enot-poloskun

ASTS SpaceMobile (NASDAQ:NASDAQ:ASTS) is a company trying to accomplish something completely unique: the coverage of the entire world with satellite-based broadband direct to standard mobile phones. However, while the aim is undoubtedly impressive and likely beneficial for the world at large, the path there looks incredibly uncertain, involving numerous setbacks, all time firsts for satellite technology, and funding that is seemingly inexorably destined to come at the cost of ongoing share dilution. Therefore, my position on ASTS is a decidedly neutral hold for now, as in my view there are still potentially astronomical gains to be had should the company succeed both in launching the world’s first mega constellation and hang on financially, or possible upside from an acquisition.

The Technology

In November BlueWalker 3 successfully unfurled and became the biggest ever commercially developed array in space. The 693 square-foot satellite operates in Low Earth Orbit (LEO) and is designed to deliver cellular broadband directly to individual phones. Oversimplifying somewhat, it does this by using a phased array approach that leverages many small antennae to focus the signal somewhat and save power.

Although this milestone is impressive, it is still very much within the testing phase, as BW3 has yet to actually connect with mobile phones on the ground. Despite this fact, it is important to understand that BW3 is not the model that ASTS intends to form the planned 168 strong constellation, but instead a model not yet constructed named Bluebird. ASTS projects that 5 Bluebird satellites will be built in the second half of 2023, with an eye towards reaching a production rate of 6 per month sometime in 2024. Bluebird will be larger but will use a lot of the same architecture as BW3 so some risk is minimised.

ASTS August 2022 investor presentation

However, with innovative all-time firsts come uncertainties. For example, if these are the largest commercial arrays ever deployed, how much risk is there in the structural integrity and durability of the proposed constellation? I am not an expert, or indeed have any relevant expertise at all in engineering satellites, but as with anything completely novel, the risk is more opaque than usual. This is more of an illustrative point than a specific one, the point is that there are so many experimental considerations to this stock that you would be forgiven for thinking this project was developed in a minor subdivision of a much larger company than ASTS.

