lcva2

Dear readers/followers

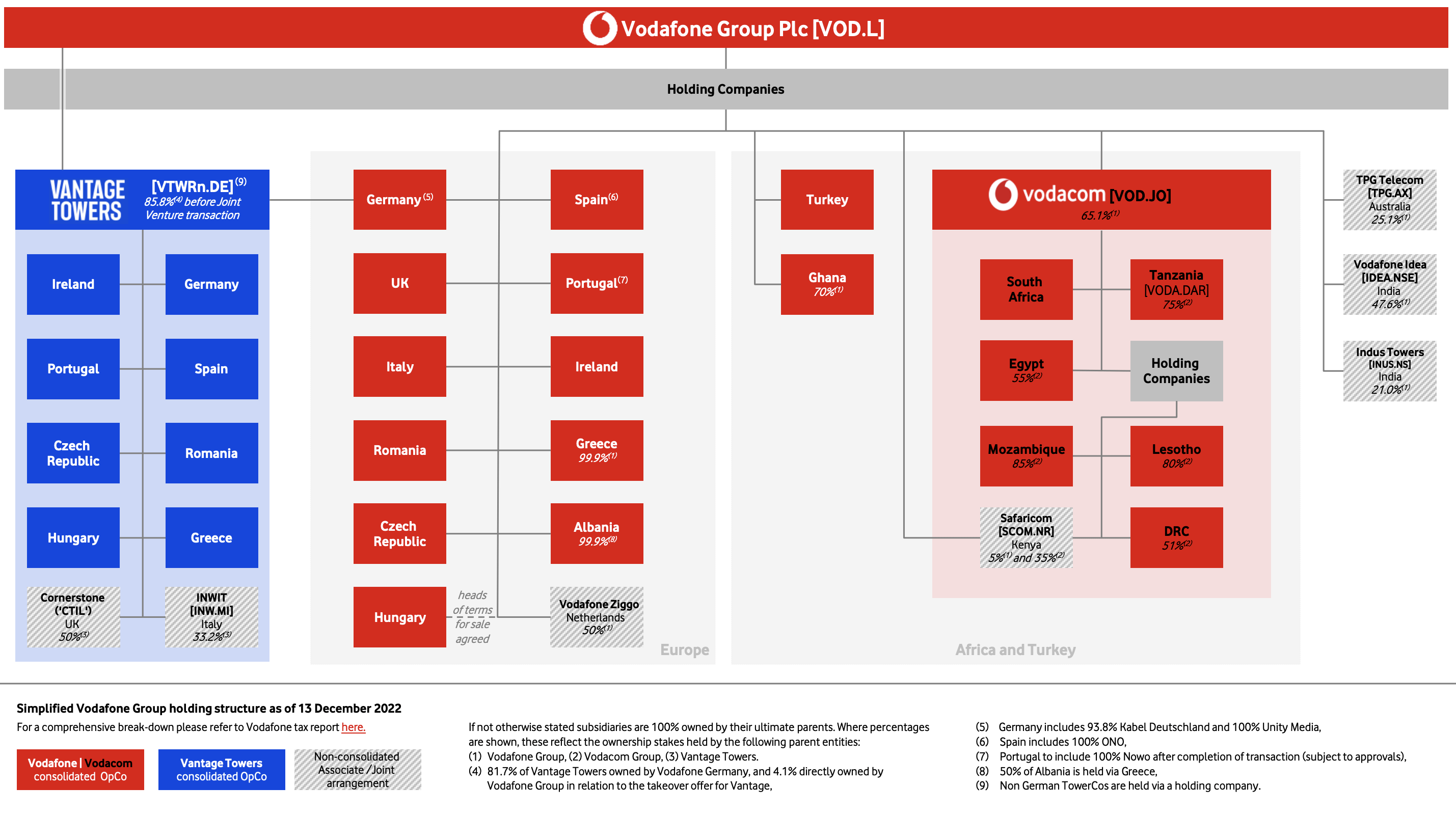

Vodafone (NASDAQ:VOD) isn’t exactly a new investment idea. The company has shown undervaluation for a long time, and I’ve even covered it before. The company has gone through one of the more extensive organizational restructurings I’ve seen over the past few years, and as late as December, has simplified its holding structure.

