nopparit/iStock via Getty Images

Today I’d like to introduce the first entry into a long term value portfolio that I’m building. Long time readers know that I’ve often been short stocks, but a number of sectors have dropped significantly enough in the past 18 to 24 months to where I now believe it’s appropriate to begin accumulating some stocks for the long term. Today’s entry is Vir Biotechnology (NASDAQ:VIR) whose stock has dropped substantially over the past 18 months on general market malaise as well as specific worries that its Covid-19 revenues aren’t sustainable. The drop seems excessive to me given the company’s growing revenues, its multiple therapeutic programs and its important partnerships with major pharmaceuticals and foundations like the Bill and Melinda Gates Foundation. Let’s dive in.

Vir Biotechnology

VIR is a company aimed at eradicating infectious diseases. Its current programs are all in the virology space, with candidate treatments for Covid-19, Hepatitis B, Influenza and HIV. As the company puts it:

Our approach begins with identifying the limitations of the immune system in combating a particular pathogen, the vulnerabilities of that pathogen and the reasons why previous approaches have failed. We then bring to bear powerful technologies that we believe, individually or in combination, will lead to effective therapies.

Pipeline

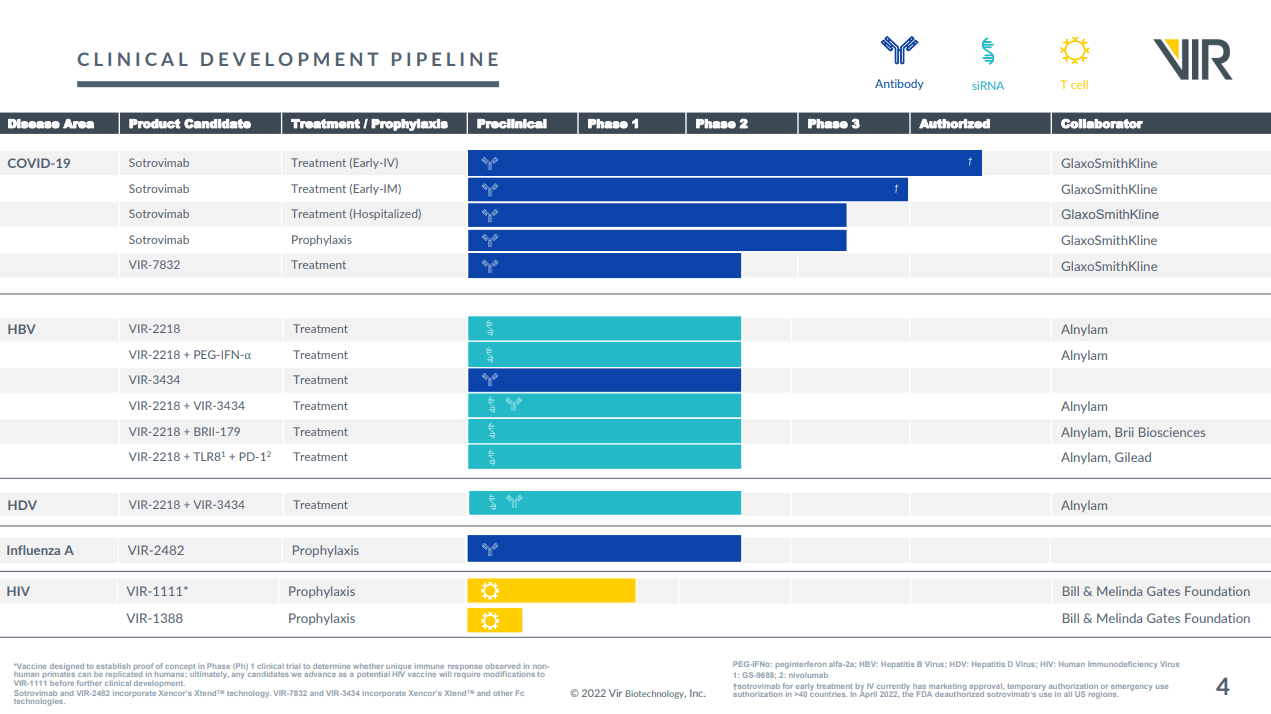

The company has a robust and well partnered pipeline, as shown in the most recent investor presentation.

