wdstock

Wells Fargo (NYSE:WFC) continues to be constrained by an asset cap, but the large bank made a large step toward closing its issues with a settlement with the Consumer Financial Protection Bureau, or CFPB. The company still has more consent orders to resolve before the all clear will exist, but Wells Fargo has made a lot of progress since CEO Charles Scharf took over 3 years ago. My investment thesis remains bullish on the stock trading at recent lows around $40.

Big CFPB Resolution

On Dec. 20, Wells Fargo announced an agreement with the CFPB to resolve one of the largest, if not the largest, remaining consent orders. The large bank agreed to $3.7 billion for the widespread mismanagement of auto loans, mortgages, and deposit accounts.

The number sounds large, but Wells Fargo is only paying a $1.7 billion civil penalty. The other $2 billion is for remediation of customer accounts of which a large amount has already been handled according to the bank. The company took a large $2.2 billion charge in Q3’22 to presumably cover some of this additional cost.

Source: Wells Fargo Q3’22 presentation

The deal led to the CFPB terminating the Aug. 20, 2016, consent order along with providing a path to closing the April 20, 2019, consent order. Wells Fargo plans to take a $3.5 billion operating loss expense, or $2.8 billion after tax expense, during Q4’22.

The large bank already had an RPL of $3.7 billion. A large reduction in the probable losses in Q4’22 would signal the consent order fines and remediation coming to an end soon.

Jefferies analyst Ken Usdin summed up what investors should watch for with Q4’22 disclosures:

Today’s $3.7B settlement does not mean that the RPL will go to zero or anywhere close to it. We would hope that the RPL would decline somewhat after 4Q given the magnitude of today’s settlement, WFC’s incremental $3.5B of 4Q op. losses, and severity of the actions.

In total, the large bank will have taken over $5.7 billion in charges during the second half of the year while the announced costs of the CFPB agreement were $3.7 billion. Not to mention, a lot of the remediation on long outstanding issues should’ve already been completed long before this agreement at the end of 2022. Wells Fargo should’ve already remediated most of the customers impacted years ago based on when the original consent orders were signed back in 2016 and even 2020.

These numbers suggest another settlement is in the works to be announced in early 2023. Wells Fargo could be finally on the final steps of solving past legal issues allowing the company to move forward.

