wacomka

Vertex Pharmaceuticals (NASDAQ:VRTX) focused on investing in scientific innovation to create transformative medicines for people with serious diseases, specifically in specialty markets. Vertex’s R&D claims to be designed to generate disproportionate success and has led to the launch of four medicines in cystic fibrosis.

Serious Diseases Programs

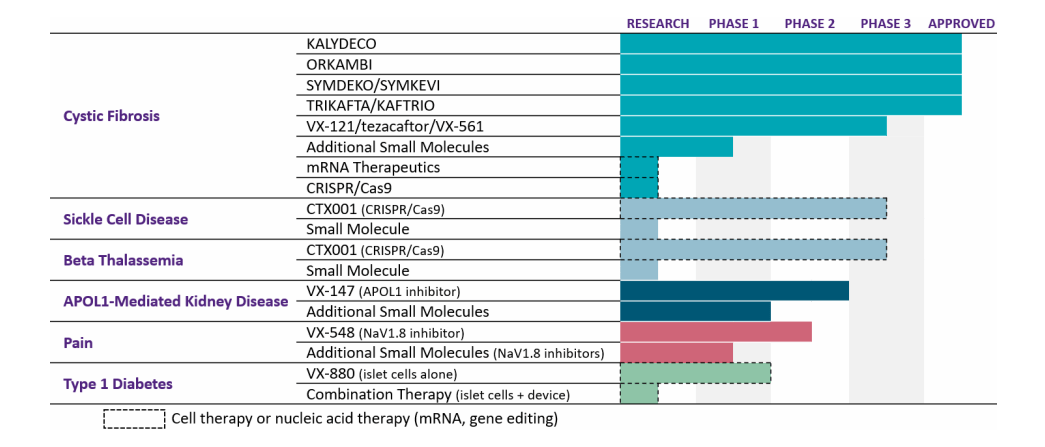

The company has a range of commercial opportunities in the near future, including treatments for sickle cell disease and beta thalassemia with Exa-cel, acute pain with VX-548, and cystic fibrosis with a vanzacaftor triple combination.

Vertex’s research and development efforts have been productive in six disease areas outside of cystic fibrosis, with positive results in five of the programs in Phase 2 development. These include treatments for sickle cell disease and beta thalassemia, acute pain, APOL1-mediated kidney disease, and type 1 diabetes. Vertex also has Phase 2 studies underway for treatments in neuropathic pain and alpha-1 antitrypsin deficiency.

In total, there are eight programs in mid to late stage development with a high chance of success, each offering the potential for a transformative medicine and a multibillion-dollar market. Vertex’s objective is to bring new products to five disease areas within the next five years.