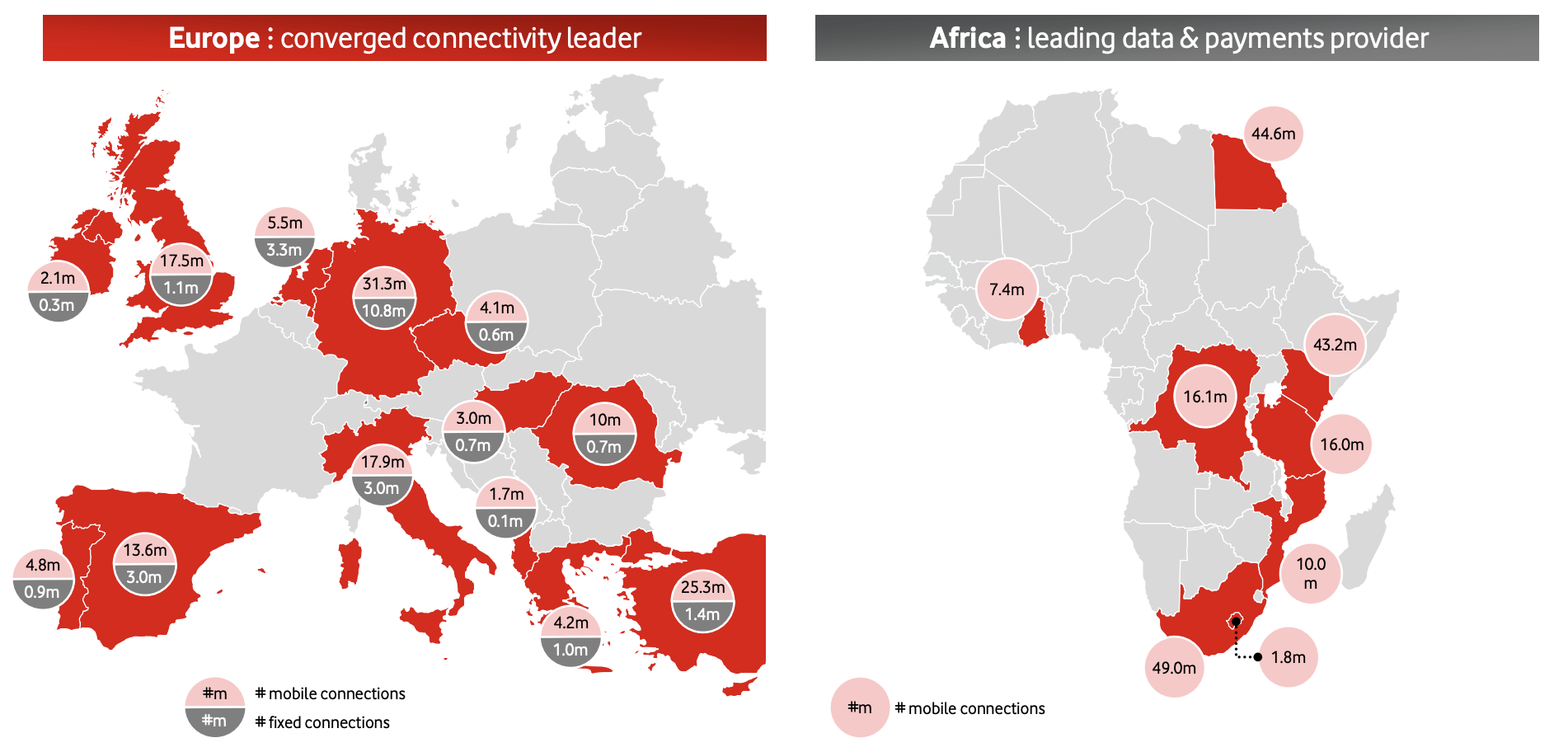

A business like Vodafone, which consists of dozens of operations in a dozen countries and more, is complex to value. This is especially true if parts of their operations are found in emerging markets or politically unstable geographies – like Turkey and Ghana, or Mozambique, Egypt, Lesotho and others. At the same time, I’m actually a fan of emerging market investments, if the mix includes a stable legacy that sort of buffers the instability found in these growth investments. And this is exactly what Vodafone does.

VOD IR (VOD IR)

To be clear, I don’t expect Vodafone to massively outperform and bounce back up in the close, near term. But my argument for investing in the company is similar to my argument in terms of investing in other telcos, which have double digits in my portfolio.

Digital infrastructure is crucial – and I see their importance and the relative value of their assets, their irreplaceability, grow going forward. At the very least, I consider quality telcos to be high-yielding bond proxies, and at best, I’ve been able to generate double-digit RoR by knowing when to buy and when to trim positions.

My current telco investments include positions like Telenor (OTCPK:TELNF), Telia (OTCPK:TLSNF), Tele2 (OTCPK:TLTZF), Deutsche Telekom (OTCQX:DTEGY), Orange (ORAN), Telefonica (TEF), AT&T (T) and Verizon (VZ). I also once again added Vodafone to that list this Friday – the London ticker.

Here I’m going to show you why.

Vodafone – Presenting the company’s current state

So, simply put, this is Vodafone today as of December of 2022.

VOD IR (VOD IR)

Vodafone hasn’t exactly been a smooth ride – as most telco’s haven’t exactly been a smooth ride. CapEx/sales ratios, increasing interest rates, churn ratios, and political instabilities not only in emerging markets but in Europe have been a cocktail that have pushed not only European “mainland” telcos down, but LSE-listed ones like this as well.

However, one of the biggest mistakes an investor can make, as I see it, is not to recognize cheap quality when it is presented to him/her.

So let me try to do that.