Too Good

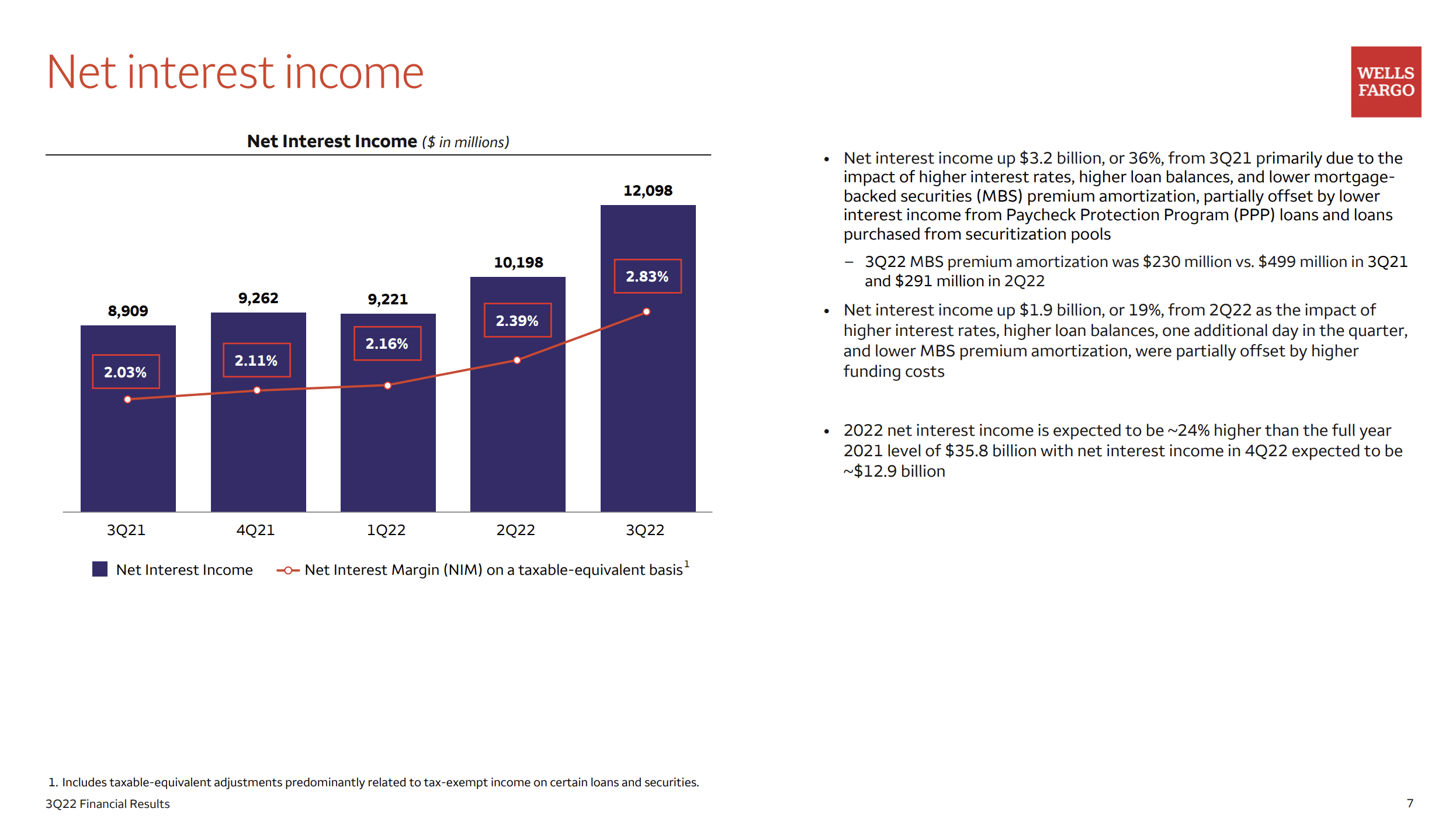

The biggest problem facing Wells Fargo is that income already has rebounded ironically thanks to the Fed rate hikes. CFPB Director Rohit Chopra complained Wells Fargo has focused too much on building new products and not enough on taking steps to fix problems. The Q3’22 net interest income probably didn’t sit well with the director after the large bank reported NII surged $3.2 billion from the prior year levels.

Source: Wells Fargo Q3’22 presentation

Wells Fargo generated an NII boost nearly double the $1.7 billion fine assessed by the CFPB. In fact, the sequential NII boost of $1.9 billion alone topped the fine.

