Hispanolistic/E+ via Getty Images

*** All figures are in USD unless otherwise noted as that is the company’s reporting currency.

Introduction

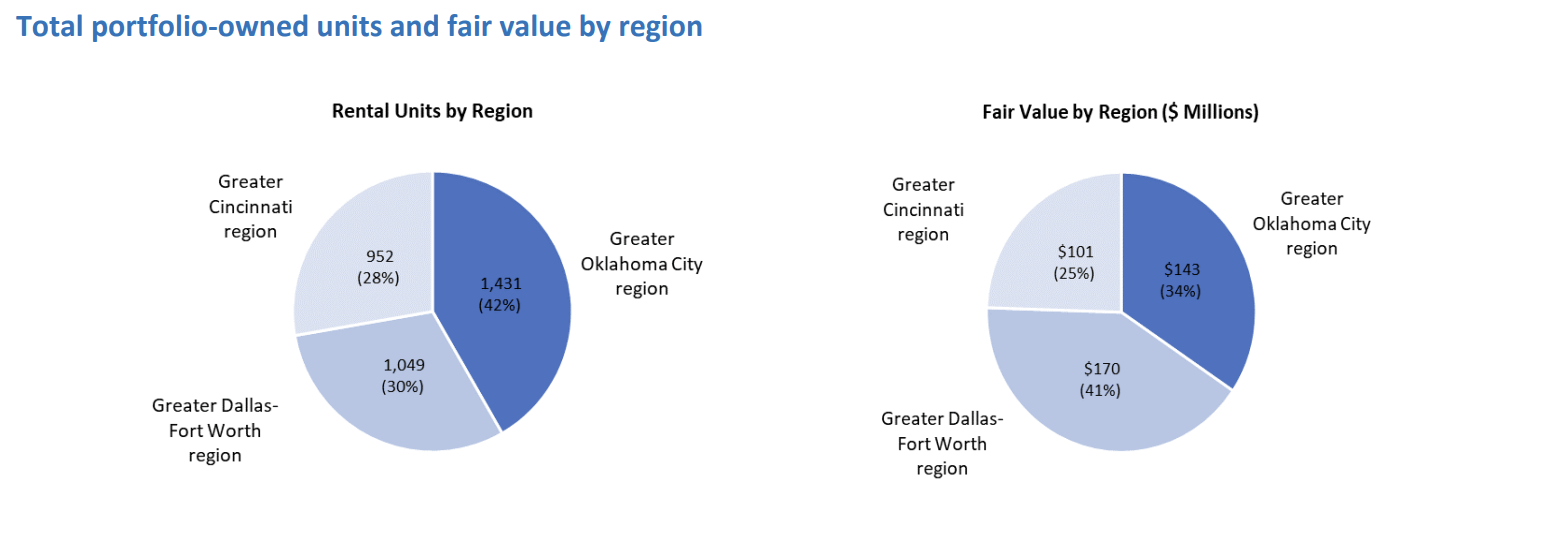

Dream Residential Real Estate Investment Trust (TSX:DRR.U:CA) is an open-ended real estate investment trust established on February 2022. The REIT completed its initial public offering of 9,620,000 units at a price of $13/share in May 2022. Proceeds of the IPO were used to fund the cash component of the purchase price for interests in a portfolio of 16 “garden-style” multi-residential properties located in the U.S. consisting of 3,432 units. “Garden-style” property means low-rise buildings, often four floors or less, housed in one common area.

The total portfolio is valued at $414 Million and properties are primarily located in three attractive markets across the Sunbelt and Midwest markets in the U.S. These include the Greater Dallas-Fort Worth region, Greater Oklahoma City region, and Greater Cincinnati region.

Q3 Report 2022 (Dream Residential Real Estate Investment Trust)

Dream DRR Asset Management LLC and Pauls Realty Services, LLC share the property management functions of the REIT and have an initial contract of ten years, and an option to renew for a further five. The base management fees are 0.25%/month of the purchase price of the properties, along with incentives tied to FFO, acquisitions, and any services provided for financing transactions. Combined these entities own over 20% of the REIT and Dream DRR Asset Management LLC’s parent company is the infamous Dream Unlimited (DRM:CA) who was the same parent company of Dream Global REIT which was bought by The Blackstone Group in December 2019 in an all-cash transaction valued at $6.2 Billion which handsomely rewarded shareholders including myself.

Performance

Although the REIT has only released one full quarter of results since its IPO, which is their “Q3 Earnings Report,” the results have only impressed.