On a high level, Vodafone is a well-yielding telco provider with one of the largest networks and the best coverage on earth. It’s able to showcase service revenue and customer growth over time, in the 2-3.5% range on a QoQ basis. It can show good EBITDAaL growth, and it manages margins of 31.5-33.5% on the EBITDAaL adjusted side. These are not sector-leading – some telcos are closer to 40% in home markets. Vodafone also doesn’t have record-setting ROCE numbers, but they are above pre-pandemic levels. Vodafone is battling with Deutsche Telekom, Telefonica, and other companies in various core European geographies, and each of these businesses manages to chomp off small bits of market share.

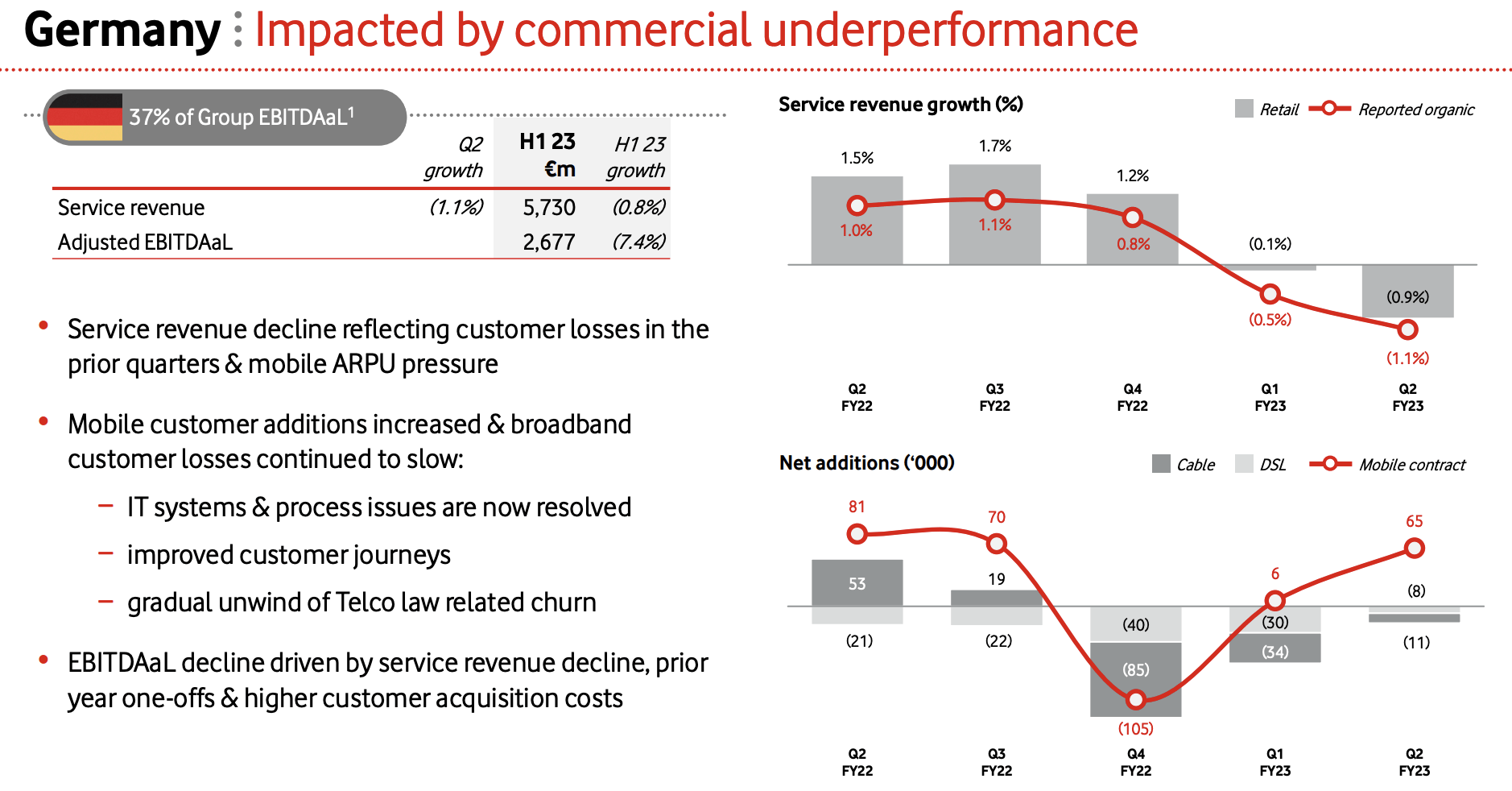

In terms of overall Group EBITDAaL, Germany is the biggest at 37%, Italy is 11%, UK is 9%, Spain at 6%, and rest-Europe at 12%. That’s core telco services. Aside from that, Financial services are 15% of EBITDAaL – that’s more or less the high-level split. The company is investment-grade rated, though “only” at BBB, meaning plenty of telcos have a notch above that.

