BeritK

Investment Thesis

The Vanguard U.S. Multifactor Fund ETF (BATS:VFMF) is a broad-based large-cap blend ETF selecting high-quality stocks with strong recent price momentum trading at low valuations. It’s a classic deep-value fund with a momentum overlay, but all ETFs following this strategy have something in common: high volatility. This feature makes VFMF inappropriate for the average investor. Furthermore, VFMF’s active fund managers have not proven their approach works based on performance since its February 2018 launch. Therefore, I don’t recommend investors buy VFMF, and I look forward to explaining why in further detail below.

ETF Overview

Strategy Discussion

VFMF is an actively-managed fund following a proprietary strategy, but the fund’s prospectus and fund overview page provide some insight into the selection process. Here are some of the highlights:

- the advisor aims to select stocks with relatively strong performance, strong fundamentals, and low prices

- the advisor uses a quantitative model to evaluate all U.S. large-, mid-, and small-cap stocks and retains discretion over the selections

- the initial screen reduces exposure to more volatile and less liquid stocks

- remaining stocks are ranked according to recent performance (momentum), strong fundamentals (quality), and price relative to fundamentals (valuation)

- rebalances occur as needed

These investment objectives are admirable but are challenging to achieve. While several active and passively managed broad-based ETFs aim to combine momentum, quality, and valuation, none score well on volatility. There’s always at least one major sacrifice, and as I’ll discuss later, VFMF’s current selections are pretty volatile.

Sector Exposures and Top Ten Holdings

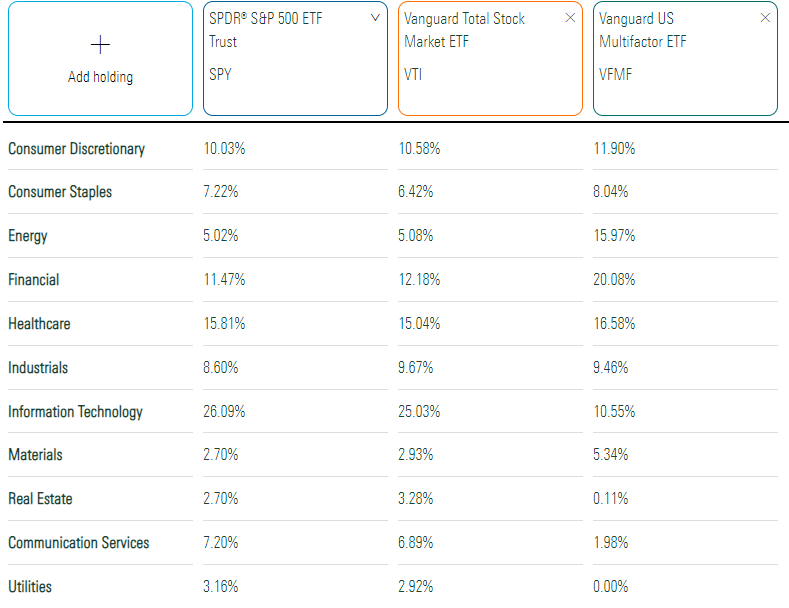

VFMF’s sector exposures are listed below alongside the SPDR S&P 500 ETF (SPY) and the Vanguard Total Stock Market ETF (VTI). The latter is the most applicable benchmark, as VFMF’s selection universe covers small, mid, and large-cap stocks.

Morningstar

Most factor ETFs, including VFMF, currently underweight the Technology sector because their valuations remain high. As discussed in this recent article on the Vanguard Value ETF (VTV), growth expectations are also questionable, but VFMF still has a healthy 10.55% exposure to this sector. Energy is significantly overweight (15.97%), as is Financials (20.08%). Compared to VTI, the remaining sector exposures are relatively minor. I also consider the zero exposure to the Utilities sector a big miss. As investors and analysts alike felt Utilities stocks were too expensive and not fit to compete with rising interest rates, I discussed the importance of owning the sector earlier this year. It’s held up remarkably well and is the easiest way to reduce a portfolio’s volatility, which VFMF surely needs.

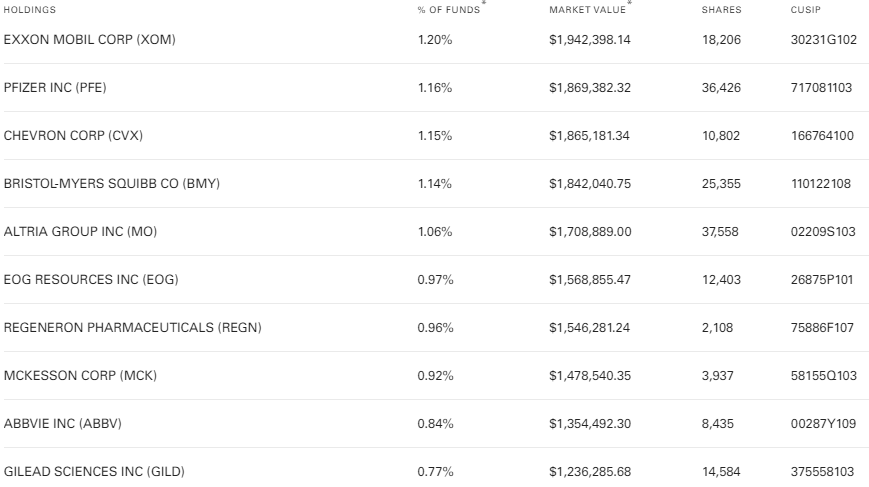

VFMF’s top ten holdings are below, led by Exxon Mobil (XOM), Pfizer (PFE), and Chevron (CVX). You’ll notice most of these companies are firmly in the large-cap territory.

