Mike Coppola

Investors in Warner Bros. Discovery (NASDAQ:WBD) have had a rough go of it since Discovery merged with AT&T’s (T) Warner Media division to form the company. We admit 2022 was a very tough year to be an investor in this name and every share purchase or option trade we did seemed to blow up in our face (other than covered calls). It was a perfect storm of shifting market trends, investors’ demands shifting and the debt market being turned upside down with the U.S. Federal Reserve raising interest rates at the fastest pace in a generation.

While portfolios may currently be ‘worse for wear’ we think that better days are ahead and that many of the issues investors and analysts have raised might be answered as 2023 plays out. Based on some large cash-secured put trades being exercised on us since December and the subsequent rally in shares, we are now positive on our positions in Warner Bros. Discovery – which is somewhat of a relief on one hand but also has us paying even more attention to this name as it is a larger holding and might provide a trading opportunity on another move higher.

With that said, right now we are still holding the name, but with earnings coming up we are watching a few key items and looking for more color from management on how they are planning to move forward on the business side. Here are some items we will be interested in during next week’s quarterly results and conference call:

The Debt

The merger to create Warner Bros. Discovery was predicated on AT&T’s desire to simplify their business and offload debt. Discovery was a company with a management team that was well versed in managing higher leverage levels and the merger seemed to solve issues for both sides; AT&T was able to get rid of a bunch of debt while Discovery was able to bulk up and create a company with a large enough content library to compete effectively against Netflix (NFLX) and Disney (DIS) moving forward.

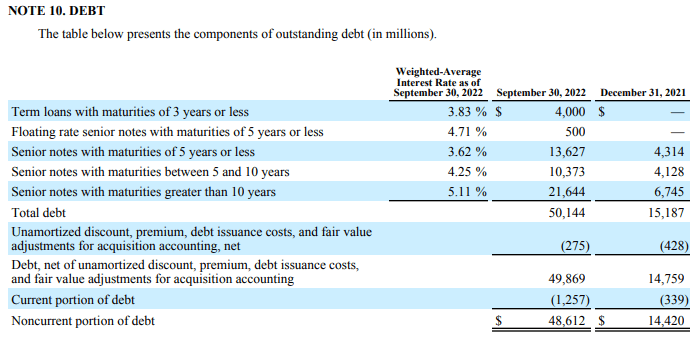

Warner Bros. Discovery Debt (Company Filing. 10-Q)

Last quarter the company ended the period with $2.5 billion cash on hand and $50.4 billion in total debt (gross, per the conference call) after having repaid $6 billion of debt since the closing of the merger. We expect that the company will continue to pay down debt aggressively in order to meet their 2024 YE goal of 2.5x-3.0x gross leverage. While the growth in EBITDA that management is predicting will help lower the current leverage number towards the target, the company will still have to pay off all corporate maturities in 2023 and repurchase some debt in 2023 as well in order to remain on track and ultimately achieve the target.

We would like to see at least $1 billion in debt repurchases for the fourth quarter ($2 billion would be ideal, but the company has already repurchased around $6 billion, so $2 billion in Q4 may be a stretch) as we believe that would set Warner Bros. Discovery up nicely for addressing debt over the next two years.

It is important to note that due to management’s goals being stated in different terms, we know that the long-term goal is measured on a gross debt target but that their statements for leverage to end 2022 are in net debt terms. This makes estimating what exactly the company does in Q4 as it relates to debt repurchases a bit more difficult because net leverage factors in the cash against the debt; so management does not necessarily have to repurchase the debt but can keep the cash on the balance sheet and it basically accomplishes the same goal.

The company will have to be aggressive in 2023 on debt repurchases because they only have about $365 million in corporate debt maturing, as it appears they have already paid off the 2023 tranche of their term loan which was due to mature in October 2023. The 2025 tranche of the term loan has $4 billion remaining on it and will most likely be a prime target for management to pay down, especially as it is now some of the higher yielding debt due to its floating rate nature (the coupon is calculated by taking 1 month LIBOR and adding 1.375%). Paying down this debt would also have the added benefit of helping with cash flow as it pays interest monthly as opposed to the semi-annual payments with the bonds.

With the prices some of their debt is trading at, management has some options for reducing the debt load at prices below par while also lowering the company’s total annual interest expense. Overall this will help improve the leverage ratios and cash flows.

EBITDA/EBITDA Guidance And Cash Flow

Warner Bros. Discovery’s management team has stated that they believe 2022 was the year that they established the foundation from which to build moving forward. Full-year 2022 Adjusted EBITDA should be in the $9.0 to $9.5 billion range, and even with headwinds in the ad market we suspect that the company will be able to achieve this range, however the company’s guidance for 2023 will be far more important because management has targeted $12 billion in adjusted EBITDA for 2023 with free cash flow conversion in the 33%-50% range.

In our opinion, 2022 is a kitchen sink type of year – the data was bad, got worse and management really cleaned house. It is probably fair to say that the Warner Media assets were more poorly run than the company’s CEO David Zaslav and his team were led to believe and thus some of the projections were too optimistic. With that said, 2023 is going to be a pivotal year for Warner Bros. Discovery if they are to reach their long-term goals as it relates to leverage and creating free cash flow.

