Sensay/iStock via Getty Images

Introduction

Warner Bros of AT&T (T) merged with Discovery Corp. in mid-2022 and formed Warner Bros. Discovery (NASDAQ:WBD). The merger makes sense because both contribute to strong synergy benefits. WBD expects synergy benefits to reach $3.5B by 2024 through marketing optimization, optimization of content workflows, technology, procurement and organizational structures.

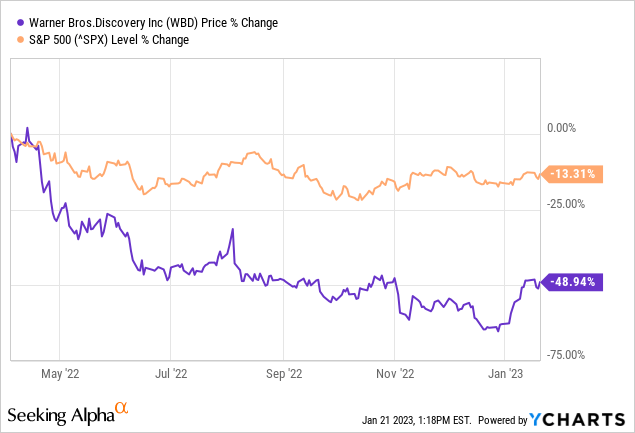

Investors have mixed views on the combined company, as its share price has fallen 49% since April 2022. Would this be a good entry point? I don’t think so. The combined company’s net debt equals 1.5x its market capitalization, and the stock trades at a premium to industry peers. The high interest rate also does not contribute to stronger earnings in the near future as the debt matures and the company has lowered its guidance.

Warner Bros. Discovery Has A Debt Problem

After acquiring Warner Bros in mid-2022, the company currently has a different financial picture. Usually when companies acquire a company of similar size, the combined company’s stock price drops due to lower earnings (goodwill write-off). The combined company is often full of debt, which is not favorable in a high interest rate environment. Even with low interest rates, the combined company’s stock price often falls.

Look at the Kraft Heinz (KHC) saga: the stock fell from $90 high to $22 low. Kraft Heinz is cash-rich, but its large net debt and increased interest expense reduced net income, giving the stock a rich valuation at $90 a share.

Warner Bros. Discovery’s cash is $2.4B at the end of the third quarter of 2022. Short-term debt is $1.3B and long-term debt is $48.6B, making net debt equal to $47.5B.

The combined company generated $10.7B in EBITDA in 2021. WBD lowered its EBITDA forecast for 2022 to $9B to $9.5B. The updated EBITDA forecast for 2023 is $12B compared to the pre-merger forecast of $14B.

The ratio of net debt to (expected) EBITDA will be 4 in 2023, an astonishingly high figure.

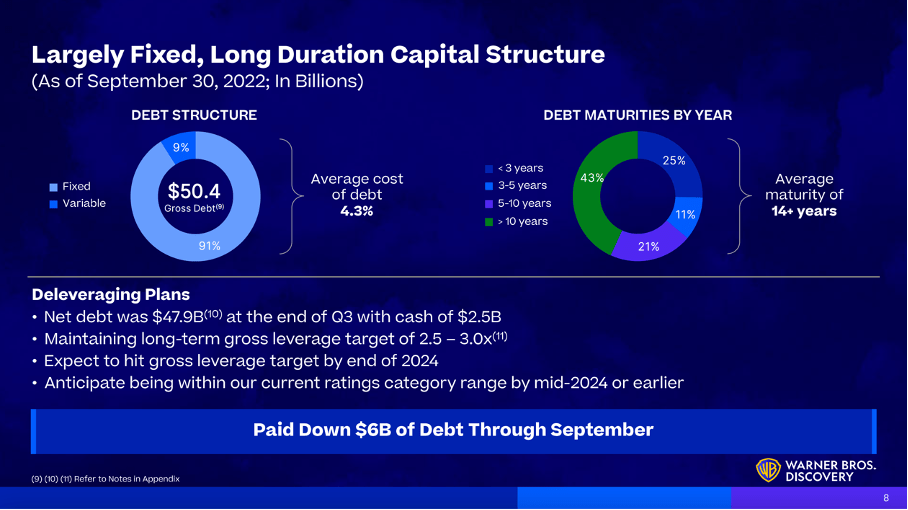

Looking at debt in more detail, the third quarter 2022 presentation shows that the average cost of debt equals 4.3%, with 25% of debt maturing between now and 3 years. WBD aims to reduce its gross debt to a gross leverage ratio of 2.5 to 3.0 and expects to achieve this goal by the end of 2024.

Capital Structure (WBD 3Q22 Investor Presentation )

Only $500M of the debt has a variable interest rate with a maturity of 5 years or less, which is currently 4.7%.