First of all, it has managed to get occupancy up to ~93% even though this is down from its initial Q2 report of 95%. The decrease in occupancy was the result of units under renovation or recently completed as the REIT has implemented a “value-add” program on its Initial Properties. For the period from May 6, 2022 to September 30, 2022 renovations were completed on 141 and 117 units, respectively, across properties in the Greater Dallas-Fort Worth region and the Greater Oklahoma City region. Return on invested capital is consistent with management’s target of 12%-16% and expect to complete approximately 80 units over the fourth quarter.

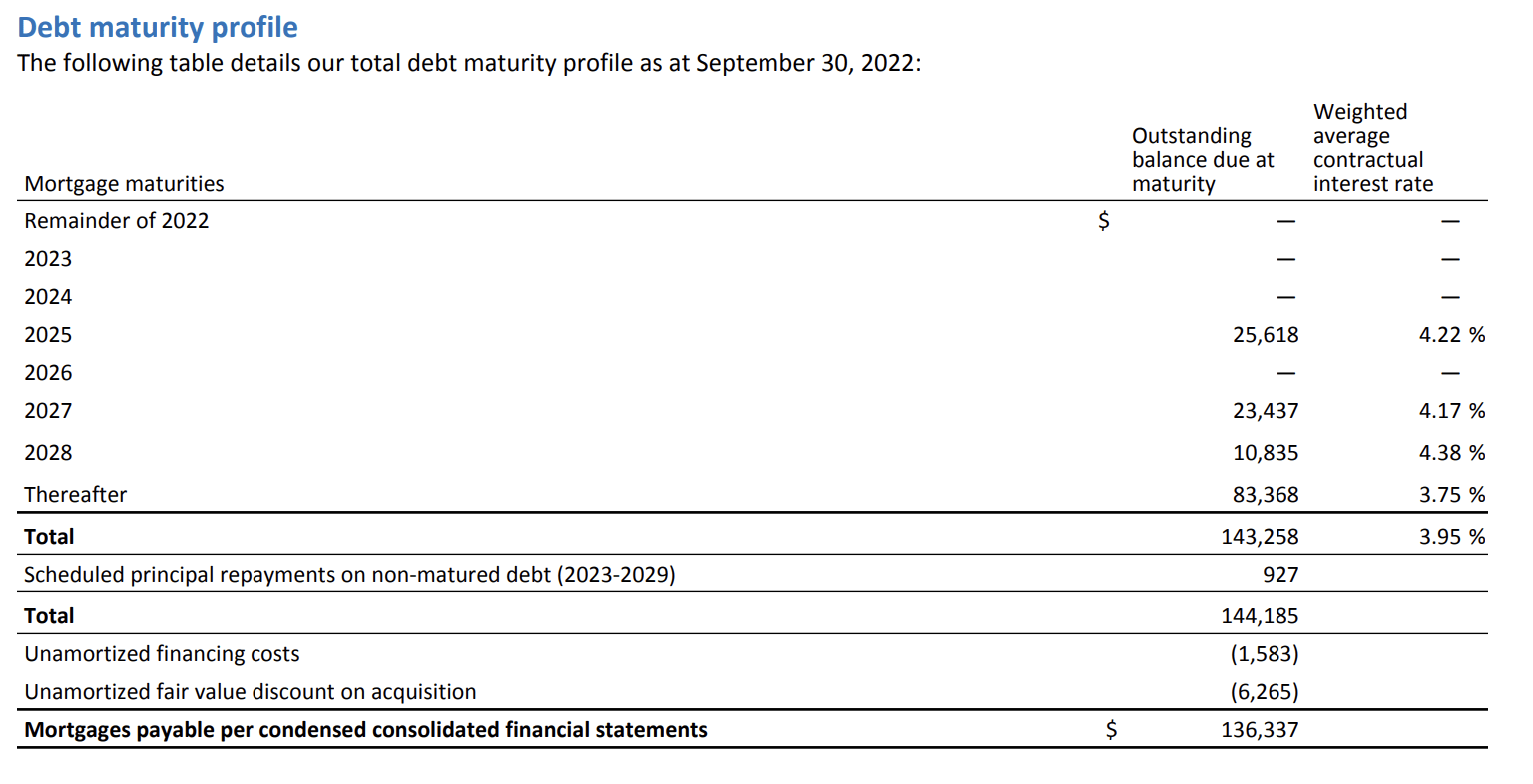

Second, management had incredible forethought to only take on fixed rate mortgage debt in June 2022 with nothing maturing until 2025 and even that only represents ~18% of total debt. Therefore, rising interest rates will have essentially no impact on FFO over the next couple of years. The weighted average term to maturity is 5.8 years with the weighted average interest rate at 3.95% which is astonishingly low as they would be hard-pressed to take on mortgage debt at less than 6% with where rates are at today.