Investor presentation

Covid-19

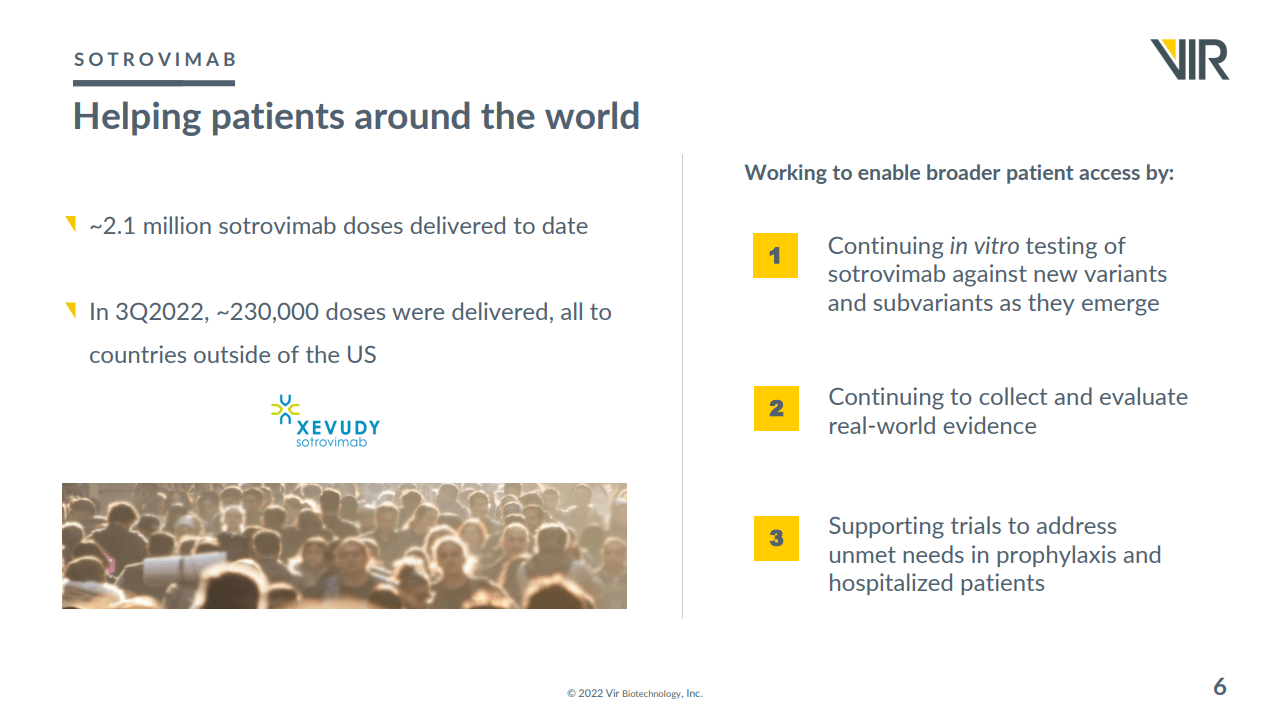

VIR has partnered its Covid-19 program with GSK (GSK), a company with an EV of $87.9B. It has an approved treatment, Xevudy (Sotrovimab), which is also being tested for further uses in Covid-19 including prophylaxis. It also has a second treatment option, VIR-7832, in Phase II clinical trials.

Sotrovimab is the company’s only current source of revenue, most of which has come from outside of the US. Here is a slide summarizing this.

