alvarez

Walker & Dunlop, Inc. (NYSE:WD) struggles to sustain growth in a challenging market. Inflation, interest, and mortgage rate increases do not work in its favor. As such, it sees continued revenue slippages that may persist this year. As interest rate hikes persist, it must also be more careful with its liquidity.

Nevertheless, I am optimistic about its capacity to sustain its operations. The strong ties with government-sponsored enterprises make it an industry staple. Also, its capitalization on M&As helps assert its dominance in the multifamily industry. Macroeconomic indicators may improve in the long run, which is crucial to its rebound.

Meanwhile, company dividend payouts remain continuous and well-covered. Yields are enticing and way better than the S&P 600 average. However, it comes with an unexciting stock price.

Company Performance

The current macroeconomic condition stays unfavorable for Walker & Dunlop, Inc. Despite the confident statements of the CEO, figures don’t lie. They point to the hammered performance of the company in the second half. It experiences the impact of mortgage market volatility. Its contraction is visible as property prices and mortgages remain fired up. It is still in contrast with the cooling down of property sales. These factors hit individual and multifamily property loan and service demand and valuation. The consolation we have now is its cost-efficiency and market positioning. These help it navigate the rugged landscape.

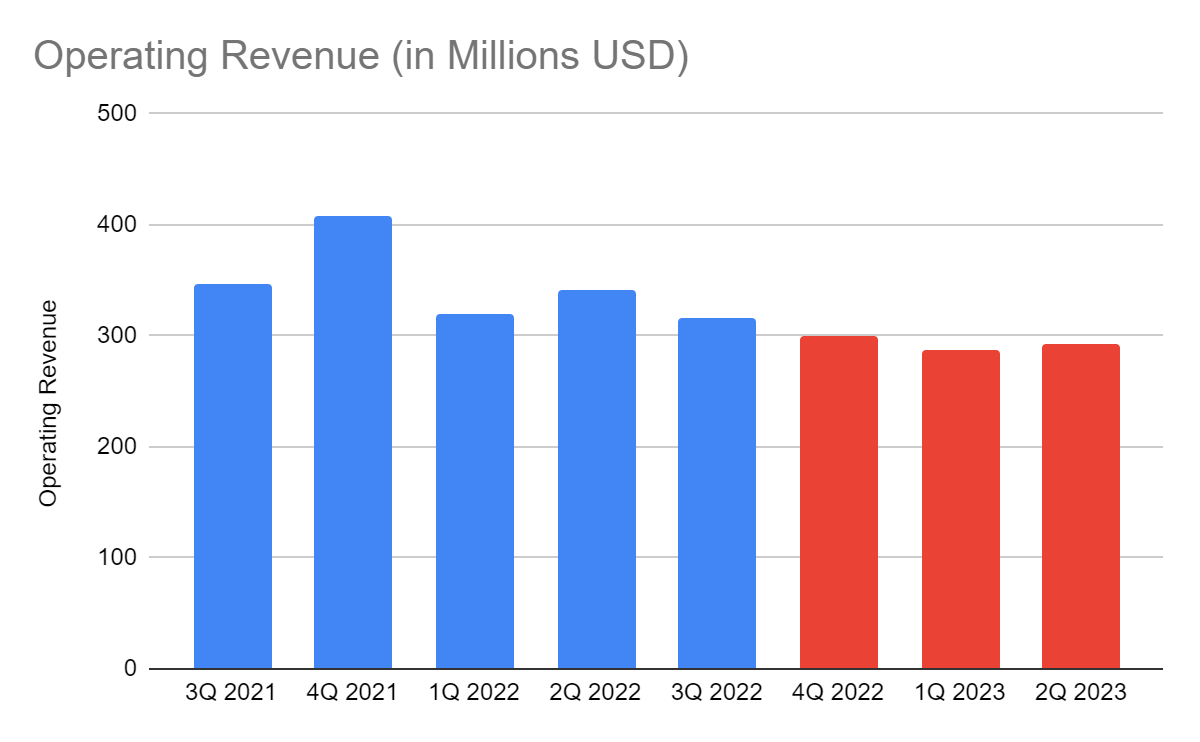

The operating revenue of $316 million is a 9% year-over-year decrease. Most of the revenue components have a noticeable decrease. It is most evident in loan originations and brokerage fees, as expected. We can attribute it to higher loan losses and the changes in its fair value. Note that interest and mortgage rates remain skyrocketing despite the continued inflation lull. It is no surprise that price and mortgage increases have a substantial impact. First, it limits WD’s capacity to keep loan rate levels flexible and favorable. In turn, it erodes the capacity of buyers and businesses to purchase properties. Second, it leads to a lower transaction volume.

Operating Revenue (MarketWatch And Author Estimation)

Thankfully, its loans held for sale do not show a fair value reduction. It reflects well-managed credit spreads with maintained liquidity associated with its credit factors. It is better than in the first half when inflation reached its peak. Also, it maintains deep ties with Fannie Mae and Freddie Mac. It now holds 17% of the Fannie Mae market share compared to 14% in the comparative quarter. As such, the company exudes prudent loan management despite the hammered yields.