Vanguard

That might be a coincidence that indicates the manager’s current preference for large-cap stocks. However, a look back at the holdings as of November 30, 2021, highlights a similar pattern. Here are the top holdings in each sector and their current market caps, according to the latest annual report.

- Communication Services: Lumen Technologies (LUMN) – $5.46 billion

- Consumer Discretionary: Target (TGT) – $65.94 billion

- Consumer Staples: Philip Morris (PM) – $156.45 billion

- Energy: EOG Resources (EOG) – $74.30 billion

- Financials: JPMorgan Chase (JPM) – $383.34 billion

- Health Care: Pfizer (PFE) – $288.08 billion

- Industrials: Northrop Grumman (NOC) – $81.51 billion

- Materials: Freeport-McMoRan (FCX) – $54.03 billion

- Real Estate: CBRE Group (CBRE) – $23.14 billion

- Technology: Alphabet (GOOGL) – $1,160 billion

I’m confident that the manager has a large cap bias, so calling VFMF a total-market-cap blend ETF may be inappropriate. That said, its weighted-average market capitalization is $58.71 billion, slightly low for a large-cap ETF.

Performance Analysis

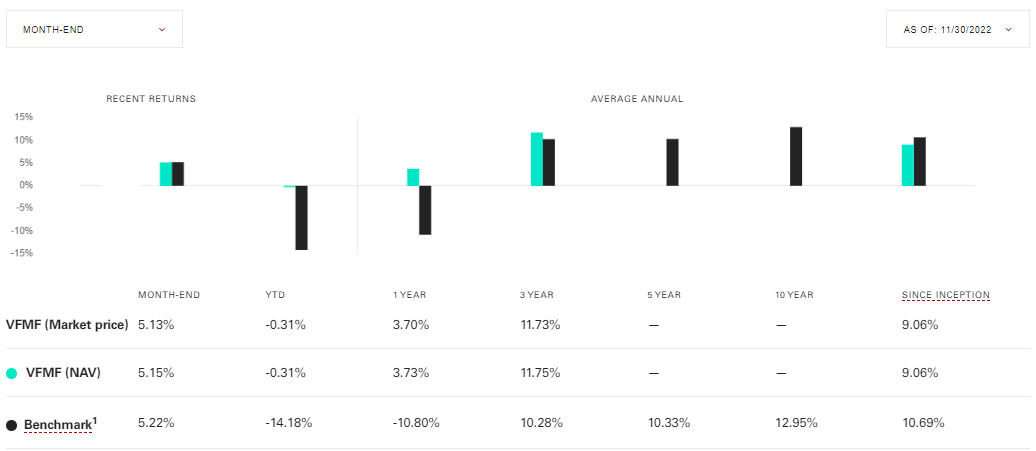

Vanguard provides the following performance information for VFMF relative to its benchmark, the Russell 3000 Index. Since its inception on February 13, 2018, VFMF has gained an annualized 9.06% vs. 10.69% for the benchmark through November 30, 2022.

Vanguard

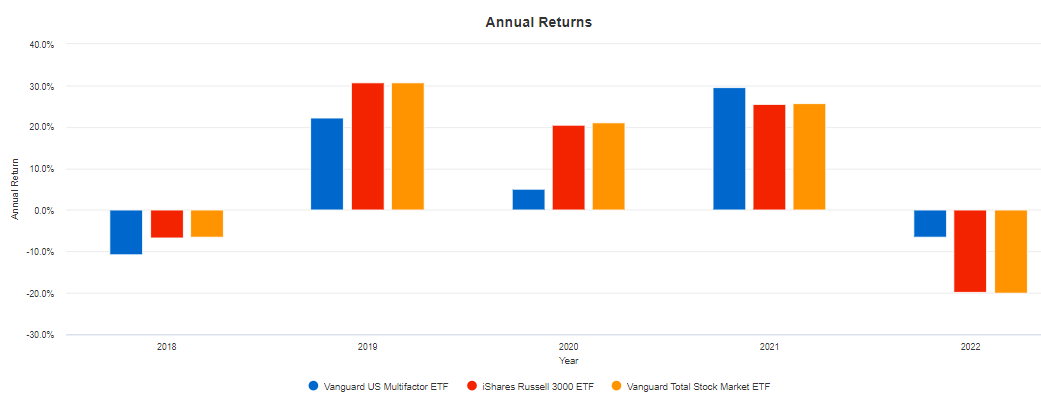

These figures include VFMF’s 14.50% outperformance over the last year (3.70% vs. -10.80%), indicating a terrible start for the fund. Portfolio Visualizer summarizes this nicely. The following graph highlights VFMF’s annual returns compared to the iShares Russell 3000 ETF (IWV) and VTI.

