Michael M. Santiago/Getty Images News

Investment thesis

On Friday, the financial results of the major banks such as JPMorgan Chase & Co. (JPM), Bank of America Corporation (BAC), and Wells Fargo & Company (NYSE:WFC) exceeded analysts’ expectations; however, investors initially seemed less excited in their reaction. All of the banks are going to face a tough and choppy 2023 with many macroeconomic challenges such as the rate of inflation and the trajectory of interest rate hikes. WFC is especially sensitive to interest rate changes as more than 56% of its revenue is derived from interest income. The management has to fight both external factors and internal challenges in 2023 and these issues can also challenge current and future WFC shareholders as well.

Q4 Earnings

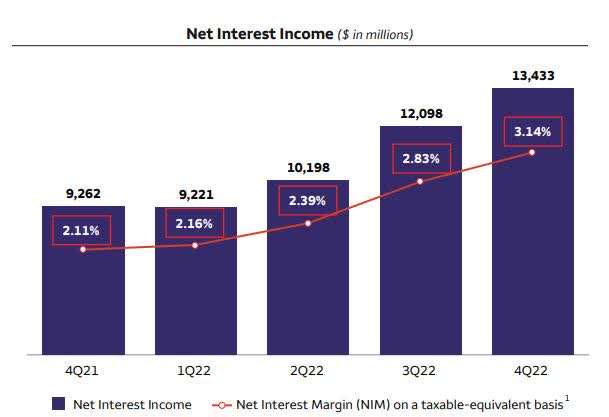

Wells Fargo reported its fourth-quarter earnings with mixed results. The company beat analysts’ estimates on NII numbers but the earning statement showed losses as previously announced. Wells Fargo reported a $13.4 billion NII, which marks a 45% surge year-on-year and an 11% increase quarter-on-quarter. This notable increase is primarily attributed to the rise in interest rates, increased loan balances, and decreased mortgage-backed securities premium amortization. Capital levels remained robust, and the company’s Common Equity Tier 1 ratio rose to 10.6% from 10.3% compared to the previous quarter. The home lending division saw a 57% drop in revenue compared to the previous year, mainly due to fewer mortgage originations, lower gains on sales, and decreased income from securitizing loans acquired from securitization pools. WFC anticipates that the mortgage origination market will continue to be challenging during 2023 and the profit margin from the sale of assets may stay low until any extra capacity in the industry has been reduced. The company’s efficiency initiatives assisted in keeping costs low, aside from operating losses. In addition, the cash cushion for loan losses also jumped higher than expected, a 22% increase compared to the third quarter figures because the company is preparing for some loan losses in the possible recessionary period. Non-interest income also declined by 15.9% Q-o-Q due to market volatility and recession fears.

Scandals have been coming up since 2016 but I believe they should go away soon as this is among the CEO’s top priorities because this will cause the Fed to lift the $1.95T asset cap. In his first announcement as the new CEO, he emphasized that he will guide the bank “in the midst of fundamental change”.

“While our risk and regulatory work hasn’t always followed a straight line and we have more to do, we’ve made significant progress, and we will continue to prioritize our work here.” – Charles Scharf, CEO.

Changing a company’s work culture takes years if not a whole decade but I am sure eventually the scandals will be dealt with and the asset cap will be lifted but it would be foolish of me to predict a certain date.

Longer-term projections based on Q4 Earnings

The longer-term trajectory of WFC’s interest and non-interest income is highly dependent on external market factors. Of course, there is significant power the management holds such as building a loyal client base, competing with other banks and lending institutions, and controlling the operating expenses but the trend of the revenue will be mostly based on the economic outlook. The external macroeconomic factors are far from stable at the moment and many analysts and banks expect a hectic 2023 which will affect WFC as well. JP Morgan is planning for a mild recession in late 2023 and early 2024. They expect the U.S. economy to expand at a muted 0.5-1% pace in 2023, as measured by real GDP, which incorporates their prediction for a mild recession beginning in late 2023 or early 2024. Based on the interest rate estimates for 2023 WFC investors can expect two things: The interest income will continue to grow in the first half of 2023 and at the same time non-interest income will stagnate or decline further. According to the management’s estimations, the first half of this year will have higher NII pacing than the second half. 2023 net interest income could potentially be around $49 billion approximately 10% higher than the full-year 2022 level of $45 billion.

4Q22 Financial Results 4Q22 Financial Results

On the other hand, the meaningful relationship with each client is becoming more and more important (possibly due to PR purposes as well).

“Going to continue to raise rates in which we pay our consumers because we’re thinking about this not in terms of maximizing short-term NII, but thinking about it in terms of the value of the relationship and making sure that we pay properly for that so that we’re continuing to recognize how expensive it is to get a new relationship and how profitable it can be to keep an existing relationship” – CEO of WFC.