Q3 Report 2022 (Dream Residential Real Estate Investment Trust)

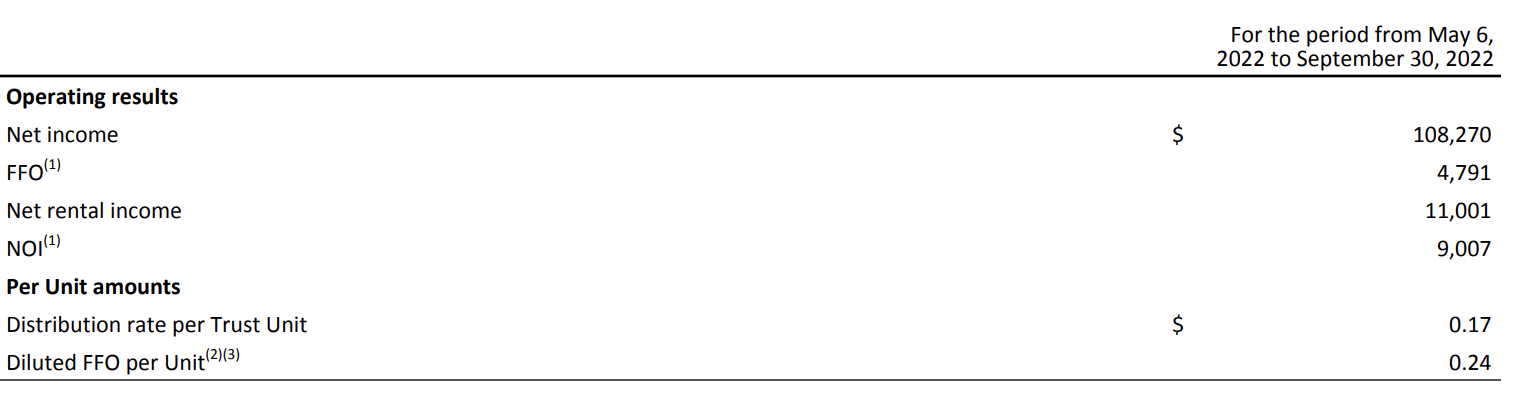

Third, 5-month FFO is $0.24/share, which more than covers the $0.035/share monthly dividend as the implied payout ratio would be 73%. More importantly, the consensus analyst estimate for the REIT is for FFO to come in a $0.60/share for fiscal 2023 which it is on track to meet and with its “value-add” program it may even exceed.

Q3 Report 2022 (Dream Residential Real Estate Investment Trust)

