DEEP ETF is a small-cap value fund that is positioned to take out the larger-cap players over the next 10 years. kickers/E+ via Getty Images

If you are in search of an amazingly constructed fund that gives you true exposure to both the size and value premium, then look no further than the Roundhill Acquirers Deep Value ETF (NYSEARCA:DEEP).

Every once in a blue moon I find a fund that is doing everything right. And even more rare is when I find such a fund that is largely undiscovered and unappreciated. I mean, if a fund is doing everything right, shouldn’t it have billions in assets under management? Not necessarily. But I will get to that later.

The Size Premium

Small-caps are generally defined as having a market capitalization of $300 million to $2 billion. There are oodles of small-cap funds in existence. They come in all shapes and flavors. But why would someone invest in small-caps? No doubt because they believe in the size premium. Smaller stocks outperform larger stocks in general.

But the majority of small-cap funds have a glaring flaw. They do something that directly works against the size premium. What is it? And does DEEP have this flaw?

Cap-Weighting Kills the Size Premium

Consider the Vanguard Small-Cap Value ETF (VBR). There are a whopping 882 stocks in the fund. But what are you really getting?

First of all, they say that the median market cap is $5.8 billion. I would say that a median market-cap for a small-cap would be closer to $1 billion. $5.8 billion for a median cap is kind of ridiculous if you call this a small-cap fund. But it gets worse yet again for the size premium. VBR is market-cap weighted.

Cap-weighting is where you weight positions in the fund according to the size. Larger stocks get more weighting. In the case of VBR, the top 40 holdings have a market cap of $7.3 billion to $20 billion. Forget mid-cap status… they are including large-cap stocks. And weighting heavily towards them.

What you are left with is a large number of small-cap stocks in a fund that have very little influence on the actual return. In my view, VBR is anything but a true small-cap fund.

The Problem of Too Much Money

Why do so many small-cap funds push the reasonable limits of market capitalization? Why do they cap-weight to further reduce any size premium? The answer is that they have too much money.

As VBR has $49 billion in assets under management, they have no other option. Can you imagine if they held only 200 small-cap stocks that were truly small? The fund would blow up. Just envision a portfolio manager having to buy $245 million worth of shares in a stock that has a market-cap of $300 million. It is preposterous. The price of the stock would go bananas! To compensate with the burden of too much money, the fund must employ tactics where the true small-cap exposure is little more than sprinkling seasoning on your plate of food.

DEEP Does It Right

And this is where DEEP does it right. It may seem like a small point but it is not. First, look at the market caps of their holdings.

- Smallest stock ESEA with market cap of $134 million

- Largest stock DOOR with market cap of $1.7 billion

YES! Finally! Actual stocks which are small-cap and under. And do they dilute the size premium by weighting towards larger stocks? No, they do not. They equal-weight their positions. They actually try to capture the size premium for their clients.

How to Define Value

In a recent article about the iShares S&P Small-Cap 600 Value ETF (IJS), I discuss my disdain for how iShares defines value. I don’t want to side-rail the discussion on DEEP, but IJS looks for value traps. They focus on value stocks which have slowing growth and low price momentum. Those are the type of value stocks I tend to avoid.

DEEP defines value using a fairly simple method that is rather effective called the Acquirer’s Multiple. In layman’s terms, the Acquirer’s Multiple is a better and improved version of the price-to-earnings ratio. What makes it better?

The Acquirer’s Multiple

The PE ratio uses market capitalization as one of the inputs. Many prefer to use Enterprise Value instead. EV includes things like debt and cash. If you do not consider the debt, your valuation ratios may be skewed. What looks like good value may not be.

Take the stock Diebold (DBD). The market capitalization is at $114 million as of time of writing. You might analyze the price to sales of 0.03 and think this is a bargain beyond your wildest dreams. But once you realize that the Enterprise Value is $2.4 billion and your price to sales ratio is 0.68, you need to re-think your thesis.

The second aspect of the Acquirer’s Multiple is to use Operating Earnings (or Operating Income After Depreciation) instead of EBIT. To explain the benefit of using this approach I will copy and paste directly from The Acquirer’s Multiple website.

Operating earnings is constructed from the top of the income statement down, where EBIT is constructed from the bottom up. Calculating operating earnings from the top down standardizes the metric, making a comparison across companies, industries and sectors possible, and, by excluding special items–earnings that a company does not expect to recur in future years–ensures that these earnings are related only to operations.

Does the Acquirer’s Multiple work as a standalone metric?