Portfolio Visualizer

In 2018, 2019, and 2020, VFMF underperformed VTI by 4.32%, 8.33%, and 16.02%. Subsequently, in 2021 and 2022, it outperformed by 3.94% and 13.50%. This track record is not impressive and suggests an unwillingness to adapt to market conditions. Investing in deep-value stocks was contrary to the ultra-bullish sentiment in 2020, and I wonder why the momentum screen didn’t improve performance after markets bottomed in Q1 2020. That quarter, VFMF underperformed VTI by 9.15%, then lagged by another 6.28% over the next six months.

ETF Analysis

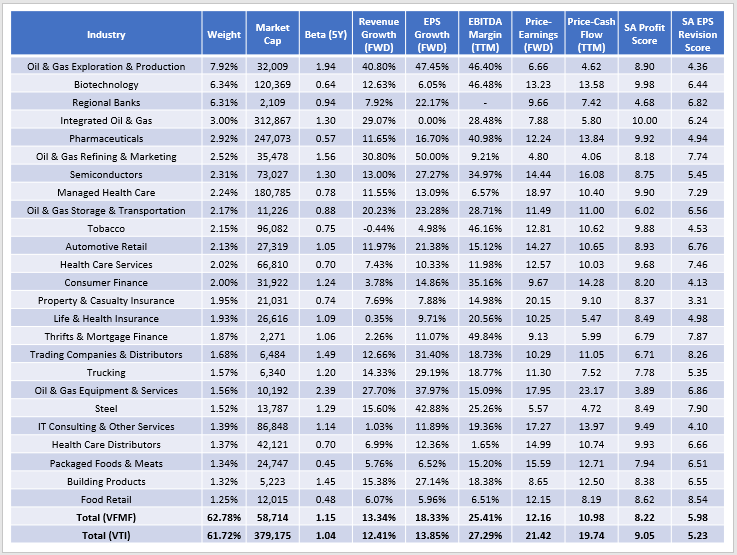

I’ve summarized VFMF’s fundamentals by industry in the table below. The top 25 total 62.78% compared to 61.72% for VTI, making it a well-diversified portfolio. However, its $58.71 billion weighted-average market capitalization is far less than VTI’s $379.18 billion. Fundamentally, you can see the advantages of moving away from mega-cap stocks.

The Sunday Investor

These advantages include a 12.16x forward price-earnings ratio and a 10.98x trailing price-cash flow ratio, roughly nine points less than VTI. These low valuations are commonly found in Oil & Gas, Biotechnology, Regional Banks, and Pharmaceutical stocks, all of which VFMF overweights. VFMF’s average Energy holding is up 67.09% this year compared to 57.77%. Since VFMF overweights this sector by about 11%, it’s been an enormous source of returns. However, in the last month, VFMF’s Energy stocks are down 8.88% on average compared to 8.41% for VTI. Since we have reasonable indications that inflation has peaked, investors should not rely on huge returns for the Energy sector as we advance.

The Energy sector is also a source of tremendous estimated earnings growth, especially among Oil & Gas E&P stocks (47.45%). Given the volatility of oil prices, whether these estimates will materialize is challenging to assess. However, I’m confident that VFMF’s earnings growth will be above VTI’s, so from a growth-at-a-reasonable-price perspective, VFMF looks excellent.

The issue is what investors sacrifice. VFMF’s five-year beta is 1.15 compared to 1.04 for VTI, indicating investors can expect higher volatility. Likely, the volatility risk is even more remarkable because of the above-average Energy allocations, as VFMF only allocated about 9% to the sector last year. A second sacrifice is lower profitability. Seeking Alpha provides Profitability Grades for most U.S. equities, and when weighted and normalized on a ten-point scale, VFMF scores 8.22/10. VTI scores 9.05/10, and market-cap-weighted ETFs like SPY are about 9.42/10. My research, using historical data provided in the Ken French Data Library, indicates investing primarily in highly-profitable companies is the key to long-term success. Deviating away from these companies, as VFMF does, is likely problematic.

On the plus side, VFMF has a relatively strong EPS Revision Grade. Following the same method, VFMF scores 5.98/10 compared to 5.23/10 for VTI. That’s the best part of the portfolio and suggests VFMF may have some solid short-term momentum. However, it may also be short-lived, as the model appears to only screen for recent price momentum rather than forward-looking estimates.

Investment Recommendation

I’m not sold on VFMF’s approach. Early performance was disappointing, and although VFMF outperformed broad-based ETFs like VTI this year, so have most value and dividend-focused funds with cheap valuations. VFMF’s main advantage is that it primarily holds high-growth stocks with solid earnings momentum at low valuations. The disadvantages are its inconsistency, high reliance on the volatile Energy sector, and low overall profitability. Investors will do better with VTI in the long run, so I’ve decided not to recommend VFMF. Thank you for reading, and I look forward to discussing these ETFs and other alternatives in the comments section below.

Be the first to comment