Investor presentation

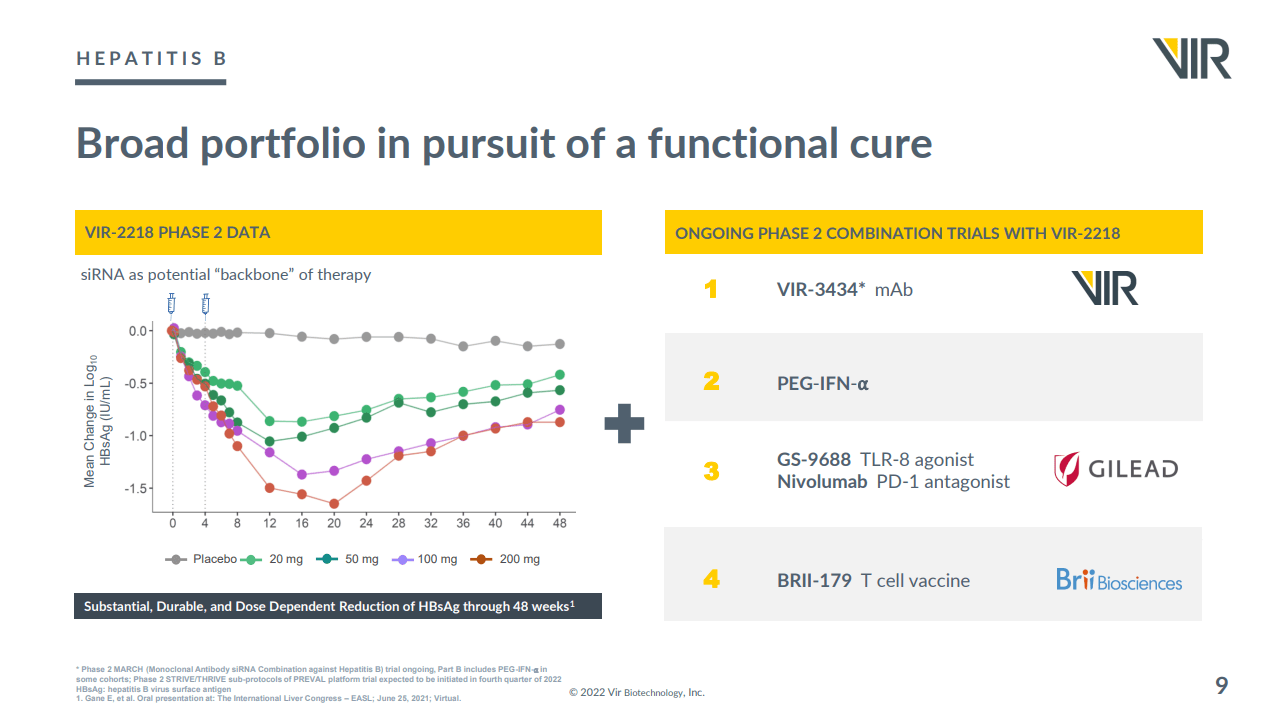

Hepatitis B (HBV)

VIR’s main partner for its lead HBV drug is Alnylam (ALNY) which is a company with an enterprise value of $26.7B. However it also has multiple partners who are using VIR’s VIR-2218 in combination trials. Here’s a summary slide showing this. Note that all of the HBV work is in Phase II clinical trials.

Investor presentation

Furthermore the combination of VIR-2218 and VIR-3434 (a monoclonal antibody) is also being studied in HDV.