What’s currently driving Vodafone’s performance is the German market. Given the 35%+ EBITDAaL exposure, underperformance here impacts group results fairly heavily, and that’s what has been happening for the past year, with a settlement in the Italian market also pushing things down. Positive trends have been emerging market growth as well as performance in Spain, the UK, and other European areas. Germany is a good example of a market that turned sour for the time being – similar to Orange’s Spanish market.

VOD IR (VOD IR)

But company fundamentals remain extremely robust, with a solid net debt progression. The cost of Vodafone debt at a weighted average is now at 2.5%, and its maturity profile sees very few maturities before 2026. Vodafone has nearly €4B cash, and an €8.1B rolling credit facility, meaning we’re up over €12B in total that can be deployed where needed.

Macro is the name of the game for Vodafone – and for most of the other telcos as well. The company is able to generate adjusted EBITDAaL of between €15-€15.2B per year, with an adjusted FCF of around €5B on a yearly basis. Major impacts remain inflation, one-off settlements not weighed up completely by OpEx savings, and new business growth.

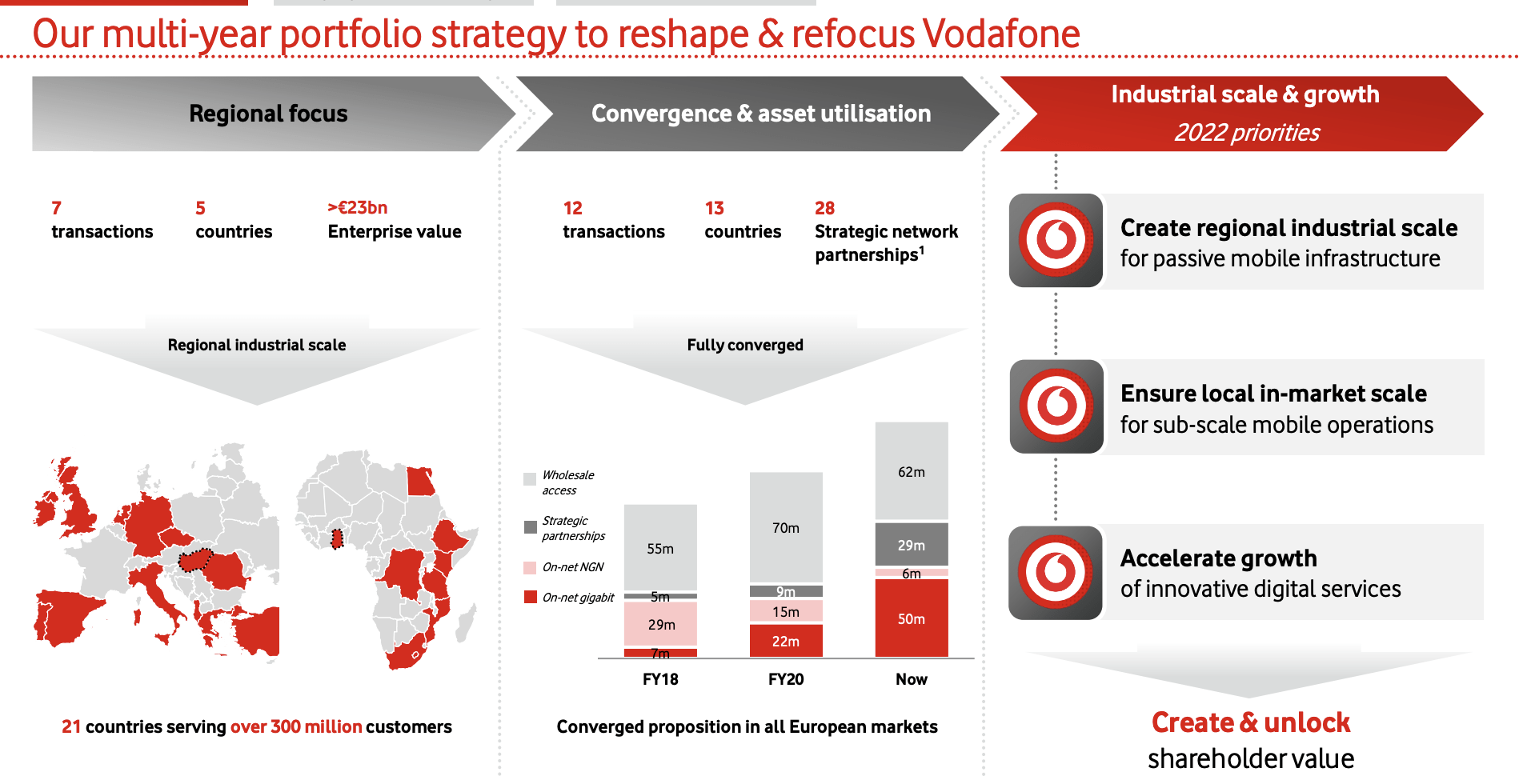

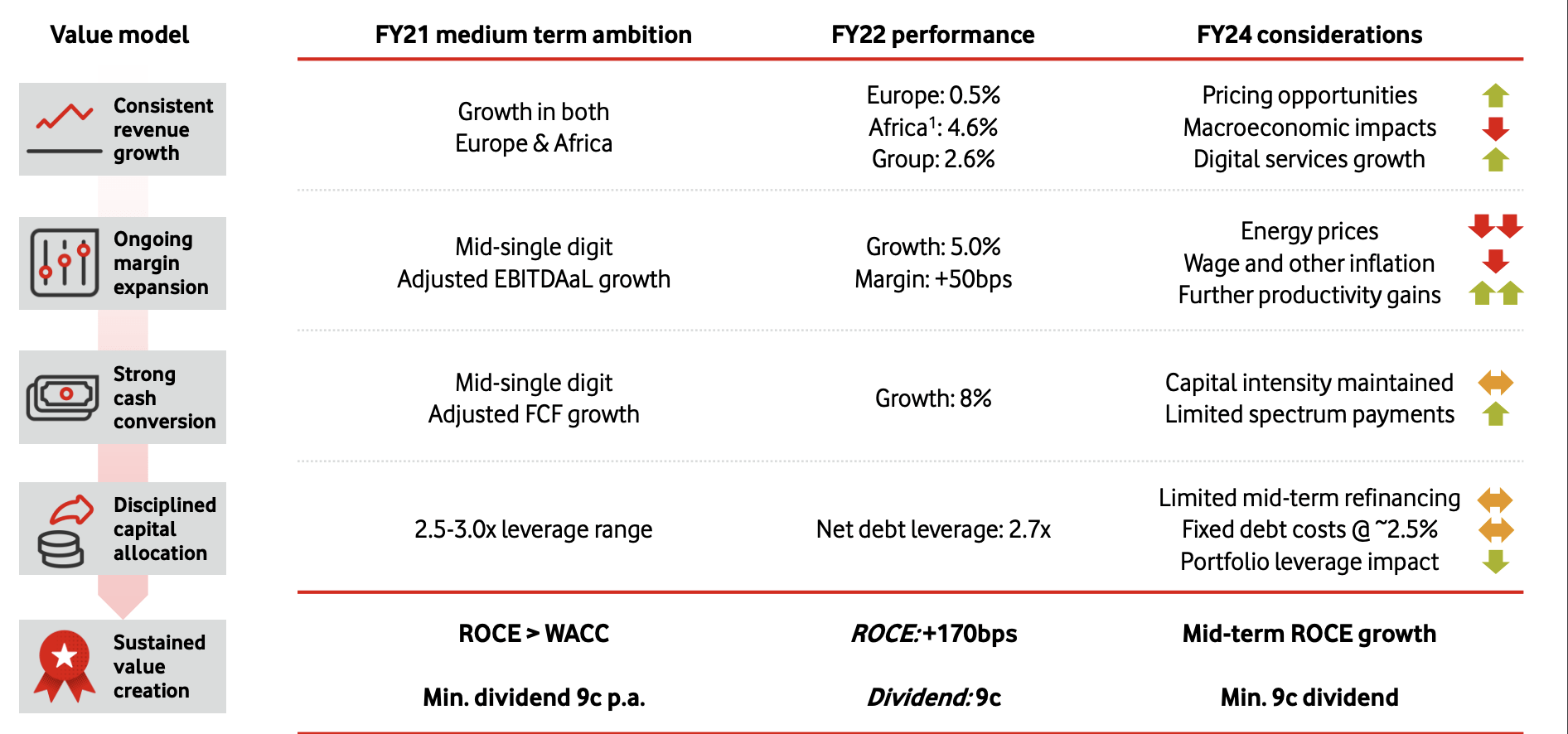

Despite the company’s challenges in Germany, the operations here are actually showing underlying strength, and the company expects to go positive here again very quickly. Vodafone also has one of the fastest networks out there, and obviously one of the best overall scales in the world. Its focus, and the core of its strategy, is now Europe (parts of it) and Africa as a growth engine.

Vodafone IR (Vodafone IR)

This is unlikely to be trouble-free – but I consider the core geographies and segments likely to continue delivering solid results that offset the worst of the downturns that can happen here – provided you buy the company at a cheap enough price. The company sees challenges…

VOD IR (VOD IR)

…but its dividend and the overall plan is “set”, and I for one see this one as very doable, which should generate some support for the share price from today’s level (we’ve already seen some of this at this time).

