Ivan Grabilin

VICI Properties (NYSE:VICI) is a well-managed net lease real estate investment trust that provides stable dividend income, a low pay-out ratio, and inflation protection to passive income investors.

Even though inflation is slowing, I believe owning a REIT that provides a hedge against income depreciation is a wise investment.

In addition, VICI Properties has a low dividend pay-out ratio based on adjusted funds from operations, and the dividend is growing in the high single digits year after year.

An Entertainment-Focused Net Lease REIT

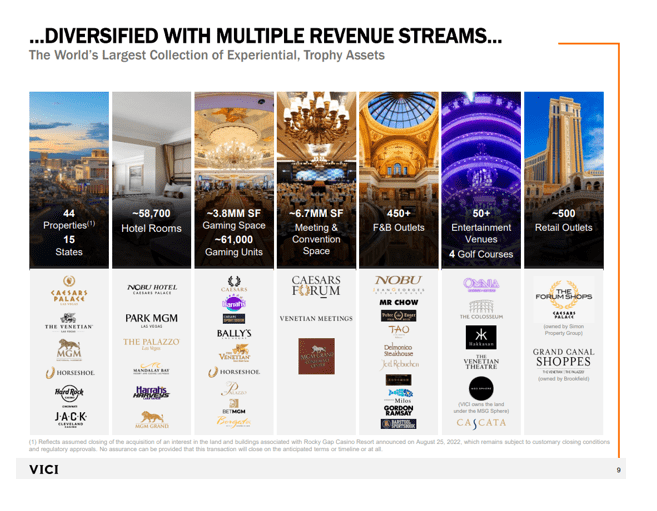

VICI Properties is a real estate investment trust that gives investors access to experiential properties like casinos, hotels, convention space, entertainment venues, and (retail) outlets. The portfolio of the REIT includes 44 experiential properties and trust properties in 15 states.

Unlike other net lease REITs, VICI Properties is entirely focused on the experiential niche in markets with high barriers to entry, such as Las Vegas, which accounts for 55% of the trust’s total square footage. As of the end of the third quarter, VICI Properties’ real estate portfolio was completely occupied.

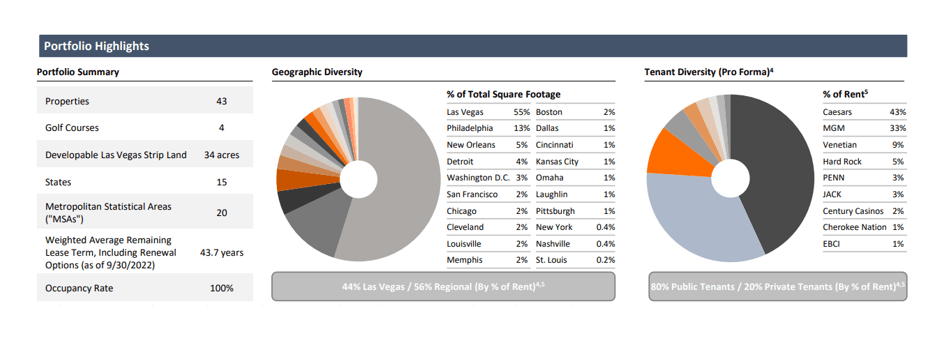

Portfolio Summary (VICI Properties)

Operator Concentration

As a major owner of casino properties, VICI Properties counts the largest and most well-known casino brands as its customers. The trust’s two largest tenants, Caesars Entertainment and MGM Resorts, account for 76% of the company’s annual cash rent.

VICI Properties has very high tenant concentration as a result of the trust’s real estate’s uniqueness, with the two largest tenants accounting for more than three quarters of annualized rental income. Having said that, the portfolio is fully performing, and VICI Properties has had no cash collection issues in recent years.

Portfolio Highlights (VICI Properties)

Inflation Protection

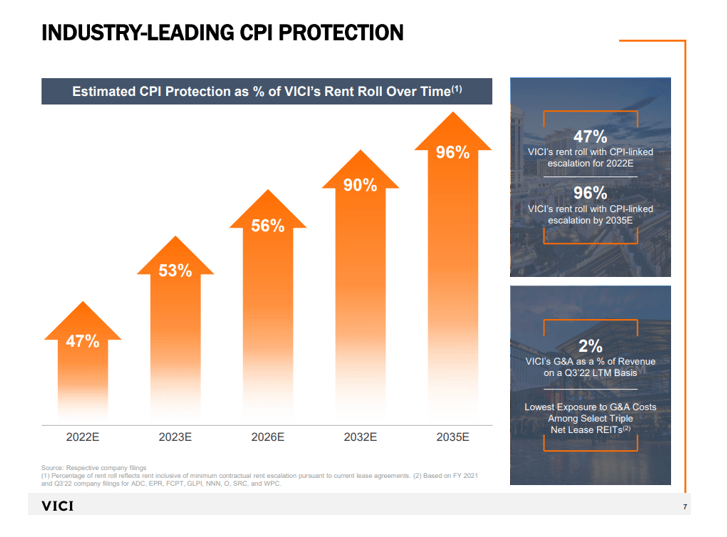

Leases from VICI Properties provide cash flow protection because the real estate investment trust links rental rates to changes in the consumer price index, which passive income investors concerned about the state of inflation will undoubtedly appreciate.

