Dimitrios Kambouris

Warner Bros. Discovery (NASDAQ:WBD) has been one of the most talked about media companies over the past year. The company’s ruthless cost-cutting measures and massive strategic shifts have caused anger and confusion among fandoms and investors alike. Despite the constant deluge of bad press, WBD is actually incredibly well-positioned in the current media landscape.

WBD is currently in the midst of a major streaming war. On one side, you have streaming and media juggernauts like Netflix (NFLX) and Disney (DIS) spending feverishly on content in an attempt to push subscriber growth numbers. On the other side, you have technology giants like Amazon (AMZN) and Apple (AAPL) with virtually unlimited sums of cash to pour into their own burgeoning streaming services.

Despite this competitive landscape, WBD has a clear path to become one of the industry’s clear leaders. The company arguably has the strongest IP lineup in the entire industry, even beating the likes of Disney on this front. With the outsized success of its recent major release, the company is also proving far more capable than its competitors at leveraging popular IP.

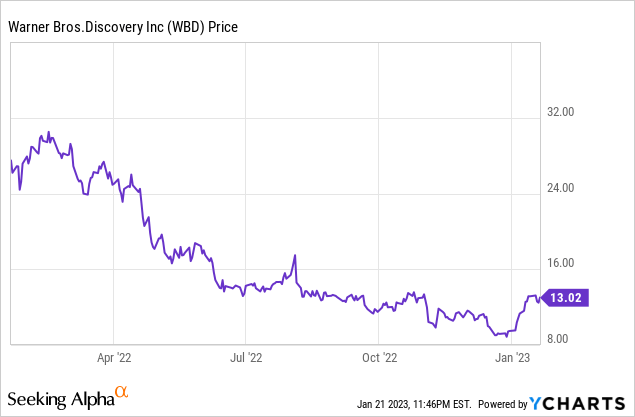

While WBD has experienced a steep decline since its spinoff, the company is well-positioned in the current media landscape.

Maximizing Franchise Potential

WBD owns some of the most popular tv/film franchises in the world, which includes franchises like Game of Thrones, Harry Potter, and DC. More importantly, however, is the fact that WBD has recently proven its ability to consistently capitalize on its IP to maximum effect. HBO, in particular, has done an incredible job adapting its highest profile IP, with the success of House of the Dragon and recent success of The Last of Us as examples.

Successfully adapting from source material is apparently far harder than it appears, evident in the countless adaptation failures experienced by other major streamers like Netflix, Amazon, and even Apple TV. HBO has proven to be the best at adaptations by far, which is especially important as its largest budget productions over the past year have been adaptations of some sort.

House of the Dragon and The Last of Us, which are some of HBO’s most expensive adaptations YTD, have both been resounding successes. In fact, House of the Dragon broke several viewership records and reached viewership levels only achieved by later Game of Thrones seasons. While The Last of Us has only just premiered, it has also premiered to incredibly high viewership numbers and rave critical and audience reviews.

The outsized success of House of the Dragon and The Last of Us, all of which occurred under the new leadership’s tenure, bodes well for WBD’s future. WBD has also made positive moves on the DC front, notably by attracting top -tier talent like James Gunn to leadership roles. While the success of DC is far from certain, WBD is making the right moves to make DC a viable competitor to Marvel.

The Last of Us was HBO’s second largest premier since 2010, only being beaten by House of the Dragon.

HBO

Quality Over Quantity

WBD’s quality over quantity approach stands in sharp contrast with the approach taken by many other streamers like Netflix. Not only is WBD focusing more on prestige title like House of the Dragon, but the company is also actively pulling its less watched and underperforming shows. This approach is already differentiating WBD’s streaming services, particularly HBO.

While it is easy to believe that WBD has been forced into such an approach due to its debt, the company is clearly not holding back on the production budgets and marketing of its top IP. In fact, WBD was rumored to have spent over $100 million on House of the Dragon marketing, making it HBO’s largest marketing campaign ever. This approach appears to be working as the company has sustained positive growth on HBO Max despite its relative dearth of new releases.

Immense Financial Strain

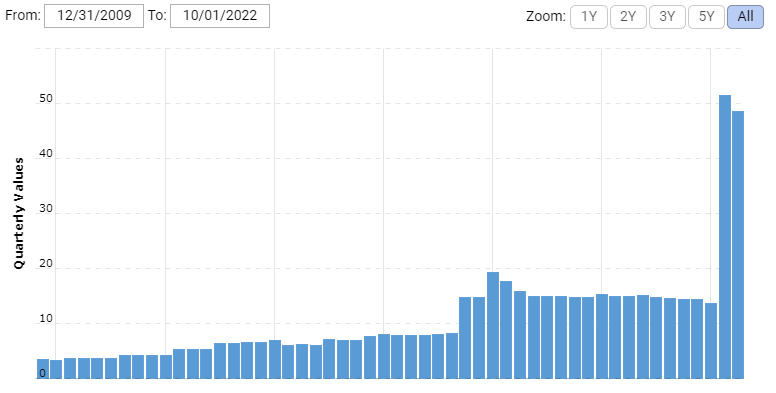

One of the biggest challenges facing WBD is its long-term debt load, which currently stands at ~$48.5 billion. As a result of this debt, WBD has had to take drastic actions to reduce costs through a dramatic restructuring process and numerous high-profile cancellations. The company’s debt load is even suspected to be negatively impacting the company’s advertising spend.

WBD also has ~20B in debt maturing over the next half-decade, which puts the company in an even more precarious situation considering current interest rate levels. If WBD is unable to generate significant revenue streams over the next few years, the company could see its valuation rapidly collapse. Fortunately for investors, WBD is proving more than capable of leveraging its vast library of IP.

The growth of streaming is also putting a financial strain on WBD’s cable and studios business, which saw revenues decline 8% and 5%, respectively, to $5.2 billion and $3.1 billion in Q3. The success the company is currently witnessing in its streaming division is not yet enough to offset the losses sustained in its other businesses. However, as WBD builds out its franchises, the company should see greater revenue streams.

WBD has racked up a great deal of debt, which will be the company’s biggest challenge moving forward.

macrotrends.com

Conclusion

WBD has spent the past year cancelling movies/series, pulling old content, and restructuring in order to save ~$3 billion in costs. With that period now over, the company can fully focus on growing its streaming customer base and building out its franchises. Even in such a competitive landscape, WBD has a realistic roadmap to become one of the largest media companies.

WBD has more room to grow at its current valuation of $31 billion. Even with its considerable debt load, it seems unreasonable that WBD is worth only a fraction of Netflix and Disney. Considering WBD arguably has an even greater IP library than Disney, WBD should see major upside moving forward.

Be the first to comment