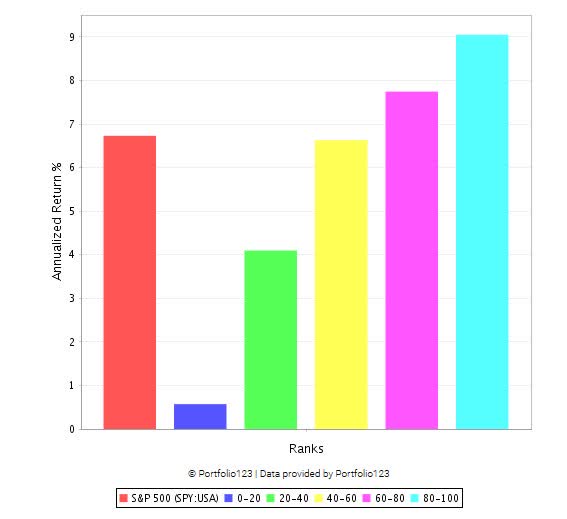

In my personal research it appears to have merit. I ran this multiple across a universe of micro- to small-cap stocks and the lowest ranked group showed only 0.6% annual return since 1999. The highest ranked group had a 9.1% compound annual growth rate. This seems like a reasonable approach for defining value which is also linked to future returns.

portfolio123.com

DEEP Goes Deeper

But the process goes much further than this. The problem with value is that you can still get sucked into value traps. Companies with weak financial circumstances could be trading at a massive discount because the situation is only going to get uglier. To mitigate this, DEEP looks at other aspects of these firms such as:

- Statistical measures of fraud, earnings manipulation and financial distress

My guess is that this would include such things as the Altman Z-Score and the Beneish M-Score.

Each potential stock is examined for a margin of safety:

- Wide discount to a conservative valuation (it is cheap)

- Strong, liquid balance sheet

- Robust business capable of generating free cash flows

DEEP tries to isolate strong and robust stocks that have cash left over at the end of the day and which are trading cheap. These are true value stocks that have a higher chance of appreciating over time.

Free Cash Flows and Small Stocks

This fund really struck on something that makes me feel all warm and fuzzy inside. They look at companies which can generate free cash flows. In all of my exhaustive research on small-cap and micro-cap stocks (and it is extensive), I have not found a single more powerful rule to weed out high-risk small-caps which under-perform the market than to analyze free cash flow. Full stop.

To illustrate, I have created an investable universe of smaller stocks.

- $100K minimum of daily turnover.

- Market capitalization between $100 million and $1 billion.

In this universe, look at stocks which have negative free cash flow for the past quarter and trailing 12 months. Since 1999 this has resulted in a total negative return of -25% or an annualized return of -1.22%.

portfolio123.com

On the other hand, I keep all stocks in the universe that have positive free cash flow for the most recent quarter and trailing 12 months. This has resulted in a total return of 4,288% or 17% annually.

portfolio123.com

How does DEEP stack up? Out of the 100 holdings, 91 of them have either positive free cash flow for the most recent quarter or the trailing 12 months. And 73 of them have positive FCF for both.

Positive Earnings

Another important measure for a fundamentally sound stock is positive earnings. Stocks with positive EBIT over the most recent quarter and trailing 12 months have a historical 19% annualized return since 1999. 97 stocks out of 100 in DEEP have positive earnings in both periods.

Auditing the Value of DEEP

What I sometimes do when analyzing a value fund is perform my own private value rank against their stocks to see if they are actually delivering value or are just saying so. After digging deep into DEEP, I can honestly say that this fund delivers very deep value. Here is my test using my own private value ranking system…

A stock with a value rank of 0 has the worst value and a stock with a rank of 100 has the highest possible value. I analyzed the value ranking of each holding in DEEP and compared it against over 10,000 publicly traded stocks. How do these stocks stack up as regards value?

- 71 of the 100 stocks have a value rank of 90 or higher out of a possible 100 (very deep value)

- 90 of the 100 stocks have a value rank of 70 or higher

And you would naturally expect a few holdings to have a lower value rank. Stock prices and fundamentals change between rebalance points. Overall, I am very impressed that they are delivering true value.

Performance of DEEP

If small-cap value has such big historic returns, why is DEEP not out-performing by a wide margin when looking backwards at the equity curve?