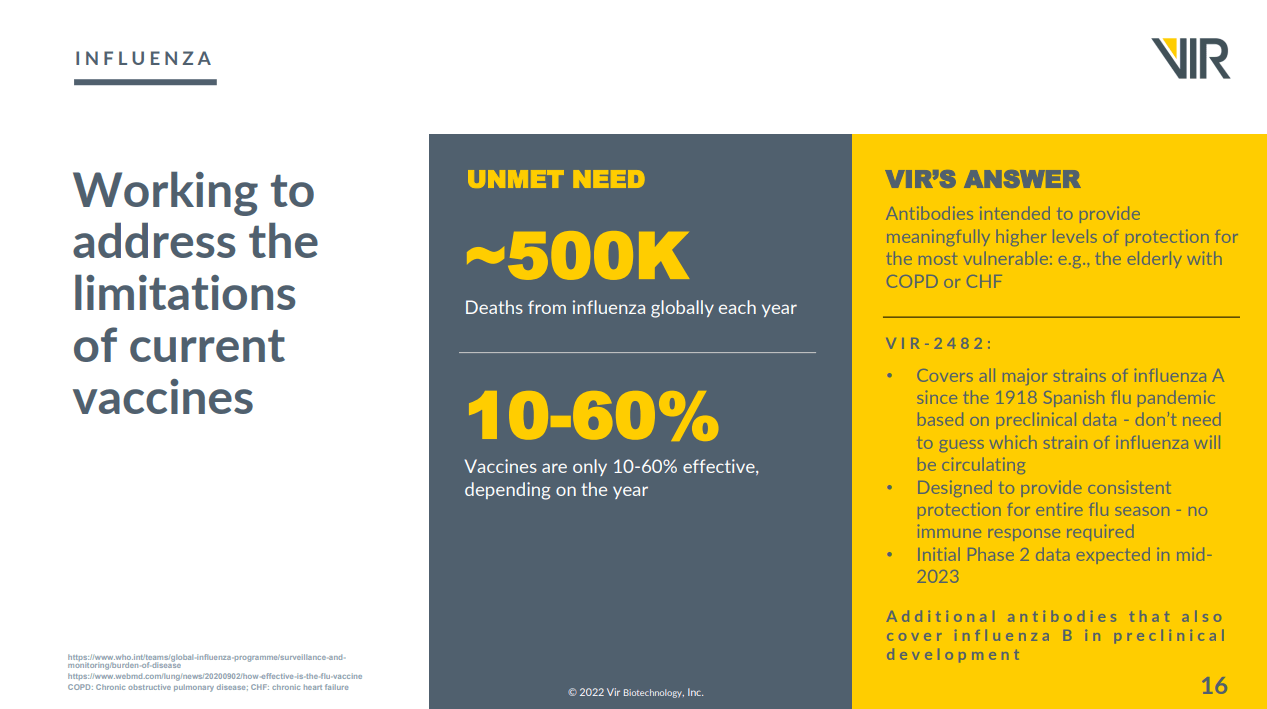

Influenza A

VIR is going it alone in Influenza, and is in Phase II trials with VIR-2482. Here’s the opportunity it sees:

Investor presentation

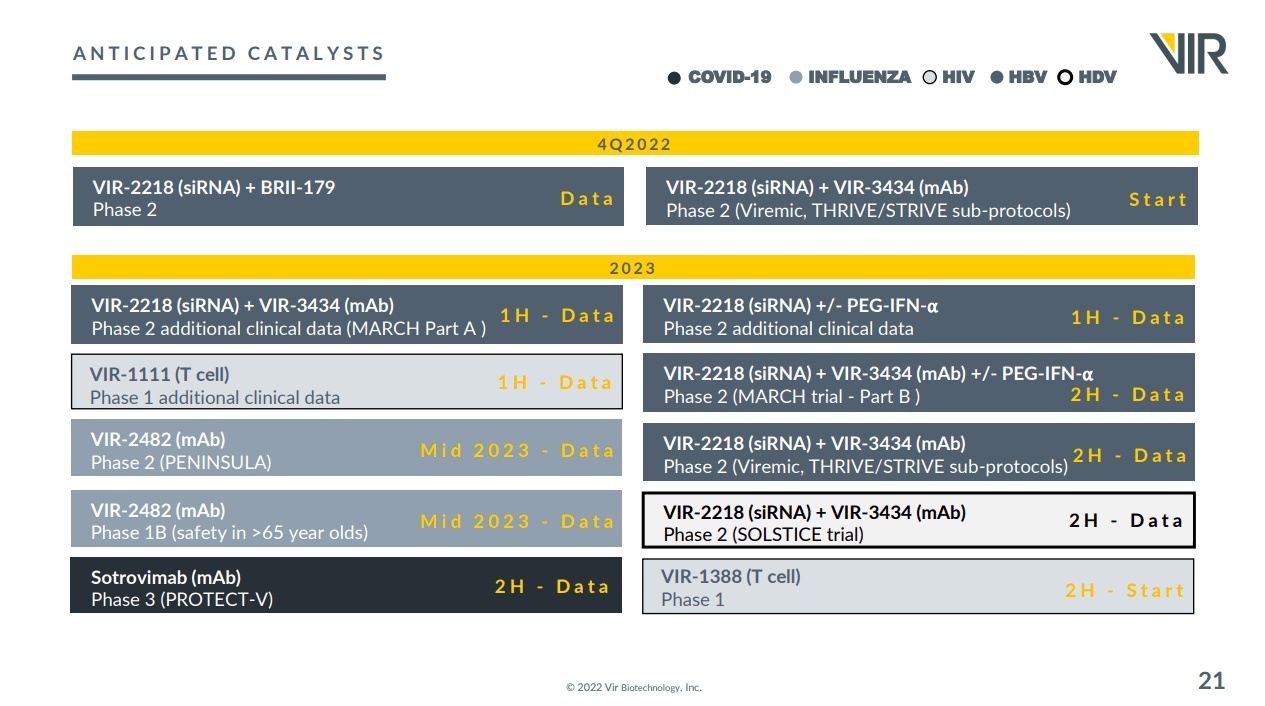

Upcoming Milestones / Catalysts

With several partnered programs, it is not surprising that VIR’s calendar is full of upcoming events. In particular it expects to see Phase II data from HBV, HDV and influenza in 2023, as well as Phase III data in Covid-19 prophylaxis. The best source for the latter trial, is directly at the clinicaltrials.gov site which includes this helpful summary (my emphasis):