The $4B term loan has a maturity of 3 years or less. With $2.4B in cash plus an expected FCF of $6B, Warner Bros. Discovery can easily service the debt without refinancing.

It is possible that the company may refinance its senior notes with maturities of 5 years or less, as the current portion of debt is significant at $13.6B. The high interest rate environment and the BBB- rating may indicate that the refinanced interest rate on the remaining portion will be much higher than 3.62%, affecting future earnings.

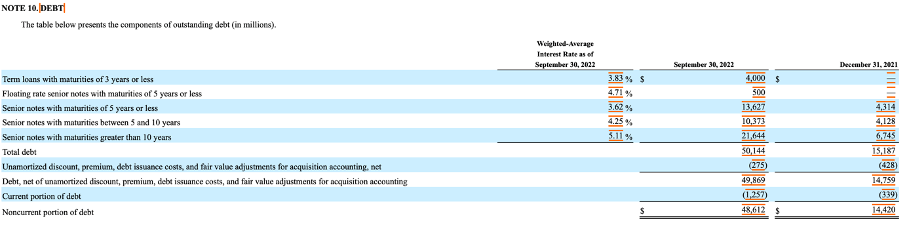

WBD’s Debt Maturities (SEC )

Looking beyond EBITDA, free cash flow is expected to be $3B in 2022, and $6B in 2023, as the company moves to implement synergy benefits.

Both free cash flow figures are weak, as Discovery generated $2.2B in free cash flow before the merger in 2021 and Warner Bros. generated $6B in FCF in the same period.

WBD generated negative FCF during the third quarter of 2022, the CEO David Zaslav said the following:

Cash flow from operations decreased nearly $700 million, primarily due to seasonality from the semiannual cash interest payment on a large portion of the acquisition debt, as well as merger and integration related costs, which totaled nearly $400 million during the quarter, including payout of retention bonuses to legacy Warner Media employees put in place prior to the closing of the transaction.

Furthermore, we reduced the balance outstanding on the securitization facility by $500 million from $5.7 billion to $5.2 billion, which also negatively impacted Q3 free cash flow, managing the program in line with a seasonal cadence of collections and revenue.

Premium Stock Valuation Compared To Industry Peers

As discussed in the previous section, debt is an important part of equity valuation. Therefore, I consider enterprise value more important than market capitalization.

The merger was completed in mid-2022, so there is no full-year data for the combined company. Therefore, I base the stock valuation on projected EBITDA of $12B in 2023.

Warner Bros. Discovery’s market capitalization is currently $32B and net debt is $47.5B (1.5x market capitalization!). The enterprise value is therefore $79.5B, making the enterprise value to (2023e) EBITDA equal to 6.6.

How does the EV/EBITDA value of 6.6 compare to other companies in the industry?

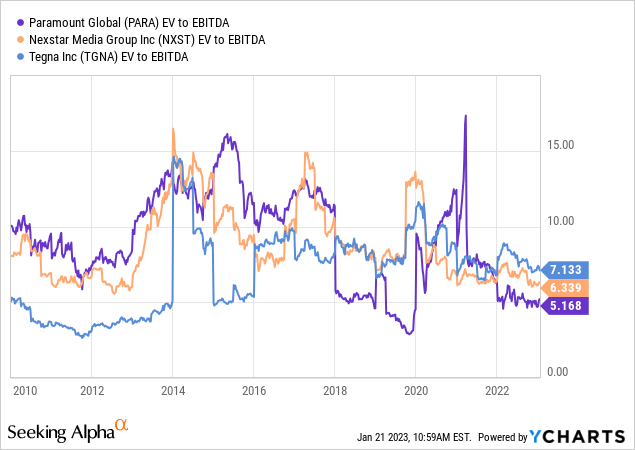

I think Warner Bros. Discovery’s closest industry peer is Paramount Global (PARA). Nexstar Media Group (NXST) and Tegna (TGNA) also provide media and entertainment. Looking at the EV/EBITDA ratios of these companies, they range from 5.2 to 7.1.

Interestingly, all these companies expect lower earnings per share for 2023, but a sharp increase in earnings per share is expected for 2024.

From the chart below we calculated that the companies’ average EV/EBITDA ratio is 6.2. That makes the valuation of WBD shares 6.5% more expensive compared to others in the sector.

Final Remark

Something that stands out is their lowered EBITDA forecast for 2023. Before the merger, WBD expected an EBITDA of $14B in 2023, it now expects an EBITDA of $12B (15% lower). WBD is currently valued on the high side compared to 3 industry peers in the communications sector.

A premium valuation, lowered expectations, large debt (1.5x market capitalization), and the high interest rate environment do not make the stock moving upward.

But there is light at the end of the tunnel: inflation numbers were better than expected (interest rates should stabilize), and debt repayment increases the company’s valuation. But for now, wait to buy the stock.

Be the first to comment