Cystic Fibrosis

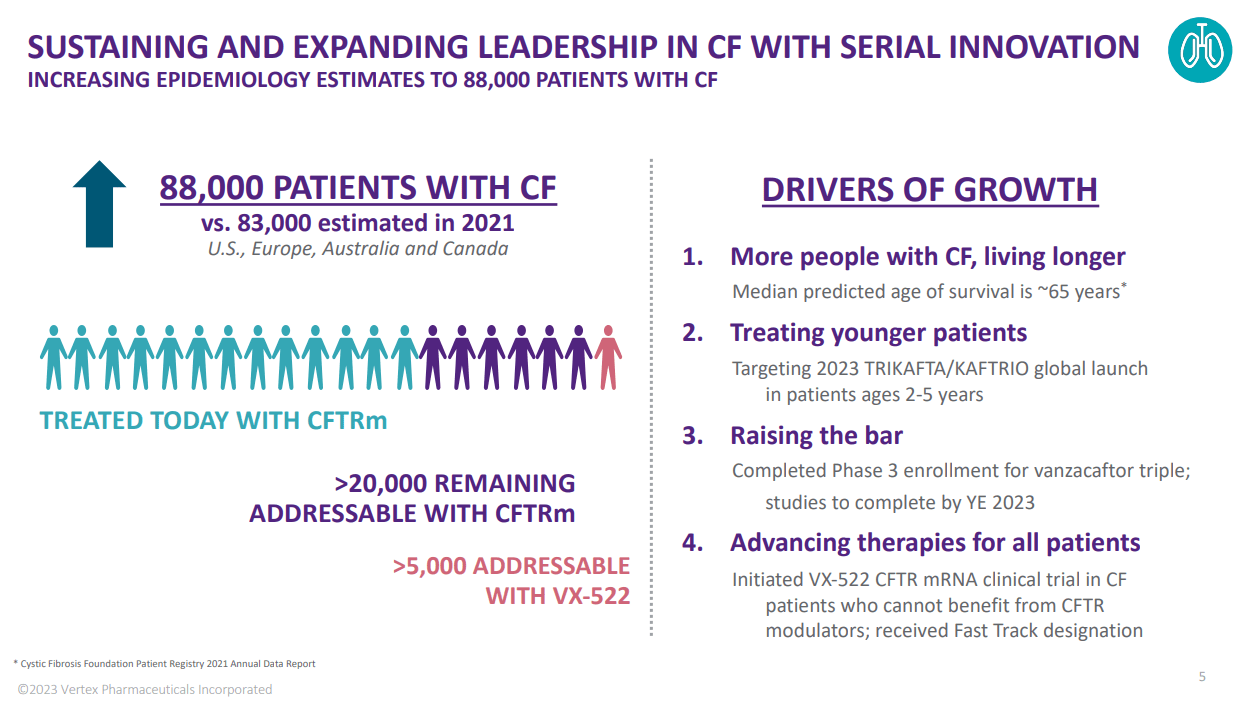

The growth of the cystic fibrosis patient population and longer life expectancy are major reasons for investment in the CF program. The company’s goal is to provide CFTR modulator therapy to all eligible patients.

To achieve this, the company has submitted a CFTR modulator for 2-5 year olds for priority review by the FDA and the next phase 3 study is expected to be completed by the end of the year. Additionally, the company is working on developing advanced treatments, including a mRNA approach (VX-522) in partnership with Moderna (MRNA) that has been cleared for clinical trials and granted Fast Track designation by the FDA.