PROTECT-V is a platform trial to test prophylactic interventions against SARS-CoV2 infection in vulnerable patient populations at particularly high risk of COVID-19 and its complications, seeking to identify treatments that either might prevent the disease from occurring or may reduce the number of cases where the disease becomes serious or life-threatening.

In PROTECT-V, multiple agents can be evaluated on the same platform across vulnerable populations, with the option of adding additional treatments at later time points as these become available. The expectation is for as many sites as possible to recruit to all available trial treatments at any time, however, the platform structure and randomisation/data collection systems allow sites to open the trial treatment arms according to their capacity.

The trial opened with intranasal niclosamide and matched placebo, aiming to recruit 1500 vulnerable renal patients in February 2021. A parallel study protocol, will be conducted in India, sponsored by The George Institute. Recruitment of approximately 750 Indian patients will commence in February 2022.

The second agent, intranasal and inhaled ciclesonide and matched placebo, will be added to the platform in early 2022 in the same renal patient population.

Sotrovimab and matched placebo will be added to the platform in early 2022 in patients who have mounted sub-optimal vaccine responses to vaccines against SARS CoV-2.

Investor presentation

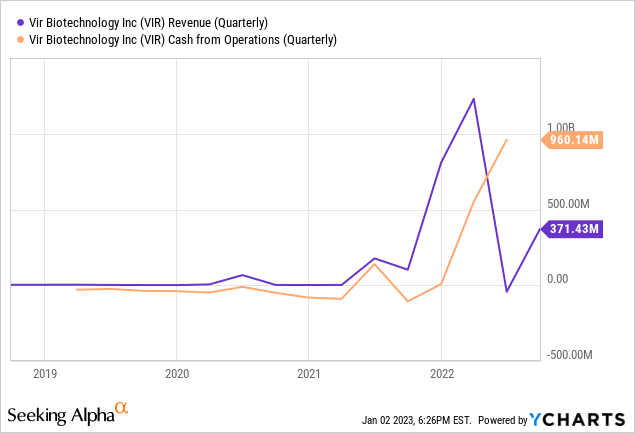

Financial Performance

Thanks to profit sharing with GSK in the sales of Xevudy the company is (currently) solidly cash flow positive.

The question, of course, is whether that will remain as Covid-19 tapers off and as more treatments come on to the market. So far, however, reports of Xevudy’s demise have been greatly exaggerated. See for example this report from November which includes these bullets (with my emphasis):

- Vir Biotechnology (NASDAQ:VIR) on Thursday reported a big Q3 beat on both top and bottom line, as a surge in revenue from the company’s collaboration with GSK helped overall revenue more than double Y/Y.

- VIR’s overall quarterly revenue was also helped by a $17.9M net reversal of the non-cash charge recognized in Q2 for potential write-offs related to excess sotrovimab supply and manufacturing capacity against uncertain future pandemic demand.