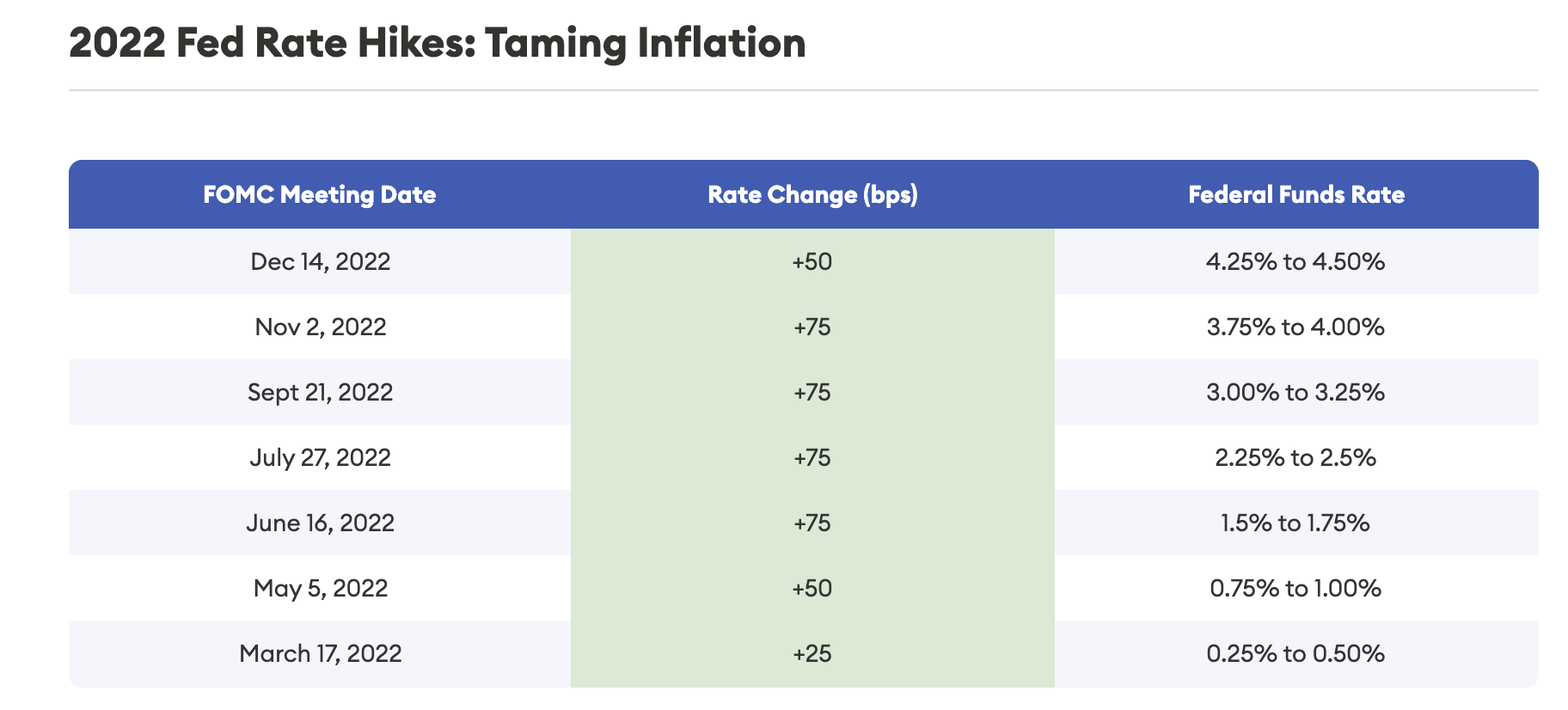

The bank even forecast another $900 million sequential NII boost to hit $12.9 billion in Q4’22. The Fed hiked rates 125 basis points during Q4 alone with another 75 basis point hike at the end of September contributing to a massive rate tailwind during the quarter and heading into 2023.

Source: Forbes

In essence, Wells Fargo is far more impacted by rate hikes than fines. In total, the bank earned $3.5 billion in Q3 and $5.4 billion on an adjusted basis when excluding the $0.45 per share in operating losses.