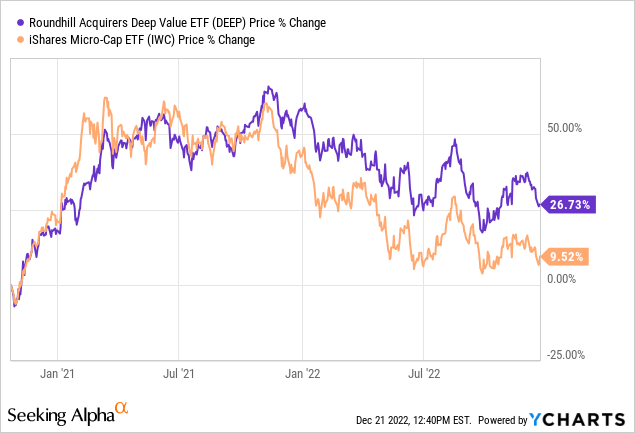

On June 22, 2020, the fund (formerly known as DVP) changed. It used to be a large-cap fund tracking a large-cap index. But it changed its methodology. Effective October 23, 2020 it began to track small-cap stocks. Therefore, anything before October 23, 2020 has no relation to the small-cap value premium. Disregard it. It is not relevant to what the fund is doing today.

This chart below shows you how DEEPs intelligent creation of a small-cap value fund beats its microcap benchmark since October 23, 2020. I expect this gap to only widen with time.

Based on my research, the type of strategy used by DEEP has generated a 15% gross annual return since 1999. Contrast this with an annual return of 6.78% of IWC. The long-term historic out-performance of a strategy that DEEP is employing has been 8.2% above its benchmark. This is according to my own personal research and is my personal viewpoint.

Risks

What are the risks?

- Small-cap stocks might underperform.

- Value stocks might underperform.

For example, my own research has shown that a similar style of small-cap value has zero returns from 2017 to 2021 while the Russell Microcap Index had a total return of 43%. To be fair, this is highly unusual and without precedent in the markets and time periods I have access to. But you should be prepared for the possibility that small-cap value could temporarily go out of favor again. Perhaps investors prefer large growth stocks like the tech boom we saw over the past decade. However, my experience is that fads come and go and undervalued small stocks will persist if you invest for many years. My message to you is to be a long-term investor. Put your confidence in what has generally worked for the majority of the years and decades. Don’t chase the latest fad. Small-cap value… true small-cap value… is where it is at.

Final Word

I work as a consultant for ETFs and funds. My specialty is small-cap and micro-cap stocks. I love value. If I was to design my perfect small-cap fund, it would be exceedingly similar to DEEP. I agree with how they weight the fund, the number of positions and, most importantly, their methodology.

If I was to make an educated guess as to how DEEP will perform 10 years from now compared to a broad micro-cap benchmark like IWC, I would think that after fees this fund should out-perform by at least 5% annually. Excess returns above a benchmark could be as high as 10% annually over the long-term or better. I know that seems high but historically this type of strategy has delivered those kinds of excess returns. But I could also be wrong. This is my own opinion based on my personal experience in this field of work.

Keep in mind that small-cap value has been depressed for the past decade. If small and value come back into favor for the following decade, I would expect DEEP to be one of the best positioned funds to take advantage of it.

The other risk I see is if too much money floods into this fund. At some point, the funds capital starts to erode returns in smaller stocks. Maybe when this fund reaches $300 million, they will need to brainstorm ideas on how to efficiently deploy capital without impacting stocks too much. My suggestion would be to create a series of funds that have different rebalance points with slightly different processes. Similar enough to retain the intelligent way they harvest the small-cap value premium but not so similar that they are investing in identical stocks at exactly the same time. Because if they become too successful, they will have the burden of too much AUM in a single strategy.

But as it stands today, this is the fund I would recommend for any investor wanting to take advantage of the small-cap value premium. Actually, I would recommend most investors to have exposure to this fund. The only reason I am not invested is that this is my line of work. I still have the belief that I can add a little incremental value by investing in single stocks on my own. Time will tell if I should have just placed my capital in DEEP instead of trying to think I might earn a marginally higher return doing it myself.

The expense ratio of 0.8%? Compared to how it is built and what it has the potential to do, that’s deep value for you. To be honest, it would still have a strong buy recommendation at 1.5% expense. You can shop and get a low expense ratio under 0.1% but you won’t find a true small-cap value fund that has the potential to deliver 2x the benchmark return like this one. I give you my word on that.

If I were to recommend one fund to investors to hold over the next 10 years, it would be DEEP. I cannot put it any other way or state it more clearly than this. I have no connection to this fund at all. It’s just a great fund and deserves far more credit than the current AUM is giving it.

Be the first to comment