Mike Coppola

Thesis

Warner Bros. Discovery’s (NASDAQ:WBD) Q2 results, which were released on the 4th of August, clearly disappointed. I previously reviewed the quarter already last month. But reflecting on low analyst expectations going into Q3 (expected for early November), I believe further analysis of WBD’s Q2 results might be necessary, or helpful.

In my opinion, there is no good reasoning why Q3 should be as disappointing as Q2. In fact, in context of restructuring efforts following the Warner Bros. integration, I argue management’s expensing and write-offs were excessively aggressive in Q2, leading to reported results that were unnecessarily low. As a consequence, investors may now have lowered Q3 expectations, which I think WBD is likely to beat easily.

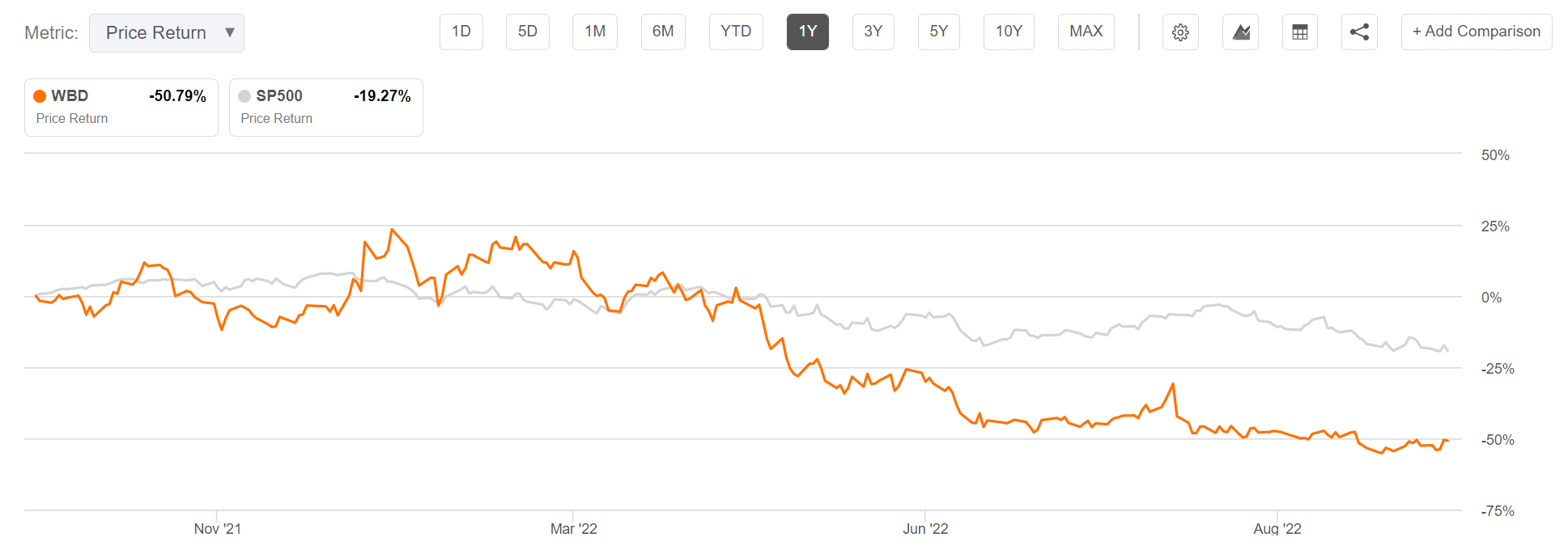

For reference, WBD stock is down about 55% since Discovery took over AT&T’s (T) Warner Bros. business.

Seeking Alpha

The Q2 Big Bath Accounting

Reflecting on a sharp stock price depreciation and a disastrous Q2 2022, an analyst could easily argue that the Discovery’s merger with Warner Bros. has been a disaster (Q2 net-loss was $3.4 billion). But Q2 data point is more complex than what numbers imply. In the June quarter, Warner Bros. Discovery arguably took what is described as a ‘Big Bath Accounting’, (or also referred to as Bloodbath Accounting): I argue management’s expensing and write-offs were excessively aggressive in Q2, leading to reported results that were unnecessarily low. Such a ‘technique’ seems very popular for company management teams after a big merger.