In FY 2022, roughly half of the REIT’s leases have rent escalation triggers tied to consumer price increases.

Moving forward, it is a top priority for VICI Properties to significantly increase the amount of rental income that is tied to the Consumer Price Index.

Estimated CPI Protection (VICI Properties)

Pay-Out Ratio And Dividend Growth

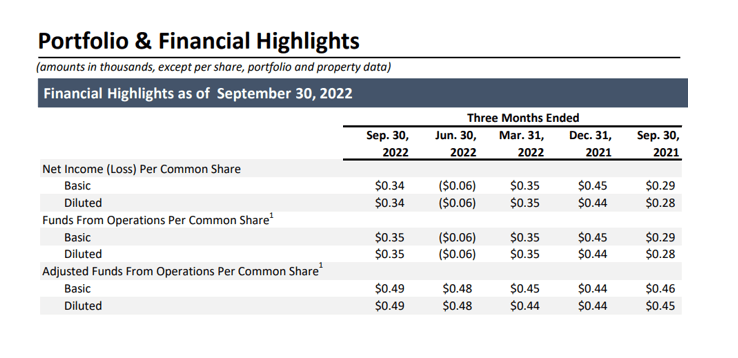

In the third quarter, VICI Properties earned $0.49 per share in adjusted funds from operations, while the trust paid out $0.39 per share in dividends. The implied dividend pay-out ratio in the most recent quarter was thus around 80%, which also holds up over time.

VICI Properties, for example, had a pay-out ratio of 78% over the last twelve months, indicating that the dividend is indeed very well covered by adjusted funds from operations.

Financial Highlights (VICI Properties)

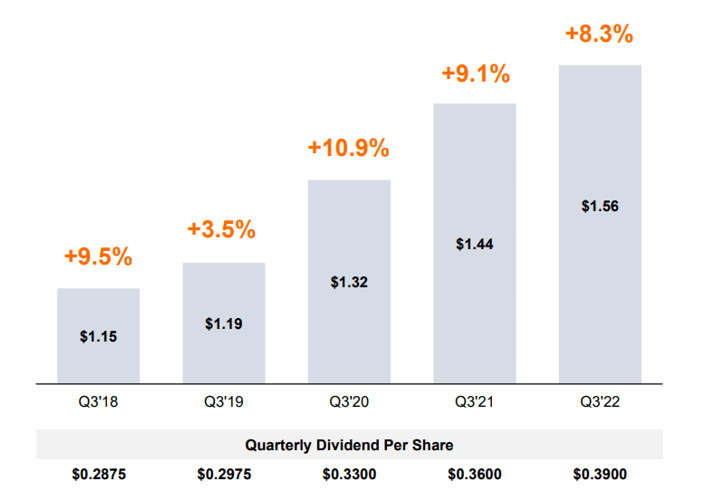

VICI Properties’ good dividend coverage based on adjusted funds from operations has allowed the trust to rapidly increase its dividend. VICI Properties increased its dividend payout by 8% per year on average between the third quarter of 2018 and the third quarter of 2022. The current quarterly dividend payment is $0.39 per share, resulting in a dividend yield of 4.52% at a price of $34.51.

Quarterly Dividend Per Share (VICI Properties)

VICI Is Trading At An Attractive AFFO Multiple

VICI Properties could easily achieve adjusted funds from operations of $2.20-$2.30 per share in 2024, resulting in an AFFO-multiple of 15.3x.

VICI Properties could earn around $2.00 per share in adjusted funds from operations in 2022.

Given that VICI Properties’ dividend is growing at a high single-digit annual rate, I believe the AFFO-multiple is quite appealing and even reflects a moderate margin of safety.

Why VICI Properties Could See A Lower/Higher Valuation

If VICI Properties has a flaw, it is that the company lacks proper diversification due to the nature of its business model. Even though they do not operate in the experiential sub-sector, other net lease REITs such as W.P. Carey (WPC) or Realty Income Corporation (O) offer better diversification and, at the end of the day, a safer dividend.

If there is a recession, especially in Las Vegas, VICI Properties’ funds from operations may be reduced.

My Conclusion

VICI Properties is a promising net lease real estate investment trust that profits from high barriers to entry in the experiential sector. The portfolio is performing well and is fully occupied.

The trust also earns its dividend from adjusted funds from operations, and the pay-out ratio is low enough to indicate that the dividend has the potential to grow in the future.

The 4.5% dividend is certainly appealing to passive income investors, as is the REIT’s ability to protect its cash flow from inflation.

Be the first to comment