Management needs to reiterate their previous guidance for 2023 Adjusted EBITDA at $12 billion. While 2024 is the year that truly matters for their stated goals, without $12 billion in Adjusted EBITDA in 2023, and at least the 33% FCF conversion to yield $4 billion to use for debt repayment the math gets fuzzy on how Warner Bros. Discovery can get to their endpoint goals. If the ad market does not seize up, we think that $12 billion in Adjusted EBITDA is doable and could be the base case for 2024 as well (assuming weak economy with some benefit from political advertising), then management will need to repay nearly $15 billion in debt from the end of Q3 2022 through 2024 in order to get gross debt to a level where the company would be just under the 3.0x leverage target. We know that the company will have about $4.6 billion in maturities in 2023 and 2024, and we suspect that the $4 billion balance left on the 2025 tranche of the term loan will be repaid in 2023, so if EBITDA guidance holds and FCF conversion goals are achieved, then we think that the company can indeed land within the target ranges.

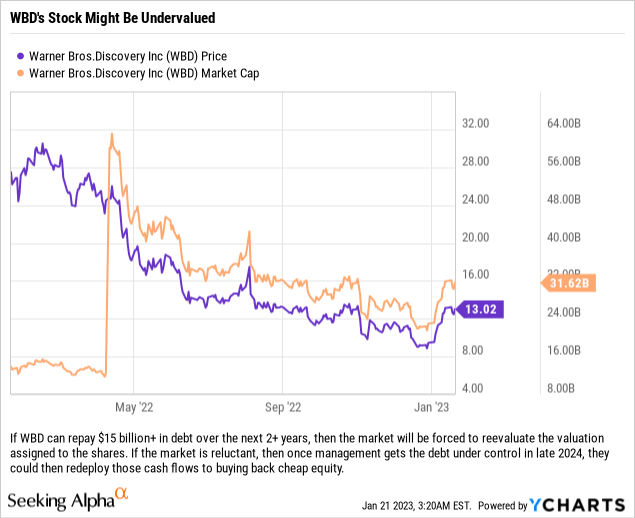

To put all of this in perspective, and to demonstrate why we think that the shares are a long-term buy, we have included a chart (see above) which shows the sharp decline in the company’s share price and the resulting market cap. If the company is successful in increasing EBITDA, cash flows and their debt repurchasing plans then the stock will have to rise significantly. If the stock does not rise, and the company is able to reduce debt by $15 billion+ in just over two years, then management could buy back a significant portion of the company in a very short period of time via a share buyback program.

New Product Releases

The new combined streaming service is set to be released in the Spring of 2023, and investors should get another update on the conference call from management concerning this item. We know that the company has been building a new interface while also constructing a modern tech stack that can perform at a higher level on both the front and back end.

Different tiers (price and advertising) will be key, especially as it pertains to the final mix among consumers because it will impact overall ARPU, ad revenues and subscriber revenues – although we will not know anything about these figures (due to expected churn from the Discovery+ service which costs less) until after the launch, management might be able to provide more insight on how all of this will break down. There was a price increase announced for HBO Max about a week ago, which is the first since its launch, and management should detail how that plays into their goal of the DTC business becoming a contributor to EBITDA in a positive way in 2025.

Investors should also see more releases for the film business, and while the box office has not returned to pre-pandemic levels the industry continues to see revenues climb higher. Potential blockbusters have new importance within the new company as they not only help the business in a big way in the current period when released but they also help drive interest in the streaming business (which is why it is important for the company’s DC division to start cranking out quality content).

Miscellaneous Items

We know that management has been looking at non-core assets and excess real estate holdings as items to divest, although they have been clear that they are not interested in selling any assets of size. The Knoxville complex has been on the market for a while, and the company has moved that item to the ‘Assets Held for Sale’ area of the balance sheet. These real estate holdings should be monetized within the next 6-12 months.

The Financial Times recently reported that Warner Bros. Discovery was looking at possibly selling a music catalogue that could generate $1 billion or more in proceeds. According the reporting, this catalogue contains the retained copyrights from the previous sale of the company’s music division and covers songs, “such as the soundtracks to the Batman films.” While the sale of these copyrights is not necessary for the company to reach its goals, a $1 billion or more transaction could allow the company to retire up to 2% of its debt.

Lastly, synergies from the merger will be updated; both for the overall savings as well as the savings to date. Savings are up to $3 billion+ but we think there is a best case scenario where savings might run as high as $5 billion depending on how aggressive management gets. A lot of the low hanging fruit has been harvested already, but these savings are key to right sizing the company moving forward.

Final Thoughts

Warner Bros. Discovery is a stock which generates a lot of passion among its believers and detractors. We think that the media business faces some serious headwinds but also recognize that there is some value in the company’s shares – especially if the management team can increase EBITDA and free cash flows over the next 12-18 months while simultaneously paying down about 30% of the company’s outstanding debt. If investors can be convinced that EBITDA can rise to the $12 billion level, then there is no question that the debt maturities that the company faces over the next few years will not be an issue.

One could probably describe 2022 as a dumpster fire – as management was forced to correct a number of missteps from previous management teams and in some cases cover the costs of fixing those mistakes with cash. It was painful to be a shareholder for sure, but 2023 should serve as the launching pad for management to release new products and begin to show investors the cash flow generating capabilities of the combined company.

Be the first to comment