That said, during the period from April to the end of June, Warner Bros. Discovery management broke a lot of bad news to investors. Here are a few considerations:

Management priced $2.0 billion of write down of intangibles, a $1.0 billion of restructuring expenses, and a further $983 million of transaction and integration expenses.

For perspective how tough management acted towards its financials, consider the Batgirl movie, which caused the company to incur sunk cost of about $70 million. As a manager that prouds himself to be cost-focused, and fighting the irrationality of the DTC streaming economics, how likely is Zslatav to cut an almost finished $70 million dollar film? Not very likely, in my opinion. But the $70 million writedown comes very opportune for the big bath accounting.

In addition, WBD lowered investors expectations regarding the DTC streaming business. The company undertook a material downward revision of the company’s subscriber count by about 10 million.

Analysts’ Q3 Expectations

Reflecting on Q3 estimates, I feel that analysts have not correctly priced the ‘bloodbath accounting in Q2’ – they arguably do not think that WBD management has front loaded all the bad news.

According to data compiled by Seeking Alpha, as of October 20th, 17 analysts have submitted their estimates for WBD’s Q3 results. Total sales are expected to be between $9.9 billion and $11.38 billion, with the average estimate being $10.41 billion. So, the dispersion is actually very wide – highlighting disagreement amongst the professional analysts. But, if an investor would assume the average as the anchor, WBD’s Q3 sales are estimated to contract by about 3.7% as compared to the June quarter. I think this is unreasonably pessimistic.

EPS estimates are between negative $0.51 and positive $0.49. The average is $-0.02. Again, I think the consensus is excessively pessimistic. If WBD management really threw everything into the bloodbath in Q2 (so, conditional upon my thesis being correct), then I struggle to see how the business can bridge an estimated $3.2 billion of gross profit into negative territory.

Reflecting on analysts’ expectations for WBD’s September quarter, I argue it is reasonable to assume that WBD may beat analyst consensus forecasts. And accordingly, there might be a nice surprise-driven price appreciation post-Q3.

Valuation

At this point, it is worth considering that WBD is trading very cheap pre-Q3 earnings. For reference, if you compare WBD’s valuation vs company peers, you note that WBD’s forward 2024 EV/EBITDA multiple is priced at an approximate -45% discount to the industry and the P/B multiple is priced at an approximate -60% discount (Source: Bloomberg Terminal, EQRV October 15th).

For reference:

- Disney (DIS) trades at an EV sales of 2.8x EV/EBITDA of 18.8x.

- Netflix (NFLX) trades at an EV/Sales of 3.6x and EV/EBITDA of 18.2x.

This compares to WBD’s estimated 2024/2025 EV/Sales of x1.4 and EV/EBITDA of x10 (Source: Bloomberg Terminal, EQRV October 15th).

As I understand that multiples might not provide an accurate valuation reference, here is what I have previously calculated for Warner Bros. Discovery’s relative multiple analysis (1), sum-of-the-parts-valuation (2) and residual earnings framework (3).

My earlier Warner Bros. Discovery article included the following valuation summary:

Warner Bros. Discovery is simply too cheap to ignore. In this article, I have highlighted three valuation models, all of which indicate more than 100% upside for WBD.

(1) The relative multiple comparison indicates a $42.9 target price.

(2) The sum-of-the-parts valuation implies $24.60 as fair.

(3) The residual earnings model calculates a $27.51 target.

Debt Remains The Major Risk

Not everything is perfect for WBD. In my opinion, the major risk factor for shareholders remains the company’s excessive debt burden. As of June 30, it had gross debt of about $53.0 billion, against cash and short term investments of only $3.9 billion. As compared to 2024/2025 estimated EBITDA, the leverage is x5 – which is clearly too much.

However, I would like to point out that as of 2022, there is little interest rate and/or refinancing risk. WBD’s Q2 results highlighted that the average duration of the firm’s outstanding debt is about 14 years, with an average cost of 4.2%.

Conclusion

In my opinion, the market is pricing too much pessimism for WBD stock. And a disastrous Q2 certainly did not help to push up the sentiment. But going into Q3, I like the negative set-up, which I believe renders WBD stock vulnerable to an upside surprise.

Given the opportunity of a sharp short-term price appreciation, paired with a potential long-term valuation upside of more than 100%, I am confident to reiterate a ‘Strong Buy’ recommendation for WBD stock.

Be the first to comment