Vertex Pharmaceuticals

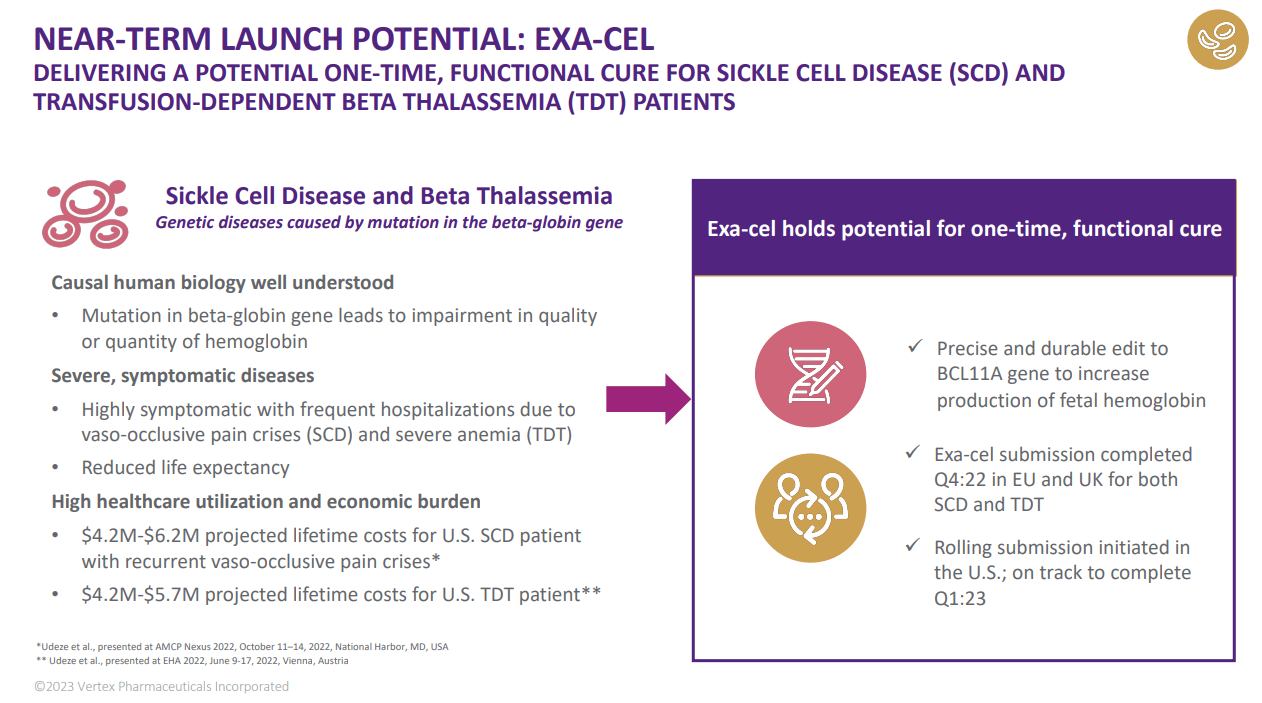

Exa-cel (CRISPR Therapeutics CTX-001)

Exa-cel is a gene therapy for sickle cell disease and beta thalassemia that utilizes the CRISPR/Cas9 gene editing method. The therapy involves removing a patient’s own cells, editing them to correct the genetic mutations that cause the diseases, and then transfusing them back into the patient. Exa-cel is being developed as a potentially one-time functional cure that could have significant clinical benefits and cost savings, as the lifetime costs of sickle cell disease are estimated to be between $4 million and $6 million.

The company is preparing for its commercial launch, with teams in place and infrastructure in place to support patients and physicians. The initial launch will target the 32,000 most severe sickle cell and beta thalassemia patients and will be available through authorized treatment centers in the US and EU. The company is also working with payers and policymakers to ensure that patients have access to and reimbursement for the therapy once it is approved.