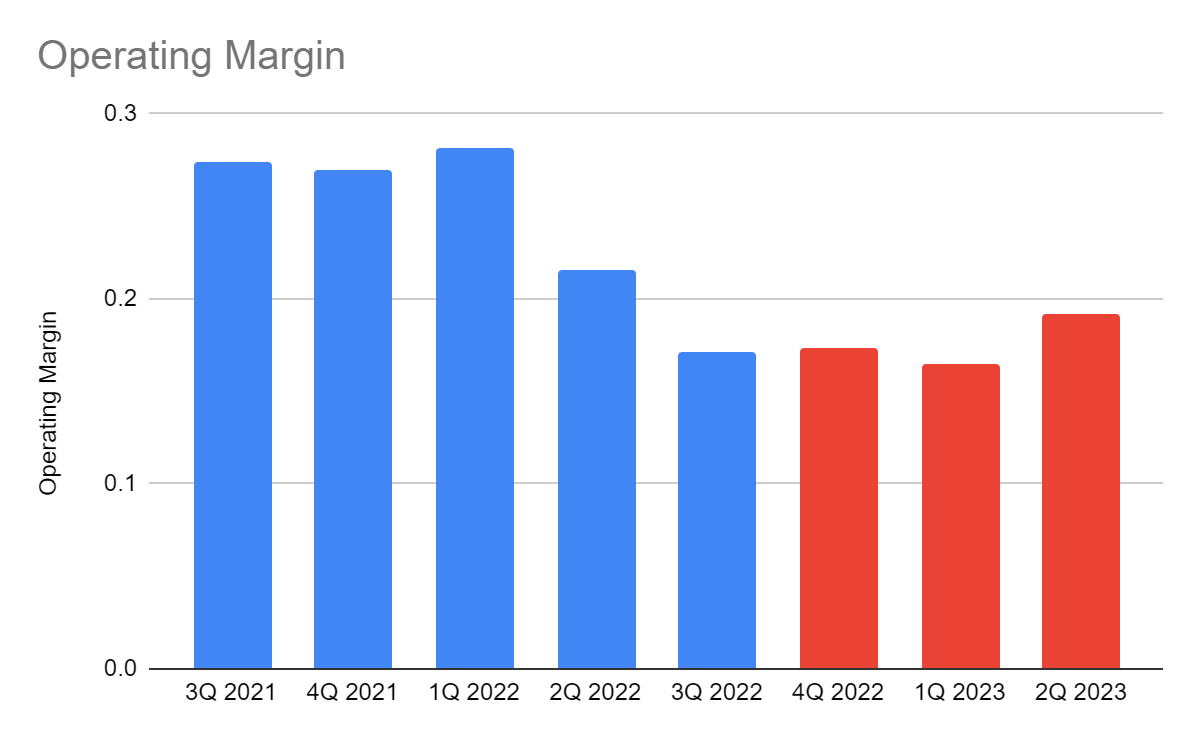

Moreover, WD makes up for its revenue slippages through its efficient asset management. It remains successful in stabilizing costs and expenses despite rising prices. The operating costs and expenses are 3% lower than in 3Q 2021. But, of course, more is needed to offset revenue reductions. Its cost-efficient strategies are still one of its strongholds. It remains viable with an operating margin of 17% lower than 27% in 3Q 2021. Margins are also lower than the sequential time series. If we adjust it using non-cash mortgage servicing rights, the EBITDA margin will be 24%. It is higher than 21% in the comparative quarter.

The company must be more careful this year as economic trends remain uncertain. But I expect its performance to be more stable in the second half. Interest and mortgage rates have yet to peak, but their increments may slow down. From the 5-5.25% and 7-7.2% estimates, I am more optimistic with my projection of 4.5% and 6.8%. But of course, the advantages may not materialize in the first half. The revenue downtrend may continue, but I expect its decrease rate to slow down. Costs and expenses may remain manageable as inflation keeps decreasing. Hence, I project a more stable revenue and a slight sequential margin expansion.

Operating Margin (MarketWatch And Author Estimation)

