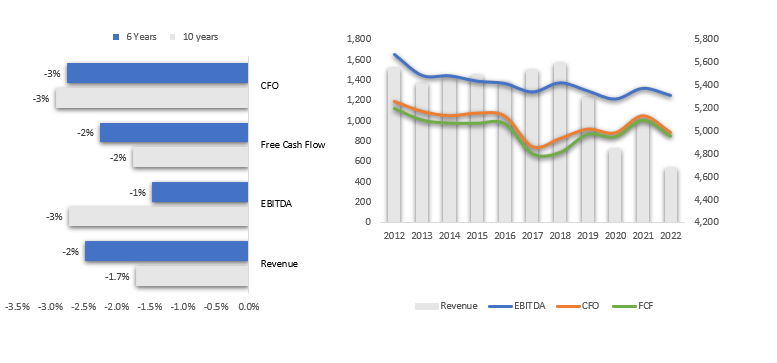

During the past 10 years, WU has been contracting its top and bottom line results. Not only revenue and EBITDA are slowing down, but also free cash flow (cash flow from operations – capex) has been growing very nicely from 1124 million in 2012 to 849 million in 2022 TTM. This is a 25% reduction in cash production in the last decade. Since Wu is buying back shares in a continuous and sizable fashion, the free cash flow per share metric has managed to increase 10% from $2 per share to $2.2 during the same time period. Often we can observe this behavior in mature businesses where cash is returned to shareholders via dividends and buybacks. Some might call this financial engineering to improve the “per share esthetics”. In the case of WU I would like to see the company continue buying back shares but, at the same time, have enough cash to invest in the company trying to interrupt the business contraction.

The chart below shows the business metrics in the past decade. Three considerations (bullet points below) can be made to add to the qualitative discussion of their performance:

SA & Author

- Accounting is doing a fine job: cash flow growth rates shadow EBITDA. This gives us confidence in the quality of the reported earnings since these get translated into hard cash on the cash flow statement.

- Growth is negative. All metrics show negative growth between -1 and -3%. Even if we zoom in and look at a shorter time period (6 years), the growth is still negative. As a sidenote, according to research, the remittance business is set to grow at 5.7% (Remittance Market Size, Share and Analysis | Forecast – 2030)

- Unfortunately, WU management has not yet been able to reduce costs at a higher pace than revenue since margins have been unchanged during the past decade. They should foster some efficiencies and implement cost-cutting measures (Devin McGranahan – President and CEO, mentioned some of the possibilities in the last conference call – so we will be looking into that in the coming 10-Q and 10-K).

2) Debt Ratios:

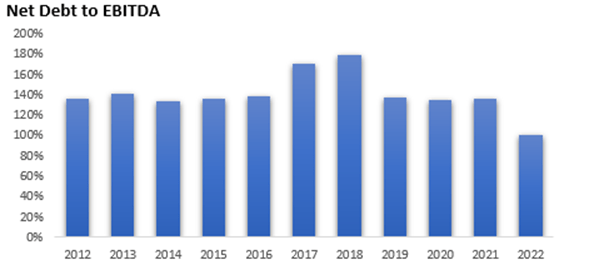

WU has been very diligent with their debt. They have maintained a balanced leverage ratio over the past 10 years and have been reducing their debt position utilizing their earnings power. Currently, their debt net of cash is $1434 Million which represents 1.1X of the current EBITDA. This is a level which can be considered very conservative and we don’t see any issue with WU servicing their debt and, if necessary, utilizing their free cash flow to reduce this further.

SA & Author

3. Valuation & Return Prospects:

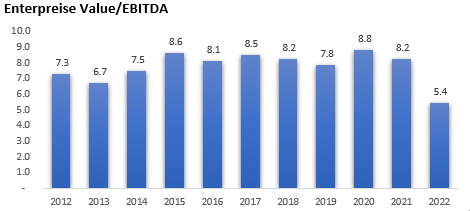

The 10-year average EV/EBITDA (chart below) is 7.7. The 2022 TTM ratio has been compressed to 5.4 at historic lows.

SA & Author

A. “The Business As Usual Scenario”:

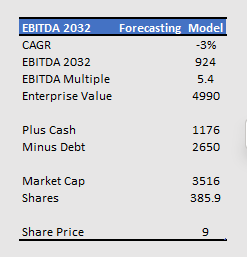

Where EBITDA and FCF compression will continue to compress at the same pace as the past 10 years (-3% per annum). Ultimately, we will attribute this business the same multiple as today, ie: 5.4 EV/EBITDA. With these inputs, the stock could be at $9 by the year 2032. Below: EBITDA Forecasting Model.