Vertex Pharmaceuticals

Acute pain management

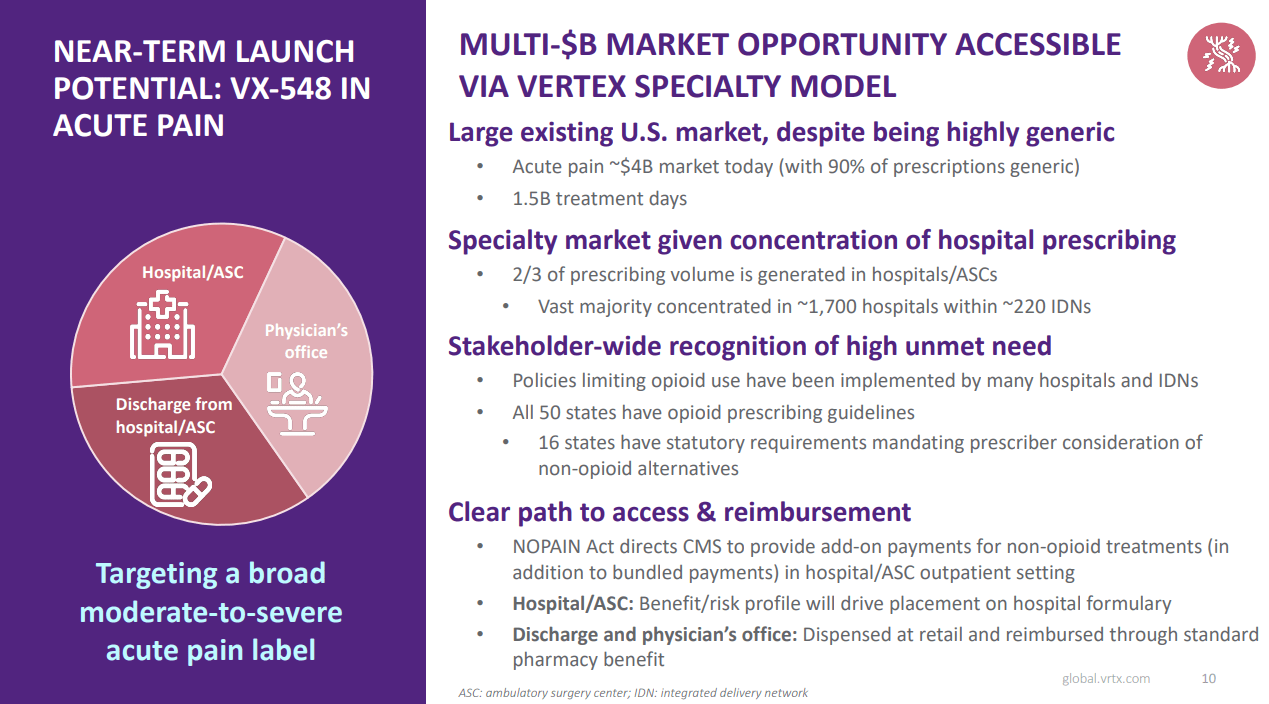

VX-548 is a potential new class of medicine for the management of acute pain that works by blocking pain signals in the peripheral nerves, which could provide effective pain relief without abuse potential. It has shown strong efficacy in Phase 2 studies, with a favorable benefit-risk profile and no abuse potential. It has been granted fast track and breakthrough therapy designation by the FDA, recognizing the high unmet need and its compelling clinical profile.

The current standard of care for acute pain is limited by the limitations of NSAIDs and acetaminophen and the side effects and abuse potential of opioids, creating a gap in this treatment segment. VX-548 has the potential to fill this gap, with a market size of $4 billion in the US and 1.5 billion treatment days annually.

Two-thirds of acute pain medicine prescriptions are driven by hospital or institutional prescribing. Almost all institutions and states have guidelines in place regarding opioid prescriptions and the NOPAIN Act, which directs CMS to make a separate payment for non-opioid medicines. This new law is part of the growing movement to utilize non-opioid treatments, and VX-548 has the potential to be a near-term effective non-opioid treatment option that can be approached with a specialty sales force.

Vertex Pharmaceuticals

APOL1-mediated kidney disease (AMKD)

APOL1-mediated kidney disease refers to a group of kidney disorders caused by specific genetic variations in the APOL1 gene. This gene provides instructions to make a protein that plays a role in fighting certain parasites and bacteria. Some APOL1 variants increase the risk of developing kidney disease, including chronic kidney disease (CKD) and nephropathy. The disease is characterized by progressive loss of kidney function, which can lead to kidney failure and the need for dialysis or transplantation.

Inaxaplin or VX-147 has the potential to treat APOL1-mediated kidney disease (AMKD), a genetic disease that affects about 100,000 people in the U.S. and EU and has no approved treatments. A Phase 2 study demonstrated a 47.6% reduction in protein in the urine, and the company is now in a Phase 2/3 trial with a pathway for accelerated approval.

Type 1 Diabetes

The company’s diabetes program for Type 1 diabetes is based on VX-880 cells, which have shown improvements in key metrics. One patient who received half the target dose even achieved complete elimination of exogenous insulin. The VX-880 program is currently in Part B of its study and is fully enrolled, with more results expected to be released this year. The company is also developing a similar program using VX-880 cells cloaked to evade the immune system, called the VX-264 program, which has filed Clinical Trial Applications in Canada and the US. The trial is expected to begin enrolling patients in Canada soon.

Financials

The company already has an interesting money generating pipeline:

Vertex Pharmaceuticals

Yes, the bulk of the company’s portfolio remains unapproved, which adds to the excitement of its prospects. By leveraging the cash flows from established revenue streams, the firm is effectively purchasing a growth call option. Should one or two of these programs prove successful, it will further enhance the firm’s cash flow generation capabilities. For the time being, let’s focus on the current state of the income statement:

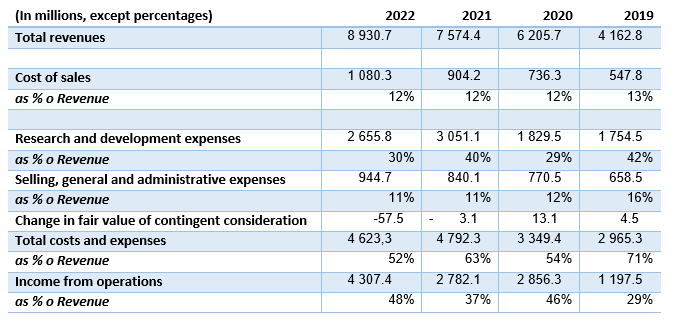

Author’s calculations based on Vertex Financials

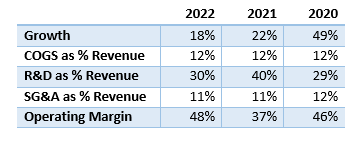

The revenue growth was approximately 18% in the year 2022. While this growth rate is commendable, it has gradually declined in recent years. The cost structure appears to be efficiently managed, exhibiting leanness:

Author’s calculations based on company financials

The cost of goods sold (COGS) and selling, general, and administrative (SG&A) expenses exhibit stability and are relatively low in comparison to revenue. Research and development (R&D) expenses tend to fluctuate and make a greater impact on the cost structure, which is expected given the company’s pipeline. The operating margins are impressive and indicate a business model with resiliency and a capacity for continued cash flow generation.

The current ratio, now just below 5, provides a strong cushion to handle any potential challenges and allows for continued investment in the pipeline. The company’s debt is minimal, mostly composed of leases.

Risks

It is important to note that the company faces several risks. I will highlight the most significant risks as perceived by me, but it is ultimately up to individual investors to thoroughly assess and determine their comfort with the uncertainty involved.

The company faces commercialization risks, including the possibility of unsuccessful commercialization of therapies, safety and compliance concerns, difficulty in gaining acceptance, coverage challenges, and competition. Additionally, the company is exposed to risks related to product development and clinical testing, including delays in regulatory approval and prolonged clinical trials and challenges in developing cell and genetic therapies. Currently, there is no commercially approved CRISPR therapy, and there may never be one.

The company heavily relies on collaborations and acquisitions to bring new products to market and executing these effectively may prove to be challenging. Issues arising from drug development could harm the company’s reputation and have a wide range of negative consequences.

Valuation

Vertex boasts a formidable commercial portfolio, featuring treatments for the debilitating disease of cystic fibrosis. The firm currently markets four highly successful medicines – TRIKAFTA/KAFTRIO, SYMDEKO/SYMKEVI, ORKAMBI, and KALYDECO – which generate a steady stream of cash flow.

Moreover, Vertex’s pipeline is a testament to the company’s innovative spirit, featuring a diverse range of cutting-edge technologies such as mRNA, cell therapy, gene editing, and small molecules. A full 40% of the pipeline stems from internal innovation, a remarkable feat in an industry that often relies heavily on external sources.

With an eye on the future, Vertex is committed to advancing its pipeline and launching five new treatments in the next five years. This ambitious goal is made possible by the firm’s strong financial footing, with a healthy cash reserve that sets it apart from many biotech firms struggling to raise funds.

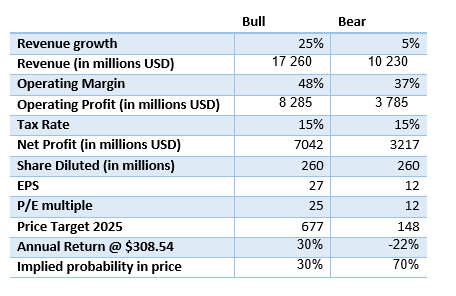

A bull and bear scenario analysis presents an insightful view into the potential value of this company by 2025. The bull scenario assumes growth of 25% and an operating margin of 48%, while the bear scenario envisions slower growth, 5%, with an operating margin of 37%.

Author’s calculations

The findings from this model highlight the unequal balance between risk and reward in this company’s profile, given the presence of several promising products in the pipeline for the coming years.

Be the first to comment