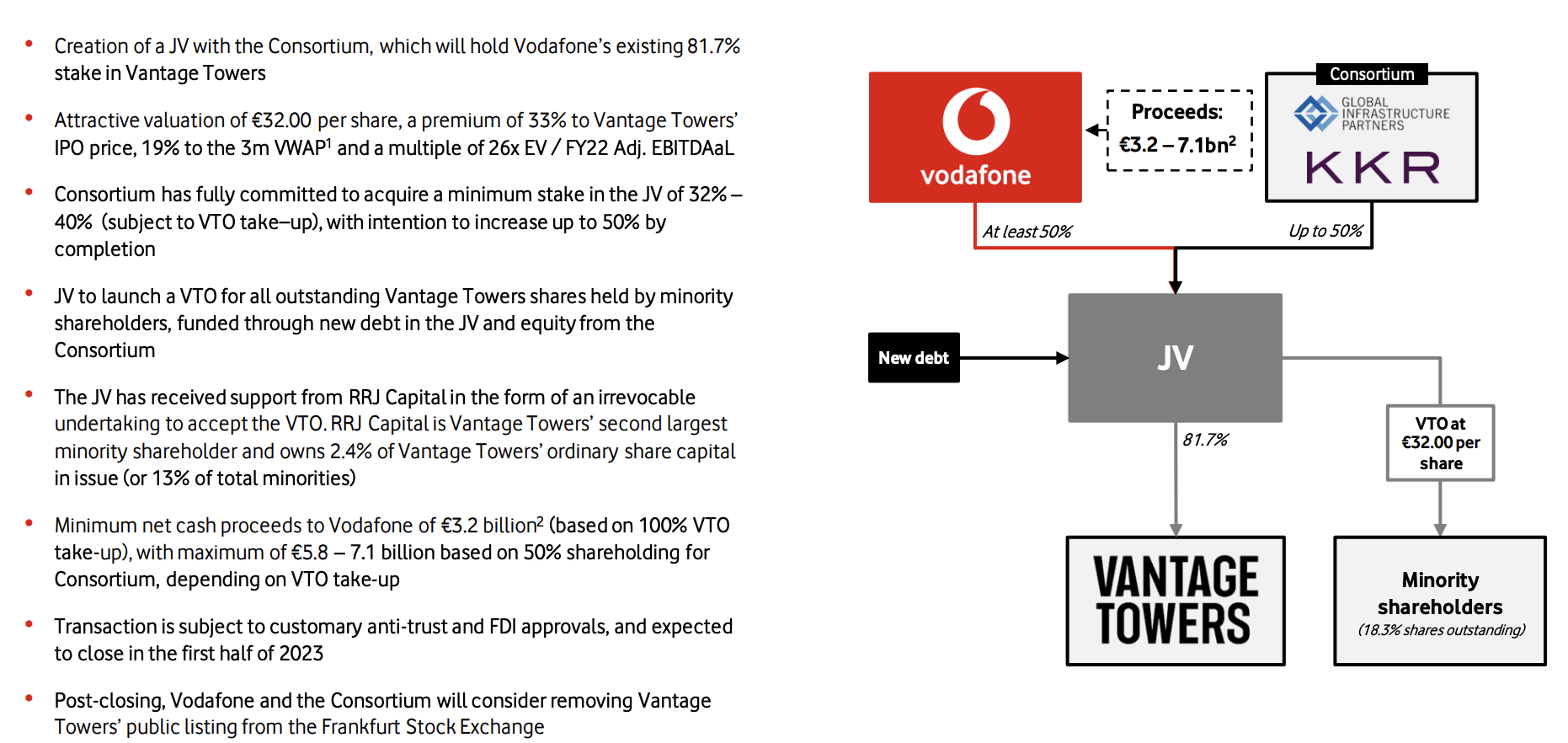

Vodafone is also part of Telefonica’s (and GIP/KKR’s plan) for a TowerCo/JV. The VOD/GIP/KKR JV holds an 81.7% VOD stake in Vantage, which in turn will be deconsolidated by Vodafone. This transaction is made at a €32/share price, which represents a premium of 19% to Vantage Tower’s volume-weighted average share price, and a multiple of 26x of adjusted EBITDAaL. This results in turn in a minimum net cash proceed inflow of €3.2B for Vodafone, and this would reduce VOD leverage by around 0.2x, which is the considered use of the cash. The maximum, as calculated, is around €7.1B, which all depends on the take-up of the voluntary offer, and this would reduce VOD leverage by around 0.5x.

VOD IR (VOD IR)

This transaction is expected to close in 1H23.

The impact of this transaction, and because I’m bullish on both the outcome and the specifics of the deal, is part of the reason why I’m currently bullish on, and am buying shares in Vodafone. The company is set to generate a substantial upfront cash amount, followed by a JV ownership of around 50%. Some argue that VOD should have kept the towers, given the value these assets hold. I respect the stance, but I consider this a good solution in an environment where delevering and focusing on the company’s capital stack in a rising interest rate environment is key.

So, I’m positive here on this transaction – and by the way, iREIT covered-REIT CyrusOne (CONE) is part of the transaction as well.

VOD IR (VOD IR)

This transaction is good news for shareholders focused on value creation – because it turns Vodafone into a more asset-light, service-oriented business that can focus more on its growth vectors in these, and emerging geographies.

One of the reasons why Vodafone is pressured in today’s markets is the mix of risky exposures and somewhat underperforming geographies and segments it has in its portfolio. It’s similar to Telenor in that way, which has to contend with its Asia exposures while legacy Scandinavia overall works pretty well.

And I would overall agree – that Vodafone isn’t the highest-quality business in terms of Telcos, or even the safest – however, there are developments when taken in the light of the company’s current development, that puts this company in a very attractive situation.