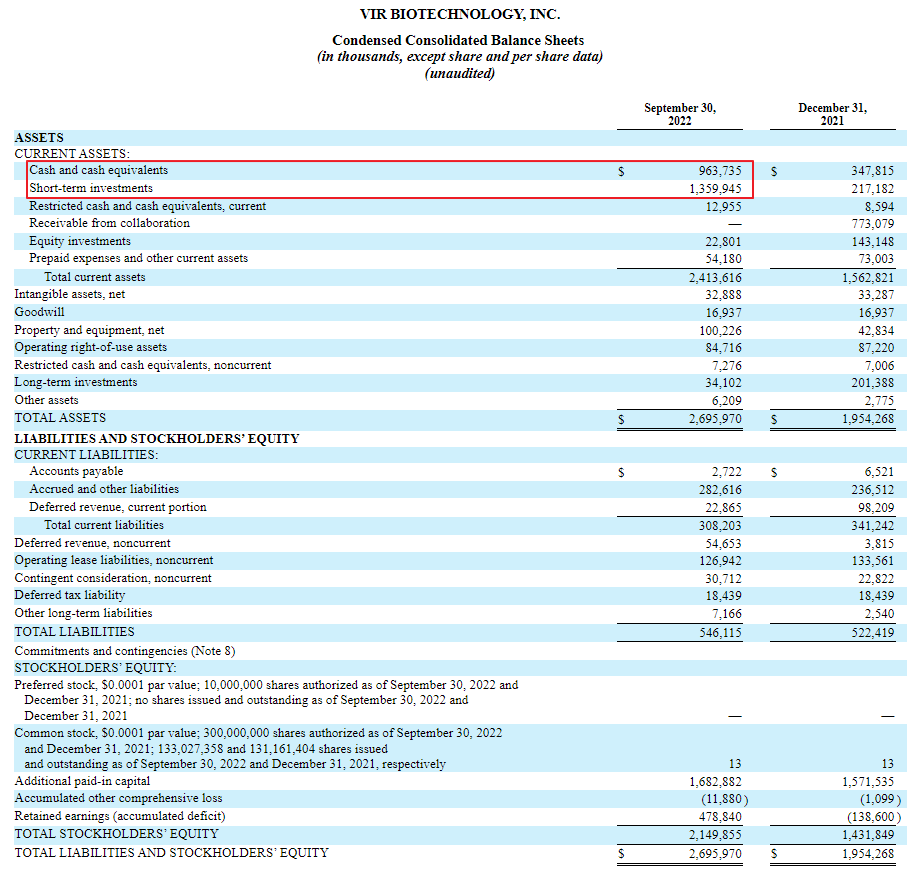

Cash on Hand

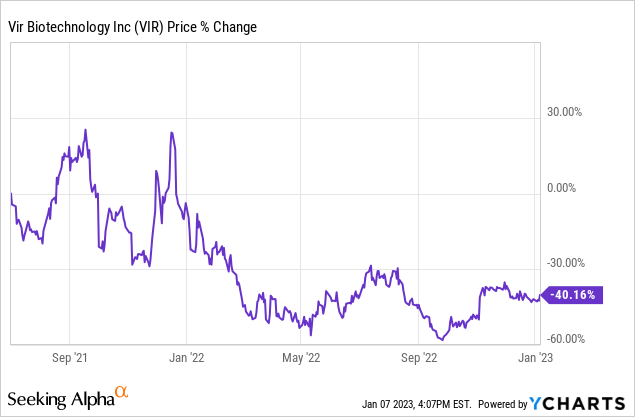

As of September 30, 2022, VIR had $963M in cash and cash equivalents and an additional $1,360M in short term investments on its balance sheet. With 133.1M shares outstanding that means the company has about $17.45 of cash and short term investments per share. With the stock trading at $26.05 this means that two thirds of the stock price is cash and short term investments. I believe this greatly reduces the risk of buying the stock at today’s prices.

sec.gov

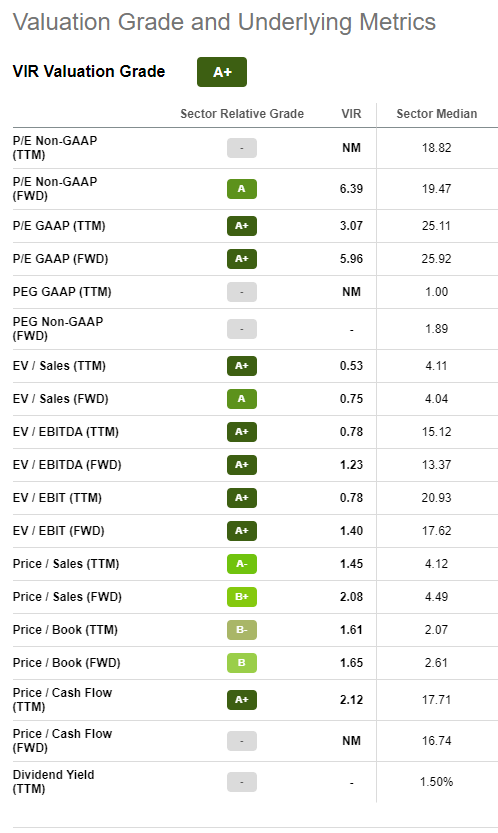

Valuation

Thanks to Seeking Alpha’s handy summary, we see that VIR is extremely attractive on most valuation measures including EV/EBIT, EV/Sales and GAAP P/E’s. This is one of the principal reasons for which I have made VIR the first entry in my long term value portfolio.