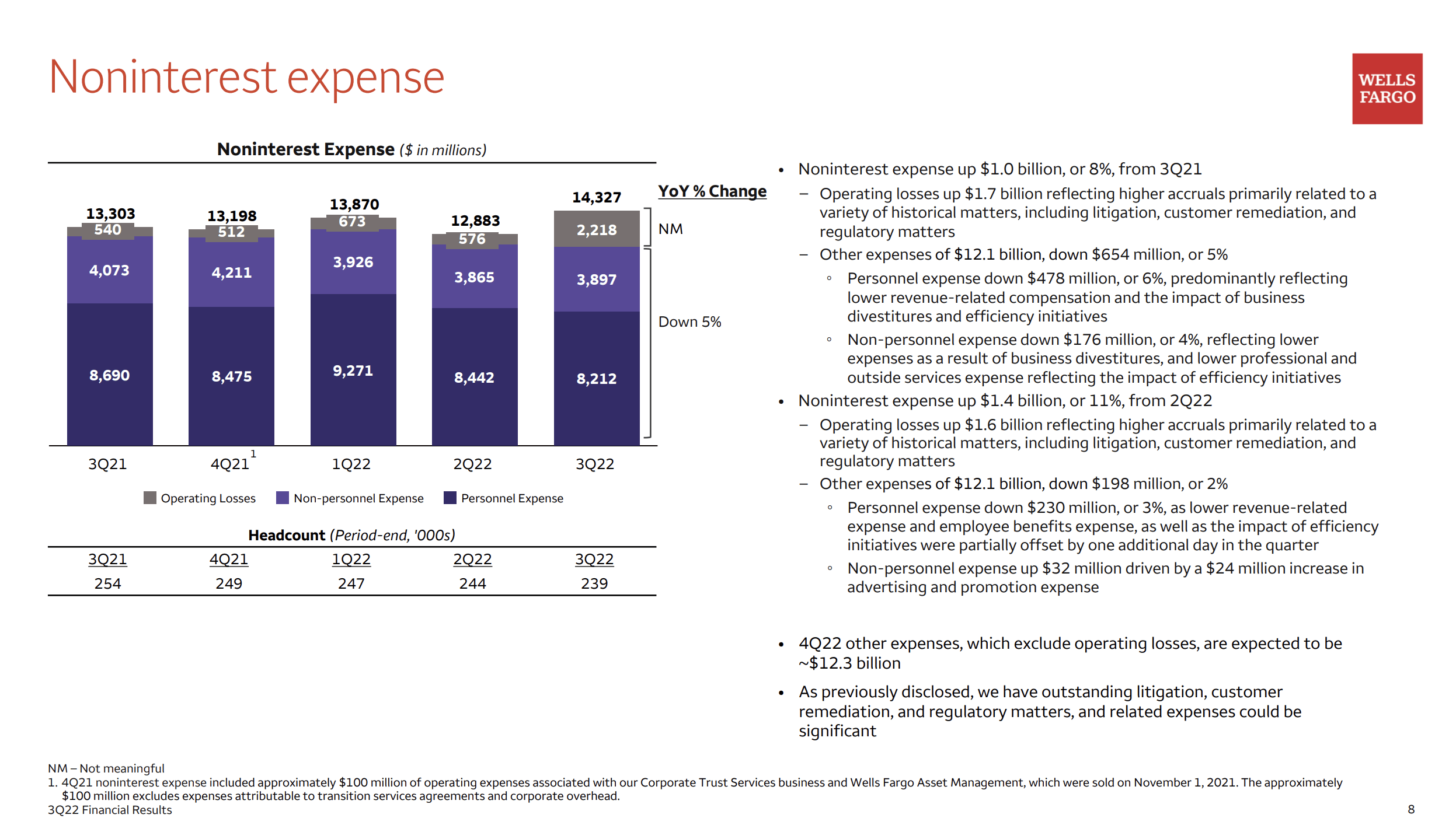

The other important story is that Wells Fargo reported Q4 adjusted noninterest expense of $12.1 billion. The large bank ended last year with quarterly expenses at $12.8 billion and guided to ~$50.0 billion for the year when excluding targeted operating losses of only $1.3 billion that have been widely eclipsed already.

CEO Scharff has long promoted stripping out $10 billion in noninterest expenses and such a goal would push Wells Fargo to ~$43 billion in annual expenses after spending $53 billion back in 2019. The bank has made some progress in stripping out costs, but Wells Fargo has set goals that would require the removal of another $5 billion in expenses from the Q3 run rate of just above $48 billion.

Under the best scenario, the large bank might just capture NII upside while costs hold steady. My 2023 projections from the end of 2021 highlighted a scenario of Wells Fargo producing $27 billion in profits due to higher revenue, not so much lower expenses. Under such a scenario with 3.8 billion shares outstanding, the large bank would produce a $7 EPS in 2023 while analysts are just above $5.

Takeaway

The key investor takeaway is that Wells Fargo is far too cheap here. The large bank has huge earnings potential with surging NII and the company took a big step toward ending the regulatory environment holding back growth.

Investors should continue building positions in Wells Fargo with the stock only at $40 despite the environment getting better for the bank whether or not the US goes into a recession.

Be the first to comment