honglouwawa

I first wrote about the Vanguard Growth ETF (NYSEARCA:VUG) in August 2021, arguing that the VUG was ground zero of the everything bubble. The ETF went on to peak a few months later before falling almost 40% to its trough in October. After an improvement in the technical picture and a sharp drop in valuations, I am covering my short positions in this ETF, although I continue to expect the VUG to post negative real returns over the long term and will look for another opportunity to short.

The VUG ETF

The VUG tracks the performance of the CRSP US Large Cap Growth Index, which selects stocks based on six growth factors: expected long-term growth in earnings per share, expected short-term growth in earnings per share, 3-year historical growth in earnings per share, 3-year historical growth in sales per share, current investment-to-assets ratio, and return on assets. As a result, the Technology and Consumer Cyclicals hold a combined weighting of 67%. The weakness in these two sectors has seen their weighting fall from 78% over the past 18 months. Fully 34% of the index comprises of the ‘Big 4’; Apple (AAPL), Microsoft (MSFT), Amazon (AMZN), and Google (GOOG)(GOOGL). The fund charges an expense fee of 0.04% and pays a dividend yield of 0.7%, slightly below the dividend yield on the underlying CRSP US Large Cap Growth Index.

Technical Picture Has Improved

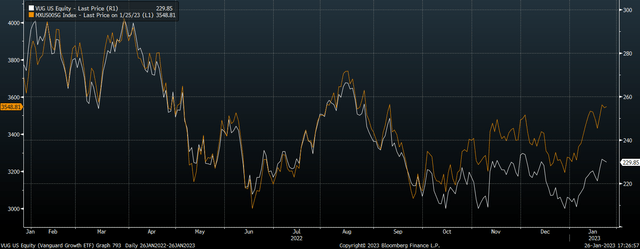

The VUG found key support in October at its pre-Covid highs and has since rallied back above down trendline resistance from the January highs. Yesterday’s weakness threatened to reastablish the downtrend, yet the dip was bought, keeping the focus on the upside.

VUG ETF Share Price (Bloomberg)

The small cap growth segment appears to be leading the rally, having broken and held above resistance-turned-support. The recent outperformance of small cap growth bodes well for a further recovery in the VUG in the near term.

VUG Vs MSCI US Small Cap Growth Index (Bloomberg)

THE VUG has been very closely correlated with US real (inflation-linked bond yields) over the past year as the long-duration nature of growth stocks makes them highly influenced by expectations of long-term interest rates relative to inflation. As I argued in ‘TIP: The Great Monetary Reversal Has Begun‘, I expect US real yields to head further south over the coming months, and this should be expected to put upside pressure on the VUG.

Valuations Have Improved But Real Return Outlook Still Negative

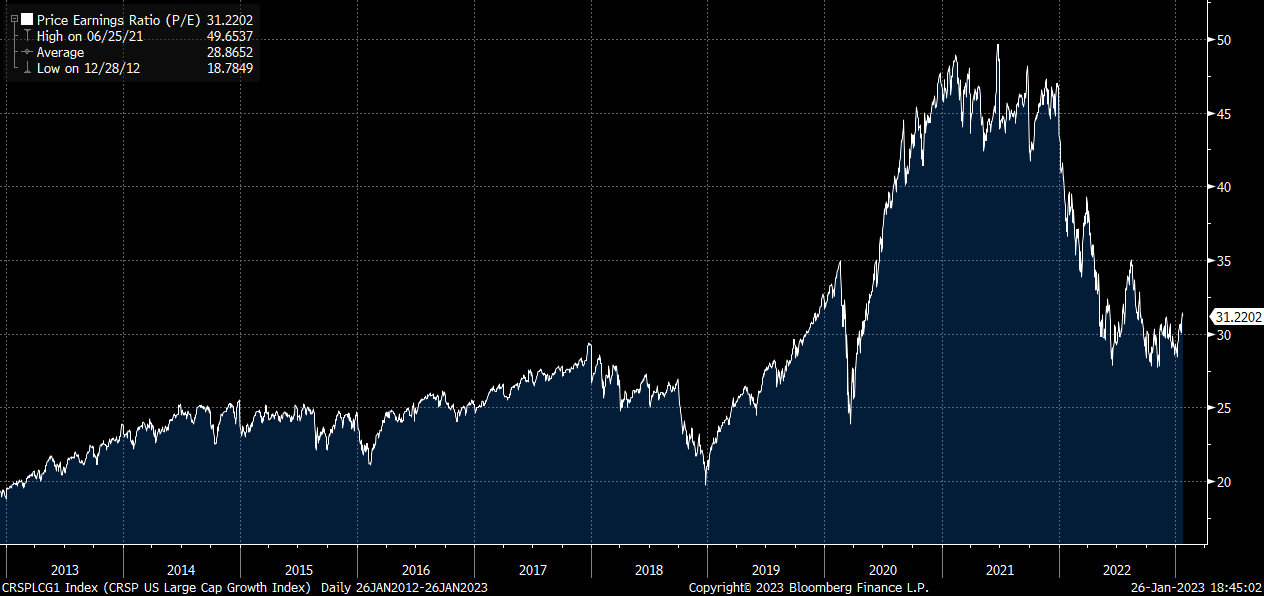

The trailing PE ratio on the CRSP US Large Cap Growth Index has fallen from a peak of almost 50x in mid-2021 to 33.1x today, thanks to a fall in share prices and a rise in earnings.