SA & Author

Potential Return:

By purchasing today’s WU at 13.77, holding it for 10 years, and then selling the stock at 9, a shareholder will make $4.77 in capital loss.

Additionally, a shareholder is entitled to the free cash flow the company is producing. These cash payments may or may not be disbursed directly via dividends. Alternatively, a company can repurchase stock or invest in M&A or other operations that would expand the business and incentivize growth.

TTM 2022 free cash flow per share is $2.2. It has been contracting by 3% CAGR in the past 10 years and we will use this rate to extrapolate the 2032 free cash flow. FCF per share will eventually be $1.62 by the year 2032.

Recap:

- Buy at $13.77

- Sell at $9 in 2032.

- Collect a total of $18.68 FCF (free cash flow), directly or indirectly, over the next decade.

- IRR (Internal Rate of Return) of 15% per annum. A $100 investment would develop into $400 in the course of 10 years.

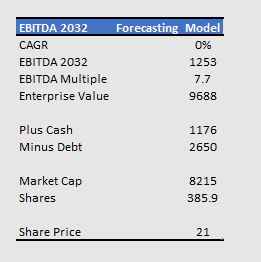

B. The “Not So Pessimistic Scenario”:

Where EBITDA compression will stop and the business stagnates. We will attribute to this business its average multiple ie: 7.7 EV/EBITDA. With these inputs, the stock could be at $21 by the year 2032. Below: EBITDA Forecasting Model.

SA & Author

Potential Return:

By purchasing today’s WU at 13.77, holding it for 10 years, and then selling the stock at 21, a shareholder will make $7.23 in capital gain.

2022 free cash flow per share is $2.2 and will be stable over the next decade.

Recap:

- Buy at $13.77

- Sell at $21 in 2032.

- Collect a total of $22 FCF (free cash flow), directly or indirectly, over the next decade.

- IRR (Internal Rate of Return) of 22% per annum. A $100 investment would develop into $757 in the course of 10 years.

Risks & Challenges

WU is experiencing a challenging environment associated with its business model. Historically, they have implemented price reductions or price increases throughout many of their global corridors. They will likely continue to implement price changes from time to time in response to competition and other factors. Price reductions generally reduce margins and adversely affect financial results in the short term and may also adversely affect financial results in the long term if transaction volumes do not increase sufficiently. Price increases may adversely affect transaction volumes, as consumers may not use our services if we fail to price them appropriately.

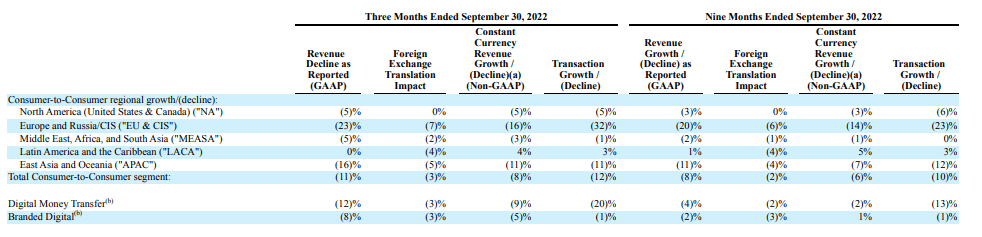

Specifically, in 2022 the suspension of operations in Russia and Belarus will negatively impact business for the year ending December 31, 2022 and likely thereafter.

From their most recent 10-Q we can observe the reduction in revenue in the various regions.

10-Q (https://seekingalpha.com/filings/pdf/16167397) (Seeking Alpha)

Conclusion

I looked into two different scenarios for this company, utilizing a rational and sober outlook for the future. Both indicate higher than market returns (10% long term S&P 500 average). Investing in companies that have already seen their highest point in the past and are now slowly decreasing their metrics can be challenging. Management could try to turn things around, and consume cash in the process (instead of distributing this to shareholders). WU has reached a point in valuation where an investment can be done. The company has low debt and is producing a lot of cash. Even in a scenario where business decreases by 3% per year, we will benefit from above average returns. This is remarkable and is only possible because it is trading near an all-time valuation low. When estimating the growth of a fast growing company, the risks of being wrong are costly and the variance of the results are very big. In this circumstance, we have a low risk investment because we don’t have to lean into the future and we know that the company is producing 16% of cash, today.

The potential that WU manages to digitalize its business successfully is an optionality that would transform a good investment into an even better one. I will monitor this in the coming years to see if revenue and earnings trends can be turned around. Should that happen, then this will be a 10-bagger investment.

Be the first to comment