The bank will be facing its own regulatory and PR challenges in 2023 as well as external market challenges. Loan growth for the year is estimated to be around the low-mid single digits. This speed of growth won’t be remarkable, though it will be consistent. The deposit base is expected to see some moderate declines over the next few quarters, before eventually stabilizing. The decline in the demand for deposits has been particularly evident in the wealth management industry. This has led to a surge of investment in cash alternatives, resulting in significant changes to how wealth business is conducted. Aside from the consumer sector, people have been searching for higher yields. This has caused an uptick in spending and has eventually led to a decrease in overall balances. To counter these issues, the management will be continuing to reduce the core expenses of the company so the profit margins can be maintained. Overemployment issues have already been addressed by shareholders but there has not been a layoff commitment from the management team.

The bank expects high-interest rates throughout 2023. During rising interest rates consumers may be less likely to take out loans, which can increase competition from other lenders, as well as from alternative forms of borrowing such as peer-to-peer lending platforms. The bank is trying to tackle the competition by introducing Flex Loan, a digital-only, small-dollar loan to help meet short-term cash needs (in amounts of either $250 or $500 for a flat fee of $12 or $20, respectively).

Valuation

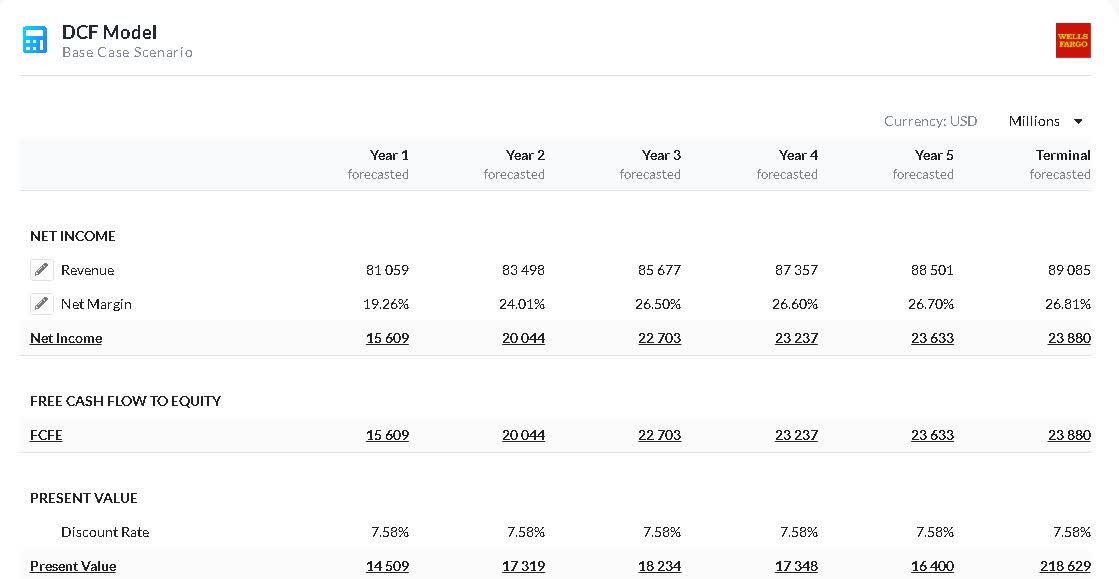

WFC is still among the most attractive valued diversified banks. Of course, the reason behind that is the internal and external challenges the bank faces and will face during 2023. The bank has the lowest P/E ratio (8.68) among its peers such as JP Morgan and Bank of America. Its efficiency ratio jumped to 82% in the fourth quarter from around 73% in the third quarter due to the total non-interest expense growing by 13% compared to the previous quarter and at the same time revenues stagnated. Based on a DCF model, the bank is undervalued looking at a 5-year term. The 12-months Wall Street average price estimate is approximately $55, a 24% difference between the current and the projected price. I am not that optimistic over the next 12 months so I would not buy WFC for the next 10-12 months for a possible 20% capital gain. Because there might be no price appreciation due to external and internal challenges but for a long-term investor the current price level could be attractive.

alphaspread.com

Final thoughts

Wells Fargo is committed to preserving its financial standing in the midst of various legal issues, external macroeconomic challenges, internal work culture, and operation challenges. In addition, they are executing several strategic initiatives, such as reducing mortgage banking operations, which may help rebuild the trust that clients and shareholders have placed in them, enhancing loan demand, a surge in interest levels and well-controlled expense amounts are encouraging. In light of the macroeconomic issues, Wells Fargo is likely to find it difficult to increase its revenues in 2023 which will have a direct impact on its share price. However, long-term buy-and-hold investors could benefit from the current discounted price of the bank.

Be the first to comment