Valuation

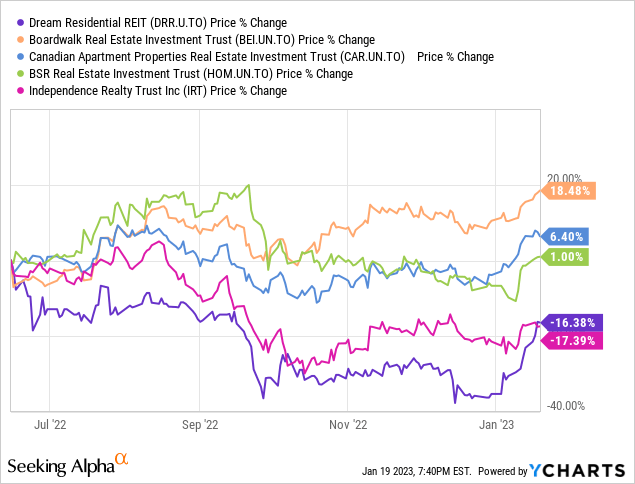

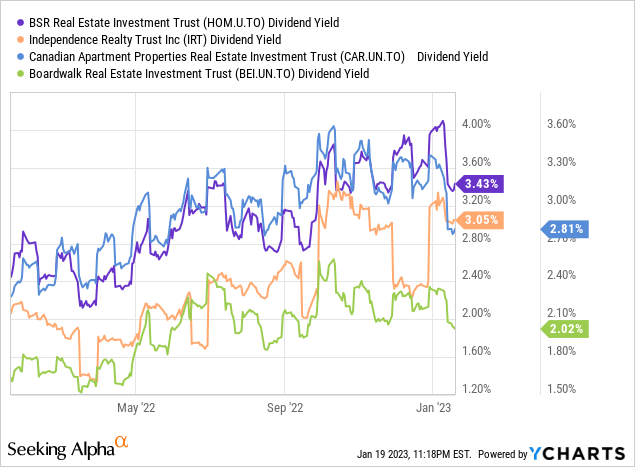

The market has not been terribly kind to this REIT since its IPO, which might be due to the general market sentiment, but BSR Real Estate Investment Trust (HOM.U.CA), Boardwalk REIT (BEI.UN:CA), Canadian Apartment REIT (CAR.UN:CA) have actually delivered positive gains since June 2022 with only Independence Realty (IRT) also being in the red.

Assuming the REIT realizes FFO of $0.60/share for its first full year of operations, the REIT would trade well below most of its peers and have the highest dividend yield at 5.09%.