Seeking Alpha

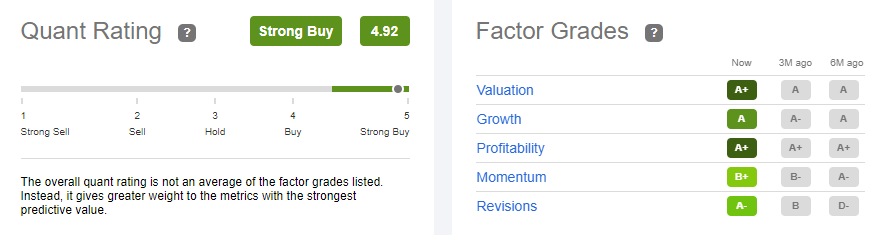

Quant Ratings

Seeking Alpha currently rates VIR as a “strong buy” with an almost perfect quant rating of 4.92. I fully agree with this appraisal and am particularly focused on the A+ ratings for valuation & profitability and the A rating for growth.

Seeking Alpha

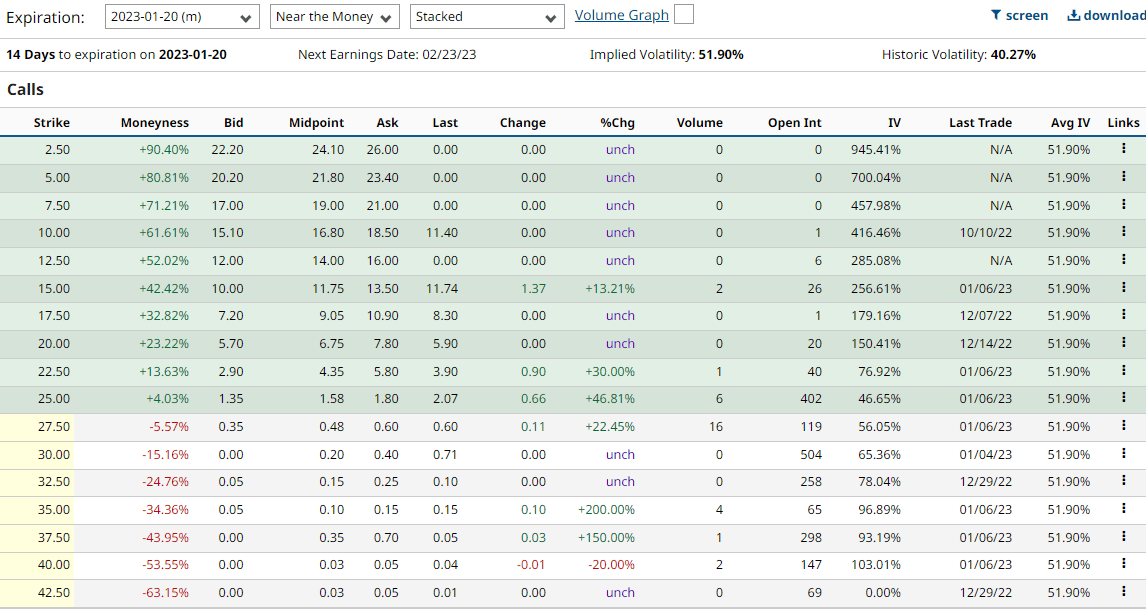

Options

VIR trades options so it can be used in strategies like covered call writing or calendar spreads. However the open interest is not particularly large so that the options won’t be as liquid as they are for more popular stocks.

barchart.com

Risks

VIR is a biotechnology company with all of the attendant risks including the risk of failed trials and new safety issues / side effects.

The biggest specific risk with VIR is that GSK’s sales of Xevudy will fall rapidly if Covid wanes around the world. However news out of China and elsewhere make me think this risk is one worth bearing. VIR’s cash and short term investments on hand also somewhat mitigate this risk in my eyes.

Summary

I have taken a full position in VIR which I intend to hold for the long term. One way I will be monitoring it will be to keep an eye on its quant rating; and should this fall to “hold” or lower I may revisit my holding, perhaps selling a portion or even all of it.

Be the first to comment