How Walker & Dunlop, Inc. Will Fare This Year

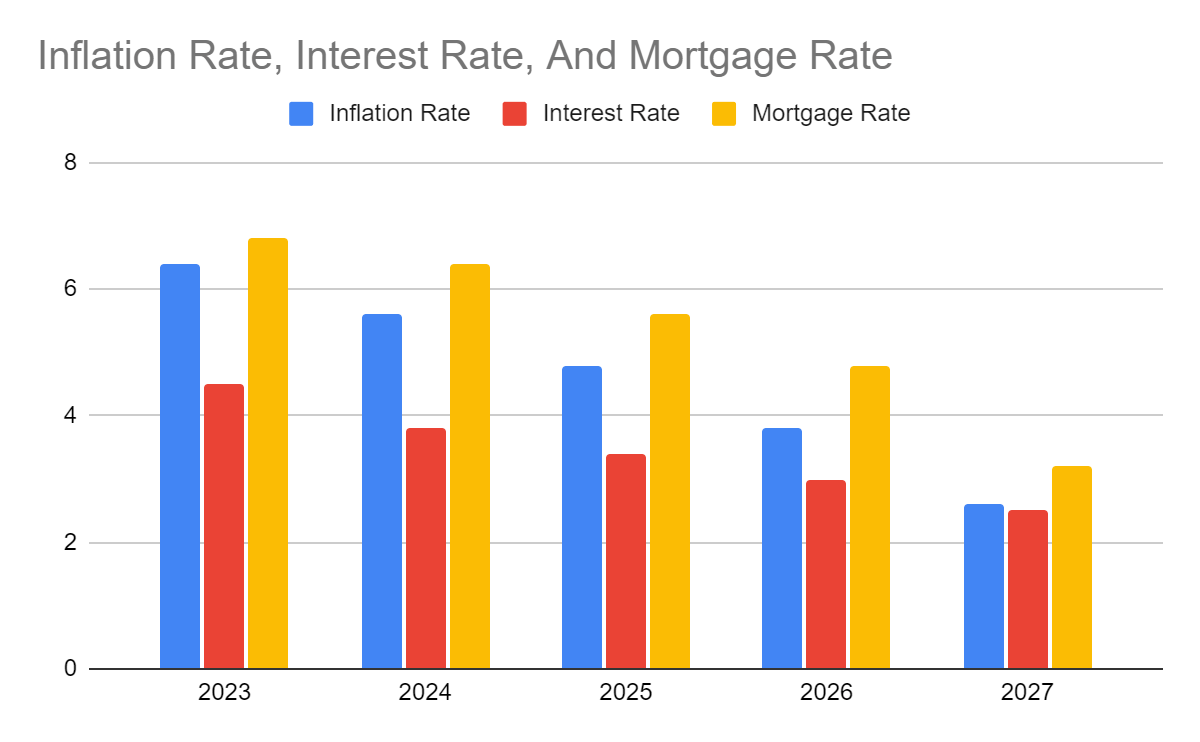

Walker & Dunlop operates in a highly volatile and cyclical market. It is my third coverage of thrift and mortgage finance companies. You can see my previous coverage here and here. I stay on the watch as I look for potential investments in the industry. Its deep ties with government enterprises make it more resilient to economic cycles. But it has to be more cautious and improve its risk management. Now risks are emerging and disrupting companies as the economy remains sour. Thankfully, inflation has become more manageable in recent months as it cools down to 7.1%. It can help manage interest and mortgage rate hikes better. I expect them to increase some more this year but with lower-than-expected increments.

Inflation Rate, Interest Rate, And Mortgage Rate (Author Estimation)

Multifamily Home Loan Rates (ST. LOUIS FED)

Also, I don’t think there will be another massive market crash. It contradicts suppositions of the second-largest bubble burst since The Great Depression. Although property sales and loan originations are cooling down, other aspects must be taken into account. After the Great Recession, property inventories have always been insufficient for market demand. We can attribute it to property builders staying in the safe zone. Construction and sales have not fully ramped up over the past decade. Also, demographics are changing while the labor market remains stable. Considering these things, properties remain relatively secure these days. Even better, we can see a slight boost in properties as prices and mortgage rates ease. The same study shows a 5% increase in people saying it’s an excellent time to buy properties. Meanwhile, the percentage of skeptics decreased from 79% to 76%. This improvement is led by Fannie Mae, one of WD’s customers.