Let me show you what I mean.

Vodafone’s valuation – very cheap without real justification

Now, I’m not saying there aren’t reasons for Vodafone to be “cheap”. I’m saying that the current level lacks justification.

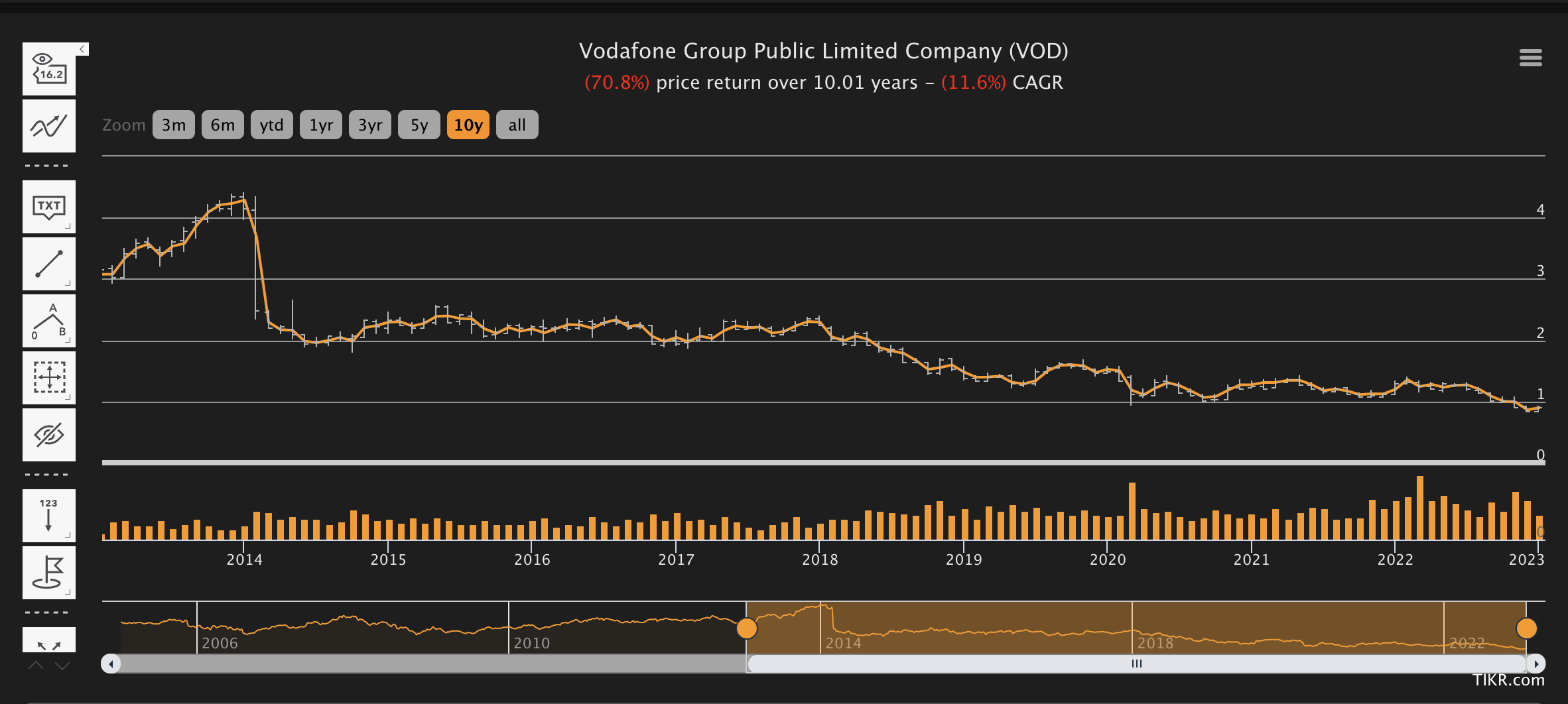

Here’s the company’s 10-year development.

Vodafone Share price (TIKR.com)