PE Ratio: CRSP US Large Cap Growth Index (Bloomberg)

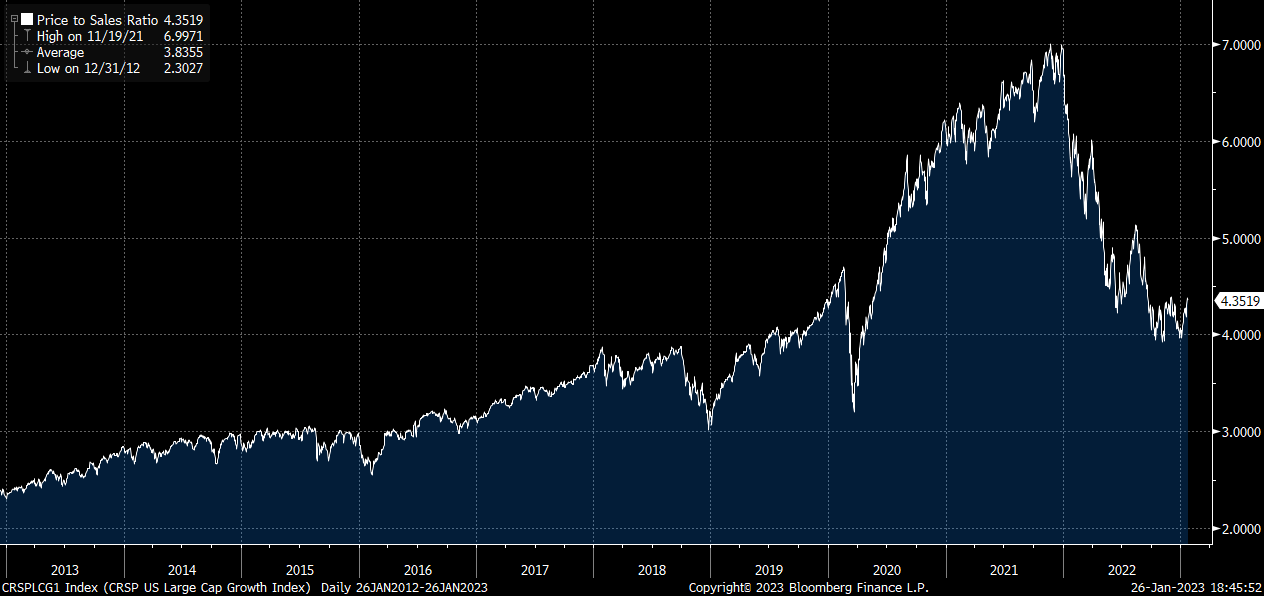

Earnings have actually underperformed sales over the past 12 months, which has seen profit margins fall over a full percentage point from their peak. As a result, the price-to-sales ratio has fallen 40% from its peak and is also back below its pre-Covid highs.

PS Ratio: CRSP US Large Cap Growth Index (Bloomberg)

However, even after such a large drop in valuations, long-term real return prospects remain poor, with the VUG highly likely to generate negative real returns over the next decade. The PE ratio remains double that of the Vanguard Value ETF (VTV), which I covered here, and is higher than any other peak seen outside the last two years and the 2000 tech bubble.

Expensive valuations have not prevented the VUG from performing well in the past due to persistent strong sales and earnings growth. Going forward, as I argued in ‘EDV: Expect Major Outperformance Vs. U.S. Stocks‘, real GDP growth is likely to be much weaker going forward. The VUG is now dominated by companies that are already mature and dominating their respective industries, meaning that future sales growth will converge to the rate of US and global GDP, below 1%. Even if profit margins remain at near-record levels of 14%, with a dividend yield of 0.8%, real returns are likely to be less than 2% annually over the long term, assuming no change in the dividend payout ratio or valuations.

The real risk in the VUG comes from a continued contraction in valuations. A mere 0.5 percentage point increase in the dividend yield from the current level of 0.8% to 1.3% over the next decade this would act as a drag on returns equivalent to 5pp per year, bringing real returns down to -3% annually.

How I Am Playing It

I have taken profit on all of my short positions in the VUG, as well as the Nasdaq, as I noted here, preferring to be long US Treasuries than short stocks growth at this juncture. If we see a strong rally in the VUG I may use strength to re-establish short positions, while any break back below the January 19 low of USD220 would suggest a resumption of the bear market, warranting renewed short positions.

Be the first to comment