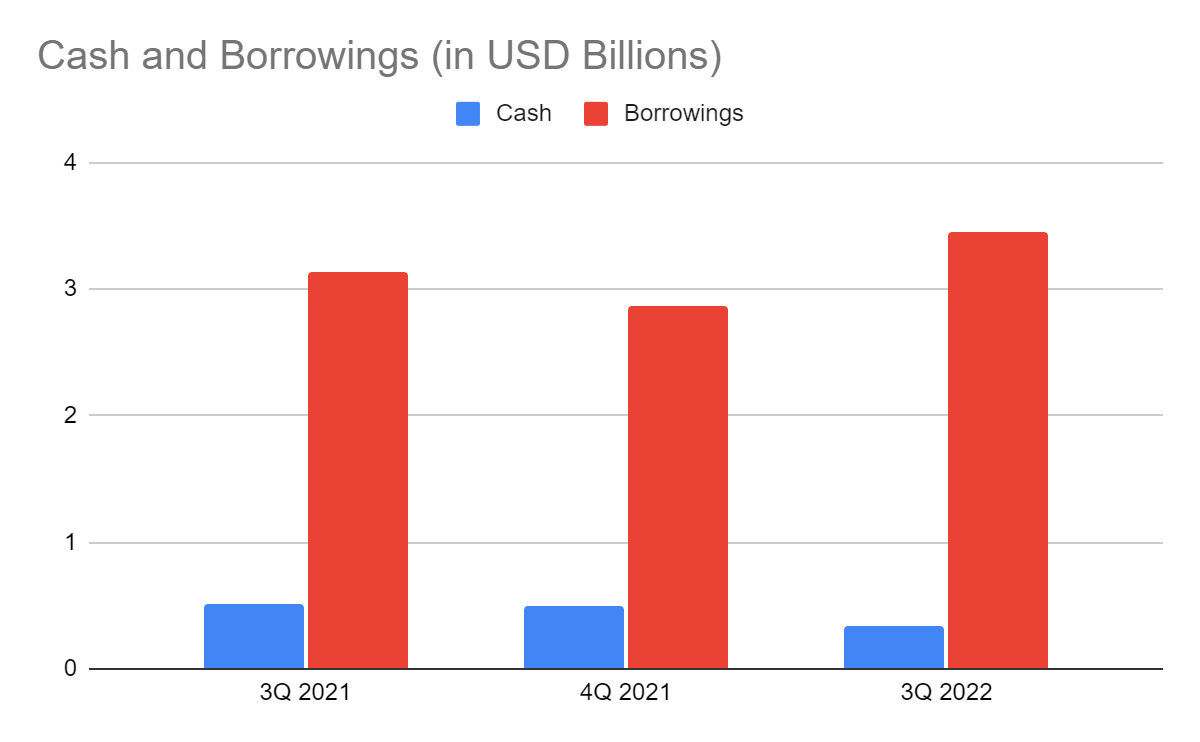

What may help WD stay sustainable is its stable cash reserves. WD capitalizes on acquisitions, so having adequate cash is crucial for its liquidity. Also, it has a lot of loans held for sale that may pay off as cash inflows in the long run. But the company must still be careful with its borrowings after increasing by 15%. It may increase further in line with interest rate hikes. It can be a double-edged sword that may hamper loan sales and increase interest expenses. Thankfully, it maintains adequate income to cover its corporate borrowings. Its Corporate Net Debt/EBITDA remains acceptable at 2.5x as of this quarter.

Cash And Cash Equivalents And Borrowings (MarketWatch)

Stock Price Assessment

The stock price of Walker & Dunlop, Inc. has been hammered in the last year. It has not regained its value even after its three-week rally. At $88, it has been cut by 41% from its starting price in 2022. Despite this, it does not seem cheap, as some price metrics suggest. The price-earnings multiple of 11.7x and my estimated annual EPS of $6.58 gives a target price of $76.98. The same goes for NASDAQ, with an estimated EPS of $6.68 and a target price of $78.20. This year, I still don’t think there will be much difference. I expect WD’s near-term performance to be better than in 2022 but still low as risks remain evident. My target EPS for 2023 is $7.80, based on the historical EPS growth. I reduced it by 5% from my original target price to account for potential risks. With that, the target price will be $92.20, a 4% upside in the next 12-18 months. NASDAQ is more optimistic, with an estimated EPS of $8.35, giving a target price of $97.7, an 11% upside.