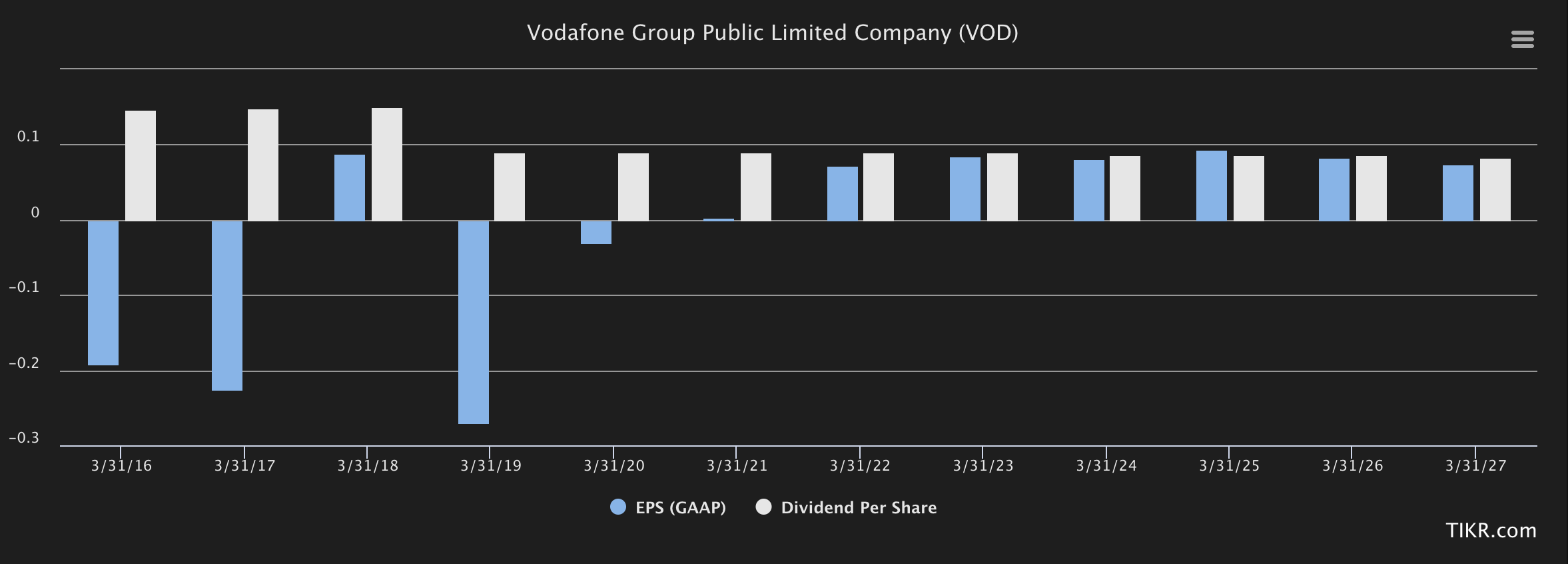

That this would scare some people off is understandable – but keep in mind the company has been deconsolidating and shifting its portfolio during most of this time, which has led to some massive GAAP losses. However, current forecasts are telling us that there is a turnaround that’s finally about to bring some stability to the table.

VOD EPS/Dividend forecast (TIKR.com)

Now it’s understandable that a company that pays a dividend not covered by earnings would be punished by the market. However, it’s my stance that a turnaround here will bring stability and reversion to the company’s valuation. The way I model for Vodafone’s growth and its measures to reduce both leverage and efficiencies calls for an EPS of about £0.08-£0.1 for the next few years, with sensitivity tables and potential growth rates allowing for above that as well. Also, remember that this is GAAP. In terms of FCF, the company has been able to generate positive FCF for every single year since 2016, at double-digit margins.

I’ve already told you the company’s peer group – and compared to almost every single peer, the company is trading at substantial P/E, EBITDA, and revenue discounts. The latest native share price is £0.92/share, which is below 10x P/E, below 6.5x EBITDA and below 2x Revenue, while most peers are closer to twice that in revenues, and at least above 10-12x in P/E. Vodafone is currently trading at less than 0.7x to sales, and this is despite a growing sales number. When you consider that Vodafone is more used to trading at sales multiples of 1.4x, then half of that starts to look like an overreaction.

Vodafone’s historical, 12-year NTM P/E is around 23.2x. It was once a very highly-considered business, that crashed down to earth in a bout of mismanagement and challenges the company did not handle well. However, at a current NTM P/E of 9.5x, the company is being severely underappreciated for what earnings are about to come Vodafone’s way. Even just stability in earnings would, as I see it, be worth around 10-13x P/E here. Remember, Vodafone’s native yield is above 8% – and that yield is covered and “confirmed”.

19 analysts follow Vodafone’s native share. 12 of them consider the company a version of “BUY”, Outperform or positive here, with a range going from £0.89 to £2.44. Even the most conservative valuation here almost puts the company cheap enough at this time – and while I can see what numbers the analyst applied to reach that target, it’s one I would call excessively negative, and not account properly for either Vantage or the current service growth rates.

The average from analysts for Vodafone is around £1.45. This implies an upside of over 35% for Vodafone, and it’s generally a direction I agree with. I would go lower by a bit and go for £1.3/share to account for some of the risks – but the upside is still double-digits here.

What I am saying in this article is that Vodafone isn’t the safest or “best” company in the Telco sector, but at this time, there’s an excessive and massive discount applied to the company’s valuation, which this time is “too much”.

For that reason, this is my current thesis on Vodafone.

Thesis

- Vodafone is a qualitative, Europe-covering Telco with an African growth vector. The company has a very good yield, and at this valuation, has an upside that goes well into the double digits even without substantially outperforming peers or its expectations.

- The company is cheap here, less than £1/share and below 10x P/E, for a world-leading Telco.

- My PT for the company is £1.3, meaning a “BUY”.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

I would say that Vodafone fulfills all of my demands here – I’m LONG VOD, and I say it’s time for you to consider the same.

Be the first to comment