| Company | Ticker | P/FFO (annualized Q3 FFO) |

| Boardwalk REIT | (BEI.UN:CA) | 17.01x |

| Canadian Apartment REIT | (CAR.UN:CA) | 20.70x |

| BSR REIT | (HOM.U.CA) | 16.52x |

| Independence Realty Trust | (IRT) | 16.40x |

| Dream Residential REIT | (DRR.UN:CA) | 14.60x |

| Median | 16.40x |

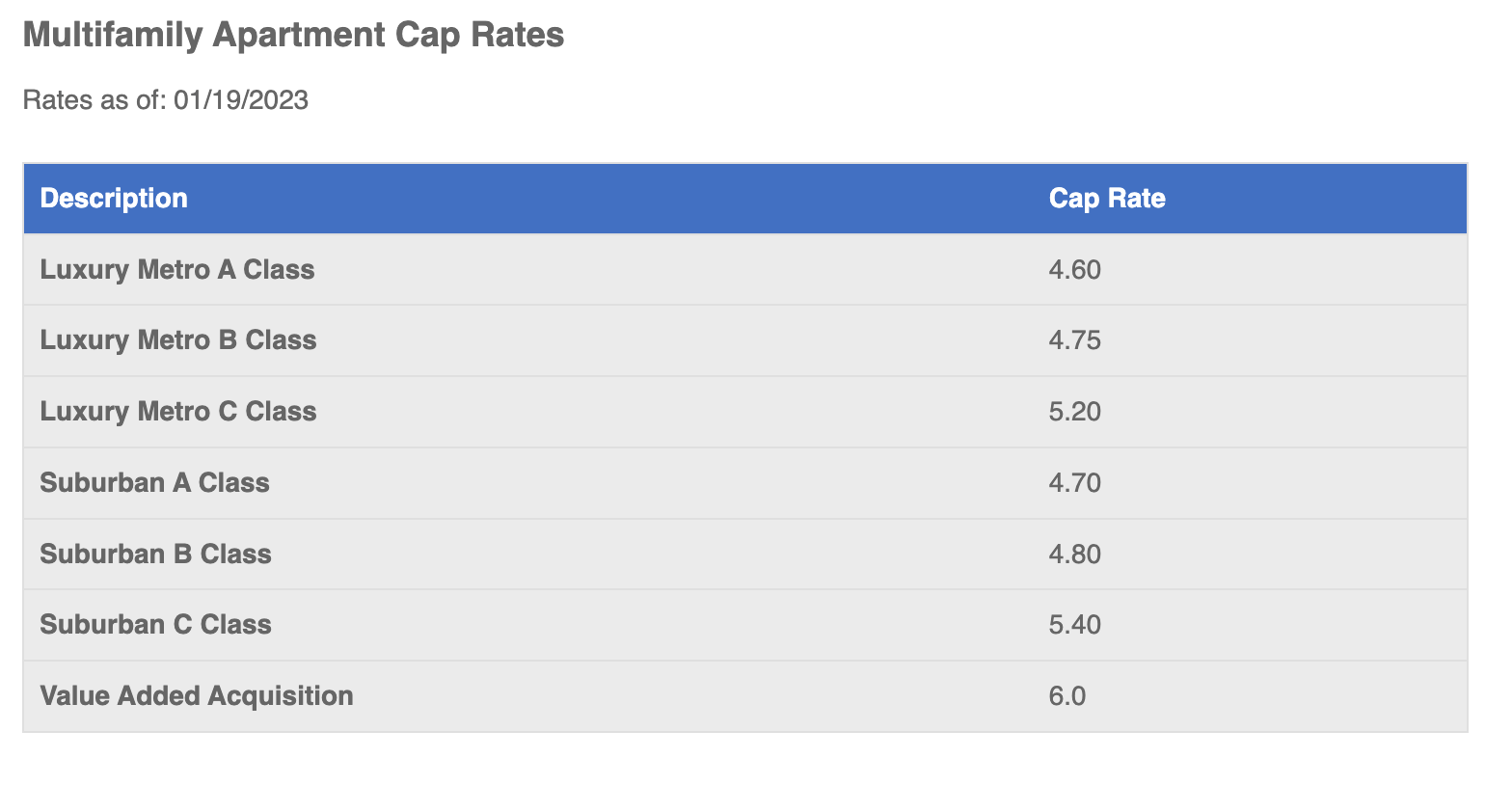

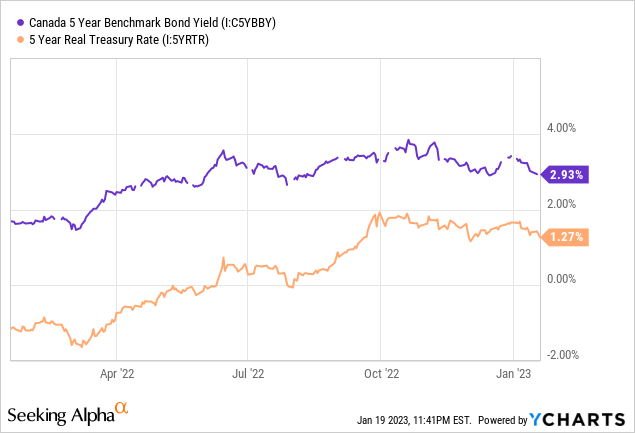

Management has estimated NAV/unit at $14.58/unit, which would imply the REIT trades at a 40% discount to NAV, which at face value looks like a steal. However, this estimate is sensitive to the cap rates used to value properties. The REIT values its properties with cap rates of 4.35%-6.15% with its weighted average cap rate being ~5%. This is not unreasonable as even Suburban Class apartments in Oklahoma have been at the 5.40%. The 5-year Canada and US Bond yields have also been running out of steam since September. Boardwalk and BSR even use slightly more aggressive cap rates to value their properties at 4.66% and 4.0% respectively, so if anything DRR is being conservative.

Q3 Report 2022 (Dream Residential Real Estate Investment Trust) CAP Rates for Apartment/Multifamily Properties in Oklahoma City (Apartment Loan Store)

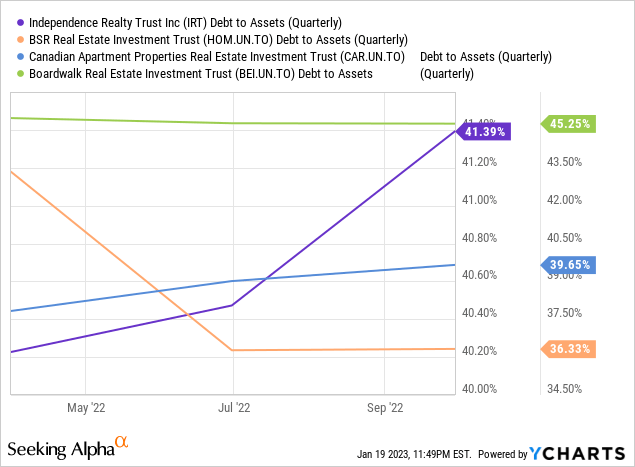

NAV will also be more sensitive when leverage is higher. Fortunately, the REIT is one of the most conservatively financed, with debt-to-total net assets of only 29%. DRR is actually the most conservatively financed of its peer group, with the rest having debt to assets of over 35%.

Conclusion

The only risk I see with the stock is it is very thinly traded, with less than 20 million units outstanding. The lack of operating history may seem like a risk, but management has an excellent track record of delivering shareholder returns through Dream Global REIT and Dream Industrial REIT (DIR.UN:CA) which is another one of my holdings. Even Dream Office REIT (D.UN:CA) delivered strong returns prior to 2020 and has held up better than many office REITs since then. I believe the set-up to initiate a position in this REIT is as strong as it ever will be at a 40% discount to NAV.

Be the first to comment