Meanwhile, dividend payments remain attractive, given the sustained growth since the first payout. It also has a yield of 3%, more than twice the S&P 600 average of 1.48%. Payments remain well-covered, as shown by the Dividend Payout Ratio of 45%. To assess the stock price better, we will use the DCF Model.

FCFF $298,000,000

Cash $344,000,000

Borrowings $3,400,000

Perpetual Growth Rate 4.8%

WACC 9.2%

Common Shares Outstanding 33,012,082

Stock Price $88.7

Derived Value $92.89

The derived value is higher than my target price using the PE multiple. There may be an upside of 4.8% in the next 12-18 months. Investors may find it an opportunity, but the potential increase remains small.

Bottomline

Walker & Dunlop, Inc. must still endure market volatility with hammered revenues. Despite this, it stays viable and liquid, showing it can sustain its operations. It can also cover its dividends with yields, a dividend investors may consider. But the stock price still has to be cheaper, given the little near-term upside potential. It is consistent with its most recent fundamentals. As its performance in a highly cyclical market shows, things may not materialize soon.

Nevertheless, I am optimistic about its long-run rebound, given its market standing. As such, investors may still have to determine or wait for a better entry point. Doing so will help avoid a potential bull trap, given the three-week rally. The recommendation, for now, is that Walker & Dunlop, Inc. is a hold.

Be the first to comment