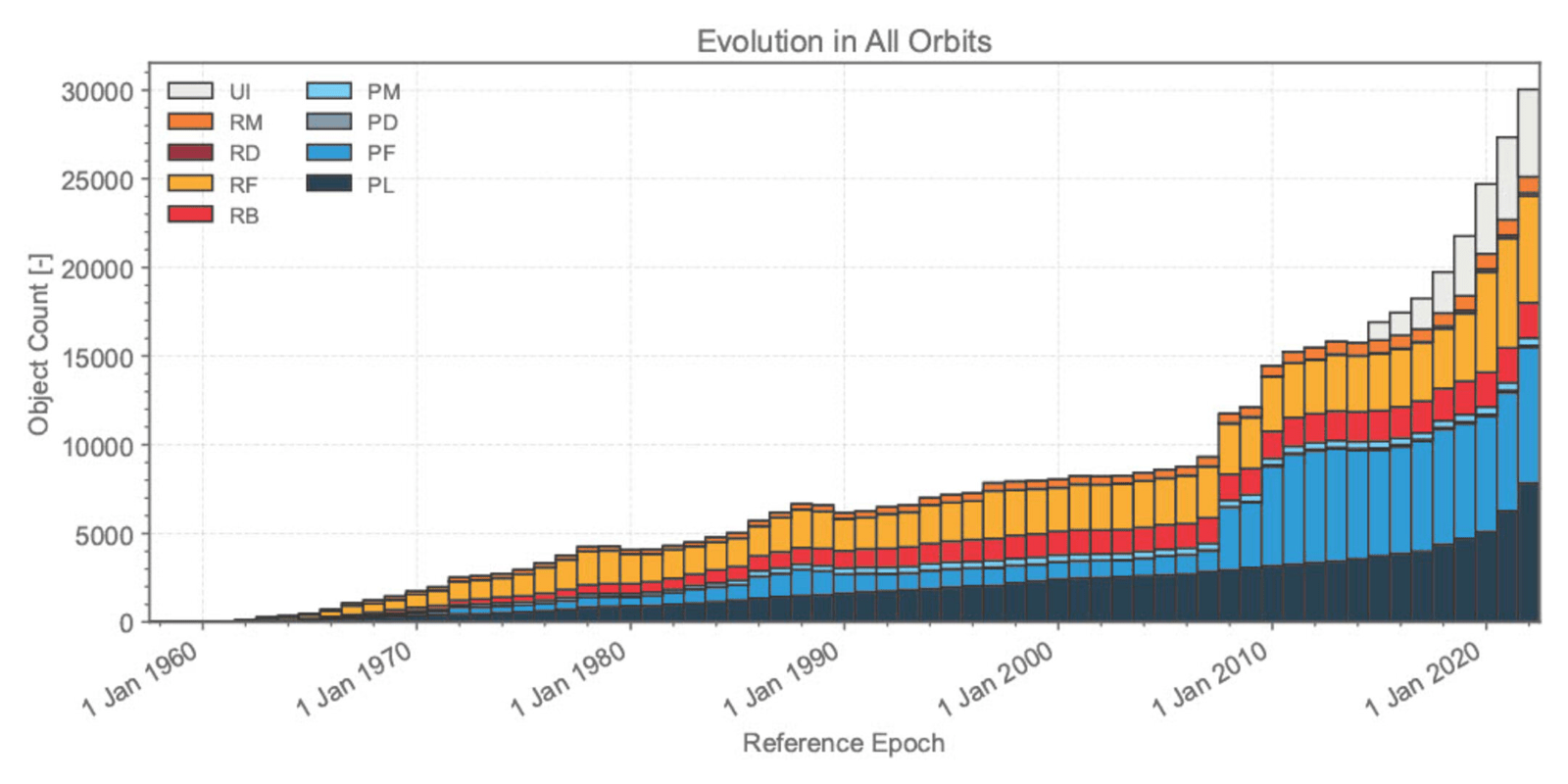

LEO is becoming more and more crowded by debris, which also represents a possible long-term risk to ASTS satellites. Presumably, this risk is greater for larger arrays which specifically is of interest in this case since ASTS are breaking records in size department. As the graph below shows, the pieces of space debris in orbit now exceed 30,000, with a marked shift in the rate of increase starting a handful of years ago.

European Space Agency

Funding And Dilution

According to Space Capital, space funding has fallen by 58% since 2021. ASTS is certainly a stark example of a 2021 SPAC now struggling to fund operations, resulting in share dilution which in my view is a key risk to potential investors.

Sean Wallace provides cost projections in the Q3 2022 earnings call:

We believe a key advantage of the Space Mobile System is its ability to be deployed in a phased manner, where we can target a modest number of satellites to provide limited coverage in specific countries. We believe this ability to phase in our coverage will provide us a first-to-market advantage and enable us to work with MNOs to introduce services and develop the market. We continue to project that our materials and launch costs for our first 20 satellites remains at between $300 million to $340 million with a midpoint per satellite cost of $16 million.

ASTS aims to eventually build a constellation of 168 satellites, so using their own projected costs, $16 million each implies roughly $2.7 billion for the whole constellation. Of course, costs could fall as production becomes more streamlined, as ASTS in earlier earnings calls projected $11 million each for the rest of the constellation. This would reduce the constellation costs to just under $2 billion. Nevertheless, this figure still dwarfs their current market cap of around $900 million, which is a worrying statistic given the company’s ongoing habit of diluting shareholder value to stay afloat. In late November, ASTS stock slid on news of a fresh stock offering of $75 million. At the time of writing, the stock sits at $5.15 around 75% down from all-time highs.

It is not all doom and gloom on the funding front, however. There is potential for funding from the FCC 5G Fund for Rural America, an up to $9 billion dollar fund which is aimed at subsidising the development of 5G for rural areas. This is complete speculation, but still a possible future catalyst that could drive the stock and solve a key issue it faces.

A Questionable TAM

ASTS bulls often cite a $1.1 trillion TAM, but it is unclear if this figure is meaningful at all. The global wireless services market is worth $1.1 trillion, but it is difficult to see how a company mostly aiming at the geographical ‘gaps’ in this market could justify defining the entire market as a realistic TAM. It is a meaningless statistic if the company struggles to penetrate the market. The figure of 5.3 billion potential users tends to be floated along with this 1.1 trillion claim, but obviously includes many urban broadband users. For this group, the use case seems questionable-are people really going to pay ASTS just to extend their coverage to a marginally greater area? It would appear the rural market is the one with the clearest use case, however presumably a large percentage will be in lower income countries. This may be an untapped market for a reason. The overall population of potential users could very well be huge, but if many of them reside in poorer regions, then monetising this service could prove a fruitless endeavour. In this sense, the $1.1 trillion TAM begins to break down under the microscope, it is likely the realistic figure is some fraction of it.

ASTS August 2022 investor presentation

Reasons To Be Bullish Anyway

Although this article thus far is quite skeptical, I can see reasonable cases to be made for the stock. The price is somewhat beaten down at time of writing, despite the successful (and historic) unfurling of BW3 which in my view eliminates some technical risk in the stock. ASTS also boasts a large patent portfolio of 2,400 either existing or pending patents and I think this combined with the impressive achievements of the company could make it an attractive target for acquisition. This is also bolstered by the fact that currently, there is no direct competition doing exactly what ASTS is attempting. ASTS also has a wide range of agreements with Mobile Network Operators (MNOs) that mean that gaining customers should be quite easy if the technology succeeds, because they will be able to buy plans through their existing providers.

Valuation

Calculating a robust valuation for ASTS is incredibly difficult because firstly, the company is incredibly speculative and the goal a hypothetical technological first, and secondly because of that fact, there are essentially no competitors that directly compare to ASTS in what they are trying to achieve. For that reason, I think it’s farcical to do an entire original valuation of-but worth looking at the ballpark figures for what might be possible.

ASTS initially projected first earnings to occur in 2023, with $1bn in revenue in 2024, reaching all the way up to a $9.5 bn EBITDA by 2027. This would imply an enterprise valuation around $76bn assuming an EV/EBITDA of 8. Now that the schedule has fallen behind, these projections seem unlikely for the given dates but might regardless serve as ballpark estimates for a particularly bullish case.

Conclusion

The aspiration to create a worldwide space based broadband network is admirable and the milestones passed so far are impressive. However, a grand project that would be beneficial for the world at large does not necessarily equate to a viable business or generate the funding to sustain itself. In easier market conditions, perhaps a more bullish outlook would be justified. But as things stand, this is a pre-revenue company continually resorting to equity dilution in a bear market with a product still undergoing development and testing. Even overlooking that, the TAM is seemingly quite vague and difficult to penetrate. Therefore, despite the enormous potential of the company, I won’t be opening a position in this stock yet.

Be the first to comment